GPN - Global Payments: 6% Revenue Boost From EVO Payments Acquisition

Summary

- Following the announcement of EVO Payments, we analyzed Global Payments and forecasted its combined revenues to reach $13.1 bln by 2026.

- In terms of margins, we expect the deal to be positive to Global Payments' margins and forecasted its operating margins to increase to 18.3% post-acquisition.

- While we see the deal impacting Global Payments' financial position, we believe the deal is positive with a net increase of $4.45 to its enterprise value.

Following the recent announcement of Global Payments Inc's ( GPN ) acquisition of EVO Payments ( EVOP ) for $4 bln, we examined the deal and determined the impact on the company’s financials in terms of its revenues, profitability margins and financial position.

Combined Business With Greater Revenues Of $22 bln by 2026

According to the company, the deal with EVO Payments is expected to be highly complementary and increases the scale of the combined business. Additionally, the combined company will serve a customer base of more than 4.5 mln merchant locations, EVO provides merchant acquiring and payment processing services to more than 550,000 merchants .

The acquisition of EVO is highly complementary to our technology-enabled strategy and provides meaningful opportunities to increase scale in our business globally, - Cameron Bready, President and Chief Operating Officer, Global Payments

| Revenues ($ mln) |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022F |

| 2023F |

| 2024F |

| 2025F |

| 2026F |

| Global Payments |

| 3,975 |

| 3,366 |

| 4,912 |

| 7,424 |

| 8,524 |

| 8,957 |

| 9,723 |

| 10,607 |

| 11,411 |

| 12,276 |

| Growth % |

| 5.3% |

| -15.3% |

| 45.9% |

| 51.1% |

| 14.8% |

| 5.1% |

| 8.6% |

| 9.1% |

| 7.6% |

| 7.6% |

| EVO Payments |

| 504.8 |

| 564.8 |

| 485.8 |

| 439.1 |

| 496.6 |

| 555.0 |

| 622.1 |

| 676.7 |

| 750.3 |

| 831.9 |

| Growth % |

| 20.4% |

| 11.9% |

| -14.0% |

| -9.6% |

| 13.1% |

| 11.8% |

| 12.1% |

| 8.8% |

| 10.9% |

| 10.9% |

| Total Combined |

| 3,975 |

| 3,366 |

| 4,912 |

| 7,424 |

| 8,524 |

| 8,957 |

| 10,345 |

| 11,284 |

| 12,161 |

| 13,108 |

| Growth % |

| 45.9% |

| 51.1% |

| 14.8% |

| 5.1% |

| 15.5% |

| 9.1% |

| 7.8% |

| 7.8% |

Source: Global Payments, EVO Payments, Khaveen Investments

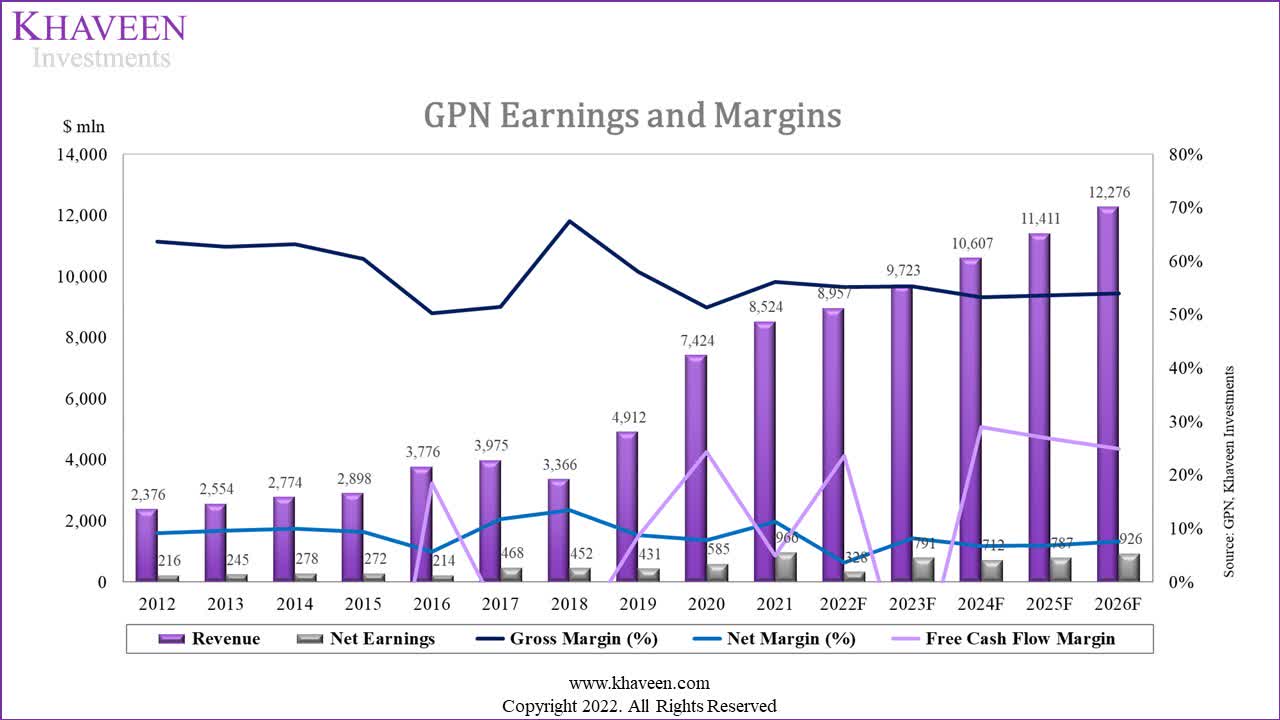

Based on the table above, Global Payments is larger than EVO Payments with a higher revenue of $8.5 bln in 2021 compared to $497 mln for EVO Payments. Moreover, the company had a 5-year average revenue growth rate of 20.4% whereas EVO Payments had a lower average growth rate of 4.4%. We projected their revenues through 2024 based on analyst revenue consensus growth followed by the 3-year forward-average growth until 2026. Combined, we expect EVO Payments to represent 6% of total revenue in 2023 assuming the deal is completed as planned by Q1 2023.

Apart from both companies in the payment processing business, each specializes in certain categories. EVO Payments operate as an integrated merchant acquirer and provides payment, commerce and other value-added solutions. It also offers processing capabilities for specific industries, focusing more on integrating business-to-business (B2B) payments in the Americas and Europe. Global Payments provides software solutions for merchants, issues, businesses and consumers. Thus, we believe this acquisition could help to increase Global Payments exposure to new geographies, increasing its scale and market share.

Positive Impact On Operating Margins To 18.3% With Cost Synergies

| Gross Margins |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022F |

| 2023F |

| 2024F |

| 2025F |

| 2026F |

| Global Payments |

| 2,047 |

| 2,271 |

| 2,853 |

| 3,811 |

| 4,788 |

| 4,944 |

| 5,367 |

| 5,855 |

| 6,299 |

| 6,776 |

| Gross Margins |

| 51.5% |

| 67.5% |

| 58.1% |

| 51.3% |

| 56.2% |

| 55.2% |

| 55.2% |

| 55.2% |

| 55.2% |

| 55.2% |

| EVO Payments |

| 340.3 |

| 375.4 |

| 389.4 |

| 354.8 |

| 420.9 |

| 454.6 |

| 509.5 |

| 554.3 |

| 614.6 |

| 681.4 |

| Gross Margins |

| 67.4% |

| 66.5% |

| 80.2% |

| 80.8% |

| 84.8% |

| 81.9% |

| 81.9% |

| 81.9% |

| 81.9% |

| 81.9% |

| Total Combined Gross Profit |

| 2,047 |

| 2,271 |

| 2,853 |

| 3,811 |

| 4,788 |

| 4,944 |

| 5,876 |

| 6,410 |

| 6,913 |

| 7,458 |

| Gross Margins |

| 51.5% |

| 67.5% |

| 58.1% |

| 51.3% |

| 56.2% |

| 55.2% |

| 56.8% |

| 56.8% |

| 56.8% |

| 56.9% |

| Global Payments Operating Profit |

| 559 |

| 793 |

| 791 |

| 1,214 |

| 1,756 |

| 1,584 |

| 1,720 |

| 1,876 |

| 2,018 |

| 2,171 |

| Operating Margins |

| 14.1% |

| 23.6% |

| 16.1% |

| 16.3% |

| 20.6% |

| 17.7% |

| 17.7% |

| 17.7% |

| 17.7% |

| 17.7% |

| EVO Payments Operating Profit |

| 45.2 |

| -23.2 |

| 29.4 |

| 18.2 |

| 71.4 |

| 45.5 |

| 51.0 |

| 55.4 |

| 61.5 |

| 68.1 |

| Operating Margins |

| 9.0% |

| -4.1% |

| 6.1% |

| 4.1% |

| 14.4% |

| 8.2% |

| 8.2% |

| 8.2% |

| 8.2% |

| 8.2% |

| Total Combined Operating Profit |

| 559 |

| 793 |

| 791 |

| 1,214 |

| 1,756 |

| 1,584 |

| 1,896 |

| 2,056 |

| 2,205 |

| 2,364 |

| Operating Margins |

| 14.1% |

| 23.6% |

| 16.1% |

| 16.3% |

| 20.6% |

| 17.7% |

| 18.3% |

| 18.2% |

| 18.1% |

| 18.0% |

Source: Global Payments, EVO Payments, Khaveen Investments

Global Payments, EVO Payments, Khaveen Investments

{kind=link}

Moreover, as seen in the table above of the gross margins of both companies, EVO Payments had higher gross margins than Global Payments with a 3-year average of 81.9% compared to 55.2% for Global Payments. We projected its gross margins as a combined business in 2023 based on its 3-year gross margins and our revenue projections in the previous point. In 2023, we see its gross margins increasing to 56.8% from 55.2% in the prior year pre-acquisition.

Furthermore, we analyzed its operating margins in which Global Payments has a higher 3-year average of 17.7% compared to 8.2% which we believe is due to its larger scale. In addition, the company highlighted that it expects to derive $125 mln in run-rate EBITDA synergies in the first year of closing. Thus, we projected Global Payments and EVO Payments operating margins based on its historical 3-year average and accounted for the synergies of $125 mln in 2023 through 2026. All in all, we expect the company’s operating margins to increase from a forecasted 17.7% in 2022 to 18.3% in 2023 post-acquisition.

Financial Impact From Acquisitions

Global Payments, EVO Payments, Khaveen Investments

{kind=link}

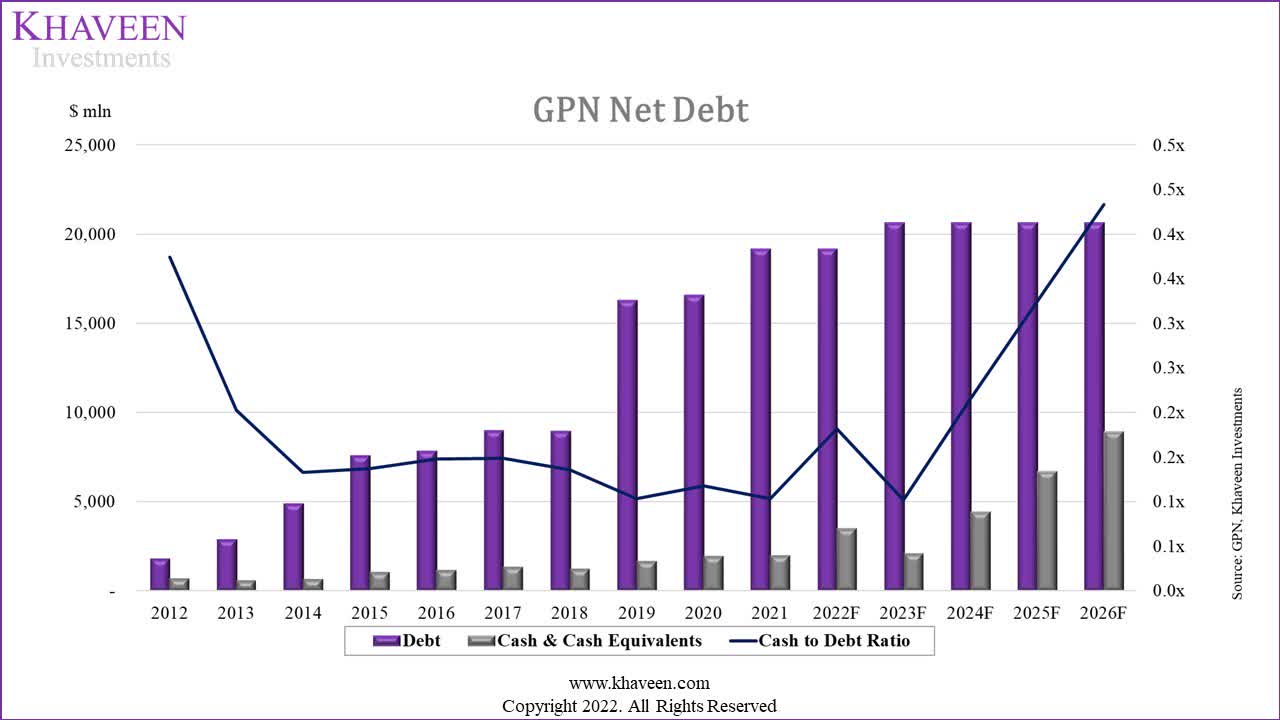

According to the company, Global Payments will pay $34 per share in cash for the acquisition at a total cost of $4 bln. The company will fund the deal with cash on hand and debt worth $1.5 bln from Silver Lake. As seen in the chart above, the company’s cash-to-debt ratio had declined over the past 10 years as the company took on more debt. Post-acquisition, we expect its cash-to-debt ratio to further decline to 0.10x but recover through 2026 at 0.43x with the positive cash generation of the company.

| Net Income Projection ($ mln) |

| 2022F |

| 2023F |

| 2024F |

| 2025F |

| 2026F |

| Total |

| Net Income (With Acquisition) |

| 328 |

| 923 |

| 847 |

| 925 |

| 1,067 |

| Net Income (Without Acquisition) |

| 328 |

| 791 |

| 712 |

| 787 |

| 926 |

| Difference |

| 0 |

| 132 |

| 135 |

| 138 |

| 140 |

| 545 |

Source: Global Payments, EVO Payments, Khaveen Investments

| Global Payments |

| $ mln |

| Enterprise Value |

| 19,982 |

| Synergies |

| 8,450 |

| Less: Acquisition Cost |

| 4,000 |

| New Enterprise Value |

| 24,432 |

Source: Global Payments, EVO Payments, Khaveen Investments

Furthermore, we calculated the net change for Global Payments' current enterprise value after factoring in the value of synergies (based on the 5-year forward net income increase multiplied by its P/E of 15.5x) less the acquisition cost. Overall, we calculated its enterprise value to increase by $4.45 bln to $24.4 bln with the acquisition.

| Credit Analysis |

| 2012 |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| Average |

| EBIT interest coverage |

| 18.5x |

| 15.7x |

| 13.0x |

| 7.6x |

| 3.1x |

| 3.4x |

| 4.5x |

| 2.9x |

| 3.9x |

| 5.7x |

| 7.8x |

| EBITDA interest coverage |

| 23.7x |

| 20.4x |

| 17.0x |

| 10.6x |

| 5.5x |

| 6.1x |

| 7.5x |

| 6.2x |

| 9.1x |

| 11.2x |

| 11.7x |

| CFO interest coverage |

| 11.3x |

| 7.5x |

| 12.3x |

| 9.5x |

| 4.9x |

| 3.1x |

| 6.3x |

| 5.2x |

| 7.4x |

| 9.0x |

| 7.6x |

| FCF interest coverage |

| -13.7x |

| -12.1x |

| -0.5x |

| -24.7x |

| 3.9x |

| -1.6x |

| -2.3x |

| 1.5x |

| 5.8x |

| 1.4x |

| -4.2x |

| EBITDA/Total Debt |

| 0.3x |

| 0.2x |

| 0.1x |

| 0.1x |

| 0.1x |

| 0.1x |

| 0.1x |

| 0.1x |

| 0.2x |

| 0.2x |

| 0.1x |

| EBITDA/Net Debt |

| 0.4x |

| 0.2x |

| 0.1x |

| 0.1x |

| 0.1x |

| 0.1x |

| 0.2x |

| 0.1x |

| 0.2x |

| 0.2x |

| 0.2x |

Source: Global Payments, Khaveen Investments

In terms of credit analysis, the company’s interest coverage ratios had also declined in the past 10 years but remained positive in 2021. Also, its EBITDA/Total Debt and EBITDA/Net Debt ratios also declined over the period.

Risk: Limited M&A Opportunity Going Forward

As the company acquires EVO Payments, we expect the company’s M&A capability for the foreseeable future until 2023 to be limited following the deal which involved $4 bln in cost and reduces its cash to debt to 0.10x in 2023.

Verdict

To conclude, we believe the acquisition of EVO Payments could be complementary to Global Payments and result in greater revenues of $13.1 bln by 2026 for the combined company. In addition, we expect the deal to have a positive impact on its profitability and forecasted its operating margins to reach 18.3% with cost synergies in 2023. Despite the impact on its financial position with the $4 bln cost, we believe the deal is positive to the company’s value with a net increase of $4.45 bln. Based on analyst consensus, the company has an average price target of $168.70 , representing an upside of 34.8%.

For further details see:

Global Payments: 6% Revenue Boost From EVO Payments Acquisition