GLP - Global Partners: Preferreds Up To 12% Yield Is It Worth The Risk?

2023-12-12 15:57:41 ET

Summary

- Global Partners offers investors dividends, dividend growth, and exposure to an irreplaceable asset base on the U.S. East Coast and Texas.

- The company has a strong growth strategy and has outperformed major oil giants in terms of total returns.

- Recent acquisitions and expansion efforts position Global Partners for future growth, but there are risks to consider such as its debt profile and potential impact of higher interest rates.

It pays to have assets that pay you back, especially if they operate in industries with natural barriers to entry. As income investors know well, getting paid is one of the pleasures of investing, because as nice as capital gains are, they don’t pay the bills like a steady dividend check does for the investor.

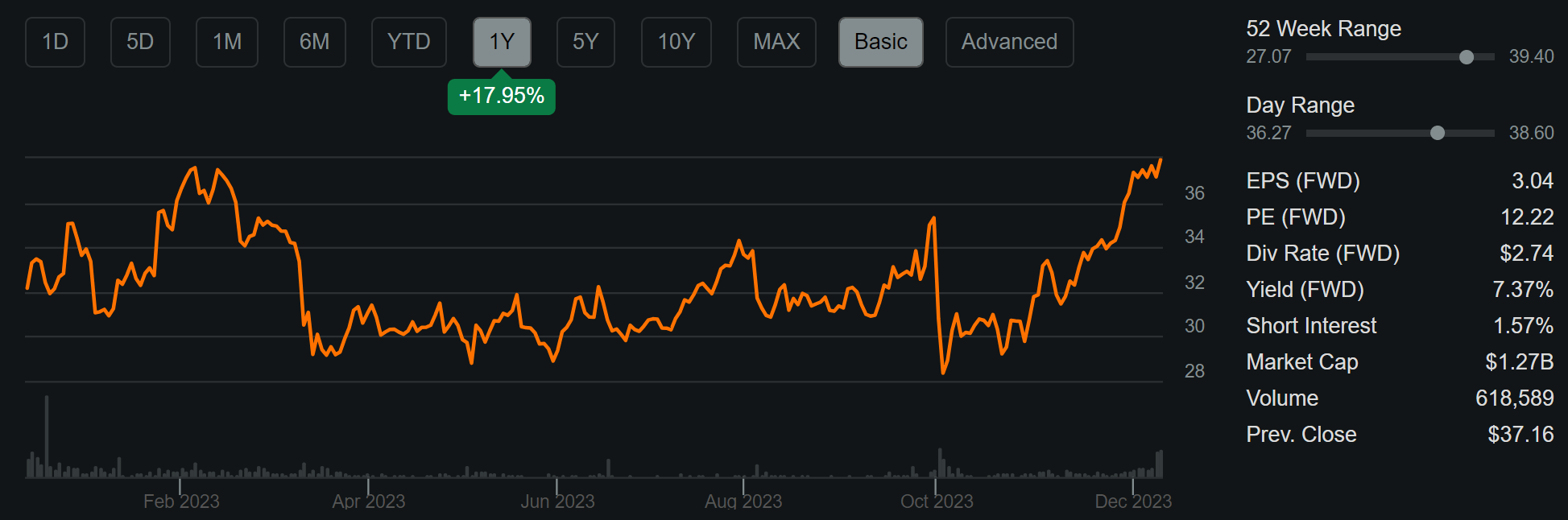

This brings me to Global Partners ( GLP ), which offers investors a little of everything – dividends (called distributions), dividend growth, and capital gains. Maybe I’m a little bit late to the party in covering this stock, as GLP is up 18% over the past 12 months, as shown below. In this article, I evaluate the stock and discuss whether it’s a worthy buy at present, so let’s get started!

{kind=link}

(Note: Global Partners issues a Schedule K-1)

Why GLP?

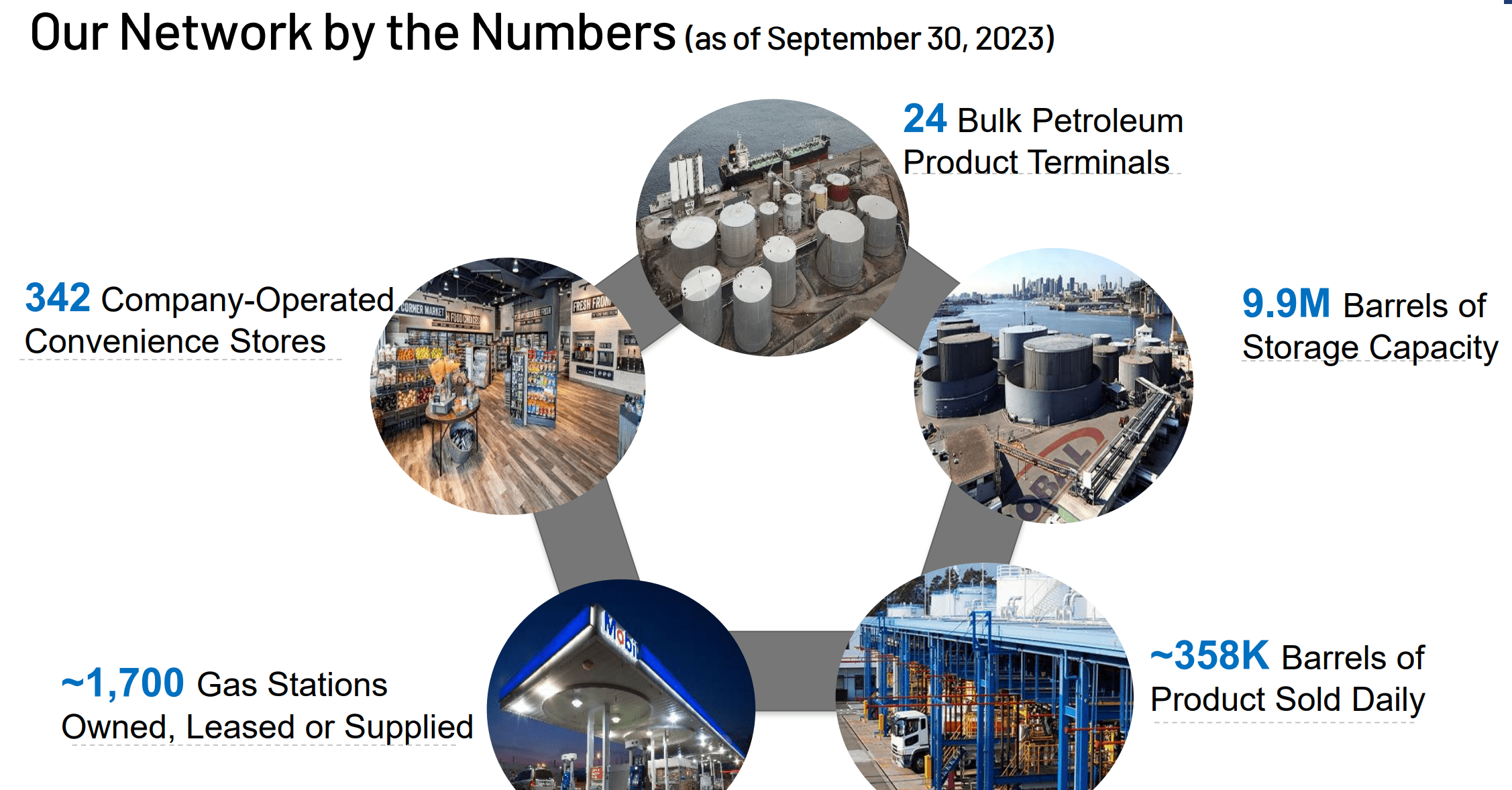

Global Partners is a master limited partnership that’s one of the "largest independent owners, suppliers, and operators of gasoline stations and convenience stores" in Northeastern U.S. It also "owns, controls, or has access to one of the largest terminal networks" in the region, distributing gasoline, distillates, and renewable fuels to wholesalers, retailers, and commercial customers. This vast array of energy assets is perhaps best exemplified by the following graphic.

{kind=link}

While some may view GLP as operating in a no-growth industry, considering that the gasoline infrastructure is already built out, there is something to be said about industry consolidation, which GLP is good at. Asset consolidation enables integration and scale and serves as an external driver of growth. This includes 60 company-operated convenience stores that were added last year, bolstering product margins by 6.1% in the first quarter of this year.

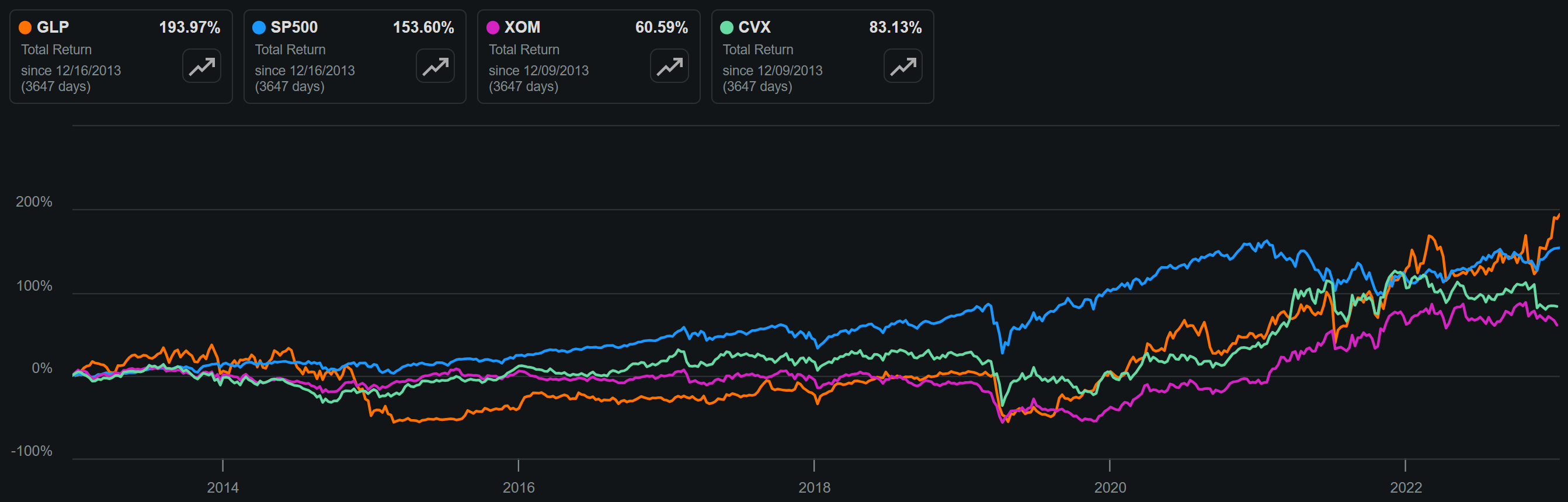

GLP’s growth strategy in recent years combined with a healthy and growing distribution has worked well for shareholders, producing a total return of 194% over the past 10 years, surpassing the 154% total return of the S&P 500 ( SPY ). Just for kicks, I’ve also included the performance of integrated oil giants Exxon Mobil ( XOM ) and Chevron ( CVX ) over the same timeframe, and GLP has outperformed both of them as well, as shown below.

{kind=link}

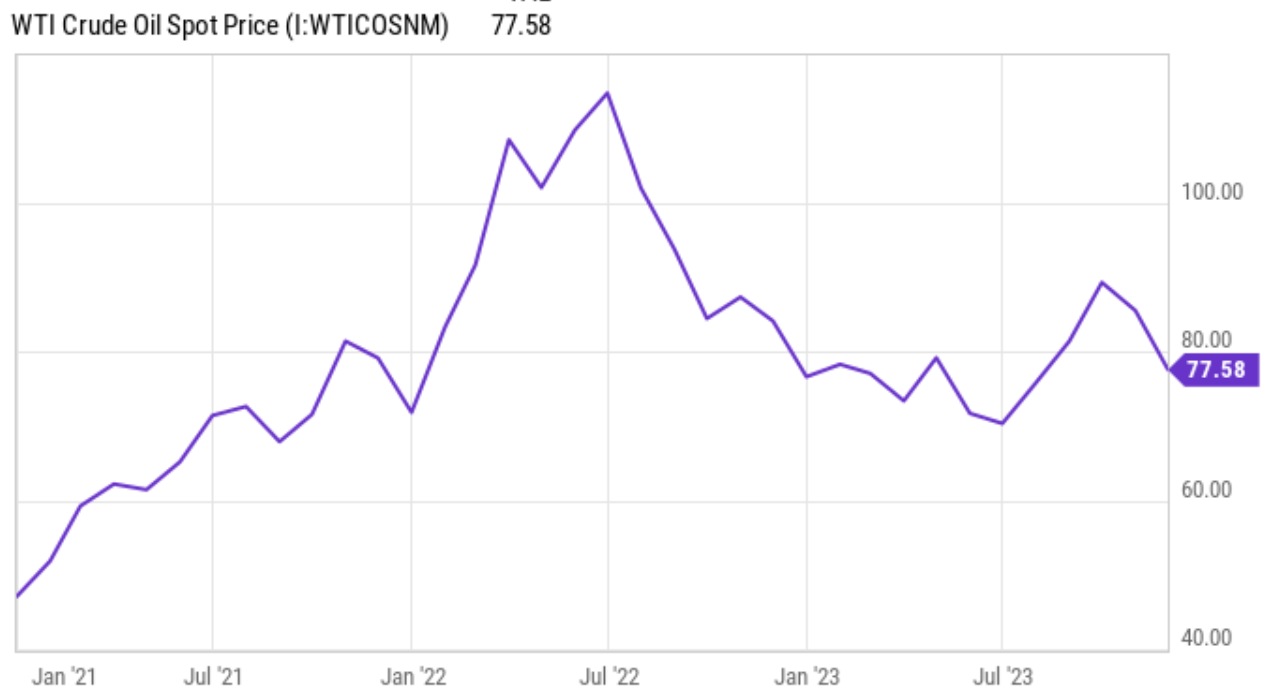

Meanwhile, GLP’s recent third quarter results may look disappointing, as adjusted EBITDA declined to $77.7 million from $168.5 million in the prior year period, and adjusted DCF declined to $43.3 million from $128 million in the prior year period. However, it’s worth noting that last year was a bit of an anomaly, considering the reverberations from a high mismatch between demand and supply in 2022. As shown below, the price of oil per barrel has declined substantially from well over $100 per barrel to $77.58 at present.

{kind=link}

As such, I believe GLP’s most recent quarterly results are more reflective of a true run-rate for the business. Looking ahead, GLP continues to find opportunities to expand its footprint, as reflected by its agreement to acquire 25 refined product terminals from Motiva Enterprises for $306 million in cash. This purchase is supported by a 25-year take-or-pay throughput agreement and is expected to close by year-end.

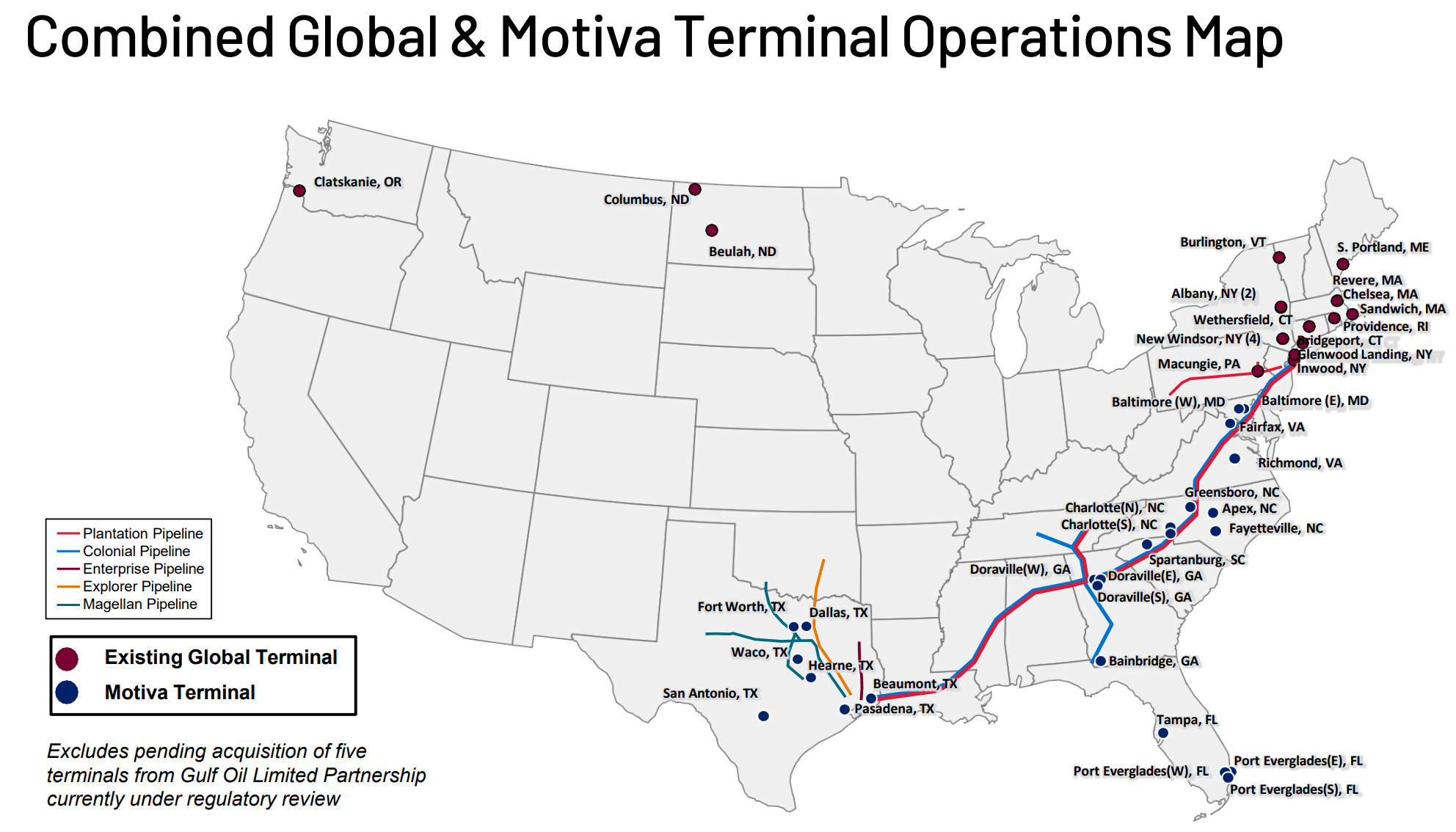

This purchase benefits GLP in that it strengthens and diversifies its terminals while opening up GLP to new commercial and retail customers in additional markets. As shown below, Motiva’s terminals expand GLP’s presents into Texas and the Southeastern regions of the U.S. and sit alongside major pipelines owned and operated by Colonial, Enterprise Products Partners ( EPD ), and Magellan Midstream, now a part of ONEOK ( OKE ), among others.

{kind=link}

Moreover, GLP is further expanding its direct to consumer footprint by recently beginning to operate 64 convenience and fueling facilities in Greater Houston market under a joint venture with Exxon Mobil. While transition to electric vehicles poses as a risk, the recent decline in gas prices throws into question the high cost of EVs for consumers.

As such, the recent growth in the hybrid vehicle market means that the gasoline market may be needed for much longer than what some industry observers may believe. Plus, in a nod to the EV market, GLP recently activated its first company-owned EV charging station, and has 5 additional EV sites under construction.

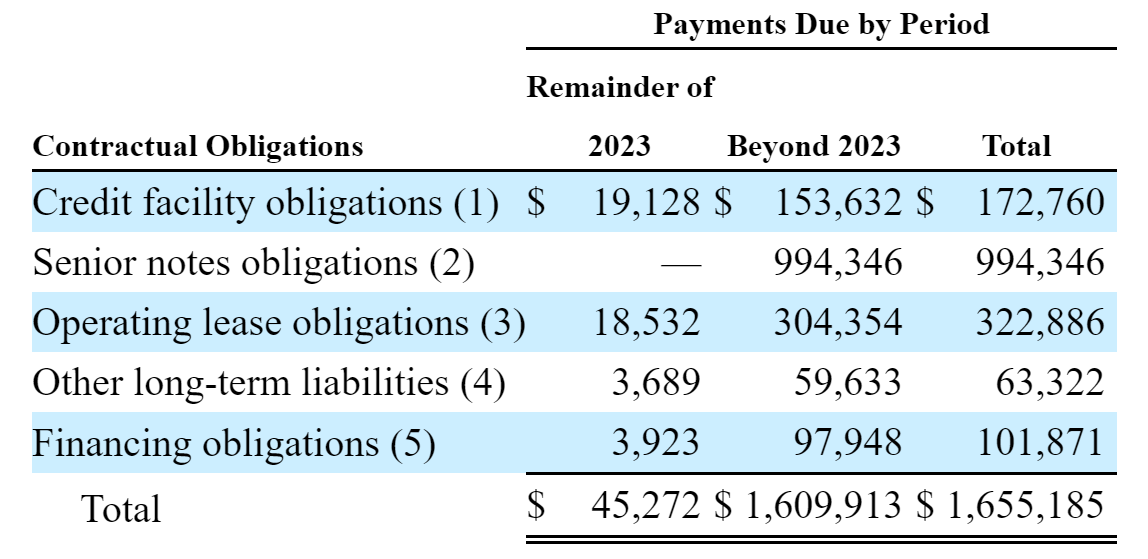

Risks to GLP include its low credit rating of B+ from S&P, which means higher cost of debt. Nonetheless, GLP is within compliance of its debt covenants and has a reasonable debt to TTM EBITDA of 3.7x, although this ratio could trend higher should the price of gasoline decline. As shown below, while GLP’s remaining debt maturities this year are not too material, it does have $1.6 billion worth of debt maturities post 2023 that may need to be refinanced at higher rates.

{kind=link}

Meanwhile, GLP currently yields 7.2%, and the DCF-to-distribution coverage ratio including the special distribution is 1.4x. GLP has also demonstrated a propensity to growth the distribution with a 5-year CAGR of 7.2%.

Lastly, GLP currently trades at $37.94 with a forward PE of 12.5, sitting just below its normal PE of 12.7. As such, I believe most of the near-term value around the stock has already been realized especially considering the potential impact from higher interest rates.

More risk-averse income investors may want to consider the Preferred Series A stock ( GLP.PR.A ). This preferred stock currently carries a forward yield of 12%, but investors should keep in mind that this is a floating distribution rate now that it trades past its call date of 8/15/2023. At the current price of $25.82, GLP.PR.A trades at a 3.2% premium to its $25 par value, signaling that the market doesn’t anticipate for this preferred issue to be called anytime soon. This preferred issue is also cumulative, which means that any missed payments must be made up unless if GLP becomes insolvent.

Investor Takeaway

Overall, GLP offers investors exposure to a diverse, economically essential asset base and a growing distribution, making it an attractive option for income-oriented investors. While there are some risks to consider, such as its debt profile and the potential impact of higher interest rates, GLP’s recent asset acquisitions adding to the bottom line could offset some of those headwinds. Considering all the above, I view GLP and its Preferred Series A stock as being a 'Hold' at present, considering that the common shares trade near their normal valuation and the preferred stock trades at a premium to par value. As such, investors may want to wait for a better margin of safety before buying at present.

For further details see:

Global Partners: Preferreds Up To 12% Yield, Is It Worth The Risk?