GLP - Global Partners: New Capacity Debt Agreements And Cheap

2023-11-06 22:54:22 ET

Summary

- Global Partners LP recently signed agreements, including the acquisition of Landmark Industries, which is expected to accelerate net sales growth in 2024.

- The company is renegotiating certain credit agreements, which could lead to more favorable debt terms and increase interest in the stock.

- While there are risks such as changes in oil prices and credit conditions, the stock remains undervalued and could see an increase in price if quarterly figures exceed expectations.

Global Partners LP ( GLP ) recently signed two agreements including the acquisition of Landmark Industries, which will most likely accelerate net sales growth in 2024. GLP is also renegotiating certain credit agreements. I believe that obtaining beneficial debt terms could accelerate the interest for the stock. Under my worst case scenario, changes in the oil price, changes in the credit markets, or the effect of covenants may deteriorate future cash flow statements. With that, I believe that GLP remains undervalued. If the new quarterly figures to be released are better than expected, the stock price will most likely increase.

Global Partners

Founded in 2005, Global Partners is a company that owns a large series of assets and an attractive diversified portfolio within the fuel and oil markets. This includes concentration of market shares in service stations within specific regions as well as a large number of accesses to various oil terminals in areas of Massachusetts, Maine, Connecticut, Vermont, New Hampshire, Rhode Island, New York, New Jersey, and Pennsylvania.

At the end of 2023, the service stations operated by the company will most likely exceed 1,600 with almost 400 under its exclusive ownership, in addition to the rest working through joint agreements or rental of the establishments. The data that stands out about this company is that it is the main supplier of oil and fuel to wholesale and retail stores as well as distributors for businesses within the states of New York and New England. The portfolio of activities and services offered by this company is completed with the transportation of fuels and refined oil mainly on the east coast of the United States and the territory of Canada.

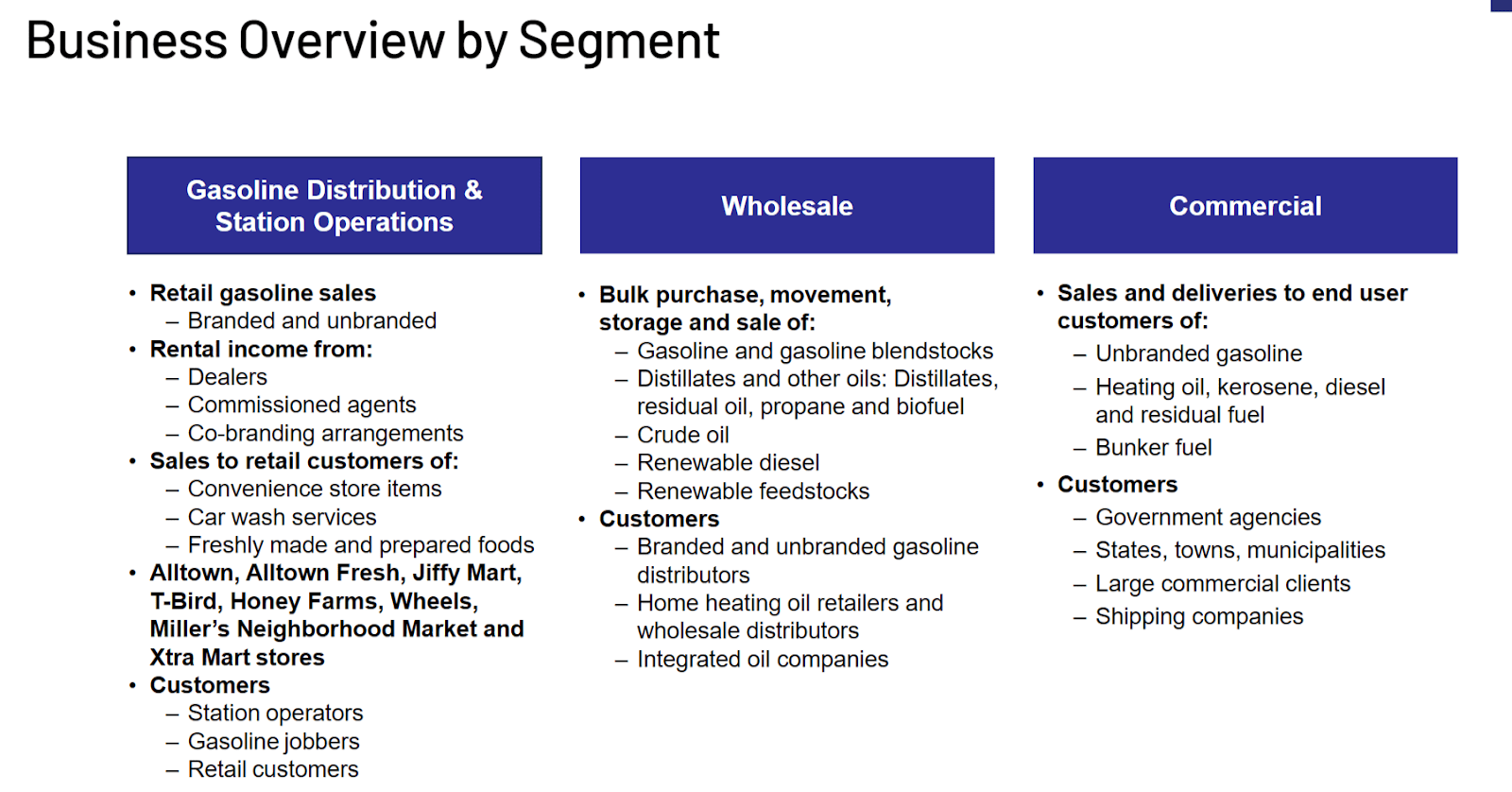

The operations are divided into three segments: wholesale sales, gasoline sales and distribution centers, and commercial activities. First of these segments is the one that has the most revenue, reaching percentages above 50% of the company revenue. The commercial segment does not exceed 10% of the annual income that this company receives. The wholesale distribution segment is dedicated to the purchase, storage, distribution, and mixture of fuels and oil for companies that then distribute it to other markets. The last of the segments, which represents the least income for the company, has public or private institutions as its final market, and the operation is similar to that of the majority distribution segment with a lower amount of product income.

{kind=link}

Balance Sheet

As of June 30, 2023, Global Partners LP reported cash worth $11 million, accounts receivable of close to $430 million, accounts receivable from affiliates of about $10 million, and inventories worth $343 million. Total current assets stood at about $900 million with a current ratio larger than 1x, so I do not really see liquidity issues at this point in time.

The largest asset is property and equipment, which is worth about $1.199 billion. The management also reported goodwill of about $427 million and total assets of about $2.936 billion. The asset/liability ratio is larger than 1x. I believe that the balance sheet appears stable.

Source: 10-Q

The list of liabilities does not seem worrying, however investors may want to study carefully the senior notes and the total amount of debt. With accounts payable of $398 million and working capital revolving credit facility-current portion worth $89 million, management also reported trustee taxes payable of $55 million, accrued expenses and other current liabilities of $140 million, and total current liabilities close to $754 million. Additionally, with a revolving credit facility of about $119 million, senior notes close to $741 million, and financing obligations of about $140 million, total liabilities stood at $2.161 billion.

Source: 10-Q

Debt Analysis, And EV/FCF Multiples

Global Partners LP signed a few debt agreements that use the SOFR to calculate the interest rate. I could read that the interest rate to be paid would most likely be close to SOFR plus 1%-2.5%. Considering the current SOFR level, I believe that assuming a cost of capital above 7.9% would make sense. I don't really know how the SOFR could change in the future, so I decided to run a sensitivity analysis using different interest rates.

Borrowings under the working capital revolving credit facility bear interest at (1) the Daily or Term secured overnight financing rate plus a 0.10% SOFR adjustment plus a margin of 2.00% to 2.50% depending on the Utilization Amount, or (2) the base rate plus a margin of 1.00% to 1.50% depending on the Utilization Amount. Source: 10-k

The company traded at close to 6.8x FCF and 7.8x FCF in the past, so I believe that EV/2032 FCF exit multiple would not be close to that figure.

Source: Ycharts

Expectations From Other Analysts Include Net Sales Growth In 2024 And Positive FCF/Net Sales

I believe that the expectations from other market analysts are beneficial, and it is worth having a look at them. They are expecting net sales growth in 2024, EBITDA growth in 2024, operating margin close to 1%, and positive net income in 2023 and 2020. More in particular, 2024 EBITDA would stand at close to $359 million, with EBIT of $237 million, net income close to $130 million, and free cash flow of about $97 million.

Source: S&P

Best Case Scenario: Organic Growth, Inorganic Growth, Geographic Expansion, Further Deals With Larger Companies Like Exxon ( XOM ), And Successful Renegotiation Of The Debt Terms

Slow organic growth is to be expected within the markets in which it already participates, which in many cases correspond to the marine industry and the railway industry, and the inorganic growth of its service station segment through the acquisition and expansion of its geographical footprint. In this regard, an agreement signed a few months ago with Gulf Oil Limited Partnership for $273 million is worth noting, which is expected to bring further storage capacity. As a result, more capacity will most likely mean further net sales growth from 2024.

{kind=link}

Additionally, Global Partners dedicates its efforts to distinguishing potential value acquisitions in the markets, and this has been part of its ongoing strategy in recent years with the most recent acquisition of Landmark Industries through the subsidiary Spring Partners Retail, owned by Global Partners, and the renowned Exxon Mobil Corporation. I believe that further deals with large groups will most likely bring the attention of the investment community, which may enhance stock demand.

On June 1, 2023, Spring Partners Retail LLC, a joint venture owned by subsidiaries of ours and Exxon Mobil Corporation, completed its acquisition of 64 Houston-area convenience and fueling facilities from Landmark Industries, LLC and its related entities. See Note 11 of Notes to Consolidated Financial Statements for additional information. Source: 10-Q

I also believe that further successful negotiations with debt owners and changes in the financial terms of some other credit agreements reached by Global Partners are relevant. Lower financial costs will most likely enhance the FCF margins, and may also lower the cost of debt and cost of capital. As a result, we may see increases in the intrinsic valuation of Global Partners.

On May 2, 2023, we and certain of our subsidiaries entered into the ninth amendment to third amended and restated credit agreement and joinder which, among other things, increased the applicable revolver rate by 25 basis points on borrowings under the revolving credit facility and extended the maturity date from May 6, 2024 to May 2, 2026. Source: 10-Q

My cash flow statements include 2032 net income worth $976 million, 2032 depreciation and amortization of about $128 million, amortization of deferred financing fees close to $6 million, and unit-based compensation expense of about $12 million.

I did not include write-off of financing fees, losses on sale and disposition of assets, and long-lived asset impairments because they do not seem recurrent events, however I did include 2032 deferred income taxes worth $9 million or changes in accounts receivable of about -$924 million.

Source: My Cash Flow Expectations

Besides, with changes in accounts receivable-affiliate of about -$34 million, changes in inventories of -$421 million, and changes in broker margin deposits worth $36 million, I included accounts payable worth $608 million. If we also include 2032 CFO worth $432 million and capital expenditures of -$189 million, 2032 FCF would be $243 million.

Source: My Cash Flow Expectations

Considering previous FCFs, which were around $499 million, and previous FCF growth, I assumed that forecasting FCF around $243 million and $890 million appears reasonable. I also used a terminal EV/FCF of 4x-7x and a WACC between 9% and 15%, which implied a forecast price between $106 and $67 per share with a median close to $82-$90 per share. Additionally, I obtained an IRR between 22% and 10% with a median close to 18%-14%.

Source: My Cash Flow Expectations

My Worst Case Scenario Would Include Changes In The Legislation Or New Technologies Among Other Risks

In my view, any restriction or change in legislation on activities within the industries to which that serves would generate an indirect effect for Global Partners in terms of the demand for its products. Likewise, the emergence of new technologies such as electricity generation or biofuels would also affect the scope for reaching new customers as long as these technologies are adopted in the markets.

On the other hand, due to the situation of international economic instability, the volatility of oil prices and the exposure to increases in interest rates that have been experienced in the United States during the last year are risk factors to take into account.

I also believe that changes in the credit conditions may also be very detrimental for Global Partners. If the company does not adequately refinance its senior notes, or does not find beneficial financial terms, perhaps shareholders could sell equity, which may lead to lower stock demand.

A significant increase in interest rates could adversely affect our results of operations and cash available for distribution to our unitholders and our ability to service our indebtedness. Source: 10-Q

Additionally, covenants could also reduce the activities Global Partners could do, or some M&A operations could be blocked. As a result, we may see a decline in future inorganic growth.

Our credit agreement and the indentures governing our senior notes contain operating and financial covenants, and our credit agreement contains borrowing base requirements. A failure to comply with the operating and financial covenants in our credit agreement, the indentures and any future financing agreements could impact our access to bank loans and other sources of financing as well as our ability to pursue our business activities. Source: 10-Q

Besides, I believe that lower revenue growth than expected or lower EPS revisions could lower the demand for the stock. It is worth noting that Global Partners, in August, delivered lower financial figures than expected, and recently one analyst lowered its EPS expectations. If investors believe that dividends may not increase in the near future, they may lower the total amount of shares acquired.

In the incoming quarterly release, investors are expecting revenue close to $4.26 billion with an EPS close to $0.69 per share. In my view, if the numbers are as good as expected, we may see an increase in the stock price.

Source: SA

Under detrimental conditions, I believe that Global Partners LP could deliver 2032 net income of $389 million, depreciation and amortization worth $20 million, and unit-based compensation expense of about $1 million. Besides, with changes in accounts receivable of about -$93 million, changes in accounts receivable-affiliate worth -$8 million, changes in inventories of -$14 million, and changes in broker margin deposits of $10 million, I also included 2032 changes in accounts payable of $240 million.

Source: My Cash Flow Expectations

Finally, 2032 CFO would be close to $422 million, and with 2032 capital expenditures of about -$126 million, 2032 FCF would be $297 million. Also, taking into account a WACC of 9%-15% and an exit multiple of 4x-7x, the implied median forecast would be close to $18-$12 per share, and the median internal rate of return would not be far from about -4%.

Source: My Cash Flow Expectations

Competitors

Each of Global Partners' business segments experiences different types of competition. Perhaps the most intense is the existing wholesale distribution for the industrial and marine sector in which the participants are companies of national scope with larger access to resources than this company. This market environment is populated by a large number of distributors to regional markets without national reach. In the same way, for the service station segment, there are a large number of stations with or without brand in addition to the gasoline that is sold in stores.

Conclusion

Global Partners did not only sign deals with large corporations like XOM, management also appears to sign new agreements with debt investors, which may enhance the company’s financial flexibility. Besides, I believe that the new capacity delivered from the deal with Gulf Oil Limited will most likely have a beneficial impact on future net sales growth. Under my worst case scenario, covenants, changes in the credit markets, or commodity changes could bring lower EPS growth and lower dividend growth. However, putting it altogether, I believe that Global Partners stock appears undervalued.

For further details see:

Global Partners: New Capacity, Debt Agreements, And Cheap