SELF - Global Self Storage: A Hidden Gem For Retail Investors

2023-04-27 20:29:37 ET

Summary

- SELF is trading at a deep discount to its NAV which offers a great opportunity.

- The market research provides a peace of mind for retail investor to go long.

- However you look at it, this is a buy.

The self-storage sector is experiencing an unprecedented level of consumer demand, and its income growth has proven to be quite resilient. The sector's demand drivers are non-cyclical and not strongly linked to the broader economy. As a result, the sector has demonstrated consistently strong performance over various market cycles, including exceptional performance during the recent pandemic and the 2008 recession.

Global Self Storage ( SELF ) is an internally managed REIT which owns 12 properties and manages one in secondary/tertiary markets in Midwest and Northeast. It is currently trading at a deep discount to its NAV which presents a great turnaround opportunity to be taken private. There are many articles on this REIT on Seeking Alpha and I find David Brown’s various analysis very close to mine. In this article, I will provide an update to NAV with a scenario analysis and argue why it makes sense to be a buyer of this REIT because of its strong fundamentals. Although it is difficult to predict the future with certainty, and there is always a risk of information bias, based on the data I have collected, I believe that in a worst-case scenario, SELF stock could be valued at a minimum of $7 per share if it were to be sold in the private market.

Market Research

When underwriting self-storge properties, first and foremost, it is essential to research the market. The rule of thumb is that if the 3 miles radius net rentable square feet per capita is below 8 (U.S. Average) then the submarket is considered undersupplied. Based on my findings from Yardi, the average net rentable square feet per capita in the 3 miles radius for SELF’s properties is 7.5 which is great. The average median household income is $86,660 which is also attractive since it means the residents have sufficient disposable income to spend on storage. I found many Multifamily development in many of these submarkets which again is a positive for a self-storage business. I looked at the new supply coming in the 3 miles radius and only found 2 new self-storage properties being developed in two of its 12 locations, which does to some extent bolster management’s claim that they operate in a high barriers to entry markets. However, to be truly certain of how high barriers to entry these markets are, it will take researching if these counties have some sort of zoning or community restrictions on self-storage construction. It is not uncommon to have strong resistance against self-storage in many jurisdictions.

Net Asset Valuation

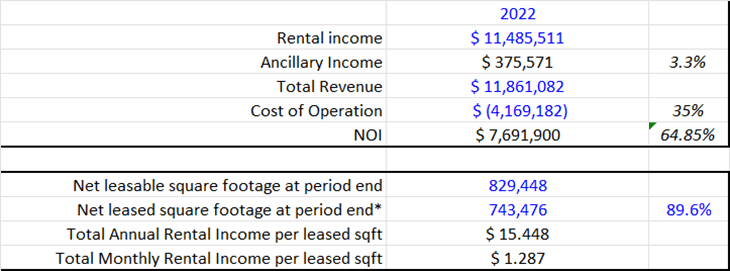

Based on the recent 10-K , and company’s reported rental income, occupancy and total owned net rentable square feet, the monthly rental income per nrsf is at $1.15 at 89.5% occupancy. If fully occupied, it would be $1.28. This is further verified by Yardi’s comp analysis, at average rent/nrsf for a 10x10 non drive-up, non climate controlled at $1.25 in the submarkets where SELF operates. Even though 8% of its storages are Boat/RV units which are rented at lower rent, $1.28 per nrsf seems reasonable considering 33% of units are climate controlled and 59% drive-ups. Please note my below valuation is very conservative, for example, I am only considering 50% of the fair value of investment in securities instead of taking the full amount of $2,366,153.Also, the revenue generated from the managed store(as 3rd party) is not even included in the NAV.

Base Case

-

Rental income Assumption: No growth. Using LTM ( $1.28 per nrsf if fully occupied)

-

Occupancy Assumption: 89.5% based on recent 10-K

-

Property Cost: same as LTM at 35% of revenue

-

Ancillary income: same as LTM at 3% of revenue

-

NOI ends up the same as LTM at $7691,900

-

Cap Rate: 7%

{kind=link}

Result as shown below, is a NAV per share of $8.45, 40% discount to the current share price. Implied cap rate of 11%. This means real estate assets are priced at only $128 per nrsf.

Author made

Worse case

-

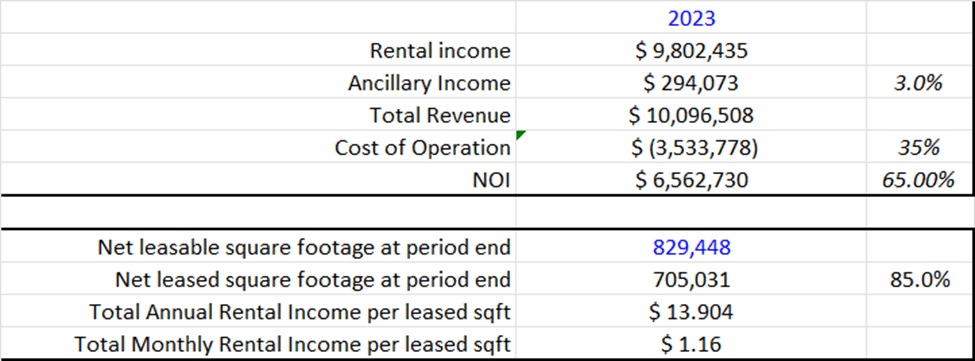

Rental income Assumption: -10% decline ( $1.15 per nrsf if fully occupied)

-

Occupancy Assumption: 85%

-

Property Cost: same as LTM at 35% of revenue

-

Ancillary income: same as LTM at 3% of revenue

-

NOI ends up at $6,562,730

-

Cap Rate: 8%

{kind=link}

Result as shown below, is a NAV per share of $6.11, 17% discount to current share price. Implied cap rate of 9.3%. This means real estate assets are priced at only $94 per nrsf.

Author made

Deep Value

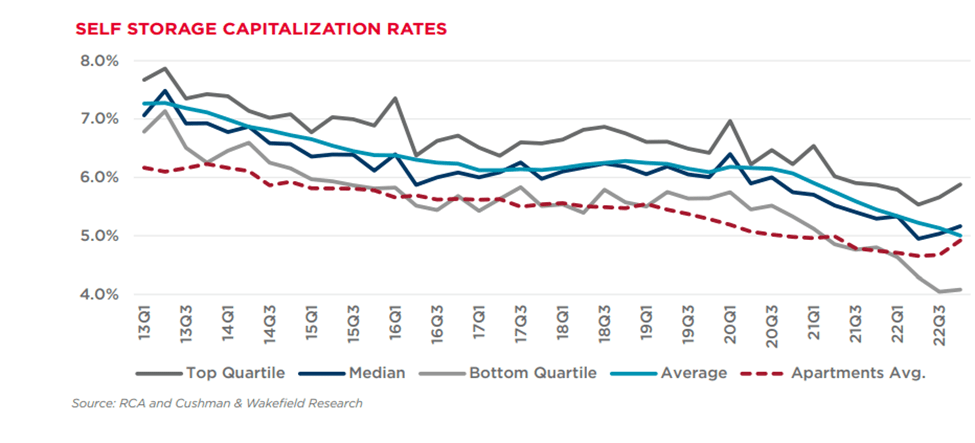

NOI margin at 64% is very low for a self-storage property. Cost could be reduced significantly to boost the NOI to a 70% margin. In today’s market, just to develop a self-storage ground-up, it costs somewhere between $85 to $115 PSF just for the hard cost. There is also significant amount of soft cost and cost of land. In 2019,SELF acquired the property at 70 Erie Station Road, West Henrietta, NY 14586, for $132/SF. Prices have substantially increased since then.

{kind=link}

There is the argument that secondary/ tertiary markets are much less attractive, trading at higher cap rates because of limited population growth. Here is my response to that:

- Cap rates assumed are already very conservative.

{kind=link}

2. According to the managers, if the barriers to entry in these markets are indeed as high as they claim, the risk of new competition is relatively low, which creates the potential for high growth.

Strong Balance Sheet

SELF has a strong balance sheet with EBITDA/Interest coverage ratio of 6.5x while the minimum required usually is around 1.5x. Debt/Total Asset is at 26%, the lowest from its peers. Its LTM EBITDA of around $5M or its cash on hand of around $6.3M would be sufficient to pay for 2023 Dividend payment+ Principal and interest payment on debt.

Why Is There Not Enough Love for SELF?

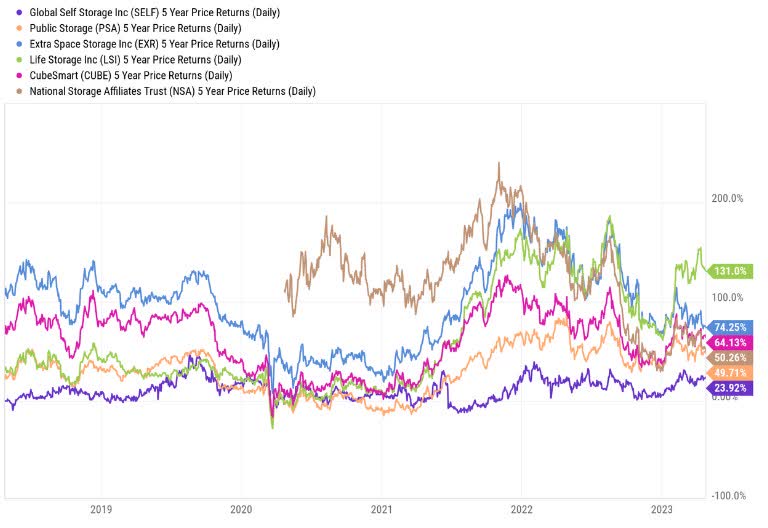

As shown below, SELF has had the lowest 5-year price return compared to the other self-storage REITs.

{kind=link}

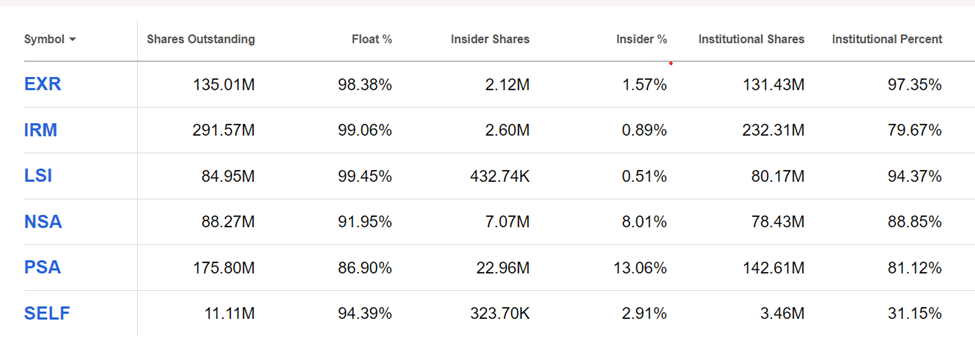

1. One main reason SELF is trading at such a high discount to NAV might be the lack of interest from institutional investors because of its low liquidity.

{kind=link}

2. Investors may not be interested in focusing on secondary or tertiary markets because they may not see sufficient growth potential. Nevertheless, SELF adopts a discerning approach to its acquisition strategy by targeting markets with relatively low self-storage supply per capita and where obtaining new development and permits through local planning and zoning boards is often challenging. This creates obstacles for potential new competitors entering the market, resulting in a greater demand and hopefully more internal growth.

3. Management seems not ambitious enough and has not taken advantage of REITs lower cost of capital vs. private investors. Based on SELF’s current capital structure of low debt and low beta, and assuming cost of debt of 5.5%, ERP of 5.6%, its WACC is less than 5.5%. It shouldn’t be that hard to find value-add opportunities with an IRR greater than 6%. Management’s issuance of 1,289,720 shares at a net price of $4.81 considering the exercised over-allotment options in 2021 has been dilutive to FFO. Even though the net proceeds was used to pay down the line of credit (with a variable and high rate), the interest costs saved have not been sufficient, therefore diluting the FFO in short term. Management could still find a value-add opportunity with an attractive IRR to boost the FFO.

3. Compared to other self-storage REITs that typically have a G&A expense of around 4% of revenue, the G&A expense for this particular REIT is considerably high at 20% of revenue. This significantly lowers the FFO.

Self-Storage Is The Best Performer During Recessions

Self-storage is often considered a recession-resistant asset class for several reasons. During a recession, people may downsize their homes or move to more affordable housing, which can lead to a need for additional storage space. Additionally, businesses may downsize or close, leading to a need for storage space for their assets and inventory. Compared to other real estate sectors, self-storage facilities typically have lower operating costs and lower capital expenditures, which can help to maintain profitability during challenging economic times. Self-storage also tends to have shorter lease terms than other real estate asset classes, which allows for more frequent rent adjustments in response to changing market conditions or unexpected inflation.

How did the 2007-2009 recession impact real estate investments? NAREIT provides the average annual total return for each real estate sector during this period:

- Residential: -6.53%

- Office: -8.16%

- Retail: -12.32%

- Industrial: -18.31%

- Healthcare: +4.92%

- Lodging/Resorts: -4.95%

- Mortgage: -16.34%

- Self-storage: -3.80%

Verdict

SELF stock is a great buy for retail investors who don't have the liquidity constraint that institutional investors have and also a great target to be taken private considering its deep discount to NAV and today's challenging environment for institutional managers to find new opportunities at a reasonable price. SELF's markets are fundamentally strong and management has the competitive advantage to add tremendous value for shareholders.

For further details see:

Global Self Storage: A Hidden Gem For Retail Investors