GNL - Global Net Lease And Necessity Retail REIT Merger: The Real Winner Is GNL Preferred Stock

2023-06-08 08:15:00 ET

Summary

- Global Net Lease and The Necessity Retail REIT are merging in an all-stock deal, creating the fourth largest net lease REIT with 1,356 properties.

- The management of the combined REIT will be internalized, with current managers at AR Global resigning from other roles and becoming employees of the new GNL.

- The merger is expected to fix governance issues, lower operating expenses, and allow for further deleveraging and acquisitions over time.

- Greater portfolio size and lower operating expenses increase preferred stock dividend coverage.

Two net lease REITs that are currently externally managed by AR Global, Global Net Lease ( GNL ) and The Necessity Retail REIT ( RTL ), have announced that they are merging in an all-stock deal.

The combined entity will become the fourth largest net lease REIT with 1,356 properties.

What's more, in a major move, the management of the combined REIT will be internalized. Its current managers at external management company AR Global will resign from their other roles that do not pertain to GNL or RTL and become employees of the new GNL.

This should go a long way in aligning interests between management and shareholders. As GNL CEO Michael Weil mentioned on the related conference call, they are excited about the growth prospects of the combined REIT "not just in portfolio but in earnings and AFFO."

In case you are thinking that management are making this move out of the goodness of their hearts, solely in a good faith attempt to do right by their common stockholders, you might think again.

First, it is unlikely that this merger ever would have happened if not for activist investor Blackwells Capital, which took a stake in GNL in 2022 and began a proxy fight to take control of the board.

Second, though you might think that 100% of the post-merger GNL shareholders would be current GNL and RTL shareholders, you'd be wrong. Approximately 45% of the new GNL will be owned by current GNL shareholders, 39% by RTL shareholders, and 17% by "the owner of the former external manager or certain of its owners."

The new GNL is projected to own $9.6 billion in assets. So, the 17% of shares that management are granting themselves amounts to a little over $1.6 billion in assets. (On the other hand, this big chunk of free stock should help to align interests between management and shareholders after the merger is completed.)

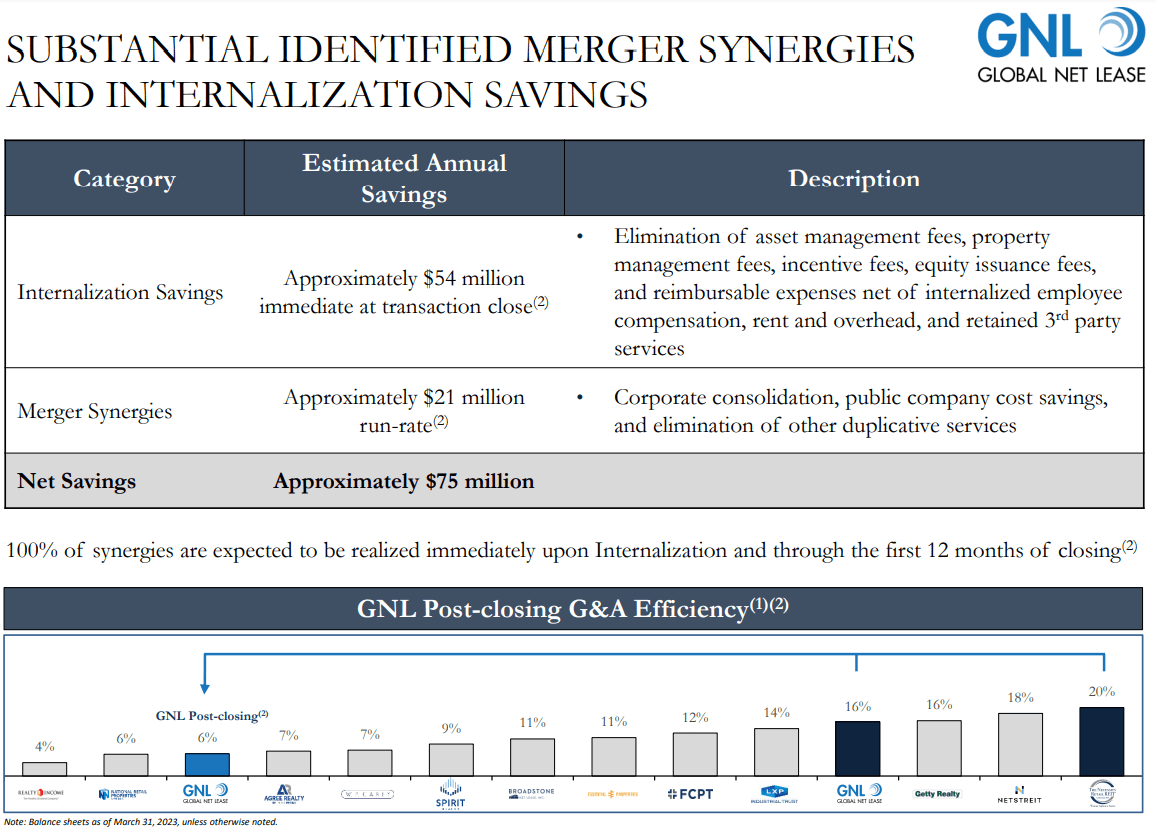

Plus, management is charging a one-time "internalization fee" of $325 million. If you consider that the combined REIT will boast about $75 million in annual synergies and cost savings, this internalization fee represents about 4.3 years of future cost savings from the merger.

That said, the deal is expected to fix many of the governance issues that have led, in part, to the poor stock price and AFFO per share performances of GNL and RTL over their histories. It is also expected to substantially lower operating expenses, as previously stated, which management says will allow further deleveraging and acquisitions over time.

{kind=link}

As you can see at the bottom of the image above, it is striking to me that GNL and RTL currently have some of the highest G&A-to-revenue ratios in the net lease peer group. You will notice that Getty Realty ( GTY ) and NetStreit ( NTST ) have similarly high G&A to revenue ratios, but they are multiple times smaller in size than either GNL or RTL in terms of total assets.

The difference in efficiency between internal and external management structures is incredible. Shareholders will be paying 1/3rd the "management fee" under an internal structure than they currently do under the external structure.

What about the portfolio of the combined REIT?

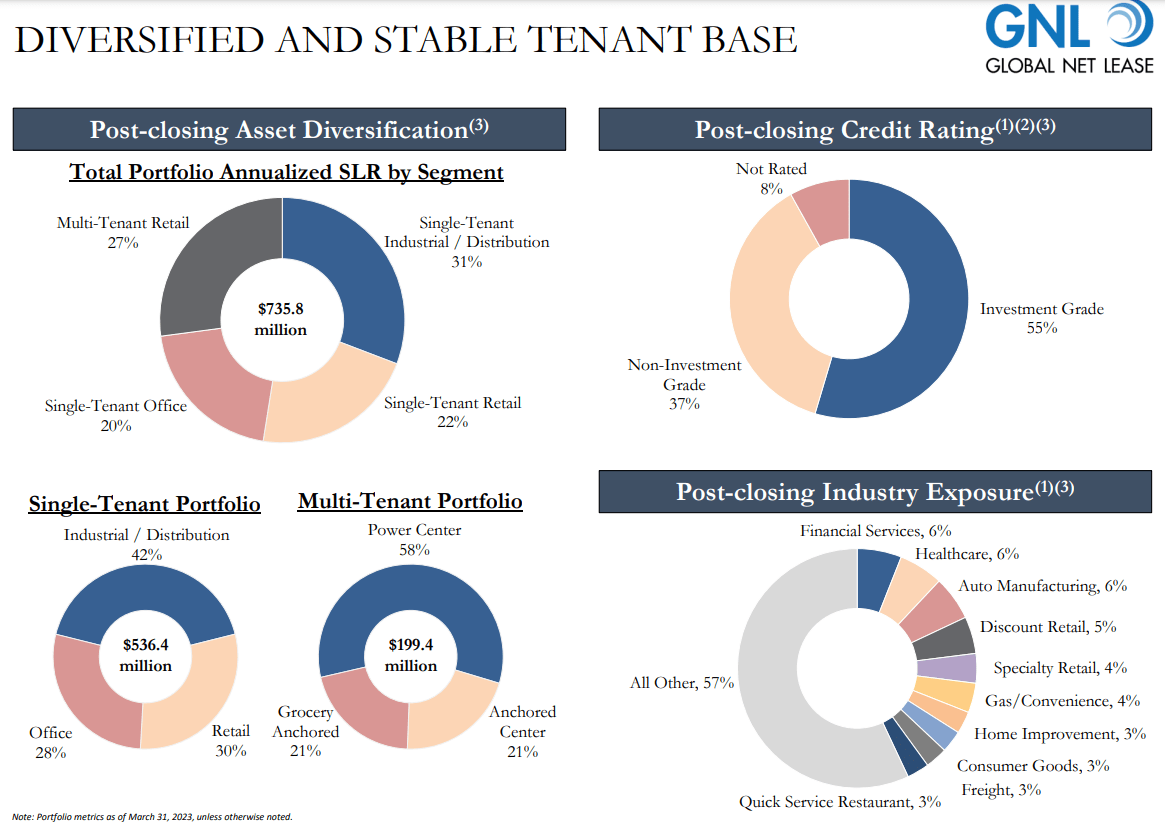

It will be heavily diversified across single-tenant and multi-tenant retail, single-tenant industrial and distribution, and single-tenant office. About 1/5th of its multi-tenant retail shopping centers are grocery-anchored.

{kind=link}

Particularly notable is post-merger GNL's tenant credit profile -- 55% of the portfolio by straight-line rent comes from investment grade-rated tenants, and some of that 8% of non-rated tenants also sport IG profiles.

Why The Merger Is Good For GNL Preferred Stockholders

GNL currently has two classes of cumulative redeemable preferred stock: Series A 7.25% ( GNL.PA ) and Series B 6.875% ( GNL.PB ), both of which trade at discounts to par. As of this writing, GNL.PA trades at a 20% discount to par, while GNL.PB trades at a 21.2% discount to par.

In March, I wrote an article explaining why I find GNL's 8%-yielding preferred stock attractive . That article provides an explanation of why I view GNL's prefs as safe in the company's current form.

But I believe this merger deal makes GNL's preferred stock more valuable and its dividends safer than they were before.

Here are six reasons:

- Stock-for-stock deal , which requires raising no new debt.

- Internalization of management , which will eliminate management fees and replace them with general & administrative expenses. The G&A is projected to be lower than the external manager fees, which is one way management expects this transaction to be immediately accretive. Since G&A is an operating expense, paid before preferred dividends, lower expenses in this area makes preferred dividends safer.

- Other synergies , amounting to about $21 million of annual savings, contribute to the total annual cost savings of ~$75 million. This represents less costs in the way of paying the preferred dividends.

- Greater size, scale, and diversification , which increases the total cash flow and EBITDA available to pay the preferred dividends.

- Reduced leverage : Management asserts that this transaction should reduce net debt to EBITDA from 8.3x for GNL and 9.6x for RTL in Q1 2023 to 7.6x after the merger closes. Lower leverage provides greater preferred dividend safety.

- Reduced common dividend payout ratio , resulting from the resetting of GNL's annualized dividend from $1.60 to $1.42 after the merger closes. This reduces the combined payout ratio of the two REITs from about 100% to about 85%, providing more retained cash.

The biggest point to emphasize here, in my estimation, is the one about size and scale. A bigger portfolio provides larger total EBITDA and therefore greater preferred dividend coverage, assuming no additional issuance of preferred stock. Given the fact that this is an all-stock deal, there does not appear to be any need or plans for preferred stock issuance.

What about The Necessity Retail REIT's two classes of preferred stock? These are the Series C 7.375% ( RTLPO ) and Series A 7.5% ( RTLPP ). To date, I have seen no update on these. They may simply continue to trade under their current names and ticker symbols and be paid by the post-merger GNL. Or, perhaps their names will change.

Why own GNL's preferreds instead of RTL's, then? My reasoning is that (1) GNL's prefs have lower coupon yields, and (2) RTL's prefs are more likely to get a raw deal by management, if either of them do.

GNL.PA offers a yield of ~9% and upside to par of 25%, while GNL.PB offers a yield of 8.7% and upside to par of 27%.

I find this to be a good buying opportunity for either of GNL's preferred stocks.

For further details see:

Global Net Lease And Necessity Retail REIT Merger: The Real Winner Is GNL Preferred Stock