GLP - GLP.PRA - Sell It Given The Refinancing Risk

2023-08-21 12:27:01 ET

Summary

- Global Partners is a U.S. independent owner, supplier, and operator of gasoline stations and convenience stores.

- The company is focused on the Northeast and is incorporated as a master limited partnership (MLP).

- The Series A preferred shares have just passed their call date on August 15, and have now re-set to SOFR+6.77% .

- The all-in cost of the Series A is above 12%, which makes it very likely for the company to call the preferred equity at $25/share.

Thesis

Global Partners ( GLP ) is a U.S. independent owner, supplier and operator of gasoline stations and convenience stores. The company is focused mostly on the Northeast and is incorporated as an MLP:

A master limited partnership is a business venture in the form of a publicly-traded limited partnership. It combines the tax benefits of a private partnership with the liquidity of a publicly-traded company. A master limited partnership trades on national exchanges. MLPs generally experience cash flow stability and are required by the partnership agreement to distribute a set amount of cash to investors. Their structure can also help reduce the cost of capital in capital-intensive businesses, such as the energy sector.

Source: Investopedia

The common units of the partnership are covered by Seeking Alpha authors with a 'Buy' rating, while the SA quant ratings currently assign the common units a 'Strong Buy' rating:

Ratings Summary (Seeking Alpha)

We are touching upon the strength in the common units to illustrate the robust corporate balance sheet and profitability (current and expected) for the company, and its implied ability to access the capital markets.

MLP structures are required to disburse a large percentage of their free cash flows to unit holders, therefore usually run a significant amount of debt. An investor will usually encounter the MLP structure in the energy storage and transportation sector.

GLP is not any different, and while the company is extremely well run and has ridden the energy boom very profitably, its capital structure is very similar to most MLPs - it has a significant amount of debt, and uses preferred share issuance heavily to obtain better Debt/EBITDA metrics.

In this article we are going to look at GLP's capital structure, current funding rates and derive an expected call date for the Series A preferred shares (GLP.PRA).

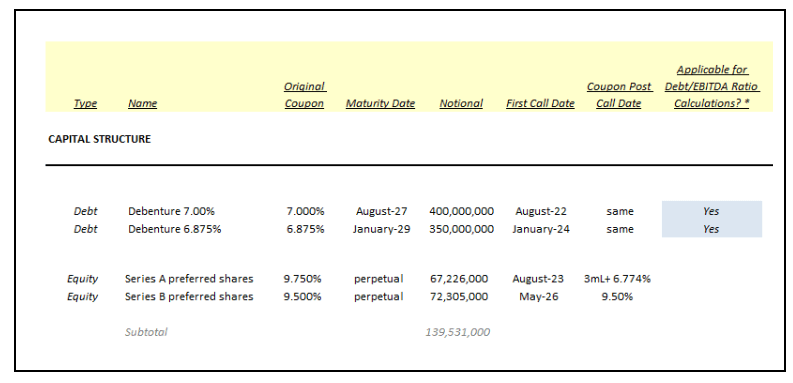

GLP Capital Structure

As discussed above, the company runs a large amount of debt, either outright via debentures and a revolving credit facility, or via preferred equity (which does not count towards Debt/EBITDA metrics):

{kind=link}

As we can observe from the capital structure snap-shot above (of term debt), the company has two debentures with very attractive maturity dates in 2027 and 2029. GLP did a good job of placing these at low prevailing rates, and is very likely to run them until maturity.

Conversely, the preferred equity slices are done at wider levels (to reflect the lack of a senior unsecured lien), and are constituted by two series of preferred equity. Series A was issued in 2018, while Series B was issued in Q1 of 2021.

To note that the GLP Treasury department did a great job in timing the rates market, issuing a fully fixed preferred tranche at the lows for interest rates in 2021. It speaks volumes on the quality of the management team.

Series A, which we are targeting in this article, was issued in 2018 with a standard 5-year non-call period and a floating rate feature:

Distributions on the Series A Preferred Units are cumulative from and including the date of original issue and will be payable quarterly in arrears on February 15, May 15, August 15 and November 15 of each year, commencing on November 15, 2018, in each case when, as, and if declared by our general partner. On and after August 15, 2023, distributions on the Series A Preferred Units will accumulate for each distribution period at a percentage of the $25.00 liquidation preference equal to an annual floating rate of the three-month LIBOR plus a spread of 6.774% per annum.

Source: Prospectus

The standard in the preferred equity space is a 5-year non-call period, after which preferred equity usually tends to reset higher (more expensive for the company) in order to incentivize the corporate to refinance it. Preferred equity is structurally perpetual, which gives it a GAAP accounting treatment of equity, thus eliminating it from Debt/EBITDA calculations.

From an accounting standpoint, preferred equity is a loss absorbing tranche, before debt is impacted. In essence, preferred equity shareholders get a higher yield, but take on more risk if the company has to restructure. From a seniority perspective common equity is wiped out first, followed by preferred equity, followed by debt and lastly general company liabilities (salaries, bills to suppliers, etc).

Usually if a company is doing well, its cost of funds are low, and is able to refinance preferred equity at attractive levels rather than let it lapse past the call date at a higher cost of funds. Conversely, companies that are in trouble tend to let preferred tranches remain outstanding because issuing new shares would be more expensive.

Series A is becoming extremely expensive for the company

GLP is a company doing extremely well, and its Series A is now re-setting to a floating rate payout. LIBOR is no longer in existence, but has now been replaced by SOFR:

{kind=link}

So the Series A has re-set to something close to 5.38% + 6.774%, which equals 12.15%! That is an extremely high dividend rate for this company. How do we know that? Quite simple - we can look where the Series B is trading:

Series B Yield (PreferredStockChannel)

The Series B, which is fixed, trades with a 9.25% yield. This means that 9.25% is a rough estimate on how much new preferred equity paper would need to pay to clear the market right now.

To put it in English, GLP needs only to pay 9.25% in order to place new preferred equity. Why would it pay 12.15% then? That is a rate almost 50% higher than 9.25%. The answer is that it will not continue to pay the current floating rate on the Series A, and the company is working on issuing new paper to take out the GLP.PRA tranche, now that it has passed its call date.

The Treasury department for this company has proven to be very savvy, and one would expect them to try to take advantage of the current rates environment by either placing an outright floater (with an all in yield closer to 9.25%, so SOFR + 4%) or a fixed to floating. We are currently experiencing historically high interest rates, with the forward curve showing us much lower rates levels in the future.

Conclusion

GLP is a company that owns a network of convenience stores that sell gasoline and distillates in the Northeast of the U.S. The company is incorporated as an MLP, structure which forces it to distribute a large amount of its free cash flow. Just like any MLP, GLP has a large amount of debt and has been issuing preferred shares to optimize its capital structure.

The GLP Series A preferred shares have just passed their first call date on August 15, and have now re-set higher to a rate close to 12.15%. The Series A was fixed at 9.75% until now, resetting to SOFR+6.77%. The current all-in rate is extremely high from a dollar perspective for a company that is doing very well, and we can see their fixed rate Series B preferred shares trading at a 9.25% yield.

The market is telling the company it can place new paper at 9.25% all-in yields, and we fully expect them to issue a new tranche of preferred equity to take out the expensive Series A. GLP.PRA is callable at $25/share plus accrued interest, and we expect the company to do so shortly. Given the current yield, the Series A should never trade above $25.75, representing a full quarter of dividends. There is no reason to hold this tranche at the moment given it is trading at a premium to its call price, thus a retail investor would do well to Sell it.

For further details see:

GLP.PRA - Sell It Given The Refinancing Risk