GLP - Global Partners: Ignore Their Common Units Buy Their Preferred Units

2023-04-12 09:18:44 ET

Summary

- Global Partners saw record-setting financial performance during 2022, but this was driven by unique operating conditions following the Russia-Ukraine war.

- Management already warned that operating conditions are normalizing going forward into the remainder of 2023, which hinders their distribution growth.

- Since their series B preferred units carry a yield that is circa 1% higher versus their common units, I feel they are more appealing.

- Apart from this higher yield, their preferred distributions also carry lower risk versus their common distributions.

- As a result, I believe that a hold rating is appropriate for their common units, whilst a buy rating is appropriate for their preferred units.

Introduction

The recent years have been quite unique with several large events, most notable in this situation, the Russia-Ukraine war that began in 2022 and sadly, continues so far into 2023. The latter ultimately made for unique operating conditions that were very profitable time for Global Partners ( GLP ) with record-setting financial performance during 2022. Although as this subsides as operating conditions normalize, it sees their ability to provide further distribution growth eroding or, at best, slowing down significantly. In light of this outlook and present market prices, I feel it prudent for investors to ignore their common units and instead, buy their preferred units ( GLP.PA ) ( GLP.PB ) that offer a higher yield with lower risk.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

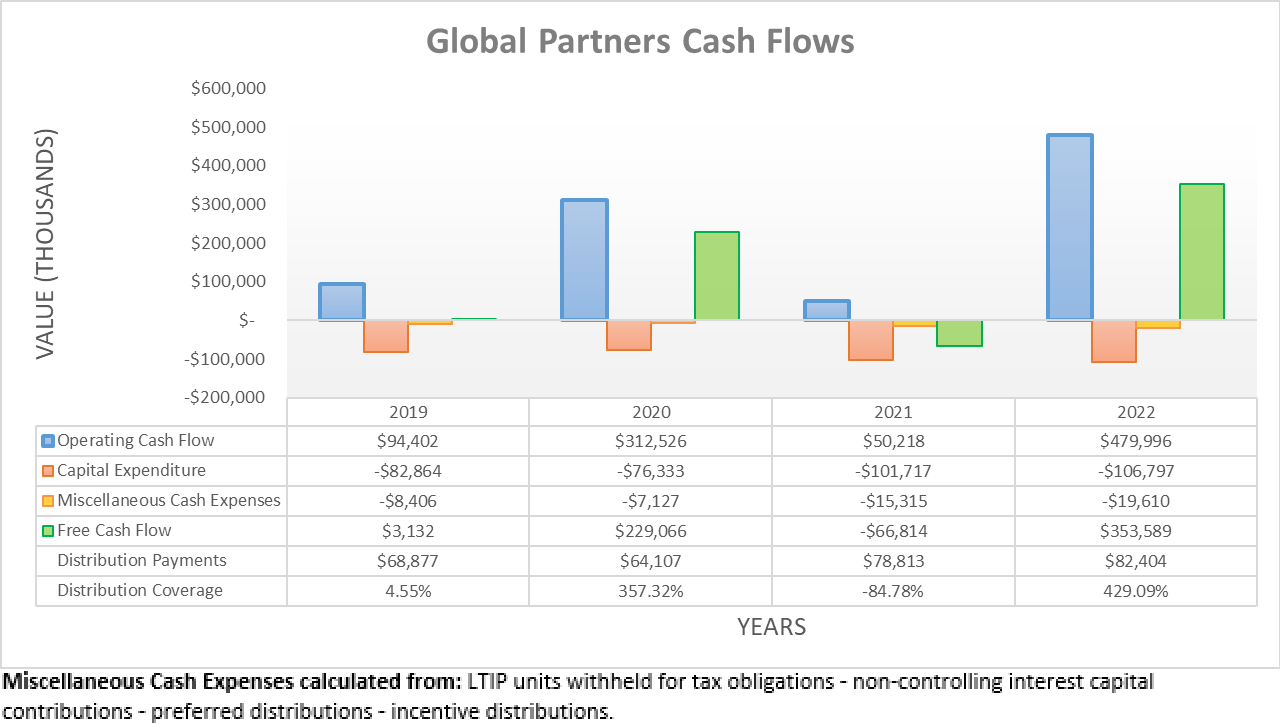

Following 2021 when they generated only minimal operating cash flow, 2022 saw a massive cash windfall with their result surging to a record-setting $480m and thus many magnitudes higher year-on-year versus their previous result of $50.2m. They were able to translate virtually all of this extra operating cash flow during 2022 into free cash flow of $353.6m thanks to their capital expenditure remaining around its routine level of $106.8m, alongside their minor routine miscellaneous cash expenses of $19.6m, as detailed beneath the above graph.

{kind=link}

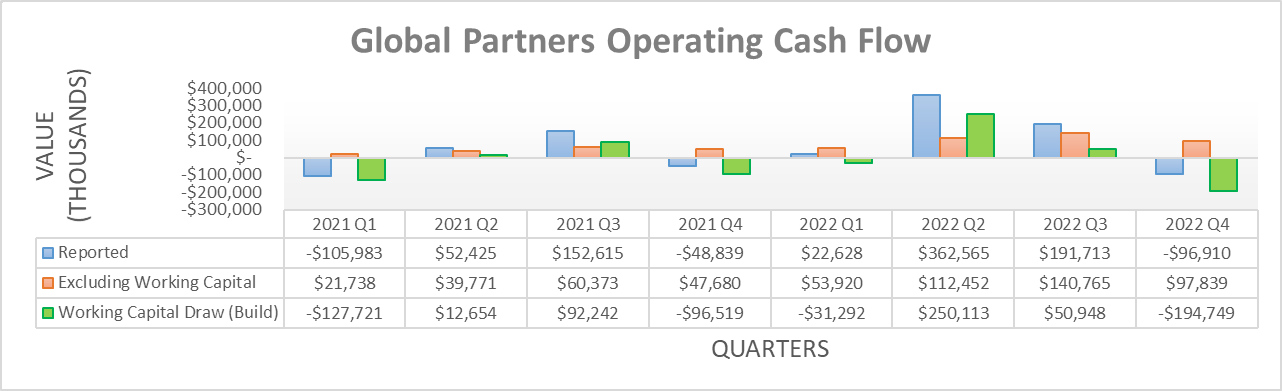

When viewing their results on a quarterly basis, their volatile financial performance is apparent with their operating cash flow swinging widely across the quarters, regardless if viewed at the reported or underlying level that in the case of the latter, excludes their working capital movements. Quite interestingly, the second quarter of 2022 that directly followed the Russian-Ukraine war actually accounted for a very large part of their full-year operating cash flow with a result of $362.6m within this one quarter alone.

At the end of the day, their volatile financial performance is nothing new to the partnership and thus merely par for the course. Whilst their record-setting results during 2022 were very positive, they obviously stemmed from unique operating conditions following the Russia-Ukraine war, and given that economic conditions are easing thus far into 2023 and seemingly likely to continue doing so during the remainder, 2022 is very unlikely to be repeated. In fact, even those running the partnership have effectively warned unitholders as such outlook, given their margins are heading lower alongside a basis to underperform, as per the commentary from management included below.

"Our expectations, as we sit here today, our margins should -- and we have seen this, margins should return back towards something more normal as the curve has flattened…"

"Now obviously, if there's some sort of event or demand is stronger than anticipated, which I feel like the bias is that it will underperform, not overperform."

- Global Product Partners Q4 2022 Conference Call.

Their volatile financial performance makes it impossible to gauge exactly where their results will land during 2023 but I suspect everyone can agree, 2022 is very unlikely to be repeated within the foreseeable future. In turn, this carries ramifications for their distributions and thus by extension, the appeal of their units going forwards into the remainder of 2023, in particular the appeal of their common units versus their preferred units.

If they sustain their most recent quarterly common distribution of $0.635 per unit, the resulting yield at the time of writing would be a high 8.38%. Whilst certainly not bad, their series B preferred units make quarterly distributions of $0.5938 that concurrently see a high yield of 9.31% right now, another circa 1% higher. As for their series A preferred units, these are due to switch to variable and can be redeemed as soon as August 2023, and thus, I feel focusing on their series B preferred units is suitable as these cannot be redeemed until May 2026 and, therefore, provide investors a stable multiple-year window of income, possibly even longer if not redeemed.

Even though the circa 1% higher distribution yield of their series B preferred units over their common units may not seem like too big of a difference, it should be remembered the former sees lower risks too. When it comes to capital structures, preferred units are prioritized over common units, hence the name and thus as a result, their distributions are fixed at a certain level and paid first and if not paid, they accrue as a liability that must be paid before future common distributions. Whereas on the other hand, common distributions can be cut and if not paid, they are simply missed forever and, therefore, they carry higher risks.

As pretty much any investor would know, a higher risk normally equals a higher yield, whereas in this case as it stands right now, the units with a lower risk actually carry a higher yield. Yes, it is true their common distributions could keep growing unlike their preferred distributions that are fixed, although I find it difficult to see sufficient growth on the horizon, especially enough to both makeup for a lower yield right now alongside higher risks.

If excluding their record-setting year of 2022 that were a result of a unique geopolitical backdrop, their free cash flow only averaged $55.1m during 2019-2021 and thus far lower than the cost of $86.3m per annum to fund their most recent quarterly common distribution, given their latest outstanding unit count of 33,995,563. Not only does this call into question their ability to provide further distribution growth going forwards as operating conditions normalize but also, it calls into question whether they can even be sustained at their present level, which raises risks that will need to be monitored going forwards into the remainder of 2023. Whereas, their series A and B preferred distribution payments are easy to fund as they only cost $6.7m per annum and $7.1m per annum, respectively.

Even if ignoring the maths and thinking from a generalized point of view, following the record-setting year of 2022, their common distributions are now at their highest level since 2015 and even if reinstated back to their all-time high of $0.6975 per unit, the resulting yield of 9.20% would only match the yield of their series B preferred units that are available right now. Importantly, they have only reached their present level after this record-setting financial performance on the back of unique operating conditions, and given the outlook for weaker times ahead, this poses a hindrance to their distribution growth, especially given their financial position.

{kind=link}

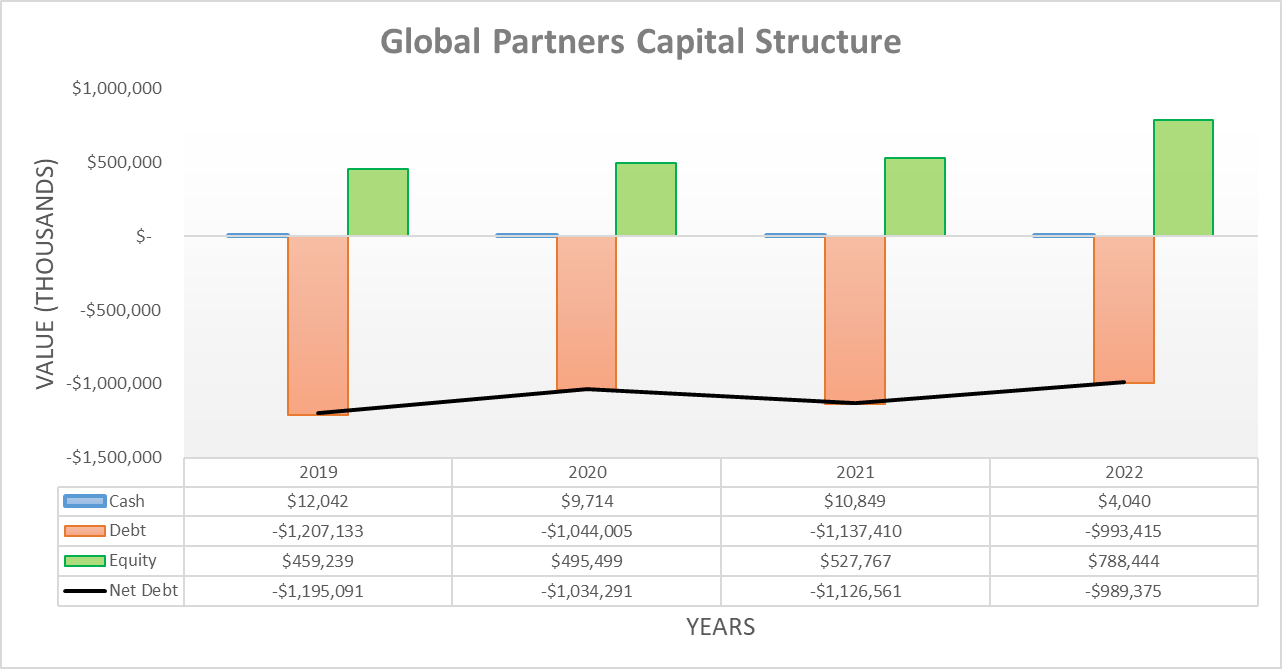

Thanks to their massive cash windfall during 2022, their net debt ended the year at the lowest point in many years, despite their $127.7m of acquisitions net of divestitures. In fact, it was actually even beneath the $1b mark, which is also a rare sight, although only marginally at $989.4m. Going forwards into the remainder of 2023, this is almost certainly will be short-lived because regardless of their yet-to-be-seen volatile cash flow performance, they are planning to close a $273m acquisition during the first half, as per the commentary from management included below.

"In December, we entered into a purchase agreement with Gulf Oil Limited partnership to acquire five of Gulf's refined product terminals for approximately $273 million in cash."

"The transaction is expected to close in the first half of 2023, subject to customary closing conditions, including regulatory approval."

- Global Partners Q4 2022 Conference Call (previously linked) .

Whilst the extent that it boosts their financial performance remains to be seen, this alone will instantly add circa 28% to their net debt as it stands right now. When combined with the aforementioned outlook for weaker operating conditions during 2023 versus those of 2022, it seems very likely that the former is going to end with net debt back above $1b, if not possibly even upwards of $1.3b and, therefore, at the highest point in many years.

The fact they are not deleveraging further boosts the appeal of their preferred units versus their common units. Apart from the fact that more debt generally equals more risks, especially for the lower-priority common unitholders, this also removes any potential narrative about creating value via deleveraging. A prime example would be NuStar Energy ( NS ) that I recently discussed within my other article , who is focused on deleveraging and, as a result, it progressively unlocks more free cash flow to fund higher distributions in the medium to long-term, as well as lowering risks and therefore, this makes their common units appealing versus their preferred units ( NS.PA ) ( NS.PB ) ( NS.PC ).

Admittedly yes, some investors may feel as though this situation instead means the common units of Global Partners carry a narrative about creating value via acquisition-led growth, thereby possibly making them appealing. Whereas on the other hand, I would caution to remember the era of refined products is winding down as the clean energy transition continues. Yes, they are not going to suddenly disappear overnight with demand likely to persist for many years to come but realistically, this outlook still caps their growth potential. Not to mention the additional debt to fund acquisitions incurs its own costs, especially in this period of tight monetary policy and thus further detracts from growth.

{kind=link}

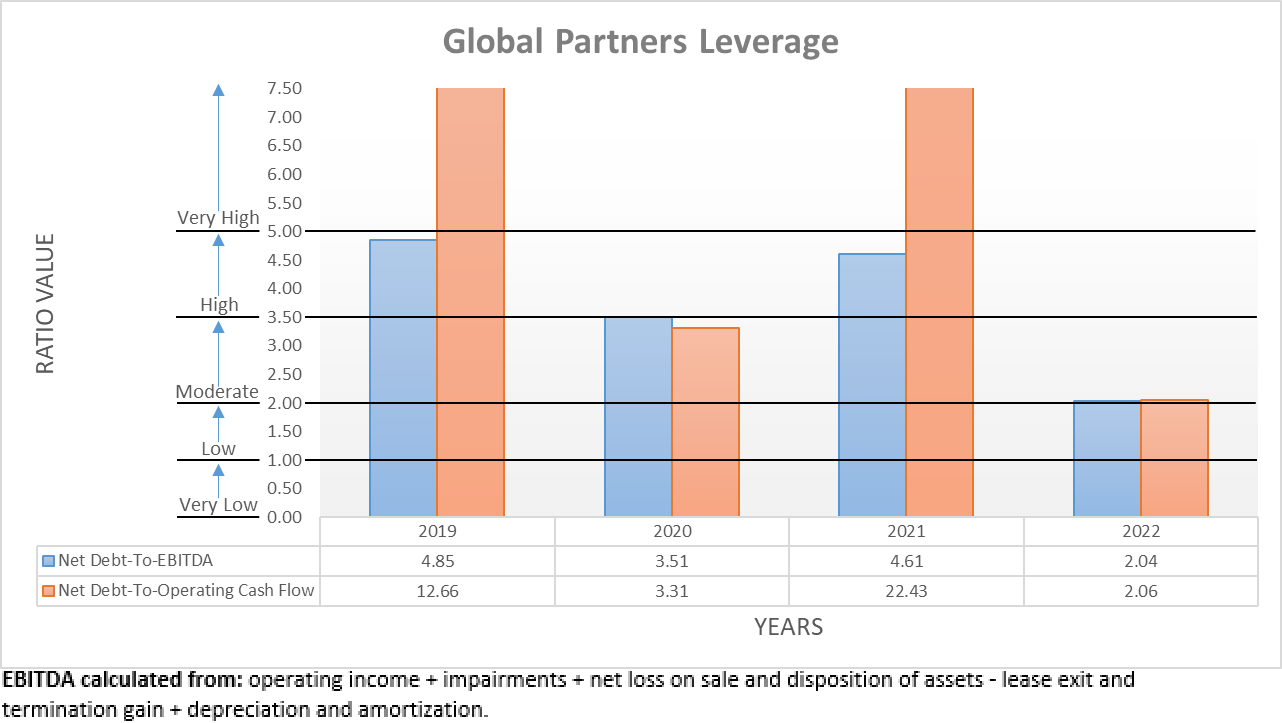

Naturally, their volatile financial performance translates into volatile leverage with their net debt-to-EBITDA and net debt-to-operating cash flow both swinging widely across the years. As it stands right now, 2022 ended with respective results of 2.04 and 2.06 that are both at the bottom end of the moderate territory of between 2.01 and 3.50.

Whilst this seems decent, it should be remembered this stemmed from record-setting financial performance alongside their lowest net debt in many years and thus will likely be higher going forwards into the remainder of 2023. As recently as when 2021 ended, their net debt-to-EBITDA was 4.61 and thus towards the top end of the high territory of between 3.51 and 5.00, whilst their accompanying net debt-to-operating cash flow of 22.43 was far above the threshold of 5.01 for the very high territory. Seeing their leverage vary between these territories does not necessarily endanger the partnership, although it still constricts their potential for growth in the medium to long term and, therefore in turn, I feel that it boosts the appeal of their lower risk preferred units over their common units.

{kind=link}

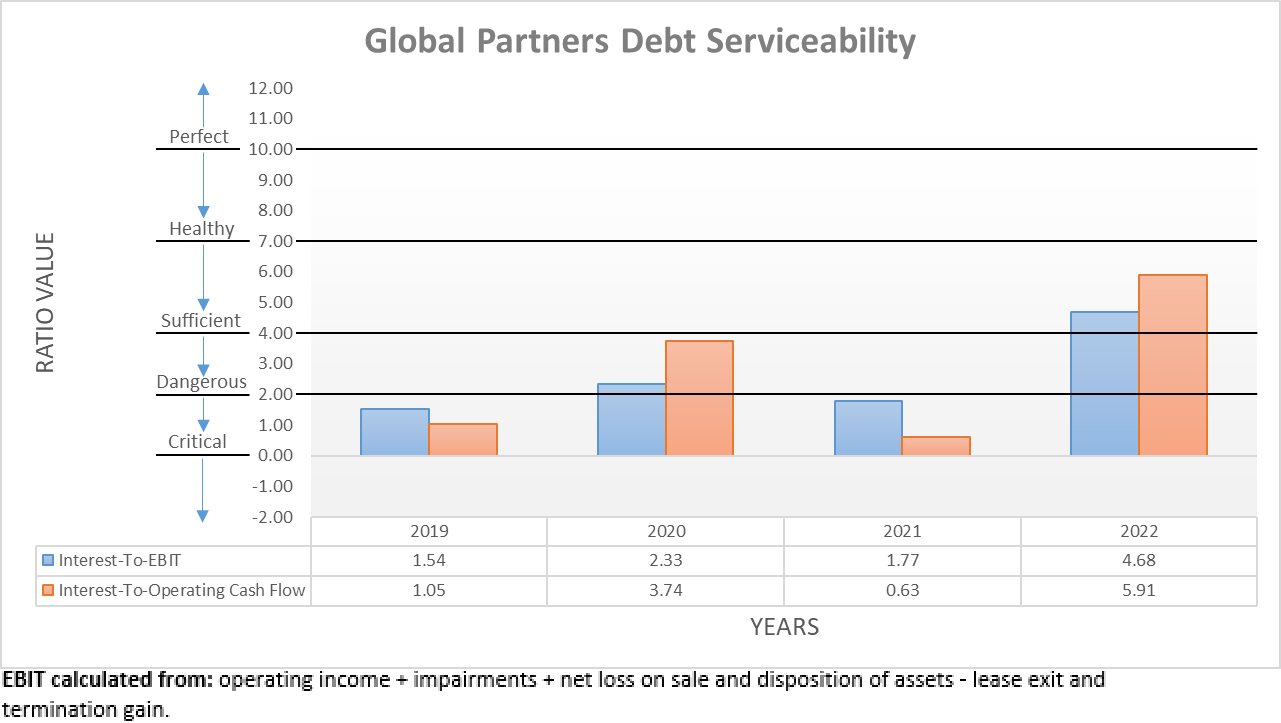

Likewise, their debt serviceability tends to move in tandem with their leverage across the years due to their volatile financial performance. When 2022 ended, their interest coverage was healthy with results of 4.68 and 5.91 when compared against their EBIT and operating cash flow, respectively. Once again similar to their leverage, this will likely deteriorate going forwards into the remainder of 2023 with lower results as their record-setting financial performance gives way. As recently as when 2021 ended, these only saw respective results of 1.77 and 0.63, which are within the range that I consider dangerous. Unsurprisingly once again like their leverage, seeing their debt serviceability vary between these territories does not necessarily endanger their partnership but it once again boosts the appeal of their lower risk preferred units over their common units.

{kind=link}

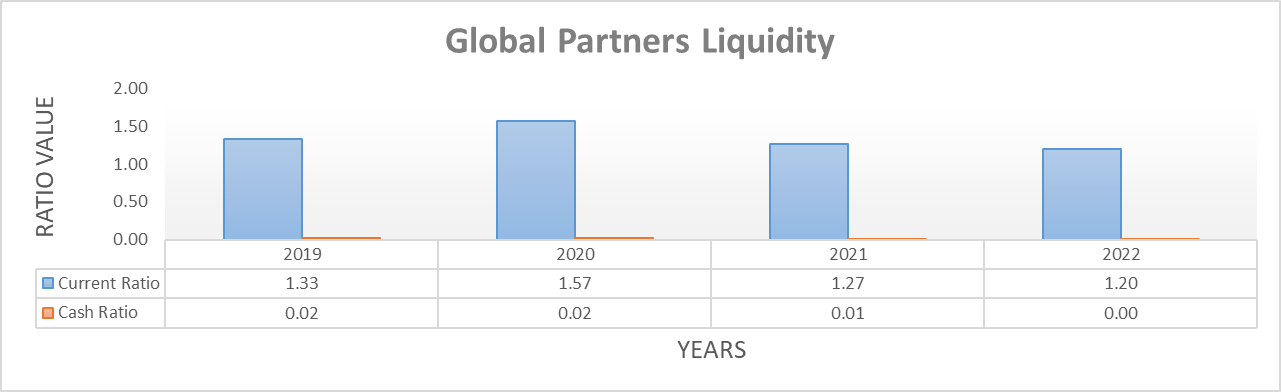

Even though their leverage and debt serviceability constrict their growth, thankfully their liquidity is adequate and thus does not pose any additional risks or hindrances, plus unlike the former two, it is far more stable across the years. To this point, when 2022 ended their current ratio was 1.20, whilst when 2021 ended, it was quite similar at 1.27 due to seeing lower exposure to their volatile financial performance.

Admittedly, their almost non-existent cash balance and resulting cash ratio of 0.00 is not ideal but thankfully, they still retain availability of $1.116b across their two credit facilities. This can fund their $273m terminal acquisition if necessary, whilst still supporting their liquidity requirements but nevertheless, it will be important to monitor their future progress with refinancing going forwards into the remainder of 2023 because it matures in May 2024. At least the remainder of their debt pertains to their senior notes that do not mature until August 2027 at the earliest, thereby providing ample breathing room once dealing with their credit facilities.

Conclusion

I find it difficult to see their common units appealing when they presently trade with a lower distribution yield than their preferred units. Even if ignoring their series A preferred units that may be redeemed later in 2023, their series B that are years away from this point and still carry a higher distribution yield, all with lower risk than common distributions.

Sure, there is obviously no growth potential for their preferred distributions, although their common distributions only reached their present level after a record-setting year that is very unlikely to be repeated within the foreseeable future given its unique geopolitical backdrop. As such, I also find it difficult to see any material growth ahead for their common distributions, especially not enough growth to make up for a lower yield right now alongside higher risks and, therefore, I believe that a hold rating is appropriate for their common units, although I believe that a buy rating is appropriate for both their series A and B preferred units.

Notes: Unless specified otherwise, all figures in this article were taken from Global Partners' SEC Filings , all calculated figures were performed by the author.

For further details see:

Global Partners: Ignore Their Common Units, Buy Their Preferred Units