GL - Globe Life: High Excess Claims Lie Ahead

Summary

- Excess deaths do not appear to be declining significantly.

- Medical claims appear to be set to soar.

- Global Life’s growth trajectory seems to be based on a false premise.

Preamble

While I was relaxing drinking my morning coffee, for my amusement I tuned into Al Gore’s tirade on the importance of reducing CO2 emissions or face “rain bombs” and “boiling oceans.” According to Al, the earth faces desertification and associated catastrophes unless we reduce the concentration of CO2 in the atmosphere. Now, I believe that prior to his rants, he ought to disclose that he has made coin to the tune of $300 million by promoting this type of alarmism. Furthermore, he ought to concede that some deserts are actually shrinking and in fact the earth is getting greener as a result of marginally higher concentrations of CO2. An explanation for this counter-intuitive situation can be found in a recent article I wrote for Seeking Alpha.

Now this is not the only peculiar state-of-affairs we can discover if we consider the world today. Back in 2020, the CDC reported around 380,000 deaths that were attributed to COVID. So, we can understand that the pandemic led to an increase in excess mortality during this time. According to one report ; “from March 1, 2020, to Jan. 2, 2021, excess deaths rose a massive 22.9% in the US.” A White House report states that; “the percentage increase in excess deaths relative to expected deaths, differed significantly across States, from a low of 5.7 percent in Hawaii to a high of 27.4 percent in Arizona.” It is widely accepted that the pandemic is on the wane, and yet, excess mortality remains stubbornly high . Moreover, the excess mortality is not entirely due to COVID.

One can readily understand that the vast majority of deaths from COVID were amongst the elderly, however, the excess deaths occurring at the present time are among working-age people . And this is not a phenomenon isolated to the US, but can be seen in other countries too. A recent report from The Institute and Faculty of Actuaries in the UK notes that mortality rates for ages 20-44 is 7.8% higher than expected. If this data were not bad enough, the report also states that; “The number of deaths registered in England & Wales in week 1 of 2023 was 3,437 higher than if mortality rates had been the same as in week 1 of 2019; equivalent to 30% more deaths than expected.” In summary, what these figures are suggesting is that there appears to be no slow down in excess deaths and that these deaths are occurring amongst the younger members of the population.

On top of that, in a number of countries and districts, the cause of death appears to be registered as unknown; the province of Alberta for example. Naturally, these excess deaths in 2021 meant that death-benefit pay-outs was a record, which led to reduced profits for US insurers. And the data appears to confirm that death-benefit pay-outs will not be declining anytime soon.

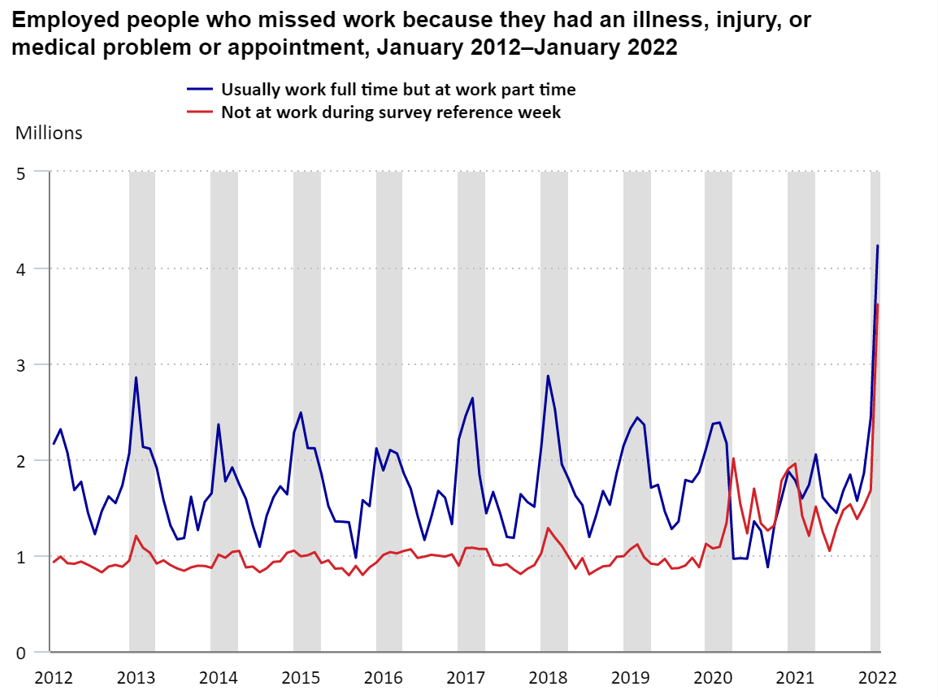

It doesn’t take a rocket scientist to surmise that if excess deaths are rising, then general sickness may well be on an upward trend. And indeed, this is the case, if the statistics from The US Bureau of Labor Statistics are to be believed. This graph makes grim reading for many reasons, not least because there appears to be no explanation put forward for this shocking state of affairs by the agencies tasked to monitor the nation’s health. This graphic should also be troubling for the stock holders of health insurance companies.

{kind=link}

Government agency

Global Life

At the beginning of November 2022, Lincoln National Group (NYSE: LNC ) reported a net loss for the quarter. Whilst the loss was not entirely due to elevated pandemic-related claims experience, these excess claims were certainly significant. This was highlighted by Randy Freitag, Chief Financial Officer, in the last quarterly earnings call ,who stated that the Life business had; “an unfavorable impact of $223 million from updating our mortality assumptions.” Since then, there has also been a downgrade on cash flow concerns, which has probably helped push the stock price down 40% since November.

In sharp contrast, Global Life ( GL ) gave a rather rosy report at the end of October, and so the stock has risen to all-time highs. Even though the stock has rallied, it could be argued that it remains fairly valued with a P/E of around 14.5. Going forward, the consensus for the company is an 18% growth of operating earnings per share for the full year 2022. Whilst this low P/E looks attractive, I'm suggesting that this figure will become less attractive following the next quarterly report.

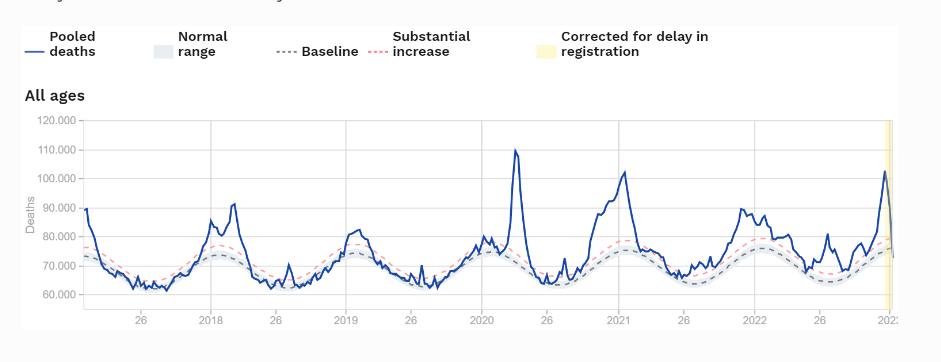

In the preamble I drew attention to the continuing high levels of mortality in 2022, which will of course affect GL's fourth quarter results. Data from the European Union gives some indication of just how bad the results could be. Throughout the whole of Europe, mortality rates accelerated in the second half of 2022 to reach the highs of 2021.

{kind=link}

In the third quarter press release, it was noted that “COVID life claims expense for the quarter ended September 30, 2022 was not significant, compared to $33 million in the quarter ended September 30, 2021. Year to date through September 30, we incurred $44 million of COVID life claims as compared to $82 million for the same period last year”. Also in the press release, the company stated that it expects a lowered claims number going forward. This expectation is not supported by the elevated levels of mortality being experienced around the world.

Since the number of deaths increased towards the end of the year 2021, it is entirely possible that death benefit claims for the fourth quarter will reach similar levels to the claims in the fourth quarter of 2021; $58 Million. On top of that, there will almost certainly be elevated medical claims resulting from the above normal levels of sickness.

The company’s future growth and stock price is based on the unproven premise that excess mortality and other health claims will normalize in the near term. Indeed, during the quarterly call, Frank Svoboda, Chief Financial Officer, stated that; “we expect underwriting margin to be up around 23%, due primarily to a decline in COVID and excess mortality for the full year.” Yet, current data shows that excess mortality is not falling and the data from The US Bureau of Labor Statistics indicates that levels of illness are rocketing.

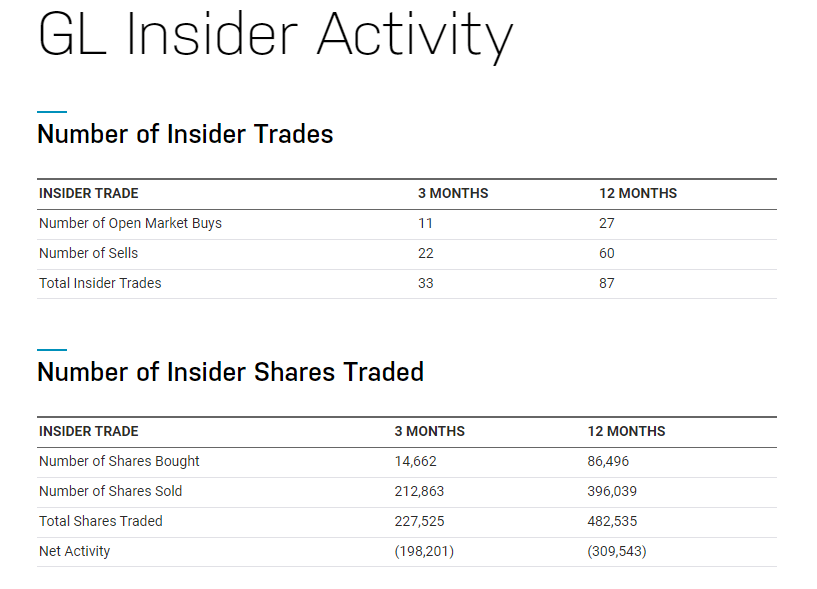

Given the positive picture painted of the future direction of the company, one would expect feverish buying by insiders. Curiously, the exact opposite is true. From Nasdaq’s data , it is evident that since the last quarterly report, there has been a sharp rise in sales.

{kind=link}

Nasdaq

Paying claims

There is no suggestion that GL will be unable to pay additional claims, as the business is quite a strong insurance company financially. Reading the balance sheet, one can easily see that there is plenty of cash in the bank, so to speak. Investors in the company may further argue that the company is taking steps to improve investment income, as noted in the third quarter results, and that the increased returns will more than compensate for additional claims.

However, the balance sheet also reveals that debt levels are elevated, which, in a high interest rate environment, is not ideal. And the trend of the book value per share is less than inspiring.

Risks

Based on the information to hand, it is unlikely that claims for the company will fall. Indeed, as I mention in my aforementioned article, claims are likely to rise. The soaring levels of sickness may not be due to an upset stomach or the sniffles, but due to newly diagnosed life threatening conditions. That said, the possibility of a decline in claims needs to be recognised and so a close eye needs to be kept on the data for this topic.

To sum up

The current stock price of GL is supported by the assumption that claims will normalize in the near term, which in my strong view is not supported by excess death and other medical related information. Therefore, one may be wise to follow insiders and sell before the next set of quarterly results.

As regards a target for the downside, I expect a fall of around 20 percent. Firstly, there is the experience with Lincoln National Group, which fell sharply on the news of unexpected claims. Secondly, there was an approximately 5 percent decline following the fourth quarter results for 2021. Typically, unexpected bad news is not a positive for a stock in my experience.

For further details see:

Globe Life: High Excess Claims Lie Ahead