GWRS - Global Water Resources: Share Dilution And Dividend Concerns Worry Me

2023-10-03 00:26:50 ET

Summary

- Global Water Resources offers solutions for water scarcity, but its financial health and management strategy raise concerns for dividend investors.

- GWRS has seen consistent growth in active water connections and recent financial achievements, but slowing dividend growth and shareholder dilution are worrisome.

- The company's cash flow issues, reliance on issuing new shares, and lack of stability in free cash flow make it a risky investment for dividend seekers.

As we struggle with water scarcity, companies like Global Water Resources ( GWRS ) are stepping up to the plate, offering solutions to manage this precious resource. But while GWRS's mission is noble and its approach interesting, is it a worthy investment? Does its financial health and management strategy align with the interests of shareholders, especially those eyeing dividends? I don't think so.

GWRS is a monthly dividend payer, which may be attractive for some. Also, the company's consistent growth in active water connections and its recent financial achievements further bolster its appeal. However, beneath the surface, there are underlying concerns. From slowing dividend growth to significant shareholder dilution and pressing free cash flow challenges, GWRS's financial strategies raise questions about its long-term potential for dividend investors.

Company Overview

Global Water Resources aims to address challenges posed by water scarcity and offers integrated water resource management services. GWRS focuses on the holistic management of water resources, encompassing the entire water cycle, from sourcing and treatment to distribution and recycling.

GWRS's approach, named "Total Water Management" aims to conserve water by using water for the right purpose. This philosophy may be especially beneficial in areas where water supplies are scarce such as in Maricopa and Pinal County, Arizona, where it serves 60,291 total active water connections. These water connections have grown at a CAGR of 7.4% from 2018 to 2023. The company operates in these counties in Arizona exclusively.

GWRS has one operating segment, but reports revenue under Water services, Wastewater recycled water services, and occasionally Unregulated revenues, separately.

{kind=link}

The company strengthened its top and bottom lines last quarter, and also reported development in its infrastructure via a mix of capital expenditure and acquisitions.

GWRS achieved new records in terms of volume pumped, attributed to high temperatures. The brand's water connections also grew by 8%, surpassing the 60,000 mark. This growth was bolstered by the acquisition of Farmers Water Company , which added 3,325 active water service connections. Furthermore, the company invested $13.7 million in infrastructure improvements.

{kind=link}

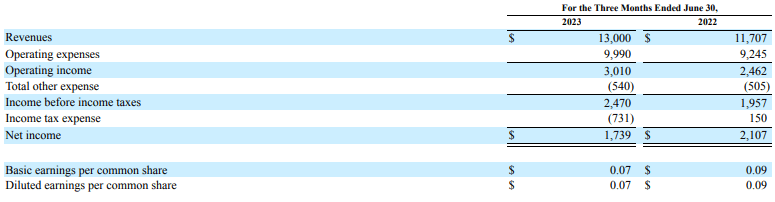

Revenue stood at $13 million, marking an 11% increase from Q2 2022. Operating expenses rose by 8.1% to $10 million in Q2 2023. The net income for the quarter was reported at $1.7 million or $0.07 per diluted share, and the adjusted EBITDA saw a 10.5% increase, reaching $6.7 million. Additionally, the company has secured its financial position by extending its $15 million line of credit through July 2025.

To give you a snapshot of management's approach to dividends and where this thesis is going, the company has paid out dividends consistently every month. GWRS has also made consistent dividend increases over the years, but the momentum of these increases is slowing down. Not only that, but the dividend increases are also becoming more infrequent.

Below is a chart of all the cash dividends paid since the company started paying them.

{kind=link}

The trend of smaller dividend increases being made more infrequently over time might be easier to see on the chart below. If the line is descending, it indicates that the rate of dividend increases is slowing down, and vice-versa. If the line dips below 0%, it indicates a year where the dividend was lower than the previous year.

I think the reason for the slowing dividend growth can be chalked up to a mix of a lack of free cash flow available to investors, management's preference for paying down debt and making acquisitions, and spending on CAPEX. But more broadly, investors' interests appear to be near the bottom of management's priorities, if they are one at all, as we'll see throughout this analysis.

Finances

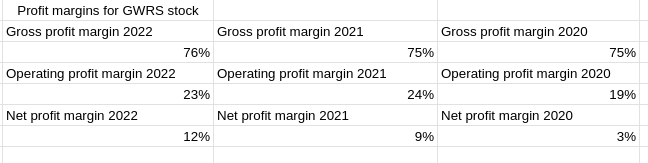

Giving GWRS some credit where it's due, it has consistently improved its top and bottom lines over the past three financial years, dug itself out of the hole attributed to COVID, and managed to substantially improve its net and gross profit margins.

{kind=link}

Some notable highlights from its income statement over the last three years is that net income rebounded to $5,506,000 in 2022, up from $1,105,000 in 2020. Retained earnings also stood at $12,395,000 in 2022, some of that which could be used for immediate dividend increases in the near future.

However, these accounting measures don't tell us the full story. When one examines its cashflow statement some of its issues come to a head. In short, GWRS's cash burn and its inability to grow cash flow fast enough are the limiting factors to its dividend growth as well as total return potential. Existing shareholders are also being diluted in process of receiving dividends, giving with one hand and taking with another.

In 2021, operating cash flow increased 40% from 2020 to $20,386,000. In 2022 operating cash flow increased by only 14% from 2021 to $23,336,000. This suggests much of the increase in cash flow was likely reverting back to its average, rather than purely an improvement. We will need to see this year's result to get a clearer picture.

GWRS is spending a huge amount of cash of investing activities and CAPEX. In 2021, it spent $20,319,000, an increase of 115% from 2020. Then in 2022 it spent $34,188,000, an increase of 68% from 2021.

All of this might be justified if one thinks it may help improve shareholder equity in the future. But the opposite of this is actually occurring. GWRS is financing its CAPEX and acquisitions, as well as paying dividends overwhelmingly from issuing new shares.

Average diluted shares outstanding increasing from around $20 million to $120 million is an extremely high price to pay in my view. Think of it this way: If you owned 1 million shares out of the original 20 million, you owned 5% of the company. Now that the number of shares has increased to 120 million, your ownership stake has now dropped to less than 1% without you selling any shares.

Furthermore, now that the dividend pool is much larger, dividends are also distributed among a much larger number of shares, which makes it far harder for the company to increase the dividend per share. It might be okay if the company was raking in cash like some Dividend Kings or Aristocrats but GWRS far from one of those.

Because in addition to its dilution problem for shareholders, it also has a serious cash burn and cash generation issue.

To give you an idea of its cash burn, in 2020 it had $12,210,000 worth of cash and cash equivalents on its balance sheet. Its net change in cash was -$7,862,000 in 2021 and then -$5,881,000 in 2022.

It might be easier to see the volatility of its cash position using the chart below.

GWRS arguably wouldn't be in the same exact position if its free cash flow was higher, which has shown some strong volatility. It notably fluctuates around the zero-line quarter-to-quarter which in turn necessitates it to raise funds from both a mix of debt and equity to pay dividends and keep the lights on.

Dividend potential

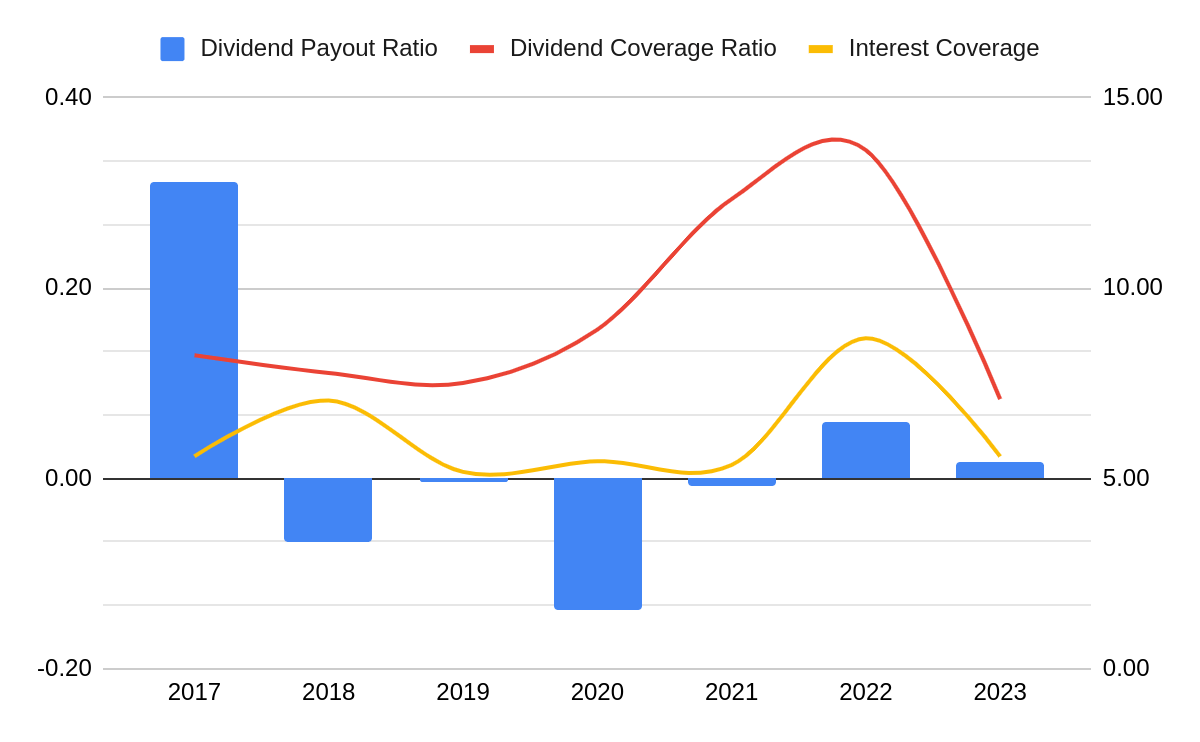

When one looks at GWRS's dividend potential superficially we can make some observations based on its earnings alone.

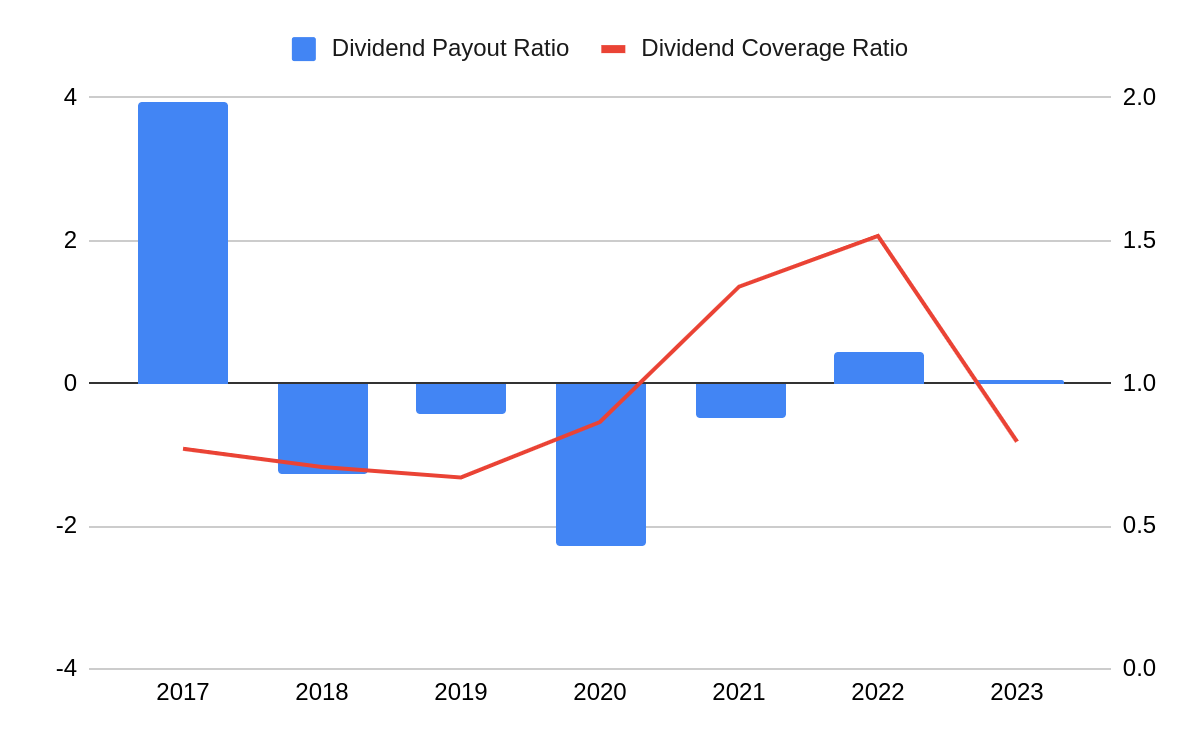

There were some years with negative spikes in dividend payout ratio, but consistently positive dividend coverage ratios and interest coverage across most years suggest that dividends are generally safe.

{kind=link}

When the data is normalized to account for outliers, we can see a healthy inverse correlation between the dividend payout ratio and dividend coverage ratio, with no alarming divergences of any sort that would suggest an issue with dividend safety.

{kind=link}

However, these ratios use accounting profits, and dividends are paid out free cash flow available to investors. In the graph below we see a mix of good and bad.

The financial debt to EBITDA ratio implies it would theoretically take 5.4 years for the company to pay off all of its debt using EBITDA alone, and assuming it spent money on nothing else. This ratio is also in downwards trend, suggesting long-term improvement. But let's not forget that it's paying off its debt through issuing equity, which disadvantages existing shareholders.

Free cash flow to equity, which represents the amount of cash available to shareholders after all expenses and reinvestments are paid, has also consistently been above total dividends to paid quarter-to-quarter. But again, it also oscillates substantially above and below the zero-line.

The instability of this cash flow measure means it would be risky to increase the amount or frequency of dividend payments, even if it was a priority for management. This is also the main reason I believe that we've observed a slowdown in this regard for both measures. The ongoing dilution also makes it harder to keep these dividend increases going, while also destroying shareholder value.

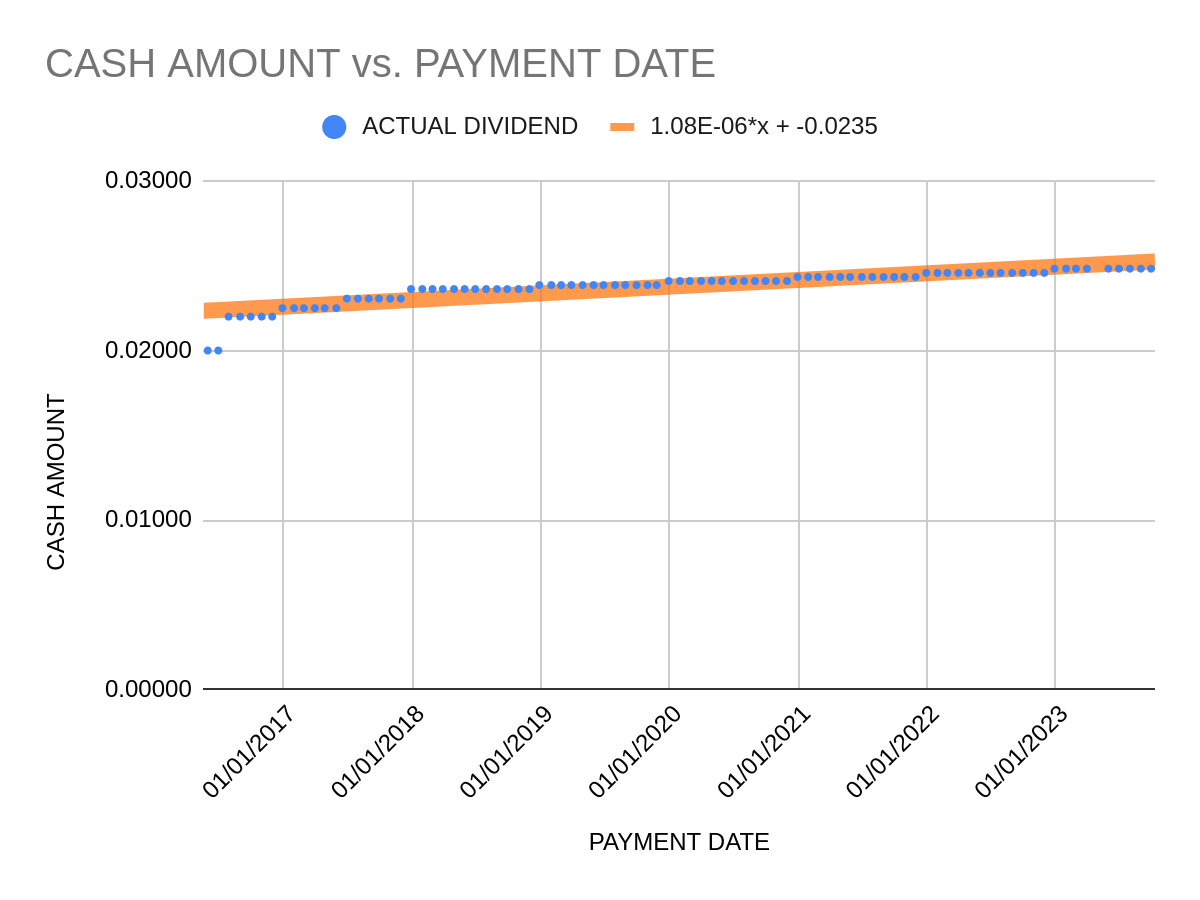

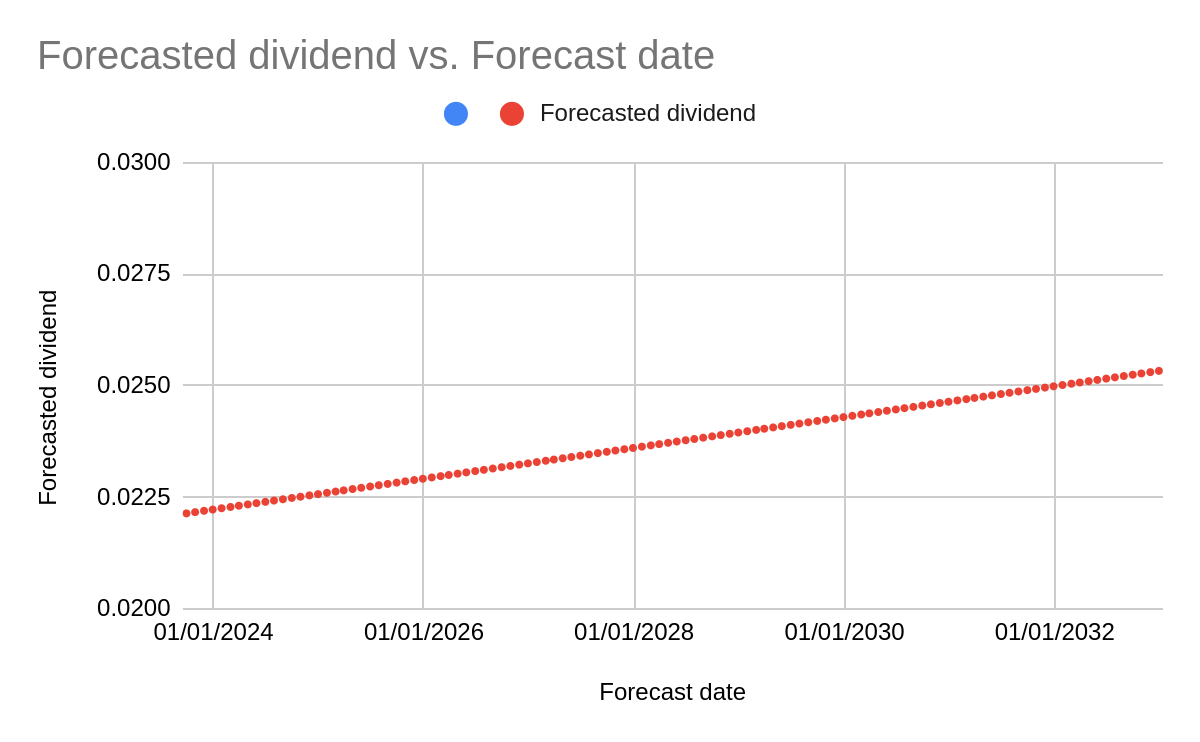

Nonetheless, if we assume that dividends will continue at exactly the same rate they have been, below is a line of best fit which forecasts what future dividends could look like.

{kind=link}

Note that the above should be taken with a large pinch of salt. It's essentially saying "If all else is equal, here's a dividend forecast for the next ten years". But of course, we all know that all else is not equal. This linear regression line just points us into vaguely the expected direction if things continue precisely the way are into the future. It also accounts for an 11% average expected margin of error.

Risks

GWRS operates exclusively in Maricopa and Pinal County, Arizona. This geographic concentration exposes the company to local economic downturns, and regulatory changes that could disproportionately affect its operations compared to more geographically diversified competitors investors can invest in. And there's also no guarantee that it will always be able to source sufficient water to meet the demand of the areas it serves.

Also, while the company has been paying down its debt, it's essential to note that it's doing so by issuing equity. If the company cannot manage its debt levels efficiently, it might face higher interest costs and further financial strain and pressure on issuing dividends.

Issuing shares can only work for so long before people begin to doubt the value of those shares, as we're illustrating now. Its diluted EPS of 0.07 at the time of writing is very telling.

For dividend investors especially who are concerned with total return potential as well as dividend growth, I feel that it would be too risky to have their capital eroded for a speculative prospect of making more later.

Conclusion

GWRS shows promise as a company with its improving top and bottom lines and margin recovery, but it hasn't been able to address its pressing free cash flow problem. Management's priorities can be inferred to be CAPEX and acquisitions, which makes sense given that it's still a relatively young company.

The fact that dividend increases are slowing down, and the dividend increases are becoming smaller, along with what I consider egregious shareholder dilution means there's little sense to me for investors to buy shares now. A lack of stability in free cash flow means that cash for future investments will need to come from either debt or equity, and it's using equity sales to pay off its debt. We can therefore assume this trend of shareholder dilution will continue, which also tarnishes its potential as a dividend stock unless it manages to substantially turn its cash flow situation on its head. A quick turnaround seems unlikely, given that water connections have grown at a CAGR of 7.4% from 2018 to 2023.

It has an interesting and noble business model, but I think we can afford to sit on the sidelines and watch if it can get its cash flow and dilution issues under control before hopping on board.

Existing shareholders can therefore weigh up if their money could be better invested elsewhere, and potential dividend investors can steer clear.

For further details see:

Global Water Resources: Share Dilution And Dividend Concerns Worry Me