GLOB - Globant: Impressive Growth Still Too Expensive

2023-05-17 12:03:07 ET

Summary

- Digitization is going to see continued strong growth, and the company will benefit from that.

- The balance sheet is very impressive, with signs of a turnaround.

- Revenue growth has been very strong; however, margins have not been increasing at all, which is the biggest factor that affects its valuation.

- Even with slight improvements in margins, the company is still too expensive right now.

Investment Thesis

With earnings just around the corner, I wanted to take a look at Globant S.A.'s ( GLOB ) financial health and to see if the current high P/E multiple is justified and if maybe the company is a good buy at these levels. Unfortunately, it is overpriced, even if we assume rather high revenue growth for the next decade. I do think that the company can be a good investment if it comes down significantly more in the future, and the risk/reward ratio is much more attractive.

Briefly on the Company

Globant has been around since 2003 in Argentina. It helps many different companies like The Walt Disney Company ( DIS ) and many other firms to transform their operations and adopt advanced technology to improve efficiencies all around, like automation, AI process, and data analytics to improve business decision-making and implement digital transformation.

In this article, I will focus on the company's historical performance mostly, to see if I can come up with some reasonable assumptions that the company can be worth intrinsically.

Digitization

The company is in a great position to perform well in the future, as digital transformation has been on the rise in the last decade. The pandemic panic has helped it achieve the next level of revenue growth, but even before that, the growth was quite impressive. Companies are accelerating their evolution into digital space more rapidly after the pandemic, which brought in a new way of looking at day-to-day operations of the companies and employees that embraced a hybrid working situation that requires up-to-date technology so that everyone stays as productive as before or even more productive. With time and advancements of AI, we will become much more productive and efficient in my opinion and the company will see much more demand for their services if they keep up with the latest technological advancements.

I believe that digitization is the single best way for any company to become more efficient and in turn more profitable in the long run. Globant will be there to help with that. There is so much potential for companies that are still at the beginning of their digital transformation. Companies in shipping and other similar industries are starting to see the benefits of becoming more technologically advanced to streamline their operations, provide better customer service, and become more efficient.

Financials

The company ended FY22 with $292m in cash and around $51m in short-term investments while having essentially no debt. This is a great position to be in, especially if we are going to experience an economic downturn in the future.

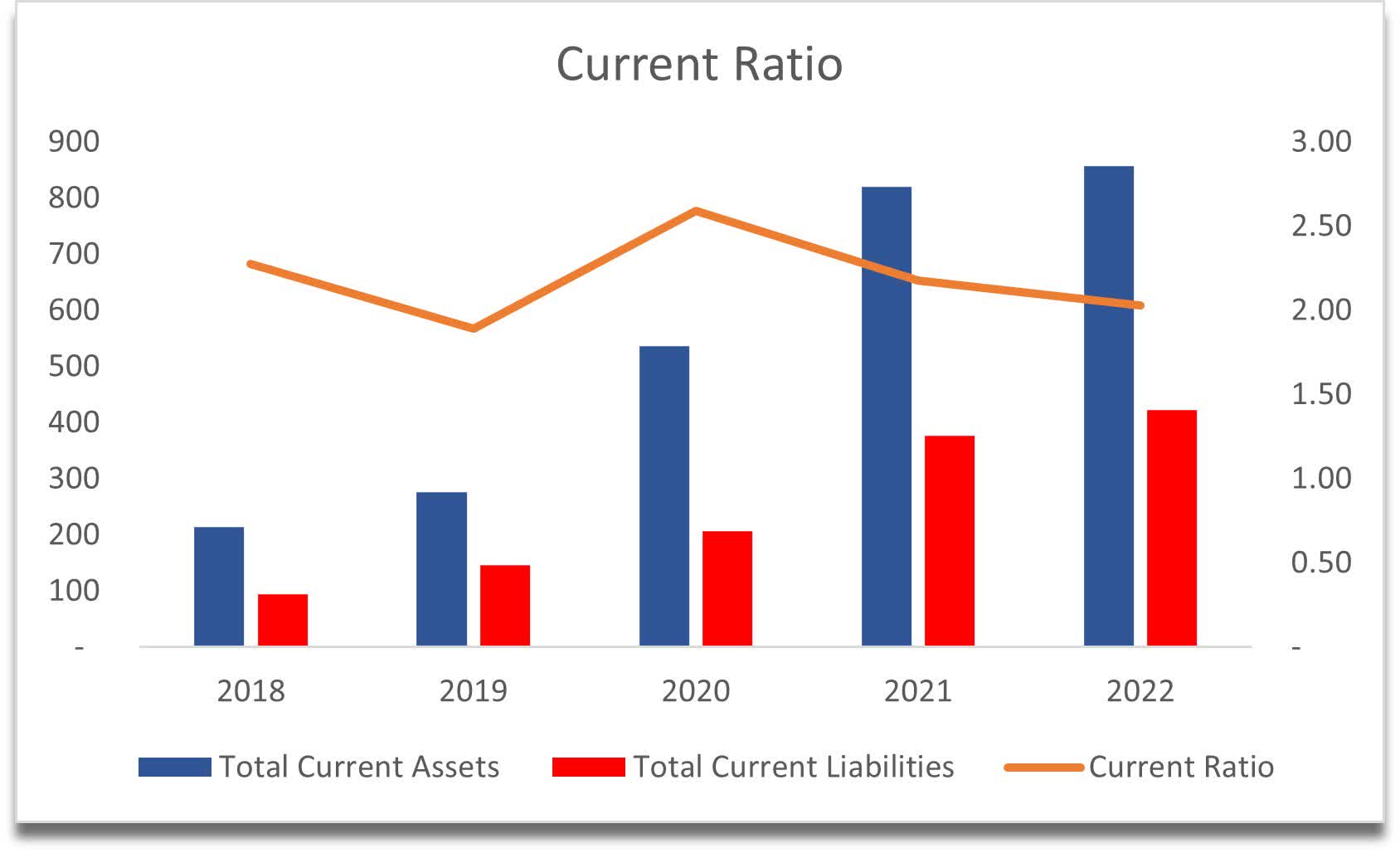

The company's current ratio is also very healthy and has been at these levels for at least 5 years now. It is safe to say that the company has no liquidity problems, as it can cover its short-term obligations twice over.

{kind=link}

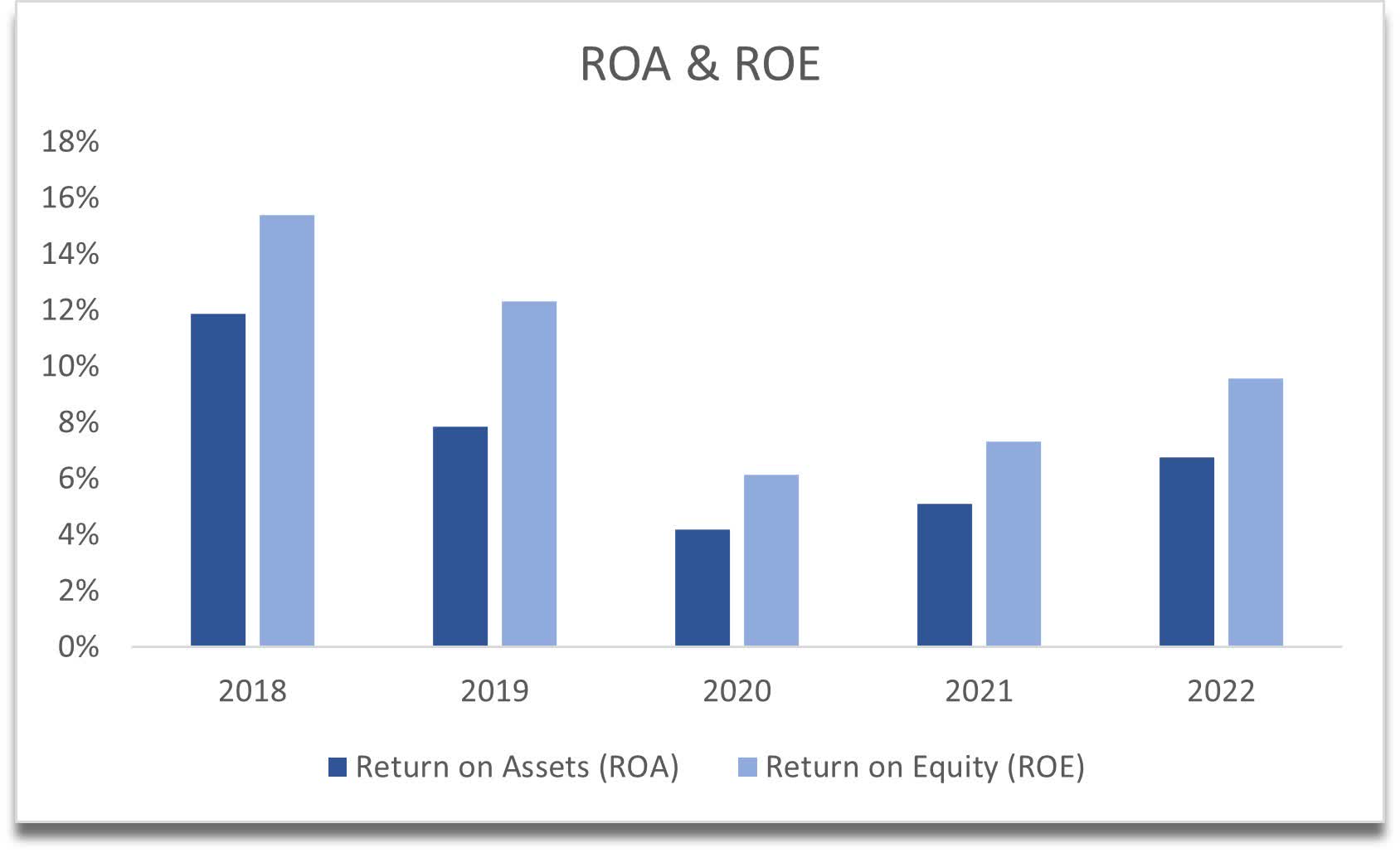

In terms of efficiency and profitability, the company has seen better numbers before the pandemic, however, the metrics seem to be having a turnaround since FY20 and are on an uptrend, which is a very good sign. ROA and ROE are slightly lower than where they were 3 years ago but are improving now, which suggests the company is becoming better at using its assets and shareholders' capital.

{kind=link}

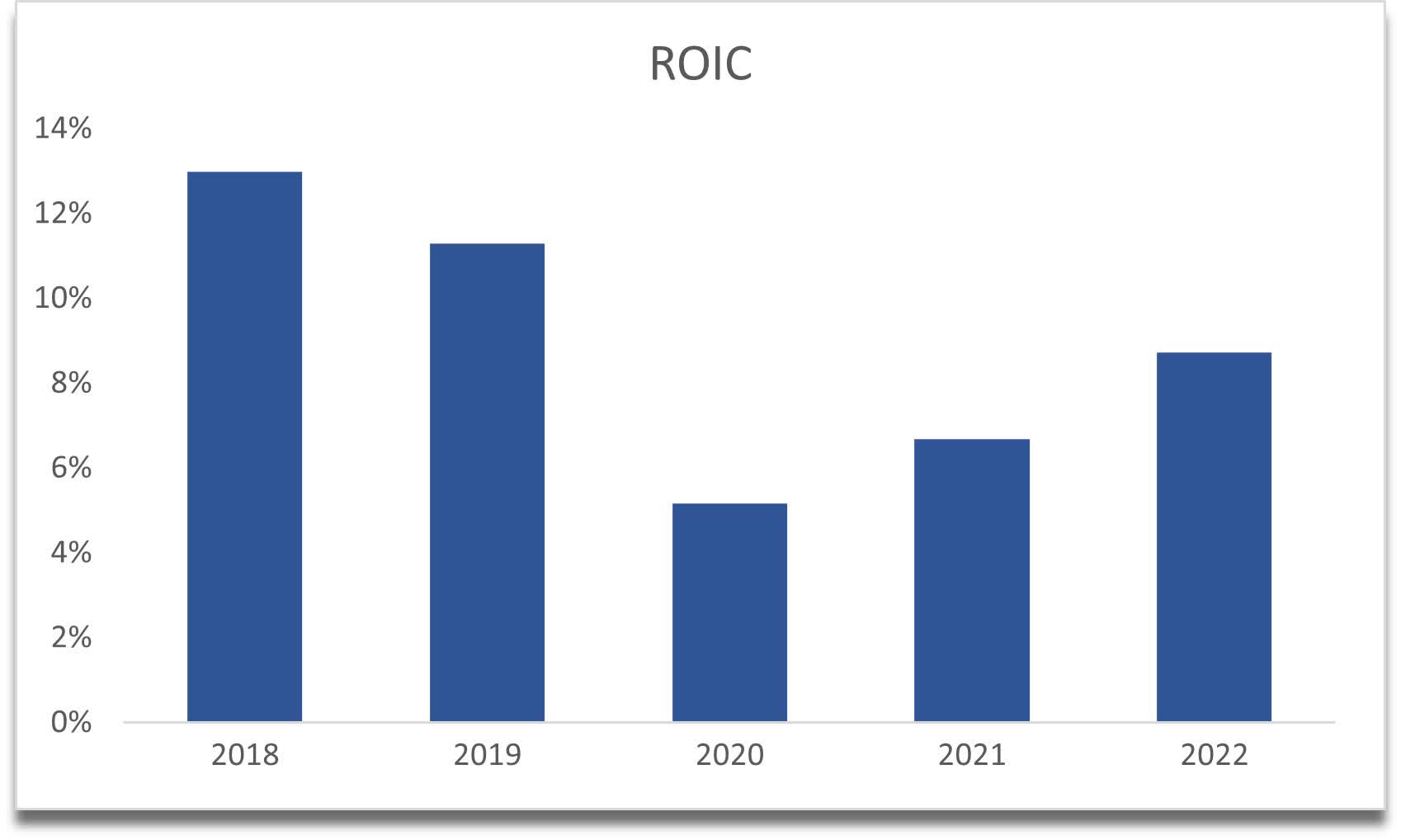

We can see the same situation with return on invested capital, which suggests the company can invest in more positive NPV projects and is enjoying much more of a competitive advantage than before and a stronger moat.

{kind=link}

Overall, the balance sheet is in very good condition with a positive turnaround on efficiency and profitability metrics, which is very promising.

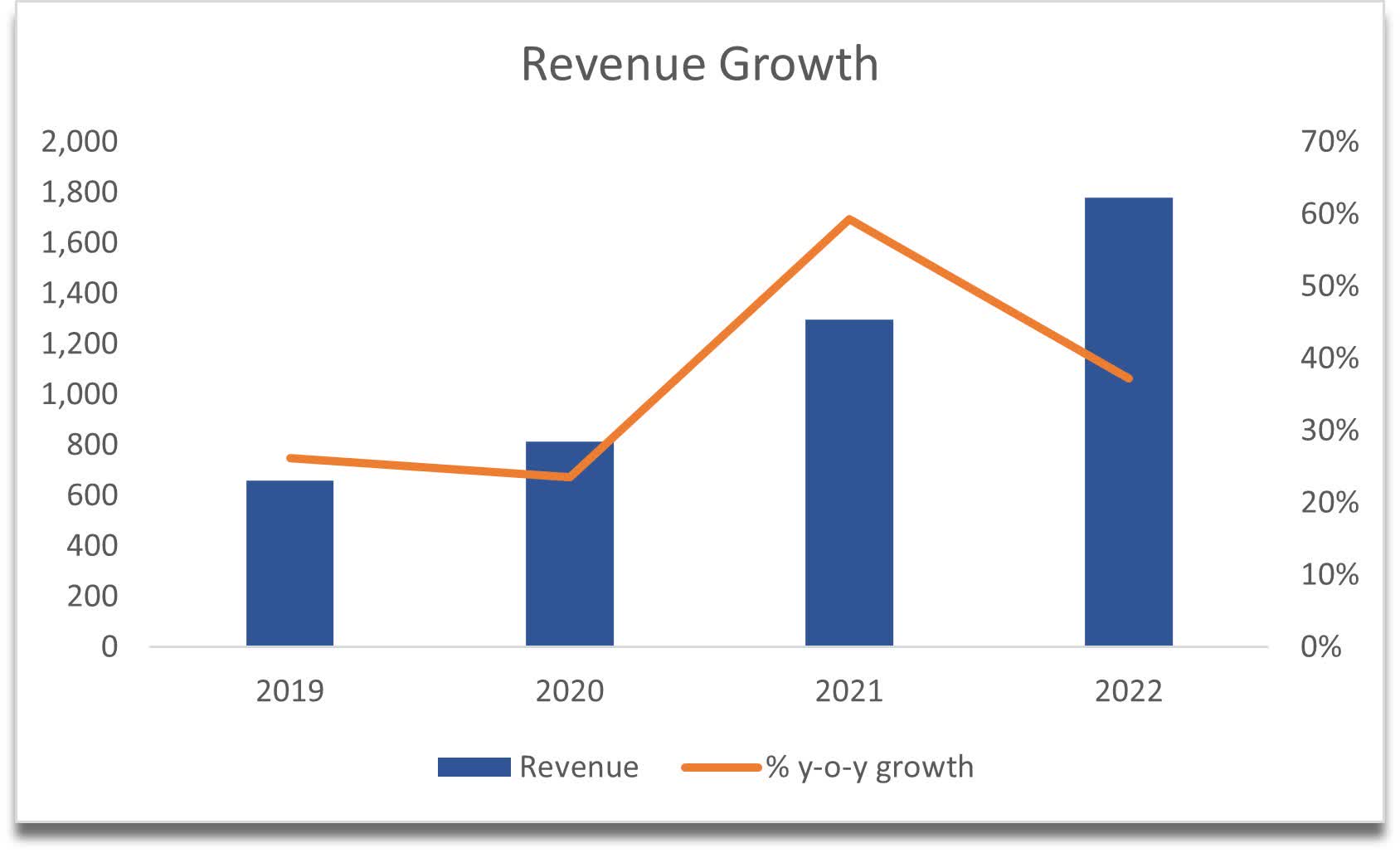

In terms of revenue, the last 10 years have been very impressive. The company averaged around 31% a year since 2013. In the latest transcript , however, the company is projecting to grow revenues by about 16% y-o-y. It is quite a bit of a slowdown, which suggests that the economic headwinds are already appearing to dampen the demand for their services. It is still a really good growth number because I've covered quite a few companies in the past couple of months, and they all seem to have very depressing revenue numbers for the full year.

{kind=link}

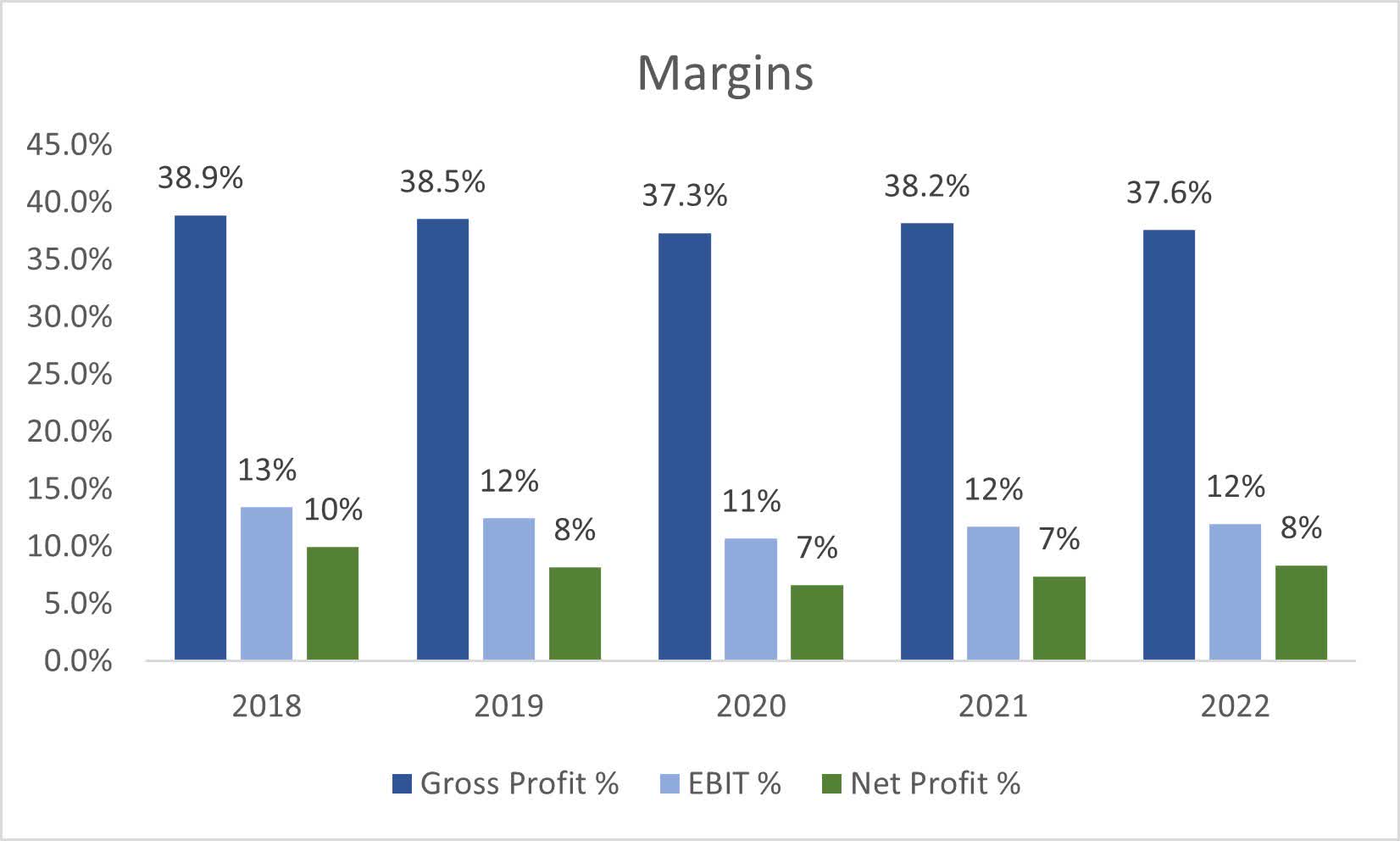

In terms of margins, these have been very steady for at least the last 5 years. I would have expected slightly higher margins all around, however, the company does face quite a bit of competition from other IT and technology service providers, but if they manage to improve on these in the future, it will become much more attractive as an investment.

{kind=link}

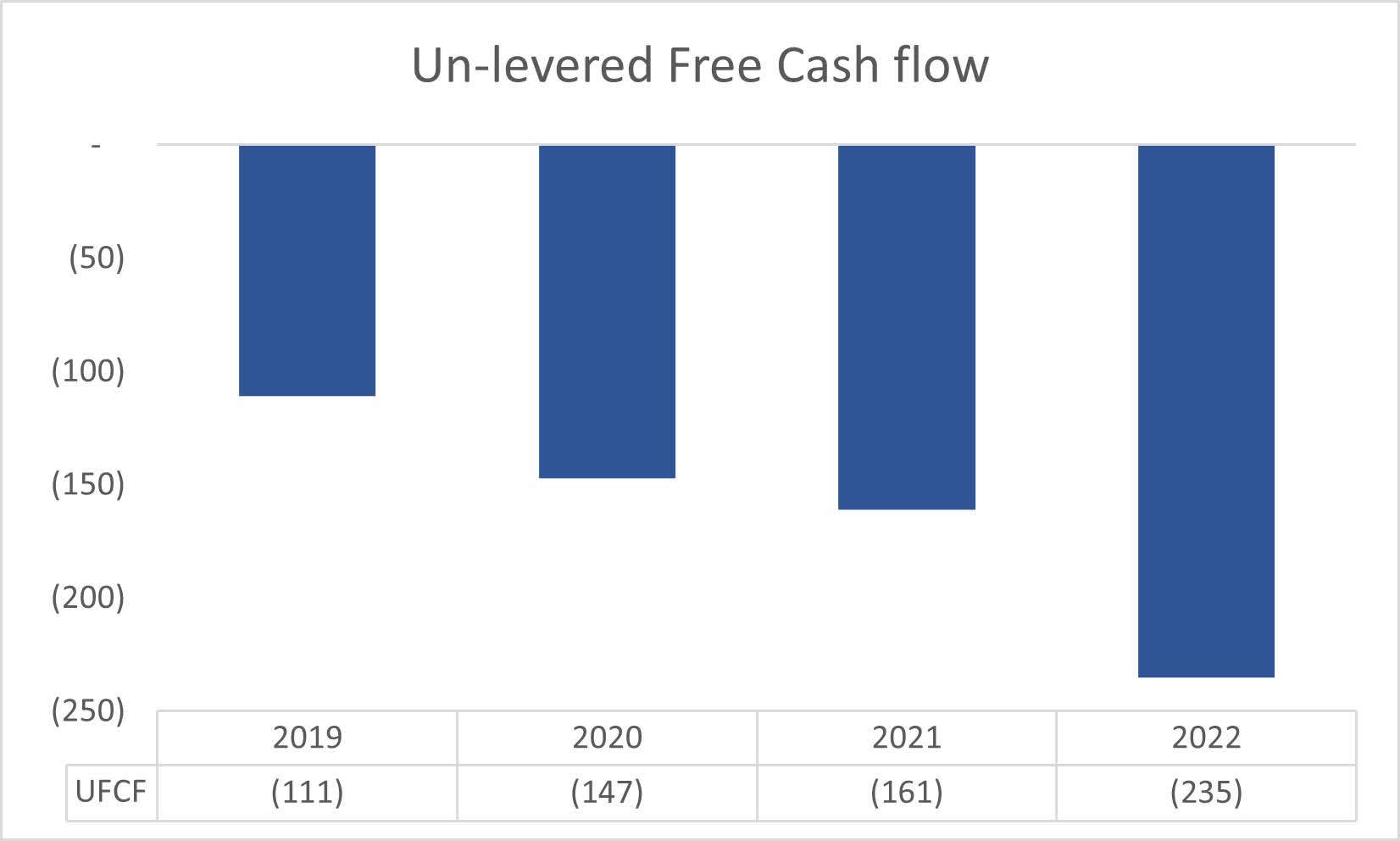

For my intrinsic value calculation, I like to use unlevered free cash flow (UFCF) which looks at the cash flow that the company generated before accounting for financing costs like interest expenses and CAPEX. I was not very happy to see that in the last 5 years, the company's UFCF has been negative and still on a downtrend, which makes it very hard to make any sort of future assumptions. The company is not generating UFCF, so for my valuation analysis, I have to assume it does in the future but also be reasonable.

{kind=link}

Overall, if the company manages to improve margins in the future, it will improve the bottom line and will be able to generate positive UFCF, but that's a big if since the company has seen very steady margins for the last 5 years.

Valuation

I decided to continue the company's impressive growth in revenues, however, slightly more on the conservative side, nonetheless still a very impressive growth. Since the management said they expect to grow at around 16% in '23, I went with 15% to be more on the safer side for my base case scenario. For '24, I decided to use 30% revenue growth which reflects the demand coming back for digitization and the company is in a good position to capture that. After '24, the company's annual growth will be around 20% per year until '32. In total, from '23 to '32, average growth per year ends up being 20.5%, which is a really impressive growth. These assumptions will bring the company's revenues from $1.78B in '22 to $11.3B, over a 600% increase in 10 years. As I mentioned the company managed to achieve around 31% growth in the last decade, so 20% is slightly more reasonable, but could still be on the more optimistic side.

For the conservative case, I went with 16.7% CAGR over the next decade, while for the optimistic case, I went with 25.5% CAGR.

In terms of margins, since the company has kept them very steady over the last 5 years or so, it was reasonable to assume that they would be quite similar over the next decade with slight improvements. I modeled a 200bps improvement in gross margins over the next decade to reflect some sort of better efficiency, which I think is more than sufficient, given that the company managed to contract margins by around 200bps in the last 5 years.

I also add a 25% margin of safety to my calculations if a company has a good balance sheet, which Globant does. I add a larger one if the balance sheet has some red flags.

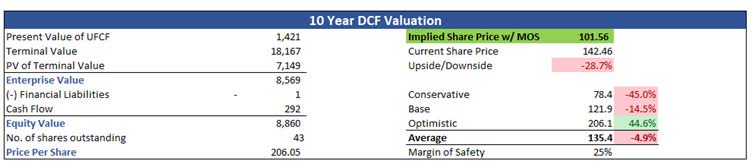

With that said, the company's intrinsic value with the above assumptions is $101.56, implying around 29% downside from the current valuation.

{kind=link}

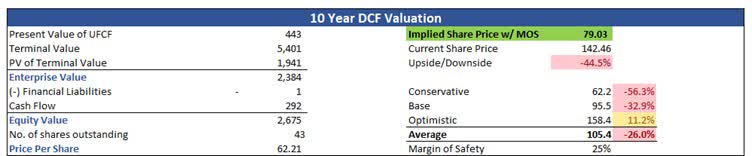

The calculation changes quite drastically if I leave margins as they were at the end of FY22, giving a downside of 44.5% from the current valuation.

{kind=link}

Closing Comments

Even with such an impressive growth potential in the future, if history repeats itself that is, the company is still quite overvalued right now and is not a very attractive investment in terms of my risk/reward needs. Even at $79 a share, the P/E ratio is around 23 which is still quite expensive in my opinion. The company needs to work on margin improvement over the next while for it to be an attractive investment for long-term investors like me.

If we are going to experience some economic headwinds soon, I would expect Globant to come down with the rest of the markets, however, it is hard to predict that, but all I know is that it is not a good investment risk-wise right now.

For further details see:

Globant: Impressive Growth, Still Too Expensive