GLP - Global Partners: Governance Concerns Trump A Strong Financial Performance

Summary

- Global Partners LP posted spectacular financial results over the past three quarters that caused its units to be one of the best-performing midstream equities in 2022.

- However, the company's results are likely temporary, as margins and volumes revert to historical norms.

- Governance concerns keep us away from Global Partners LP units.

Global Partners LP ( GLP ) handily outperformed analyst expectations in 2022. Its $66 million, $75 million, and $135 million of Adjusted EBITDA in the first, second, and third quarters beat consensus estimates by $12 million, $22 million, and $42 million, respectively. Third-quarter Adjusted EBITDA grew by 24.9% from the previous quarter and 112.8% from the previous year. The tremendous outperformance caused GLP units to be the sixth-best performer in our coverage universe in 2022, ending the year up 48%.

When we last reviewed GLP in April 2022, the gas station operator was operating in the midst of soaring gasoline prices. At the time, the company’s volumes were shrinking in an extremely tight gasoline market.

Shortly thereafter, however, conditions turned for the better. Prices at the pump peaked and then plunged for months after refiners responded to record-high gasoline margins, high diesel demand, and a loosening crude oil market by ramping up gasoline production.

Gas station financial results outperform when gasoline prices fall, as they adjust their retail prices more slowly when wholesale prices fall than when prices increase. The lag between a falling wholesale price and the retail price boosts margins. This phenomenon led GLP to generate bumper cash flows, particularly in the second and third quarters. Over the first nine months of 2022, GLP’s gross profit surged 55% over the first three quarters of 2021. The gain was driven by significantly higher fuel margins amid declining volumes sold and increased convenience store activity.

The quarterly margin performance is shown below. Gross operating margin in 2022 surpassed 2020, the last time plunging gasoline prices led to an outsized increase in fuel margins.

{kind=link}

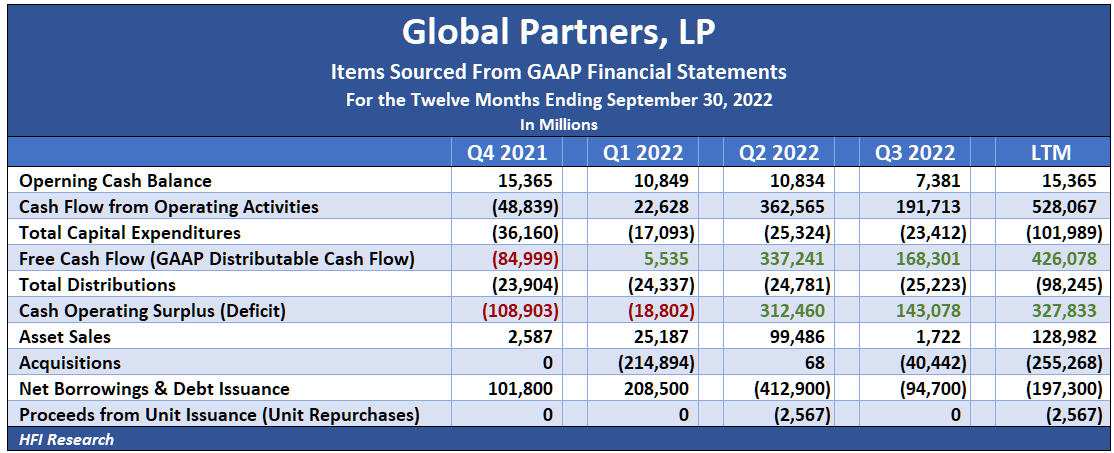

The higher margins led GLP to generate a massive $455.5 million cash flow surplus over the past six months and a $327.8 million surplus over the past year.

{kind=link}

Management allocated the surplus cash flow and $129.0 million of asset sales toward paying down $197.3 million of debt and $255.3 of acquisitions. The acquisitions included the assets of Tidewater convenience stores for $40.4 million, Miller Oil for $$60.1 million, and Consumers Petroleum of Connecticut for $154.7 million. The first two acquirees were located in Virginia, and the third in Connecticut and New York. They are consistent with GLP’s strategy to consolidate Eastern U.S. gas stations.

Questionable Sustainability of Recent Financial Performance

GLP’s results are tied to fuel margins and volumes. While the past few quarterly results were unusually good, we do not believe they are sustainable over the long term. As a result, we expect GLP’s extraordinarily high return on capital employed, which was 26.0% in the third quarter, as well as its rock-bottom 1.9-times debt to Adjusted EBITDA, will revert to historical norms. If so, absent significant debt reduction, we expect its unit price to decline.

Governance Concerns are Front and Center

Aside from the short-term nature of GLP’s financial results, governance concerns also keep us away from the units.

GLP is run in the old-school mold of MLPs in which the limited partner’s capital is used as a vehicle to enrich the general partner and its affiliates far out of proportion to public common unitholders. Time and again, this arrangement has led to permanent losses for common unitholders. While we’re not predicting such trouble for GLP’s unitholders, it is important to recognize that GLP’s corporate governance practices are just as egregious as other MLPs whose common unitholders suffered losses while its general partner walked away rich.

For one, GLP’s general partner is incentivized to increase the partnership’s common distributions. The concern raised by such an incentive is that management, which controls the general partner, distributes more cash flow in good times than the partnership can afford in bad times. Eventually, the partnership enters a downturn overextended, forcing it to slash distributions to pay down debt. The distribution cuts cause the unit price to plunge with little hope for a recovery for at least several years.

GLP currently distributes $0.625 per quarter to common unitholders. Its incentive distribution rights (IDRs) stipulate that the general partner’s override on the common distribution increases from 23.7% to 51.3% for distributions in excess of $0.6625. Clearly, the Slifka family, which controls GLP through its ownership of GLP’s general partner, will make out far better than common unitholders when the override steps up. The IDRs serve as a big shiny carrot hanging over the general partner that increases the risk of bad capital allocation decisions.

Offsetting this risk is the fact that GLP’s business tends to be stable. Volumes tend to be higher when margins are lower and vice-versa. A stable business can be run with higher leverage. However, we can envision a future scenario in which gasoline shortages bring about higher prices and lower volumes for a prolonged period, inducing financial stress among gas station operators. This would be the sort of downturn that could expose unitholders to loss if management continues to increase distributions from current levels.

A second corporate governance concern relates to the insider dealing that reared its head in the second quarter of 2022.

In January 2015, GLP acquired the Revere Terminal on Boston Harbor in Massachusetts from the Slifka family for $23.7 million. In June 2022, GLP sold the terminal for $150 million to an unnamed buyer. It also entered into an arrangement with the buyer to lease back the facility. When GLP had originally bought the terminal from the Slifka family, it agreed to pay them 50% of the net proceeds from the terminal’s sale. As a result of this agreement, the Slifka family earned $44.3 million of the proceeds from the terminal’s sale in June. Such a windfall would have been unlikely without the participation of outside common unitholder capital in the deal, which funded the initial purchase and remained at risk over the asset’s holding period.

These transactions occurred without the level of public unitholder representation we prefer to see. We won’t speculate on their propriety, but in our experience, these kinds of inside deals are a red flag for unitholders. They suggest the partnership is run for the benefit of its controlling unitholder at the expense of outside common unitholders, and that the latter will lose in any conflict of interest. The arrangement is ripe for abuse and runs the risk of growing worse for outside common unitholders over time. As long-term investors, this is an arrangement in which we refuse to participate.

Conclusion

Above all else, Global Partners LP’s corporate governance keeps us away from considering its equity for long-term purchase. Moreover, Global Partners LP units appear cheap based on 2022 performance, but the situation can change for the worst swiftly if margins correct to historic norms. The company's business and financing model also haven't been tested amid gasoline shortages, which could be a risk amid a bona fide oil supply crisis. Existing unitholders should be aware of these potential negatives that lurk in the outlook for the units.

Based on fundamentals, we’re maintaining our Hold rating on Global Partners LP and $29 price target. However, if Global Partners LP’s governance practices become more egregious, we’ll change our rating to a Sell.

For further details see:

Global Partners: Governance Concerns Trump A Strong Financial Performance