GMRE - Global Medical REIT: A Strong Buy At Attractive Valuations And 7.8% Dividend Yield

Summary

- GMRE's business model operates on a net-lease structure focusing on properties that are predominantly medical offices and facilities operated by established healthcare systems providing essential care in local communities.

- GMRE is attractively priced at just 11.5x forward P/FFO and 11.6x TTM P/FFO, with a TTM dividend yield of 7.8%.

- We believe that overwhelming pessimism towards the economy and the real estate sector is overblown and that GMRE's profitability estimates will eventually be upgraded to reflect the realities of a milder-than-expected recession.

- Due to GMRE's highly selective and targeted approach to concentrating on community healthcare facilities, its business model is highly resilient to economic downturns and insulated from competition.

- We initiate coverage of Global Medical REIT (GMRE) with a "Strong Buy" rating.

Increasingly favourable odds for a U.S. economic "soft landing" supported by evidence of cooling inflation and a less hawkish Federal Reserve, are beginning to lift investor sentiment lately. Some of the biggest beneficiaries of this rebound in sentiment are value stocks, many of which have enjoyed strong double-digit gains since the market bottomed in October 2022.

Real estate names that we currently cover have significantly outperformed in recent weeks and look set to be the best-performing assets in our portfolio for 2023. Our favourite picks include Blackstone ( BX ) which we initiated coverage in our January 5 article and D.R. Horton ( DHI ) which we initiated coverage in our October 18 article . We continue to maintain a "Strong Buy" rating on both.

In this article, we highlight why we are adding the small-cap Global Medical REIT ( GMRE ) to our list of favourite real estate picks and initiating coverage of this REIT with a "Strong Buy" rating.

Our set of criteria for identifying potential outperformers are deceptively simple: attractive valuations, profitable and resilient business models, reasonable growth, competitive advantages that limit direct competition, and pessimistic sentiment. In the following sections, we will discuss how well GMRE satisfies each of our criteria and how this REIT presents an attractive opportunity that we think will add value to our portfolio's performance.

Attractive Valuations With Room For Growth

Admittedly, we are late to the party in identifying GMRE as a great value pick. At the time of writing, GMRE is already sitting on a spectacular gain of 49% from its $7.14 close on 12 October 2022.

For most investors, we can imagine how emotionally distressing it would be to be recommended a stock that had already risen by 49%. But from an objective standpoint, being late to the party doesn't mean that we should give up on a stock with the potential to outperform and deliver more gains. Indeed, if we compare GMRE's current price of $10.69 at the time of writing to its $17.83 close on 3 January 2022, GMRE is still trading at 40% below its peak.

{kind=link}

Standard valuation metrics indicate there is ample room for GMRE to outperform. The REIT is currently priced at just 11.5x forward P/FFO and 11.6x TTM P/FFO, with a TTM dividend yield of 7.8% and a 4-year average dividend yield of 6.6%.

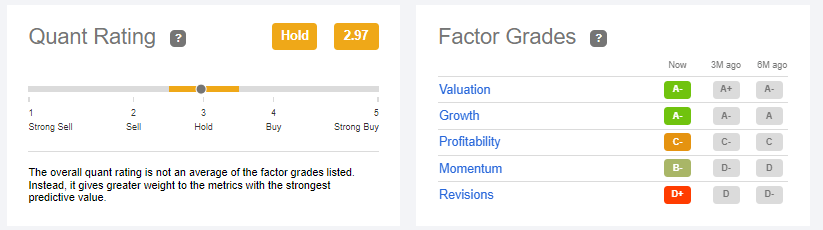

Seeking Alpha's proprietary Factor Grades currently assign an "A-" grade for both valuation and growth factors for GMRE, which satisfies our valuation and growth criteria for identifying outperformers.

{kind=link}

Although Seeking Alpha's Quant Rating currently rates GMRE as a "Hold", we note that this is mainly due to previous downward revisions in EPS and revenue estimates, which are backwards-looking.

This is an important point and is exactly what we look for based on our criteria for pessimistic sentiment. We believe that overwhelming pessimism towards the economy and the real estate sector is overblown and that as GMRE emerges from the current economic slowdown, profitability estimates will need to be revised and upgraded to reflect the realities of a milder-than-expected recession. This reversal in bearish sentiment will play a key role in driving GMRE's outperformance in 2023.

Resilient Business Model, And Limited Competition

Healthcare has become an increasingly popular long-term investment theme driven by major factors including an ageing baby boomer generation, increasing demand for quality healthcare, and a growing preference to age comfortably within one's community independently without having to rely on costly institutional care.

GMRE's business model operates on a net-lease structure focusing on properties that are predominantly medical offices and facilities operated by established healthcare systems providing essential care in local communities.

Due to GMRE's highly selective and targeted approach to concentrating on community healthcare facilities, its business model is highly resilient to economic downturns and insulated from competition. Whenever GMRE acquires a purpose-built property and leases it to a major healthcare operator in a local community, it effectively enjoys a monopoly in that area for the life of the lease. And according to GMRE's latest investor presentation deck published in November 2022, the weighted average lease term of its portfolio of properties was 6.4 years.

Furthermore, because population densities in local communities are much lower compared to the big cities, it makes little sense for competitors to set up new facilities in the community to engage in direct competition with GMRE. GMRE's assets are generally low-risk in nature since it focuses on properties that provide essential healthcare. 68% of GMRE's net leasable area consists of medical office buildings and 17% is leased to inpatient rehabilitation facilities. That means its portfolio of properties also enjoys stable occupancy rates that were last reported at 97% in September 2022 .

Perhaps investors may think that surely by pursuing a safe and stable business model GMRE would have to sacrifice growth and profitability. Of course, we shouldn't expect GMRE to produce growth rates that we see in the high-growth-high-failure world of the biotech industry. But GMRE has nonetheless grown its portfolio of assets by 56% since its IPO, with a weighted average capitalization rate of 7.7% .

{kind=link}

To be fair, GMRE is a small-cap REIT with a market capitalization of US$722 million. Thus there is nothing special about the REIT being able to grow its assets at such a blistering pace. Being small, however, also means there is a long runway for growth and management seems keen on making new acquisitions when the economic environment eventually improves. The only real benefit that a small-cap REIT like GMRE is missing out on, is the flexibility to make deals and occasionally sell assets when prices are favourable, which also provides an added boost to income.

Insulated From Higher Borrowing Costs

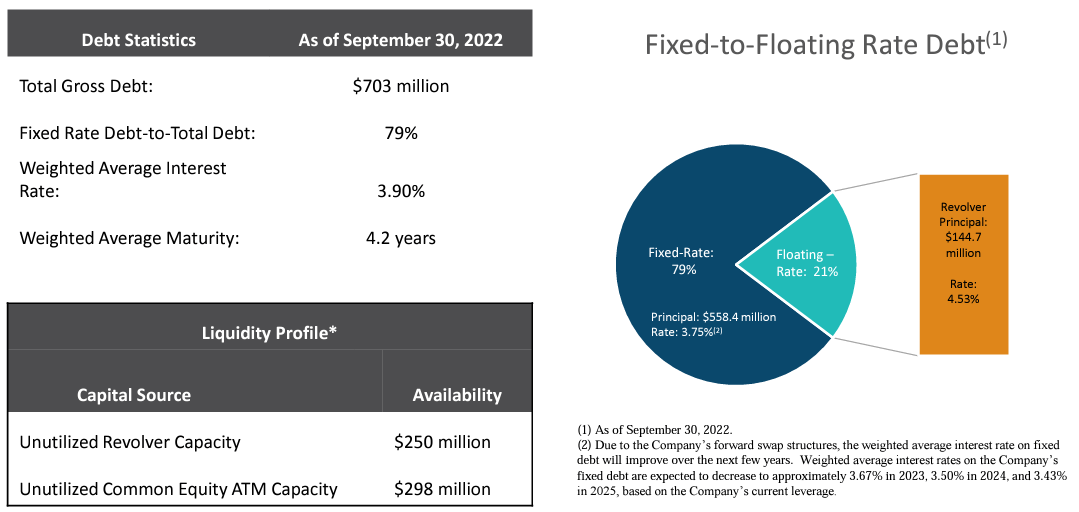

We believe one of the main reasons investors have remained stubbornly pessimistic and risk-averse to the real estate sector is due to fears over higher interest rates, which usually mean that companies that rely on borrowing are likely to be subjected to higher borrowing costs. However, GMRE's debts are mostly fixed rate and we see this as a major advantage for the REIT.

As the accompanying figure shows, around 79% of GMRE's existing debt is fixed rate with a weighted average interest rate of just 3.9% as of 30 September 2022. Meanwhile, the remaining 21% of its floating-rate debt is being financed at a manageable rate of 4.5%. According to management, GMRE also has existing forward swap structures in place that would further improve the weighted average interest rate on its fixed-rate debt in the next few years, essentially insulating the REIT from the threat of high borrowing costs over the medium term.

{kind=link}

Staying Invested Over Market Timing

Having outlined our bullish view on GMRE, we think it might be worthwhile to briefly discuss our broader view on the equity market and how we view GMRE as part of our much broader portfolio strategy for 2023 and 2024.

We continue to see attractive investment opportunities within real estate and expect our favourite picks to continue to outperform over the medium term. Our view, however, is nonetheless subjected to swings in market sentiment. Thus, while we believe that the U.S. economy will only see a mild recession in 2023, investors should expect the occasional bumps and a good dose of market volatility along the way.

Real estate is one of our favourite investment themes right now due to a combination of depressed valuations, pessimistic sentiment, resilient balance sheets, and the prospect of a relatively mild and manageable recession. Great real estate investment opportunities are hard to come by and we have not seen valuations being so attractive since the global financial crisis in 2008-2009. More importantly, we see no evidence that the current economic downturn will even come close to being as disastrous as that of 2008.

As proponents of long-term investing, we urge investors to ignore the short-term volatility that inevitably resurfaces from time to time and to stay invested at least over the next 12-24 months, by which we expect valuations on these names to have fully recovered to pre-pandemic levels.

Sure, we may consider trimming our positions from time to time to take some profit whenever we see strong 30%-40% rallies hereafter, but we remain committed to staying invested with the intent to buy on dips over the next 12-24 months.

So long valuations are attractive, don't sell in anticipation of minor pullbacks. Sell when big sustained rallies lose momentum, and then get ready to buy on the dips.

In Conclusion

GMRE satisfies our criteria for identifying potential outperformers, and we like the REIT's highly selective and targeted approach to concentrating on community healthcare facilities.

GMRE is attractively priced at just 11.5x forward P/FFO and 11.6x TTM P/FFO, with a TTM dividend yield of 7.8%.

We initiate coverage of Global Medical REIT with a "Strong Buy" rating.

For further details see:

Global Medical REIT: A Strong Buy At Attractive Valuations And 7.8% Dividend Yield