UMC - GlobalFoundries: A Unique Company With Potential Going Forward

2023-06-20 14:26:35 ET

Summary

- GlobalFoundries is well-positioned in the semiconductor foundry market, focusing on specialty process technology and benefiting from its manufacturing locations in favorable jurisdictions.

- The company's future prospects highlight the potential for generating a 12% annualized total return, even at today's share price.

- Profitability is increasing at a steady pace as the company continues to scale and even take market share.

- Investors can consider options strategies for downside protection and income generation while waiting for a better entry point or the anticipated growth period to improve the valuation.

Thesis

The share price of GlobalFoundries Inc. ( GFS ) is currently fairly valued while the company waits out a period of stagnant growth. The future is showing green shoots emerging and investors could soon be presented with a buying opportunity. The company finds itself in a unique position, being the only major pure-play semiconductor foundry company with all of its manufacturing locations in favorable jurisdictions and its headquarters in the U.S. This comes at a time when the United States and the European Union both brought to fruition their respective chip acts, with which GlobalFoundries and the industry as a whole are set to benefit strongly. Although the company is presently unable to sufficiently compete in the node scaling race, its strategy of maintaining a strong position in specialty technology platforms seems wise.

The Onshoring Advantage

Major competitors, including Taiwan Semiconductor Manufacturing Company Limited (TSM), are hastily investing in future fabs to be located in the U.S. and EU. These fabs are coming online starting from early 2024 but McKinsey anticipates key challenges for U.S fab construction due to factors including a shortage of construction talent, a greater emphasis on sustainability, supply chain complexity, navigating federal and local incentives and difficulties with performance management and execution.

McKinsey & Company

Meanwhile, GlobalFoundries already has all of its fabrication foundries based in the north-eastern United States, Germany and Singapore. The importance of the existing location factor cannot be overstated as customers are currently searching for foundry partners that are insulated from supply-chain and geopolitical issues. Research shows a huge discrepancy between the regions where most of the semiconductor supply comes from and the regions where most of the demand is. Specifically in the U.S., the 14% of semiconductor supply from the region pales in comparison to the 34% share that the region demands.

McKinsey & Company

The deal with General Motors Company ( GM ) shows the automaker is looking to secure U.S.-made processors that will enable it to avoid the factory-halting chip shortages that kept millions of cars from being manufactured during the pandemic. Another recent deal with Lockheed Martin Corporation ( LMT ) formed a strategic collaboration to advance U.S. semiconductor manufacturing and innovation and to increase the security, reliability and resiliency of domestic supply chains for national security systems.

Additionally, the accreditation from the U.S government which was enabled by the GlobalFoundries fulfilling the DoD requirements for having stringent security processes, equipment, and oversight in place to accept and protect sensitive information and manufacture trusted chips in a way that ensures they are secure and uncompromised, was another display of trust from one of the most stringent institutions out there.

It becomes apparent that there is a strong demand within western institutions to have a semiconductor foundry partner that best adheres to security and reliability requirements. GlobalFoundries is continuing to show that it is the partner of choice for these customers.

Foundry Expansion

GlobalFoundries is continuing on its path of expanding its footprint in the U.S., the EU and Singapore. The company announced plans in July of 2021 to build a new fab in upstate New York, adjacent to its existing Fab 8 facility, doubling capacity when ready. $1 billion is also being invested at the existing fab. In May 2023, news broke that the company completed the purchase of 800 acres of land needed for the development of the second fab on the Fab 8 campus.

Just a few weeks ago, GlobalFoundries and STMicroelectronics N.V. ( STM ) finalized an agreement for a new 300mm manufacturing facility in France. The agreement supports the company's $20 billion revenue ambition while benefiting strongly from the European Chips Act in the form of significant financial support for the €7.5 billion CapEx (currently ~ $8.2 billion).

Much of the current CapEx is going towards foundry expansion at the existing Fab 7H facility in Singapore. During the Q1 2023 earnings call , the CFO David Reeder explained to an analyst asking about CapEx, the following:

So first let me start with just by saying that the majority of that CapEx is really related to Fab7H on our campus there in Singapore. And really giving us the capability longer-term to be able to satisfy some of these LTAs that we're signing today, as well as some of those LTAs that we've signed in the past.

When we talked about our expansion plans, we talked about increasing our wafer capacity from about 2 million wafers in 2020 to about 2.4 million wafers in 2021 to about 2.6 million wafers last year to about 2.8 million wafers this year to north of 3 million wafers in 2024 and we're actually very much on track to deliver that capacity.

The Foundry Market

The pure-play semiconductor foundry market is a very concentrated one with 79% of the market being captured by just three companies, with GlobalFoundries having the third largest market share globally. During the period of Q3 2021 - Q1 2023, from the 5 major players, only TSMC and GlobalFoundries increased their market share. TSMC is without a doubt the behemoth of the industry and dominates the market for bleeding-edge process technologies and is taking market share from Samsung Foundry, a part of Samsung Electronics Co., Ltd. (SSNLF).

Counterpoint Research

The semiconductor foundry market is expected to grow at a CAGR of 7.34% during the period of 2023-2028, growing from $143.12 billion to $203.94 billion.

Mordor Intelligence

The Technology Platform

Due to the enormous scale and the deep EUV domain knowledge advantage that TSMC has, GlobalFoundries delivers its focus largely on specialty markets. As we can see, the revenue mix has become considerably diversified over the past year; certainly a favorable development from relying heavily on the smart mobile devices market in the past.

GlobalFoundries Inc.

The company offers FinFET, RF SOI, Silicon Photonics, SiGe and Feature-Rich CMOS solutions within its technology platforms. In particular, its RF SOI (Radio Frequency Silicon-on-Insulator) process technology leads the market with a 75% share in top premier smartphones in RF FE, Audio & NFC while being the first fully qualified high-volume RF SOI foundry solution on 300mm wafers.

The FDX FD-SOI platform is an advanced semiconductor technology that offers a compelling combination of performance, power efficiency, and cost-effectiveness. Its fully-depleted silicon-on-insulator architecture, dual-voltage operation, RF and analog integration capabilities, low-power design, backward compatibility, and industry ecosystem contribute to its appeal for various applications, particularly in the IoT, automotive, and mobile markets. Markets where GlobalFoundries already has a strong footing, and is looking to differentiate itself.

GlobalFoundries stepped out of the scaling race at the 12nm FinFet process technology to mainly focus its resources on these specialty markets. We observe this strategy to be prudent, as playing catch-up with TSMC would be a very costly and risky endeavor compared to establishing its own leadership within these specialty semiconductor markets. Fab 7 in Singapore is dedicated to building and testing feature-rich radio frequency ((RF)), embedded memory and analog and power solutions with technologies ranging from the 130nm to 40nm nodes. As we showed above, this is also where GlobalFoundries is currently allocating a large amount of CapEx.

Increasing Profitability

The company has seen very positive developments in profitability over the past 5 years. The gross margin, EBITDA margin and ROE are all trending upwards over the time period. It is important to note that in October of 2021 the company IPO'd , raising ~ $2.6 billion. The investments the company was able to make with the IPO proceeds are seemingly bearing fruit and adding to its scale and continuing to boost profitability. We anticipate that the continuing investments the company is making, especially in specialty process technology, will continue to improve profitability metrics through pricing power and scale.

Seeking Alpha

Valuation

At the time of writing, the share price is $62.46 with an enterprise value of ~ $34.2 billion. The TTM free cash flow is negative $994 million. However, a large portion of the CapEx is going towards growth CapEx, which should reward shareholders in the future.

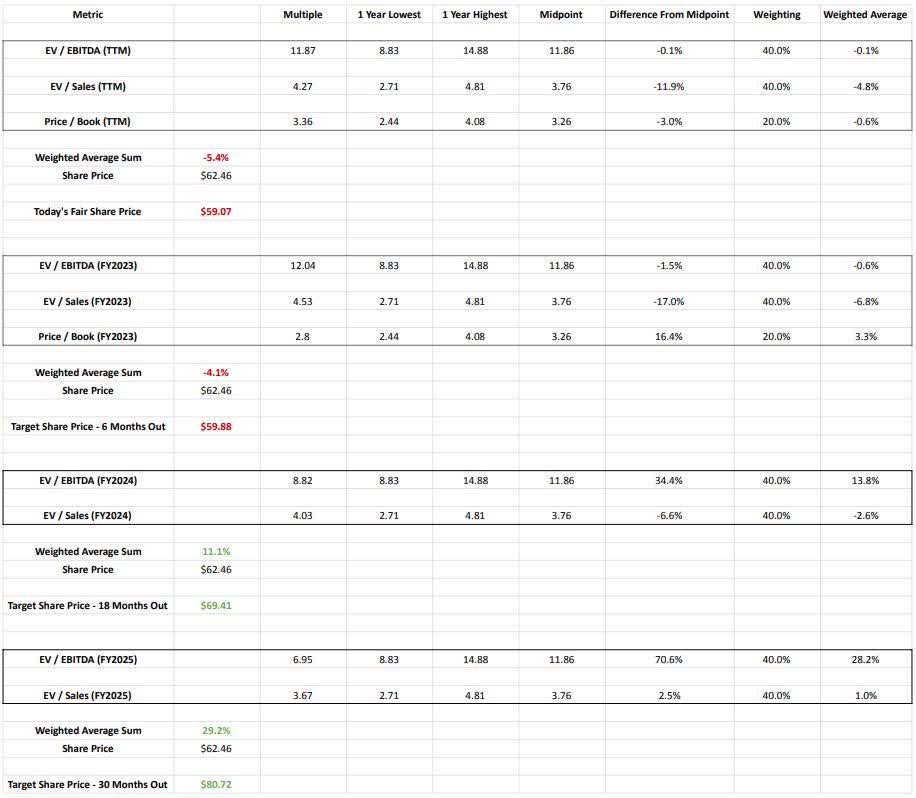

We will use the trailing twelve month EV / EBITDA, EV / Sales and Price / Book metrics as valuation metrics to compare the current valuation to historical levels.

The aim is to find the lowest and highest multiple the stock has traded at in the past 1 year. We are using data from the past 1 year, as that covers a relatively stable valuation range and doesn't include large swings in valuation that came to be directly after the IPO. From the lowest and highest multiple points of each of the three metrics, we will calculate the midpoint. We can now see the difference in share price between the current price and the price that shares would be if the midpoint of each metric was to be reached again. In other words, if the valuation was to revert to the historical mean.

Now we just have to assign a weighting to each metric and calculate the weighted average of each metric. We will attribute a weighting of 40% to both EV / EBITDA and EV / Sales as these metrics focus on the underlying business profitability and growth in relation to valuation, which is what we primarily want to focus on. We are attributing a 20% weighting to the Price / Book metric as it showcases the value of the underlying shareholder equity in this asset heavy business.

With the current share price of $62.46 and a weighted average sum of -5.4%, we calculate today's fair share price to be $59.07 ($62.46*0.946).

Now that we have our basis of comparison, we will seek to take the forward multiple estimates of each of the three metrics and compare that to the historical valuation trading range. The forward multiples in conjunction with the historical valuation range of the business can give us a good indication of what the fair value of the share price will be at the end of the fiscal year, based on our model of mean-reversion. This will take into account analyst expectations of the industry moving forward, macro conditions moving forward, the performance of the business itself on top of the valuation range the market has historically given the business.

With the current share price of $62.46 and a weighted average sum of -4.1%, we calculated our target share price at the end of FY2023 (~ 6 months from now) to be $59.88 ($62.46*0.959).

Going further into the future, we will remove the Price / Book metric as the factors that determine an accurate book value this far out simply become too murky. We don't want to have this distort our valuation model and therefore we will stick with EV / EBITDA and EV / Sales metrics going into forecasts for FY2024 and FY2025.

For both FY2024 and FY2025, EV / EBITDA and EV / Sales multiples are calculated by extrapolating forecasted non-GAAP EPS growth and revenue growth, as we anticipate both non-GAAP EPS and EBITDA to grow at very similar rates and enterprise value to remain constant, if the share price was to remain constant.

{kind=link}

Our model shows the business to currently be slightly overvalued. Based on our calculation of the future valuation, the forecast looks brighter and there is a case to be made for generating a ~ 12% annualized total return going forward. Since the IPO, earnings and revenue estimates were always beaten , so there is a good chance that actual future earnings will come in higher than expected, raising the price target further.

With a current share price of $62.46, risk-averse investors, or investors that desire income while they wait out a flat growth period, can profit from the relatively high IV by writing the 19th January 2024 $65 strike call option, for a current mid-price of $6.90, to open a covered call position. This strike price is just above the modeled fair value price of today, and with the generated premium, presents a maximum profit of $9.44 ($71.90 - $62.44). This strategy would provide ~ 11.1% downside protection. In addition, the annualized return of just the option premium would be ~ 18.8%. If the share price increases above $65 and the shares are called away, the annualized return of just the share price increase would still be ~ 6.9%. Combined, the total annualized return would be ~ 25.7% in that scenario.

Another lucrative strategy would be to write the 19th January 2024 $60 strike put option, for a current mid-price of $5.75, to open a cash secured put position. This strategy would in effect provide the investor with a $54.25 entry price, if the share price is lower than $60 by expiration day. Investors could also see this as providing ~ 13.1% downside protection from the current share price. The total annualized return of this strategy would be ~ 16.4%.

Risks

Undeniably the biggest risk for GlobalFoundries is having TSMC encroach in the niches where the company is investing heavily. TSMC certainly has a vast amount of resources to deploy as they wish, although keeping up the market leadership in the node race is a costly endeavor, minimizing the risk of strong and targeted intrusion.

The cyclicality of the industry can lead to deeper than expected business cycle contractions. During industry downturns, there may be excess capacity and reduced demand for foundry services, leading to pricing pressures and underutilization of manufacturing facilities.

The business model is very capital intensive. Free cash flow can at times be negative, or low, resorting to capital markets to finance operations and the lack of ability to distribute capital to shareholders. Major competitors are TSMC, Samsung Foundry, Intel Corporation (INTC), United Microelectronics Corporation ( UMC ) and SMIC. Major competitors are continuously ramping up CapEx in the race to increase market share and there is a risk that GlobalFoundries is unable to keep up with the CapEx needed to remain competitive. However, this risk is also mitigated due to the company having the third largest market share as of now.

Advanced Micro Devices, Inc. (AMD), Cirrus Logic, Inc. (CRUS), Infineon Technologies AG (IFNNY), Marvell Technology, Inc. (MRVL), MediaTek Inc, NXP Semiconductors N.V. (NXP), Qorvo, Inc. (QRVO), Qualcomm Inc. (QCOM), Samsung Electronics Co., Ltd, and Skyworks Solutions, Inc. ( SWKS ) are the ten largest customers , representing 70% of wafer shipment volume in 2022. If any of these customers is to move to a competitor's foundry, it would have a material impact on the business.

Conclusion

GlobalFoundries is establishing a strong position in certain niches within the semiconductor foundry market. Our view is that management is taking prudent steps with the resources it has to deepen its domain knowledge within specialty process technology. The company is not overextending itself into more capital intensive and competitive platforms. Its existing and expanding manufacturing footprint within in-demand jurisdictions, provides a strong competitive edge and offers customers something unique. Nevertheless, our valuation model indicates that the company is currently slightly overvalued, and will continue to be so in the near future if the share price remains the same. Investors who have not yet initiated a position could benefit from waiting for a slightly better entry point, or consider the options strategies outlined above. As such, we are assigning a hold rating to the stock.

For further details see:

GlobalFoundries: A Unique Company With Potential Going Forward