GSAT - Globalstar: Supply Issues But Apple-Related And IoT Strengths

Summary

- Globalstar has started to recognize some of the revenues associated with the partnership with Apple to enable the iPhone 14 to send emergency messages through its satellites.

- This trickle in revenues could turn into a river with the launch of the direct-to-satellite service and positively impact the fourth quarter results.

- However, the company is suffering from supply chain issues which are not only creating revenue shortfalls in its core business but also leading to more losses.

- Thus, offering a mixed picture, this can be a trading opportunity, which I further substantiate using price-to-sales valuations.

- Depending on whether supply issues are solved this year, this stock is also a long-term hold, thanks notably to strength and product differentiation in commercial IoT.

Last year has seen the satellite communications services provider market undergoing transformational change after Apple (NASDAQ: AAPL ) partnered with Globalstar ( GSAT ) and the possibility of Samsung (OTCPK: OTCPK:SSNLF ) entering into a collaboration with Iridium.

With the iPhone 14 direct-to-satellite service as I explained in an earlier thesis in September, Globalstar stands to benefit from the majority of the $450 million that Apple has earmarked for the project as well as from the expansion of its core business. Hence, revenues for the fiscal year 2022 which ended in December could significantly increase compared to 2021 as I will show later.

In these circumstances, its stock losing more than $1 (or more than 40%) of its value since early November is quite challenging to understand for those who have put in their money.

Hence, for investors, the aim of this thesis is to identify the reasons for this downside, namely by focusing on the supply chain and profitability, but, first, I provide some insights into the Apple partnership.

Apple Partnership Translating into more Revenues

For those who are not aware, Apple is providing emergency communications in the form of an SOS call for both its iPhone 14 and iPhone 14 Pro models. The service makes use of Globalstar's constellation of LEO or low-earth orbit satellites.

This was a big development for this company with a 30-year track record in the satellite sector, namely for its SPOT family of products which provides emergency communications, personal messaging, and location-based tracking services. Furthermore, SPOT enables data transmission using specially conceived mobile devices called satellite phones which have now been extended to the latest generation iPhone ecosystem.

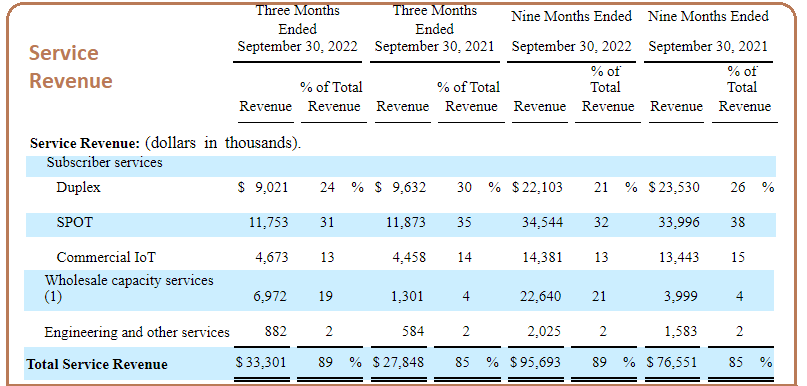

This Apple partnership has contributed to an increase in service revenues by about $5.5 million (33.3 million - 27.8 million as per the table below) in the third quarter of 2022 (Q3). This is 15% more than the same period last year and has been accounted for in the wholesale capacity segment.

Service Revenue for Q3 (seekingalpha.com)

{kind=link}

Looking ahead, the rest of the revenues should reach the income statement only as the services are deployed according to an SEC filing by Globalstar dated September 7. For this matter, there are also some performance obligations associated with the project which determine the timeline of the payments made by Apple to the satellite company. This implies that getting the full payment can take time, the reason being that in order for a smartphone to connect to a communication device thousands of miles away into space, there is a need for satellite coverage and activations on the network. Also, as part of the agreement, Globalstar has to upgrade some parts of its infrastructure and even construct/launch new satellites.

Supply Chain Issues and Profitability

Thus, part of the reason for the stock's volatility could be related to investors having been disappointed by the revenue being too little (only about $5.5 million while the talks were about hundreds of millions of dollars). For this purpose, the start of the stock's downturn somewhat coincided with the release of Q3's financial results at the beginning of November.

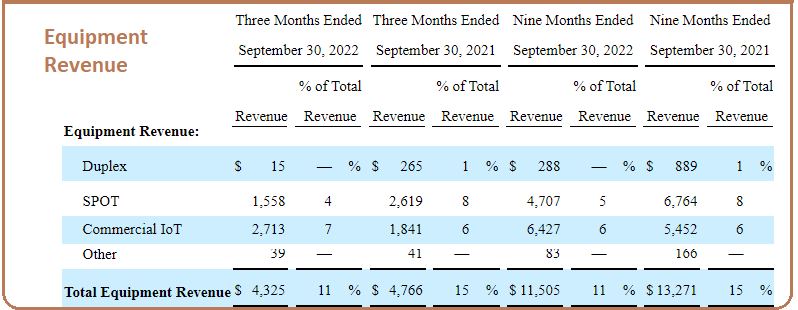

However, the main reason for investors' pessimism could be the supply chain problems faced by the company and which have adversely impacted subscriber equipment sales. As a result, these decreased by $0.4 million with respect to Q3-2021 as pictured below. This is significant as it represents about 10% of the $4.3 million of the total equipment revenue seen for Q3.

Equipment Revenue for Q3 (seekingalpha.com)

{kind=link}

Looking forward, since this is a business that is driven by device sales, be it for satellite phones or Commercial IoT (Internet of Things), lower equipment sales implies fewer subscription sales. This may in turn result in lower service revenues for the fourth quarter. As a matter of fact, supply chain issues have already adversely impacted Q3's subscriber-driven service and activations for many of the company's core products, and had it not been for the Apple partnership, there could even have been a regression in revenues, instead of growth.

There is also the impact on profitability.

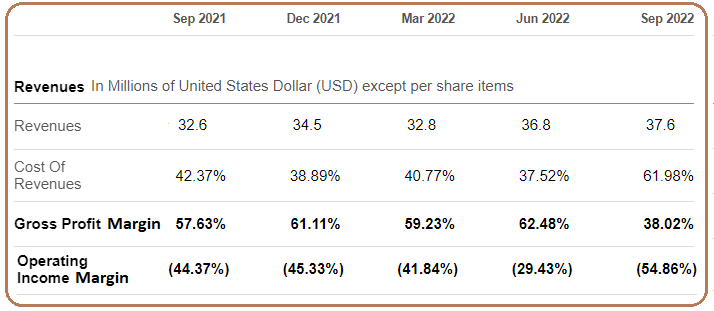

Now, as a manufacturing company, Globalstar does have to incur some fixed costs, and supply chain challenges also reverberate into higher raw materials (components) costs as well as additional shipping expenses. These have all propped up the cost of revenues to 62% resulting in a r ecord-low gross margin of 38% as shown in the table below.

Quarterly Income Statement (seekingalpha.com)

{kind=link}

Therefore, as a result of lower revenue relative to fixed costs, profitability has been impacted significantly with the company missing EPS by $0.10.

Now, looking deeper into the supply chain challenges, these were due to component shortages which have constituted a headwind over the last quarters, preventing Globalstar to produce its most popular devices, both for SPOT and IoT. According to the corporate report, some of the issues had been resolved as of November 2022, with normalization expected only this year.

Valuations and the IoT Growth Driver

Therefore, for the value investor keen on profitability, this is not a stock to opt for as there is no exact timeline for resolving the supply chain problems. On the other hand, there are opportunities for growth-oriented investors looking to profit from the Apple partnership.

In this case, related revenues should accelerate in the fourth quarter, more precisely in November as per the CEO. To further support this fact and to show that there has been no delay in deployment, there has been an a nnouncement by Apple concerning an "expansion" of the Emergency SOS satellite feature to several countries in western Europe. Thinking aloud, for the iPhone company to expand its use of Globalstar's satellites implies that there have been no serious glitches in the latter's performance.

Now, considering that Apple just transfers $50 million out of the "majority of the $450 million" to Globalstar in Q4, the company could end up its FY2022 with $195.95 million instead of the $145.95 million analysts expect as pictured below.

Table prepared using data from (www.seekingalpha.com)

{kind=link}

This would in turn imply a revenue growth rate of 57.6% over FY2021's $124.3 million . Now, since sales form the denominator of the forward price to sales multiple, it would be reduced by around 40% (57.6-17.42) to 6.56x. Now, since this is much lower than Globalstar's five-year average of 10.90x , it means that the company's forward P/S is undervalued based on a historical basis. Of course, this is subject to Apple doing the payment in Q4.

Extrapolating further, after having lost more than 40% of its value since its $2.28 peak, an upside to $1.6 is possible based on the current share price of $1.33 appreciating by just 20%.

I am also optimistic for the long term as Globalstar is a key player in the satellite IoT market which is seeing accelerated growth of 40.3% CAGR, and is expected to continue till 2026. In this respect, commercial IoT service revenue saw a 5% increase thanks to a substantial increase in the subscriber base, encompassing a 24% surge in the volume of activations (new subscriber devices being activated). Moreover, the fact that related equipment sales increased by 50% in Q3 should translate into higher services revenue in Q4 and points to continued strength in this segment.

Looking at the industry, Globalstar faces competition from Iridium ( IRDM ) which is also seeing rapid growth in IoT with the majority of its subscribers coming from this segment as I pointed out in a recent thesis. Now, Apple's partner also has a large IoT customer base and on top is developing a two-way design module to expand its offerings.

Now, there is a plethora of applications around IoT where data from sensors have to be transmitted over vast distances to locations deprived of conventional mobile networks. One concrete example is an oil and gas company tracking remote assets by transferring the data reported by sensors to HQ or headquarters located hundreds of miles away. These pertain to one-way communications, or data being transferred from the sensor to HQ for someone to take a decision on what action to undertake like dispatching someone to activate a safety valve after a leak. Globalstar is working on two-way connectivity, like for example automatically activating the safety valve following the sensor reporting a leak.

Conclusion

Therefore, in addition to the direct-to-satellite iPhone 14, Globalstar can also rely on activating more IoT devices, while offering clients the option of availing of the two-way product differentiator. Thus, the company which scores a superior B+ score for growth should maintain its position this year.

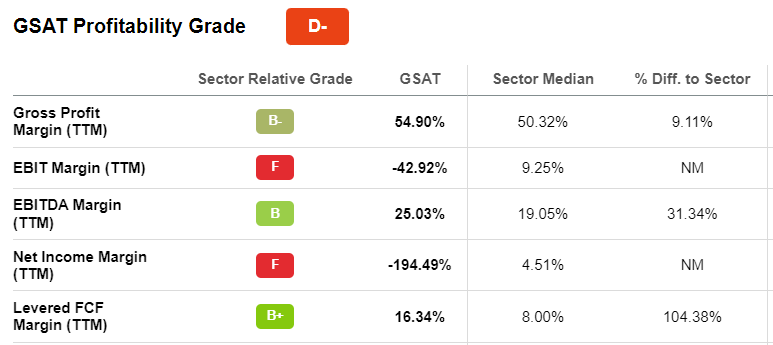

Shifting to profitability, the operating (EBIT) margins are negative as pictured below, and likely to remain so till there is an improvement in the supply chain. Still, that partnership with cash-rich Apple should help the company maintain its superior B+ score as to the levered free cash flow margin in 2023, by helping to offset cash shortfalls likely to be suffered as a result of not being able to ship products to customers in time due to unavailability of components.

GSAT Profitability Grade (www.seekingalpha.com)

{kind=link}

Looking at the stock price action, Globalstar could be a trading opportunity when financial results for Q4 are announced in the first week of February and the share price could appreciate and reach $1.6 driven by the iPhone catalyst.

Finally, volatility should continue to prevail as supply issues are likely to take center stage when Globalstar reports results for subsequent quarters amid deteriorating macroeconomic conditions due to higher recession risks. Also, with high inflation, do expect costs to stay elevated which should continue to put pressure on the company's profitability, but, to somewhat brighten this bleak picture, the automation features provided by IoT can help to lower expenses for GlobalStar's customers while increasing the efficiency of operations.

For further details see:

Globalstar: Supply Issues, But Apple-Related And IoT Strengths