SELF - Global Self Storage Is An Interesting Company But Also Expensive

Summary

- SELF is a small REIT operating 13 storage space properties in the U.S. northeast.

- The company's management has been conservative and did not jump on the bandwagon of recent real estate and self storage properties speculation.

- With great cost management and fast-growing revenues, the company's operating income and margins exploded since 2020.

- However, in my view, SELF is currently priced for perfection, implying revenue growth of 20% without any corresponding cost increase.

- I believe SELF is a great company to follow, but not to buy at current prices.

Global Self Storage ( SELF ) is a REIT that owns and operates 13 self storage properties in the North East.

The company's income and margins have jumped significantly in the last three years thanks to cost control coupled with fast growing rental rates. On top of that, the company is financially strong and seems to have a conservative management. These characteristics all indicate quality.

However, in my opinion current prices already discount the most optimistic scenario for the future. In this context any negative development, particularly a slowdown in rent price growth, would render the investment expensive.

Although I like the company, I don't see it as a great investment opportunity right now.

Note: Unless otherwise stated, all information has been obtained from SELF's filings with the SEC .

Business description

Self storage in towns and suburbs : SELF owns and operates 13 self storage properties. All of them are located in towns or suburbs in the North East (Connecticut, Illinois, Indiana, New York, Ohio, Pennsylvania, South Carolina, and Oklahoma).

Supply conscious management : The company indicates that it looks for properties in markets where expected supply is constrained. This seems more logical than blindly following demand.

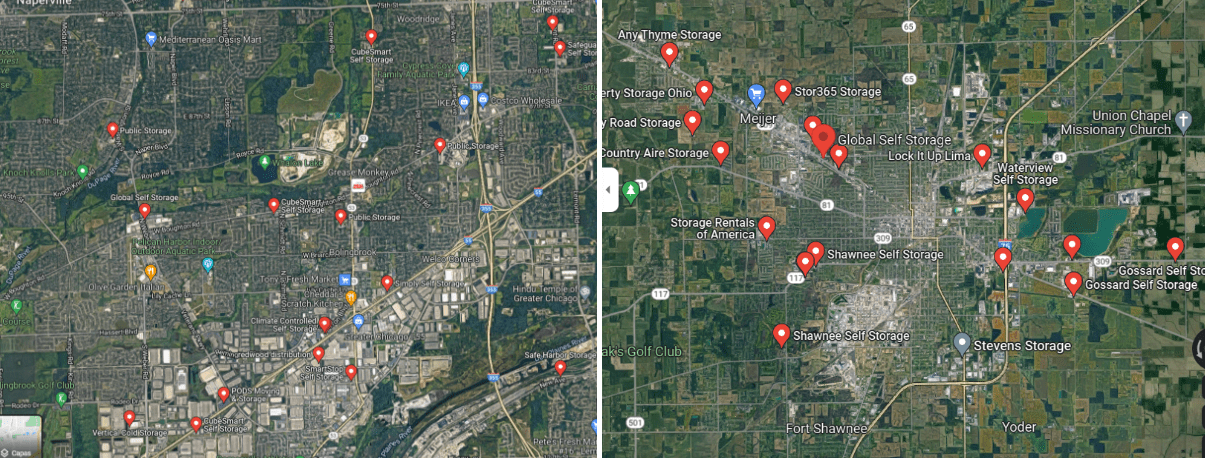

However, a simple study of Google Images does not necessarily reveal a lack of competition. For example, SELF's two largest properties, in Bolingbrook, Illinois (left) and Lima, Ohio (right), are in relatively supplied markets (the red dots in the maps below indicate other self storage businesses).

Self storage properties in Bolingbrook, IL and Lima, OH (Google Maps)

{kind=link}

Conservative capital allocation : Because a REIT has to return most income to shareholders, it becomes difficult to accumulate cash to redeploy in the business. This makes capital allocation much more strategic, because it has to be financed by expensive and risky debt or dilutive share issuance. SELF did not jump into the speculation wagon of 2020 and 2021, with 8 properties purchased in 2013, four in 2016 and one in 2019. Compare this strategy with the explosion seen in construction spending on self storage.

Construction spending on self storage properties (Neighbor.com)

Conservative + supply conscious = value : Value Managers are conservative when allocating capital and that avoid investing when their industry is frenetically increasing supply are value managers.

Low financial leverage : SELF does not have a lot of debt. As of 3Q22 , it holds $16 million in fixed rate notes payable, against cash holdings of $6.5 million and securities (mostly equities) for $2.6 million.

No big shareholder : According to the company's proxy statement for FY22 , SELF's largest shareholder holds 6.5% of outstanding shares, and the managerial team holds 6.9% of the company's stock. In general, I prefer companies with at least one strong owner, especially a manager-owner.

Recent developments

Revenues exploded : SELF's revenues have grown consistently and significantly since the beginning of the pandemic. This has been completely fueled by higher rental rates, given that the company did not increase leasable space. This contrasts with relatively more stagnant revenues between 2017 and 2020.

Great cost management and high operating leverage : SELF's income from operations grew even faster than revenues thanks to amazing cost management and operational leverage. Although some costs provide more leverage (like non inflation adjusting depreciation), other costs are surprisingly below their pre-pandemic levels, like SG&A.

Valuation

A growth multiple : SELF is trading at an adjusted P/E ratio of almost 16x to operational profits ("adjusted" meaning after subtracting unrealized losses from its securities portfolio). Such a multiple implies growth.

Growth from rental increases : Because the company has not acquired or developed new properties recently, all growth has come from rental price increases that are above cost increases. For the 9M22 period, costs are already rising by 8%, in line with inflation.

Revenue growth is not slowing down : As of 3Q22 and 9M22, same store prices per square foot were still growing 18% and 19% respectively, YoY. These levels are both well ahead of inflation and well ahead of national average rental prices for self storage, which fell 2% in 2022 according to Storage Cafe .

Costs are starting to pick up steam : From the charts above, a faster rate of increase can be perceived at the CoGS level (cost of operations as called in SELF's financial statements).

How sustainable is revenue growth? : Normal economic theory indicates that if national inflation is 8%, rental prices cannot keep growing at 20% rates forever. The recent increases are being felt at the occupancy level, falling 4 percentage points in 3Q22 compared to 3Q21.

The company is priced for perfection : With a market cap of $56 million, the company would need to grow operating profits by 64% in order to return 10% on its price (from the current $3.4 million TTM). Even if costs are completely frozen, implied revenue growth of 20% is not likely sustainable with current inflation and the trend in occupancy levels.

Longer-term considerations

Capital allocation in another cycle : There has been a lot of supply growth in the self storage space. Some players are heavily leveraged. This implies that the industry should reach a downward capital cycle at some point. With almost $10 million in cash, SELF's management may be able to prove that it can allocate capital countercyclically. This is one of the most (if not the most) important characteristic to evaluate from management, according to Warren Buffett.

If the company proved that it can allocate capital during the downward portion of its industry's cycle, I would confidently recommend it even at current multiples. This has not been the case yet, so I recommend waiting.

Conclusions

Although I like some characteristics of SELF's management, and the company has done very well in recent years, I believe it is currently priced for a very optimistic scenario that may not materialize.

I believe SELF is a great stock to continue following. On the one hand, a lower price for the stock would imply lower risk in terms of growth assumptions. On the other hand, as the industry's cycle advances, SELF's management could prove outstanding countercyclical capital allocation abilities, which would justify today's multiple.

For further details see:

Global Self Storage Is An Interesting Company But Also Expensive