GNL - Global Net Lease: 15.66% On Common Or 8.50% On Preferreds?

2024-01-18 04:14:01 ET

Summary

- Global Net Lease Inc. has underperformed even our modest expectations over the last two years.

- The company's previous external management and frequent stock issuances have been major concerns.

- We look at the newly internalized REIT and weigh the prospects of high yields on its different securities.

Our experience with Global Net Lease Inc. ( GNL ) was borderline pleasant. While we had grown accustomed to the repeatedly dilutive stock issuances and were not exactly fond of the external management that was in place, we still felt we could "harvest" money of this. The equation was high dividend, plus high call option premiums, plus a stock that basically goes down slowly, creates at least 10% plus total annual returns. That was the theory anyway. In practice, our two year love affair with this REIT produced 10% total (not annualized) returns, while the stock delivered a negative 21% in total returns over this time frame.

Conservative Income Portfolio

We review where this one stands with no more skin left in the game and tell you why the stock has underperformed even our modest expectations. We also go over why the preferreds make more sense, but the best security comes from the bonds.

Are We Done With Stock Issuances?

GNL's big issue for the longest time had been the external management and the model of growth in revenues over all other metrics. It was not uncommon for management to mention NAV that was 40-50% higher than the price and also issue stock at the same time. You can see that in the chart below and even disregarding the recent large acquisition of RTL, share count growth has come at every single point.

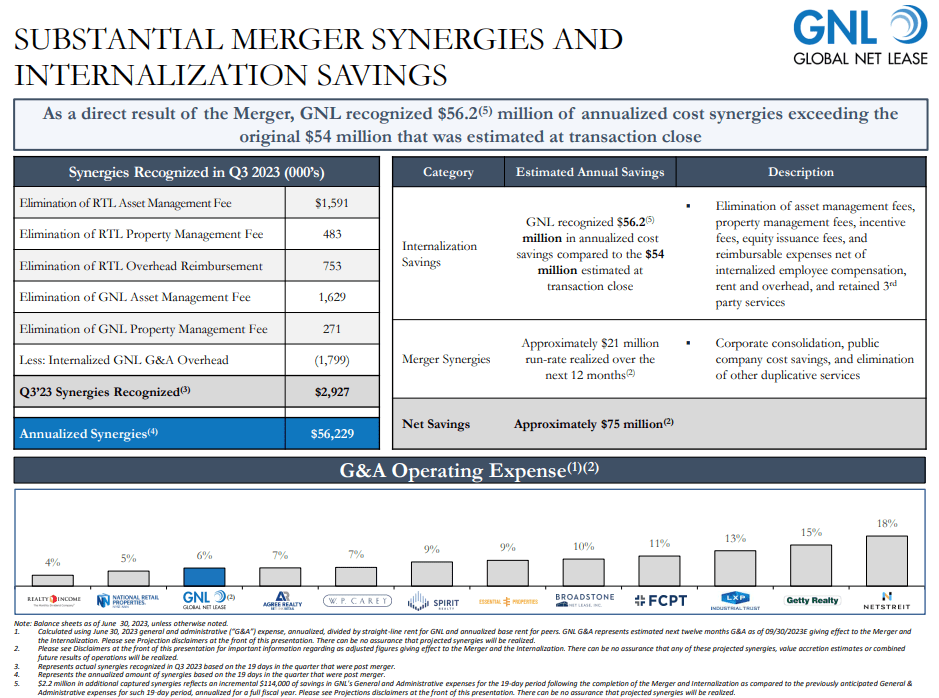

With RTL in the bag, GNL has talked about just how efficient things have become at the mothership.

{kind=link}

A lot of bullet points grace that slide and investors should read all of them, but that big albatross of external management is now gone. Dispositions were up on the list of things to do in the last 12 months and net debt to EBITDA has moved a smidge lower.

{kind=link}

Some of this was simply from assimilating in RTL, which was running a lower debt load compared to the standalone GNL. The key thing to watch will be whether management shows a true owner mentality and focuses on the long run. We will still see acquisitions for sure (more on the reason for that in the next section), but they are likely to be tempered.

{kind=link}

The Portfolio

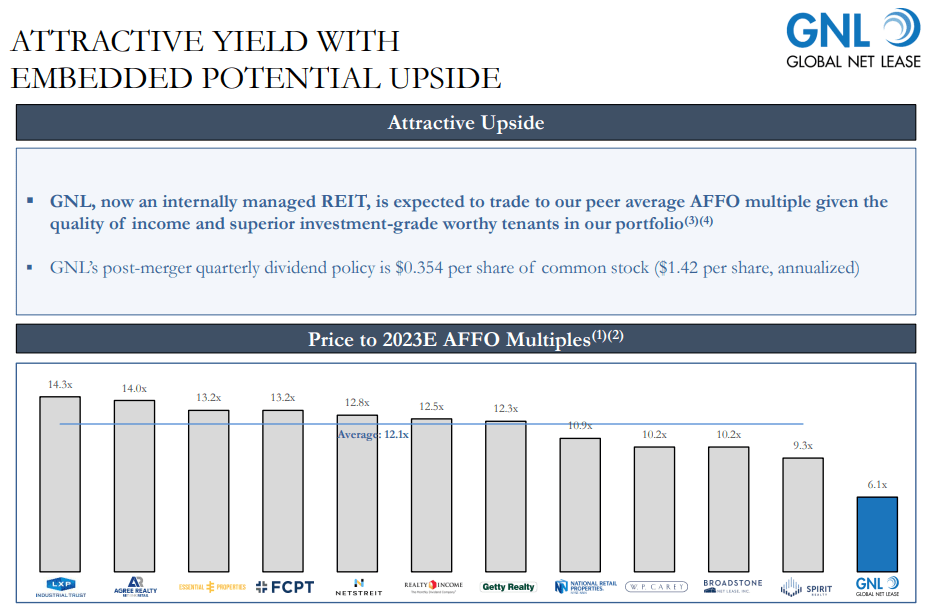

If we had a nice retail or industrial portfolio here, we would see the potential for a decent rerating. Note multiples are based on September 30, 2023 prices.

{kind=link}

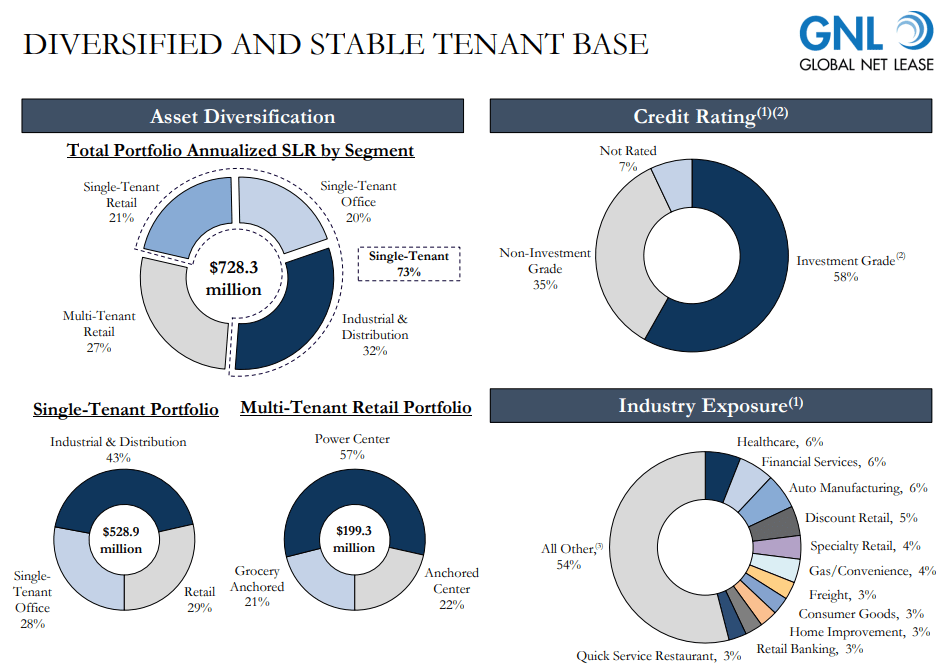

We could have seen the argument for it as well and we did give Spirit Capital Inc. ( SRC ) a straight buy rating when it was trading at 9X FFO. But the problem with those comparatives is the portfolio shown below.

{kind=link}

That single tenant office at 20% is not going to allow any multiple expansion. Realty Income ( O ) was happy to unload its single tenant office properties and Orion Office REIT Inc. ( ONL ) trades at near 4X funds from operations. Office Properties Income Trust ( OPI ) is trading near 1.0X trailing 12 month FFO and likely won't make it another 24 months if its bonds are remotely right. W. P. Carey ( WPC ) took the wrath of millions of shareholders rather than hang on to single tenant office properties. Can SRC methodically dispose and create value out of this? It will be tough. Lexington Industrial Trust ( LXP ), did manage to do it. But it was a painful journey and the stock still lags O, WPC and NNN REIT, Inc. ( NNN ), despite the ending multiple today being way higher.

Outlook & Verdict

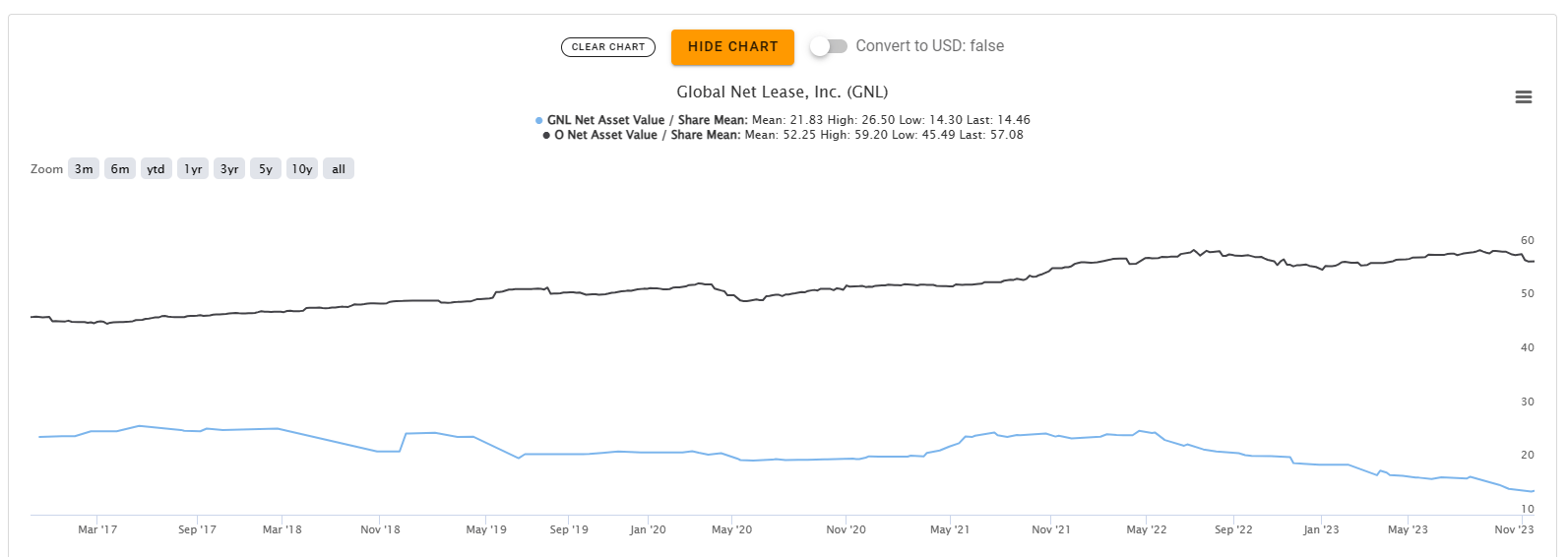

Over the last 8 years, GNL's NAV estimate has fallen by about 50%. Realty Income's is up about 20%.

{kind=link}

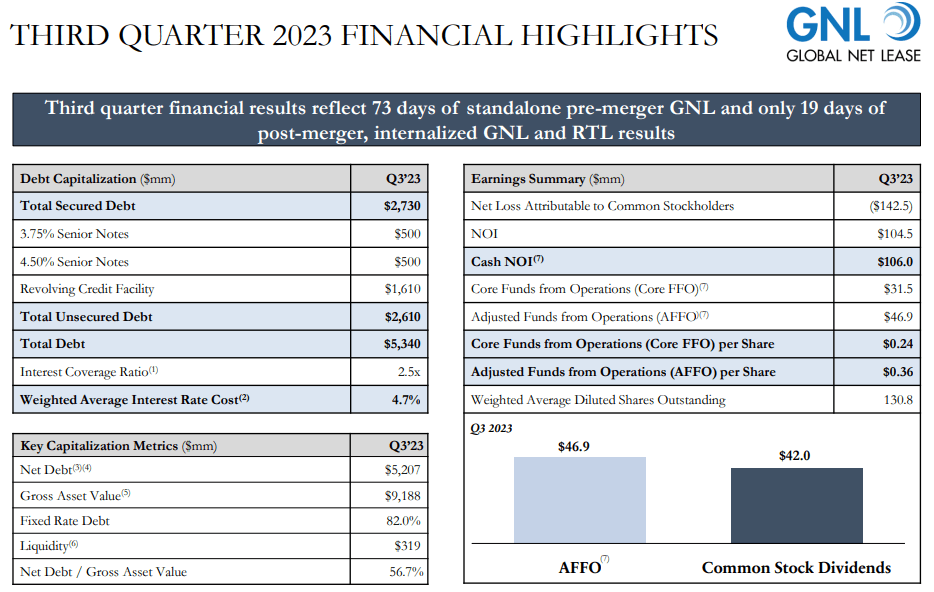

The current NAV estimate of $14.46 is probably way too optimistic, considering the single-tenant office exposure. On top of that, GNL is running an almost 8X debt to EBITDA multiple on the portfolio. Sure, half of it is secured debt, but it is still risky.

{kind=link}

With long weighted average leases in place, it is unlikely to be a death knell for the stock. You could also argue that it is highly probable that the company delivers more dividends than the stock price over time. None of that suggests that it might make a good investment. After all, investors are still underwater from IPO even accounting for dividends. We barely made money over the last two years and that was after a lot of call premium harvesting.

We still think this one is best avoided.

The Preferred Shares

GNL has a few preferred shares trading.

- Global Net Lease, 7.25% Series A Cumulative Redeemable Preferred Stock ( GNL.PR.A )

- Global Net Lease 6.875% Series B Cumulative Redeemable Perp Preferred Stock ( GNL.PR.B )

- Global Net Lease, Inc. 7.50% Series D Cumulative Red Perp Preferred Stock NYSE ( GNL.PR.D )

- GNL-E Global Net Lease, Inc. 7.375% Series E Cumulative Preferred Stock ( GNL.PR.E )

Two of these were "OGs" and two inherited from the RTL acquisition. They are all ranked the same. At present, they all sport very similar 8.5% yields with GNL.PR.A having the highest and GNL.PR.D the lowest. Some differentiation is expected as the market weighs potential probabilities of redemption in case we go back to ZIRP. Our take here is that the preferred yields are still on the low side for the relative risk here. Yes half that debt is secured against properties, but with the rate of value destruction that we have seen, we would not be exactly getting enthralled with an 8.5% yield.

GNL Q3-2023 Presentation

Now, they are still better than the common for sure. Those who went into the IPO for the preferred shares actually have positive total returns today versus the negative ones on the common. But at present, we need more yield to get interested.

Preferred Stock Trader who does all his fast trading for our service also hit the exits on the RTL bond recently . That said, if you really have to take an investment in GNL, the bonds are still the best relative bet. They are yielding about 8% to maturity right now on the 2027 notes and we think GNL should make it through that hump (the company, not the current dividend) with no issues. That is what we would focus on.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Global Net Lease: 15.66% On Common Or 8.50% On Preferreds?