HR - Global Medical REIT Enters Deep Value Territory But Doesn't Belong

2023-05-09 14:56:41 ET

Summary

- GMRE has gotten far too cheap.

- Rent growth has kept up with interest rate increases to keep FFO strong.

- Management has elected to slow external growth until spreads make sense.

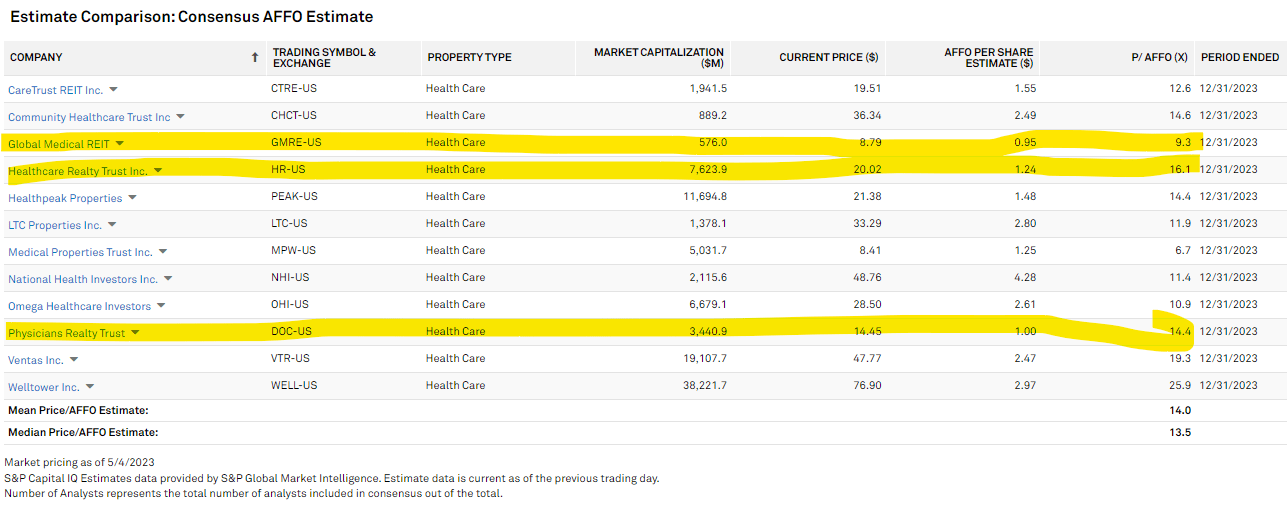

Deep value is a section of the investment universe that trades at extremely low multiples or massive discounts to asset value. Global Medical REIT ( GMRE ) fits both of those categories with a P/AFFO multiple of 9.8X and price to Net Asset Value ((NAV)) of 73%. It also boasts a 9.25% dividend yield which is also characteristic of the space.

In an efficient market, a stock’s fundamental characteristic would match its valuation. There are plenty of reasons why a stock could legitimately trade in this deep value range where it would be a fair deal for investors.

- Secular decline

- Bad management

- Extreme leverage

- No growth prospects on a long-term basis

- Competitive disadvantage

The list could go on, but the idea is that the upside that comes with the extreme value is balanced out by a risk of similar magnitude. Thus, on a scenario weighted basis, the expected return would be in line with the equity market.

In the absence of such problems, a stock trading at deep value is set up to substantially outperform. The cashflow yield alone is market beating, so really valuations this low only make sense if the long term trajectory is negative growth.

I wanted to discuss this background on deep value as a context for GMRE as I think it clearly does not belong at this level of valuation. Let us go through each of the six problems bulleted above to show that GMRE is not your typical deep value play.

Secular stability

Medical office as a sector has steady demand that even seems to persist through economic downturns. Peer medical office REITs Healthcare Realty Trust ( HR ) and Physicians Realty Trust ( DOC ) trade at 16.1X and 14.4X 2023 AFFO, respectively.

{kind=link}

These are multiples that are roughly in-line with the market and do not imply that the sector trades at a discount. Only GMRE trades at a deep value multiple within the MOB sector.

Well-aligned management

Small REITs are often confronted with the problem of being subscale such that overhead costs eat up too high a percentage of revenues. There are two ways to combat this challenge:

- Growing to a sufficient size

- Running lean

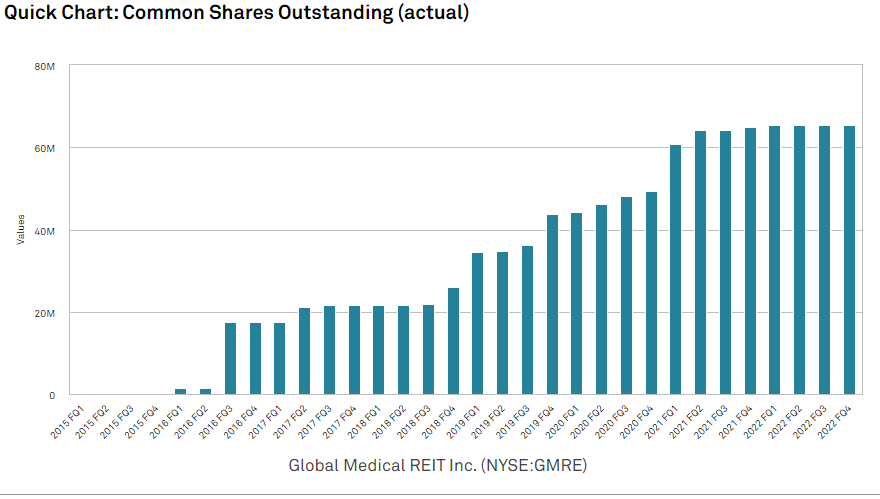

GMRE has successfully employed both methods. It has issued quite a bit of equity.

{kind=link}

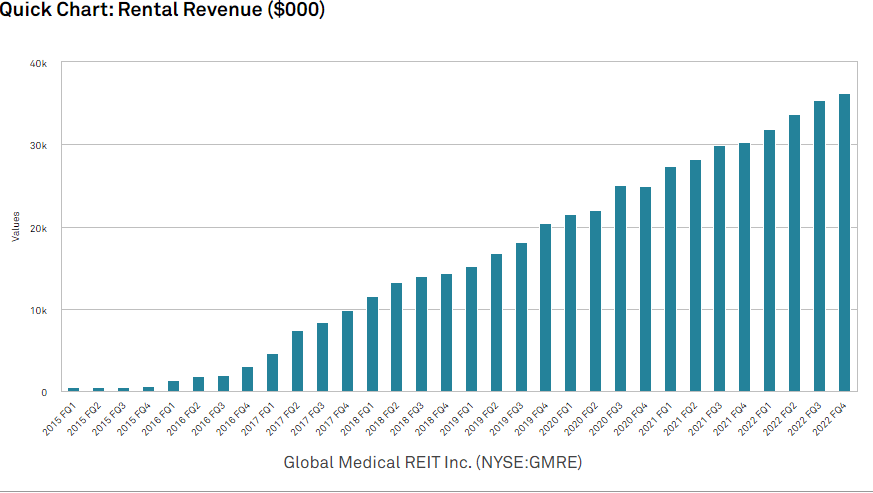

The raised funds were put directly into acquisitions such that revenue grew at a greater pace than share count.

{kind=link}

These were targeted high cap rate acquisitions with IRRs that exceeded GMRE’s cost of capital. As such, it was accretive on a per share basis despite the equity issuance.

{kind=link}

The present environment is putting management teams to the test with cap rates remaining stubbornly low despite cost of both debt and equity rising dramatically.

Bad management would just keep growing, but GMRE recognizes the spreads and knows growth for the sake of growth would not be accretive to shareholders. This is evident from an exchange on the 1Q23 earnings call

Robert Chapman Stevenson Janney Montgomery Scott LLC:

"Just a follow-up. Jeff or Alfonzo, is that -- that 7.5%, 8%, is that where you guys would be seeing acquisitions these days? Is that where the cap rate is on the quality assets that you guys would be buying in the market today, if you were?"

Jeffery M. Busch Chairman, President & CEO :

"I'll first answer. Our cost of capital is too high right now. We have to be accretive. I've always said we have to be some level of accretiveness. So right now, it would be hard for us to buy 7.5 to 8. Unless it's OP units and unless -- like the last year, they took the OP units at a premium."

Instead, management is going lean with declining G&A and accretive asset sales. Note below that G&A run rate dropped to $3.8 million from $4.2 million in the prior year period.

{kind=link}

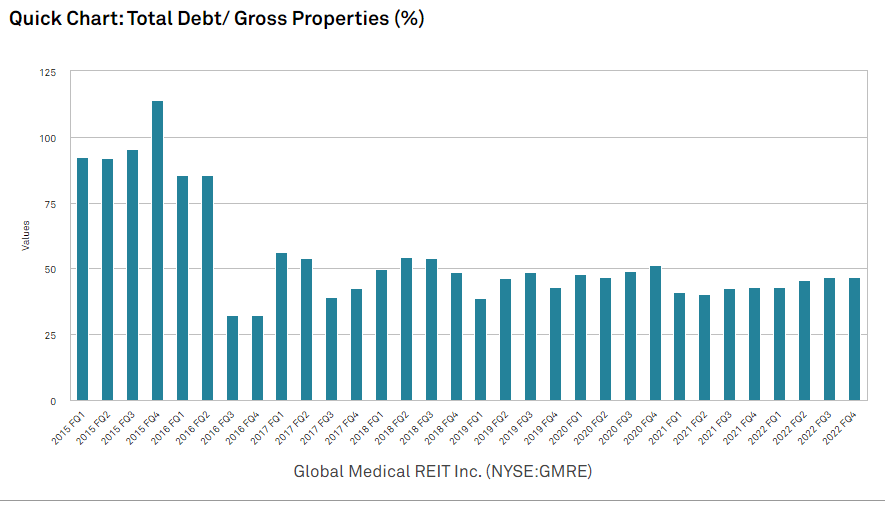

Reasonable leverage

There have been times in GMRE’s history in which it traded at a premium multiple. They used those times to fund acquisitions primarily with equity which resulted in debt to total assets dropping significantly.

{kind=link}

It stands today in the mid 40s which is a reasonable level, but GMRE has plans to further reduce leverage through asset sales.

Roughly $90 million of assets slated to be sold are in various stages and most with LOIs. These sales are happening at cap rates around 6%-6.5% with one of the sales in the 5s.

That sales cap rate is almost identical to the cost of debt GMRE is paying down which makes it debt reduction that doesn’t hurt AFFO/share. That is a rare opportunity and I really like seeing GMRE take advantage of spreads being out of whack.

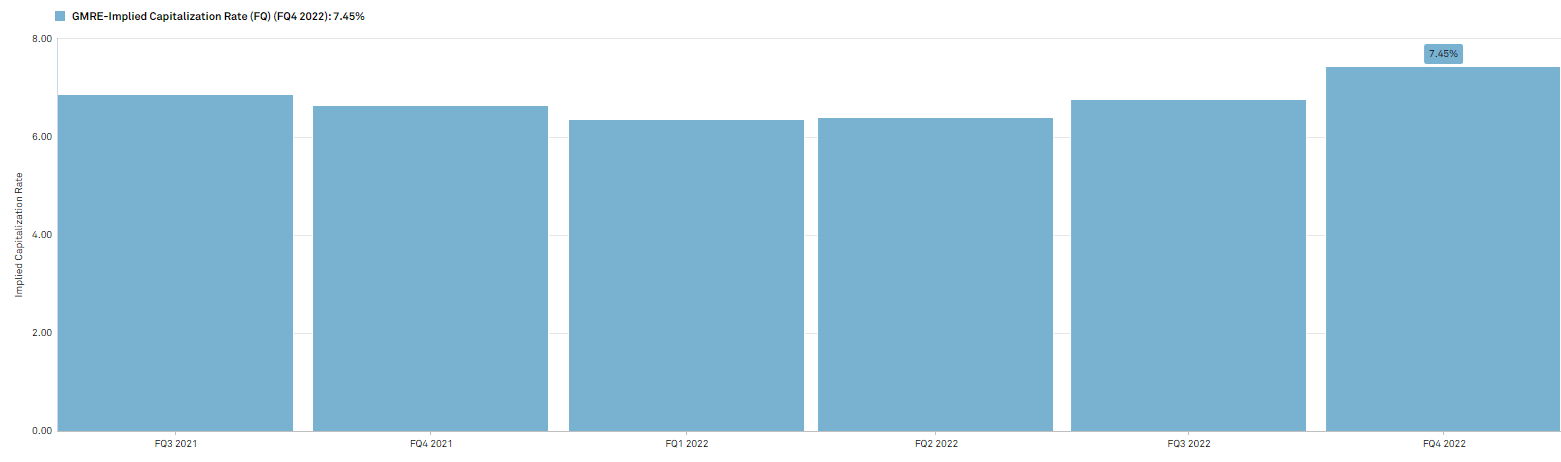

See, in the private market, medical office is a well-liked asset class and still transacts at cap rates in the low 6s. GMRE’s stock however, is trading at an implied cap rate of 7.45%.

{kind=link}

This disconnect makes any asset sale extremely accretive to investors because proceeds can either pay down expensive debt or buyback stock, each of which improves shareholder value.

Given GMRE’s market cap below $1B I agree with the paydown of debt taking precedence over buybacks.

Organic growth hidden by interest rates

The market reacted rather harshly to GMRE’s 1Q23 earnings report.

{kind=link}

I thought the report was fantastic.

Perhaps the reason the market did not like it is that it had the appearance of negative growth.

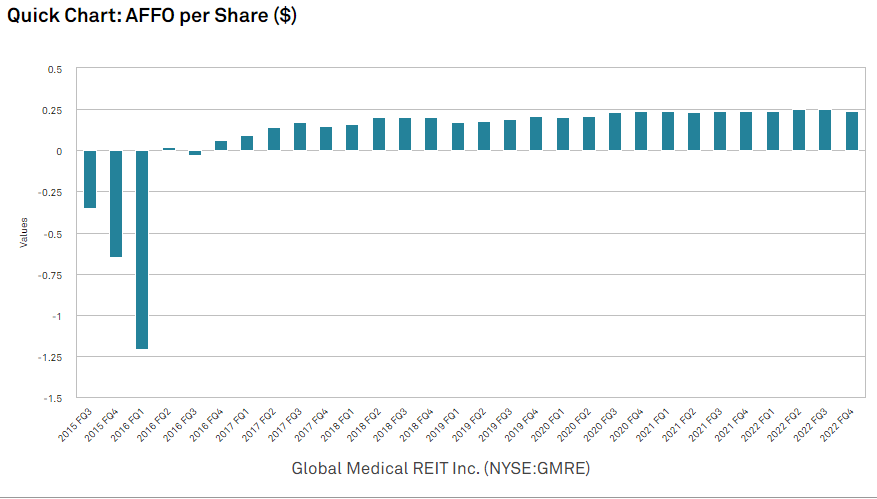

AFFO/share came in at $0.23 as compared to $0.24 a year ago. Prima facie, that is a bad look.

However, it is worth noting that the rapid rise in interest rates added $3.470 million to interest expense compared to the prior year quarter. That is $0.05 per share or $0.20 per share on an annualized basis.

Thus, the baseline AFFO GMRE would have generated in 1Q23 would have been $0.19 with exception to the organic growth they produced.

- Rents were rolled up.

- Vacant space was leased.

- Occupancy hit a local peak of 97%.

While I anticipate interest rates remaining high for a while, they are highly unlikely to climb further. In fact, the market consensus is a Fed cut in July. I think that is optimistic, but it does seem likely that we are at or very near the end of the hiking cycle.

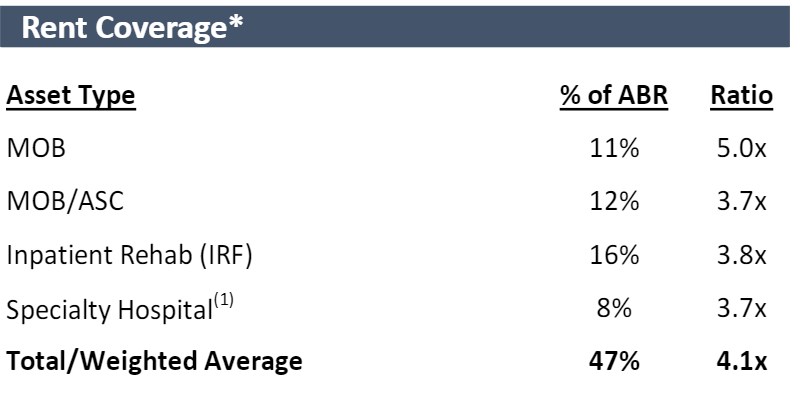

As such, interest expense should be flat to down going forward while the organic growth in GMRE’s revenues is likely to continue. Medical office is not like other types of healthcare that are struggling right now. Operators are highly profitable with GMRE’s average tenant having 4.1X EBITDARM coverage of rent.

{kind=link}

Most of GMRE’s leases have built in escalators. I anticipate AFFO/share growing even if interest rates remain high and growing rapidly if interest rates subside.

Competitive advantage

I really like REITs that have differentiated acquisition strategies. Highly marketed properties that go to the highest bidder are hard to make money on because whatever margin there is for the buyer gets competed down to a breakeven NPV.

GMRE circumvents the bidding wars by going after properties that require a bit more due diligence. Perhaps it is a weird location, or a shorter initial lease term. Something is keeping institutional buyers away, but the oddity is often not a bad thing.

It simply makes the property sale less competitive and allows GMRE to buy at 8% cap rates when more traditional properties are bought at 6%.

This cycle of asset sales which GMRE is currently executing is proving their business model. The properties they are now selling in the 6s were bought in the 8s. Since acquisition GMRE has re-leased the properties on much longer lease terms which makes them far more attractive to your standard institutional buyer. GMRE does the work and clips the spread as a result.

Fair value

GMRE has grown AFFO/share faster than peer MOB REITs. In my opinion, it has a superior business model. Over time I think it can begin to trade in line with peer multiples around 15X AFFO, but for now due to its still small size I think a slight discount is warranted.

In my opinion, fair value is about 14X AFFO or roughly $13 per share. This represents about 47% upside to today’s price.

The bottom line

GMRE is showing incredible resilience in tough times and a clear plan to grow during better times. It is a well-managed company and trading far too cheaply for its fundamental prospects.

For further details see:

Global Medical REIT Enters Deep Value Territory But Doesn't Belong