GNL - Global Medical REIT: Why We Are Lowering Our Price Target

Summary

- Global Medical REIT beat estimates for Q4-2022.

- They have managed their interest rate risk rather well and management is focused on value creation.

- We tell you what was negative about the quarter.

When we last covered Global Medical REIT Inc. ( GMRE ) we looked at the net asset value or NAV, and offered our estimate as to where that likely stood. We also gave it a buy rating and explained our rationale as to why we preferred it over Physicians Realty Trust ( DOC ).

GMRE's dividend yield is juicy and sustainable in our opinion. It also beats DOC's yield by 2%. While risks are obviously higher for a smaller REIT focusing on secondary markets, we do believe the strategy is worth pursuing and so far we have been impressed with management actions. We rate the shares a Buy with a $12.50 price target in two years.

Source: A Look At Where NAV Possibly Stands

The REIT has done ok since then with total returns matching that of the S&P 500.

Seeking Alpha

We examine the Q4-2022 numbers and tell you why we are reducing our price target.

Q4-2022

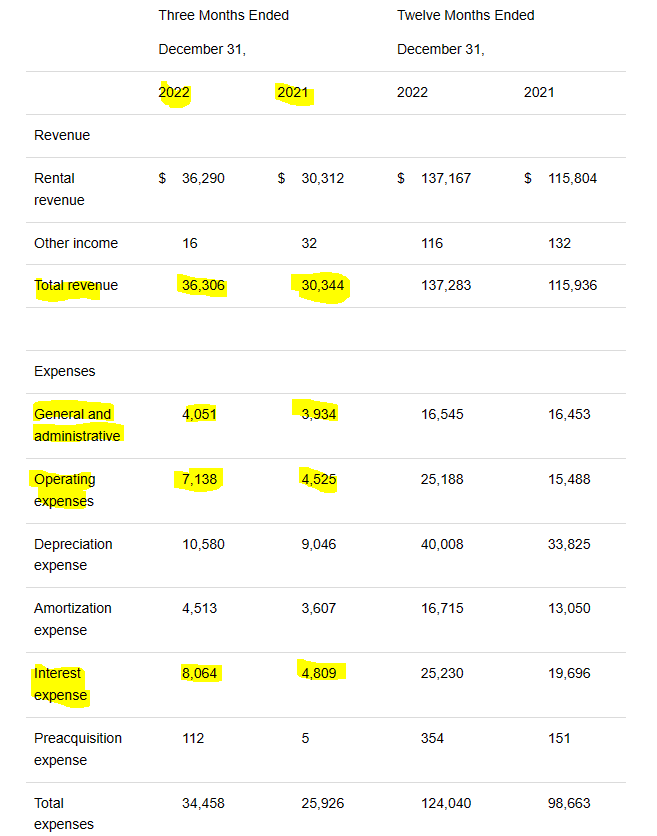

GMRE delivered a solid fourth quarter and the adjusted funds from operations (AFFO) number narrowly beat the 23 cents per share estimate. While the company did highlight the revenue growth of 19% year over year, the AFFO stood flat, thanks to expenses rising strongly as well. On that front, it was nice to see excellent cost control on the general and administrative front.

{kind=link}

GMRE Q4-2022 Press Release

That is the primary expense area where management has maximum control. It is also the one they need to control to show economies of scale. On the other hand, the operating expenses for properties were wild and rose at a 57% annualized clip in Q4-2022. Of course some was due to new properties, but exceeding the revenue run-rate by so much is going to neutralize any good from the previous line. While investors might pay attention to interest expense, they need to keep an eye on this. That brings us to the interest expense and it rose by 67% year over year. This was due to higher debt load as well as interest rates moving from 2.88% (2021) to 4.07% (2022) on the company's liabilities. With interest rates still rising into 2023, the variable component of GMRE's debt will continue to reprice higher. Interestingly, GMRE's fixed rate debt will benefit from its swaps and actually move lower during 2023, 2024 and 2025.

The Company’s fixed debt totaled $558.1 million on a gross basis at December 31, 2022, representing 79% of its total debt, with a weighted average interest rate of 3.75% based on the company’s interest rate swaps and at current leverage, with a weighted average maturity of 3.8 years. Due to the company’s forward swap structures, the weighted average interest rate on fixed debt is expected to improve over the next few years. Weighted average interest rates on the fixed debt are expected to decrease to approximately 3.67% in 2023, 3.50% in 2024, and 3.43% in 2025, based on the company’s current leverage.

Source: GMRE Q4-2022 Press Release

Outlook

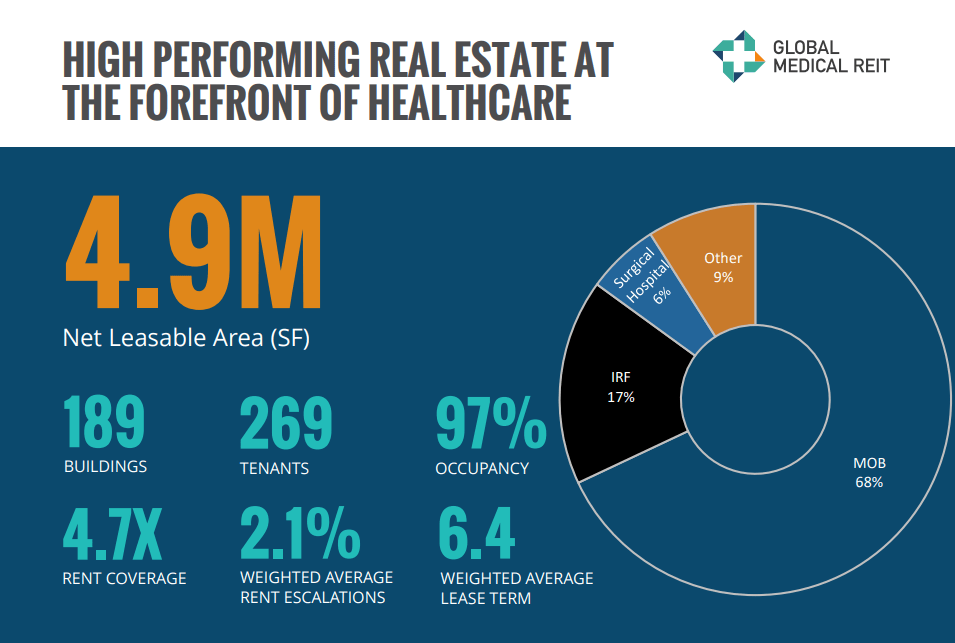

The primary reason to invest in GMRE is the quality tenants that generally have no issue paying rent on time. To that we will add that healthcare acts as a defensive asset class during recessions. Note that slides used below are from the November 2022 presentation, but very little has changed on this front in Q4-2022.

{kind=link}

GMRE November Presentation

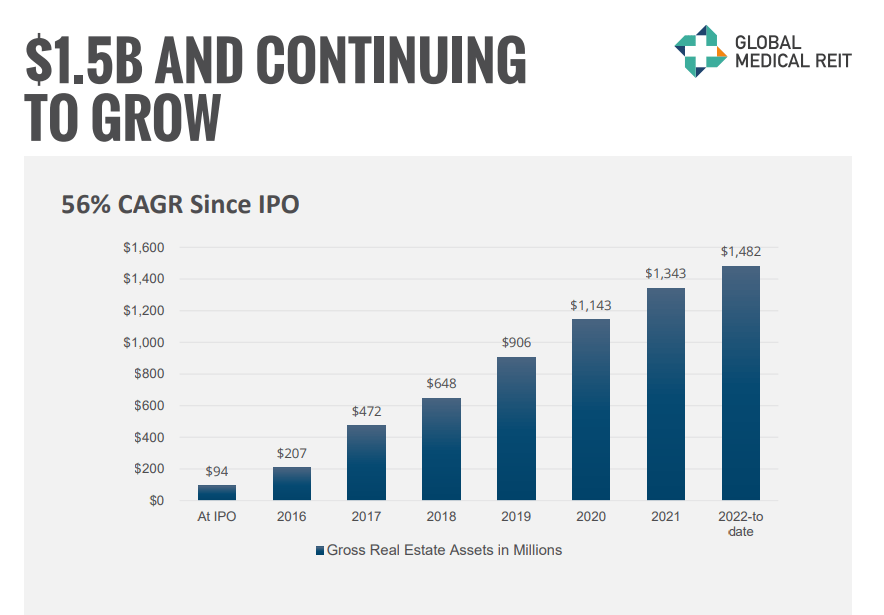

GMRE has also shown impressive growth from inception and investors are likely anticipating more.

{kind=link}

GMRE November Presentation

Unfortunately we don't see any growth in the near future for this REIT, at least anything that will meaningfully move the needle on their AFFO. The reason is that GMRE has been able to grow in the past, thanks to a stock that generally traded at a solid premium to NAV. It has also been able to grow as interest rates were low for that entire period. Today, the shares are trading near $10.25 and our earlier estimate of NAV near $12.00, still stands. The shares are trading a discount, albeit a small one. Management will likely confirm this as well and at least their actions, which show virtually no share issuance in 2022, backs this up. We are actually in firm agreement with them here and think that issuing shares at a discount to NAV should remain the domain of externally managed firms like ( GNL ) which want to grow without regard to shareholder value. Nonetheless, GMRE's route is blocked for share issuance. With risk free rates now over 5%, we doubt that GMRE can place new debt under 6.5%. So any acquisition with pure debt will add little juice if cap rates are around 7.5%. Finally, the firm is paying out 84 cents annually in dividends and the AFFO run rate is just slightly higher. Retained cash flow might add up to buy one small property annually. With higher interest rates and possible widening of cap rates, we think the stock will struggle to rise. We are lowering our 2-year target to $11.50 from $12.50. It still makes sense to hold from an income perspective but the volatility could get higher during a recession. On our existing positions, we took the opportunity on the ride up to sell the July $12.50 covered calls for 50 cents on February 2 .

Interactive Brokers February 2

This gave us another 9.3% of annualized yield over the yield of the stock. Since it fit with our price target objectives, there was really nothing to lose by getting called on the stock over $12.50.

Global Medical REIT Inc. 7.50% CUM PFD A ( GMRE.PA )

The preferred shares occupy an unusual position here. Long back we had suggested that in an era of low interest rates, GMRE.PA might work for those betting on higher rates. The rationale then was that these would not be redeemed if GMRE was faced with rising rate costs. At the same time the very high coupon would create a floor price (See, Global Medical REIT Preferred Might Be A Good Bet On Rising Rates ). At the present price $25.33, GMRE.PA offers an unexciting opportunity. The stripped yield is about 7.4% and we will note that the stripped yield in January 2022 was around 7.2%. Of course the Federal Funds rate is now 5% higher and is expected to climb 50-75 basis points more. We see the security as a bit overvalued although investors are likely focusing on the fact that the AFFO (calculated after deducting preferred dividends) is more than 10X the preferred dividend level. We therefore rate this security a hold.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Global Medical REIT: Why We Are Lowering Our Price Target