URTH - GLQ: Best To Look Elsewhere Given The Risks Of This CEF

2023-10-11 13:35:41 ET

Summary

- The Clough Global Equity Fund is heavily invested in the United States, which may not be ideal for American investors seeking geographic diversification.

- The GLQ closed-end fund has experienced significant losses, down 64.83% since November 2021, due to its high level of leverage and exposure to the American equity markets.

- Despite its poor performance, the fund offers a high distribution yield of 12.93%, which may offset some of the share price declines for investors.

- The fund failed to cover its distributions over the past eighteen months. It is uncertain how sustainable it will be at the new lower level.

- The fund has a very attractive valuation right now, but it might not be worth the risks.

The Clough Global Equity Fund ( GLQ ) is a closed-end fund, or CEF, that is designed as a method by which investors can obtain geographical diversification along with a high level of income from the assets in their portfolio. Despite this stated purpose of investing in companies from around the world, the fund was very heavily invested in the United States back in 2021, which was the last time that we discussed it. This is a shame, because the biggest problem that most American investors have is that their portfolios are too exposed to the United States, which could cause them to experience financial problems if America goes through financial turbulence that could have been easily avoided through sufficient geographic exposure. The fund does do a decent job on the income front, though, as it boasts a 12.93% yield at the current price, which is easily in the same ballpark as most fixed-income closed-end funds and better than many equity ones.

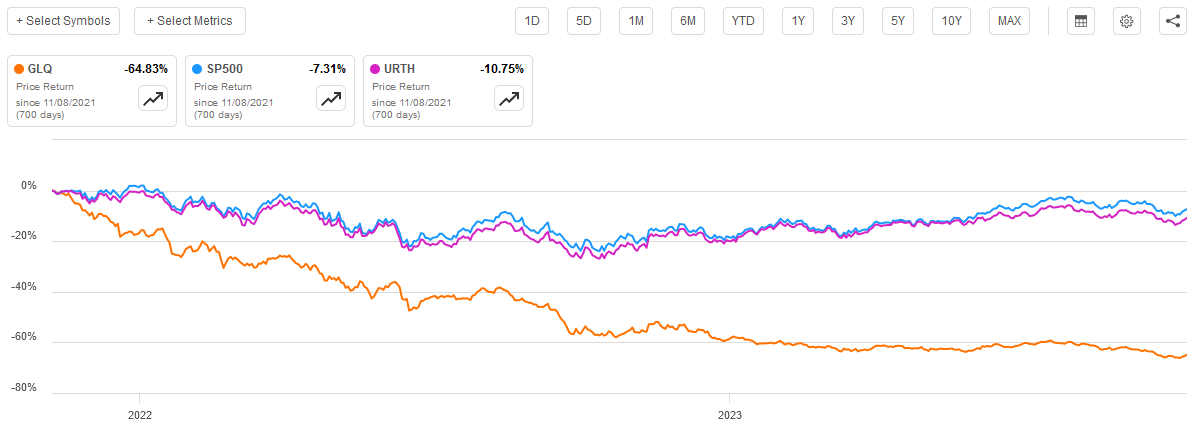

In my previous article on the fund, I mentioned that the fund’s extremely high level of leverage could pose a very real risk in the event of a decline in the American equity markets. That proved to be the case last year. That previous article was published on November 8, 2021. Since that time, the Clough Global Equity Fund has been completely obliterated, as its share price is down a whopping 64.83%. This is far worse than the 7.31% decline in the S&P 500 Index ( SP500 ) or the 10.75% decline in the MSCI World Index ( URTH ):

{kind=link}

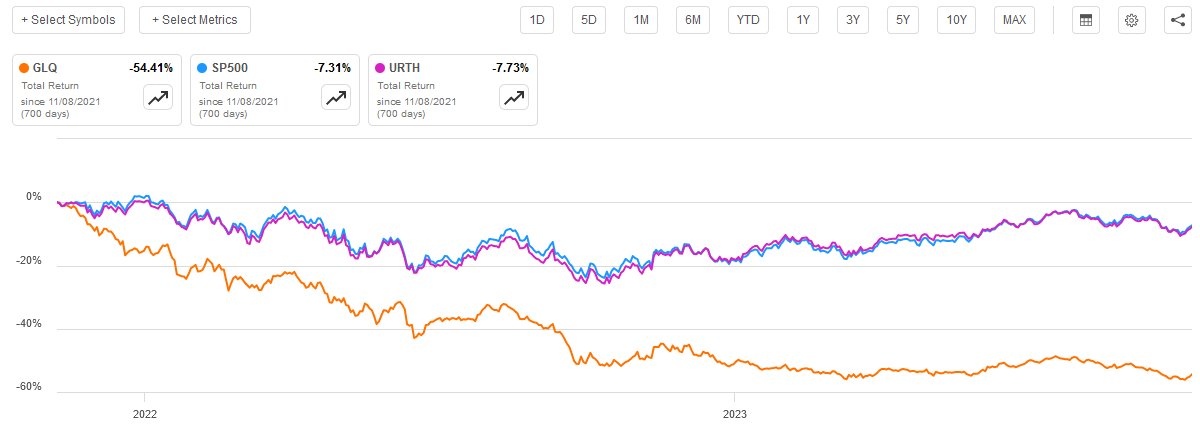

However, this fund has a much higher yield than either of the indices, and the payments received by investors over the period will help to offset some of the share price declines. Even so, investors in the fund have still lost over half of their money since the date of publication of the initial article. Obviously, investors in either of the indices have done much better:

{kind=link}

As so much time has passed since the date that the prior article was published, it goes without saying that a great many things have changed both in the market generally and with this fund in particular. As such, it is a good idea to revisit it and attempt to determine if purchasing this fund could make any sense today.

About The Fund

According to the fund’s website , the Clough Global Equity Fund has the primary objective of providing its investors with a very high level of total return. This is not surprising considering that the name of this fund suggests that it is an equity fund. The fund’s portfolio reinforces this, as it currently has 116.45% of its net assets invested in common equities alongside comparatively small allocations to bonds and other things:

CEF Connect

The one thing that most readers will undoubtedly notice is that the fund’s cash position is negative. This is because the fund employs leverage as a method of boosting its total returns. We will discuss this in more detail later in this article, but it does seem likely that this is the thing that got the fund into trouble last year and caused the losses that it ultimately took.

The focus on total return is certainly not surprising considering this portfolio. After all, common stocks are typically purchased by investors who are looking for total returns. The yield on the S&P 500 Index is only 1.50% today so clearly, nobody is buying common stocks solely for income. A money market fund or anything in the fixed-income space would serve far better in this capacity. Rather, investors in common stock are hoping to benefit from price appreciation as the issuing company grows and prospers. The combination of capital gains and yield is basically the definition of total return.

The name of the Clough Global Equity Fund suggests that it invests in common stocks issued by companies from all over the world. The fund’s website states the same thing:

The Fund intends to invest primarily in a managed mix of global equity securities. The Fund is flexibly managed so that, depending on the Fund’s investment adviser’s outlook, it sometimes will be more heavily invested in equity securities in U.S. markets or in equity securities in other markets around the world. Investments in non-U.S. markets will be made primarily through liquid securities, including depositary receipts (which evidence ownership in underlying foreign securities) and exchange-traded funds.

As I pointed out in my previous article on this fund, it was very heavily invested in the United States at the end of 2021. At that time, the fund had 104.12% of its net assets invested in American equities while being net short the United Kingdom, Italy, France, and Ireland. There was no foreign country whose securities represented anywhere close to the American allocation. That heavy weight towards the United States actually made a lot of sense at the time, since the S&P 500 Index outperformed the MSCI World Index over the eleven-year period that ended on December 31, 2021:

{kind=link}

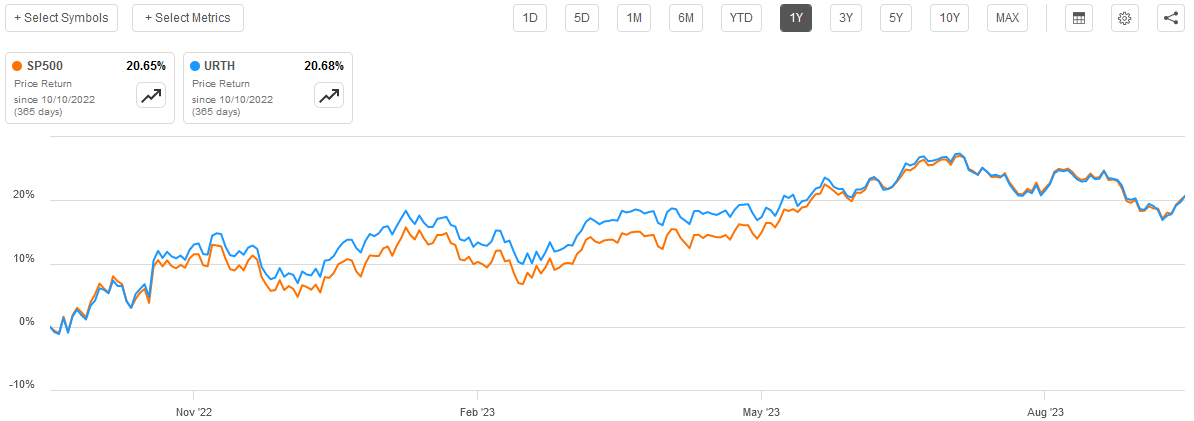

However, it makes a bit less sense today. The MSCI World Index has slightly outperformed the S&P 500 Index (SP500) over the past twelve months:

{kind=link}

As I pointed out in a recent article , the financial markets of the United States are quite likely to come under severe stress over the coming years which further makes the case for having exposure to a variety of nations and their respective economies. However, this fund still retains its substantial exposure to the United States:

CEF Connect

As we can see here, the fund currently has 109.52% of its net assets invested in either American common equity or fixed-income securities. That is less than the fund had the last time that we discussed it, but not by very much. There is no other country that comes anywhere close to this level of exposure. As such, this fund still does not look like a very good way to reduce your exposure to the United States. I explained a few of the problems with having too much exposure to one’s home country in my previous article. Here is the most significant for most readers:

The second problem with home country bias is that it overly exposes an investor to the economy of one’s own nation. Think about it. We already live and work in our own nations so there is always a chance that our incomes and livelihoods will be threatened if the economy of that nation goes south. If your portfolio is entirely or heavily invested in that nation, then an economic calamity could not only disrupt your income but could wipe out your savings as well. Although many economies are connected today, there are still some that remain strong when others weaken. Thus, by having your savings internationally diversified, it may be possible to avoid the worst of these effects.

In various previous and recent articles, I discussed several of the impending economic problems facing the United States, including an aging population, slowing gross domestic product growth, and rapidly deteriorating government finances. While other nations in Western Europe and Japan face some of the same challenges, they have different methods of handling them that may prove more or less effective. As such, it may make more sense than ever to have your assets spread around the world for diversification purposes. While this fund on the surface appears to do that, a closer look at it reveals that it is nowhere near as effective as might be hoped. As such, if you want to include this fund in your portfolio, it is important to ensure that you are invested in sufficient other assets to ensure that you actually do manage to achieve international diversification.

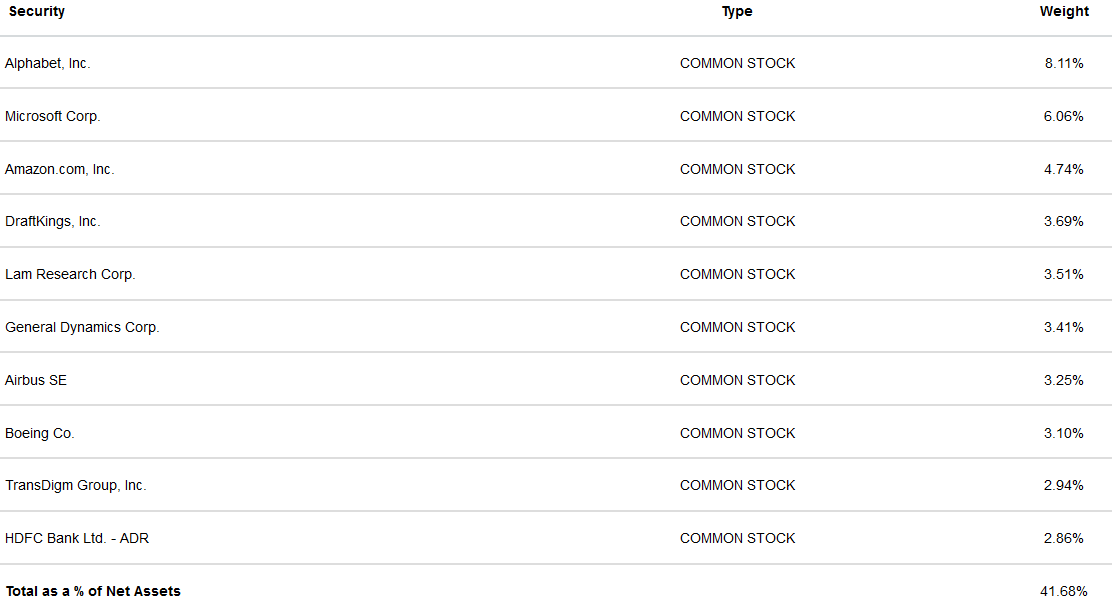

Despite the fund as a whole being very heavily weighted towards the United States, we can see that it has some foreign companies among its top ten holdings:

{kind=link}

Airbus ( EADSF ) and HDFC Bank ( HDB ) are both foreign companies and given their respective weightings, they probably account for their home countries’ entire representation in the fund. Overall, though, the vast majority of these companies are American. Fortunately, we do see some differences here between the Clough Global Equity Fund and most other domestic equity funds. Alphabet ( GOOG ), Microsoft ( MSFT ), and Amazon.com ( AMZN ) tend to be among the largest holdings in just about any equity fund that invests in American stocks. These three companies account for a substantial portion of the S&P 500 Index by themselves, and they are all among the largest and most widely held companies in the United States.

However, the remainder of the companies here are not so commonly held. This is especially true with DraftKings ( DKNG ), which is a popular stock here on Seeking Alpha, but it is not especially popular among fund managers and so is rarely seen in the largest positions of a closed-end fund.

There have been a number of changes since we last discussed this fund. In fact, the only companies that are currently among the fund’s largest positions that had that honor when we last discussed it are Microsoft and Amazon.com. All of the remaining companies on the list were added within the past two years. This could lead someone to predict that this fund has a very high annual turnover. That is indeed the case, as its 198.00% annual turnover is one of the highest that I have ever seen a closed-end fund possess. This means that the company is spending a lot more money trading stocks than most other funds of comparable size so it will need to generate sufficient excess returns from its investments to offset its trading activity. When we consider its poor performance relative to the indices, it does not appear that the fund is doing that.

Leverage

As shown earlier in this article, the Clough Global Equity Fund employs leverage as a method of boosting its returns beyond that of the underlying assets. I explained how this works in my previous article on the fund:

Basically, it borrows money in order to purchase common stocks. As long as the purchased asset provides a higher return than the interest rate that the fund has to pay on the debt, the strategy works quite well to boost the fund’s overall return off of its portfolio. Unfortunately, the use of debt is a double-edged sword because it boosts both gains and losses. As such, we do not want to see the fund use too much debt since that would expose us to too much risk. I do not like to see a fund’s leverage above a third as a percentage of assets for this reason.

Note how I pointed out that the use of leverage increases both gains and losses. This could be one major reason why this fund underperformed the market so severely since the start of 2022. The fund’s leverage is substantially above that one-third level, as its leveraged assets currently comprise 39.73% of the fund’s overall portfolio. This is in line with the leverage that the fund had the last time that we discussed it, which suggests that it is reducing its debt as its asset values decline, but its leverage is still very high. This is especially true considering that this is an equity fund so by its very nature its assets will be more volatile than those of a fixed-income or debt fund. As such, it appears that this fund is running a very high-risk, high-reward strategy. That will work out fine during bull markets characterized by low interest rates, but that is not what we have right now.

Distribution Analysis

As mentioned earlier in this article, the Clough Global Equity Fund has the primary objective of providing its investors with a high level of total return. However, as is the case with most closed-end funds, it aims to maintain a relatively stable net asset value and distribute the majority of its investment profits to the shareholders via a distribution. These investment profits include both dividends and capital gains and as anyone reading this is likely aware, capital gains can be quite large, especially when leverage is involved. Thus, we can probably assume that the fund will boast a fairly high distribution yield.

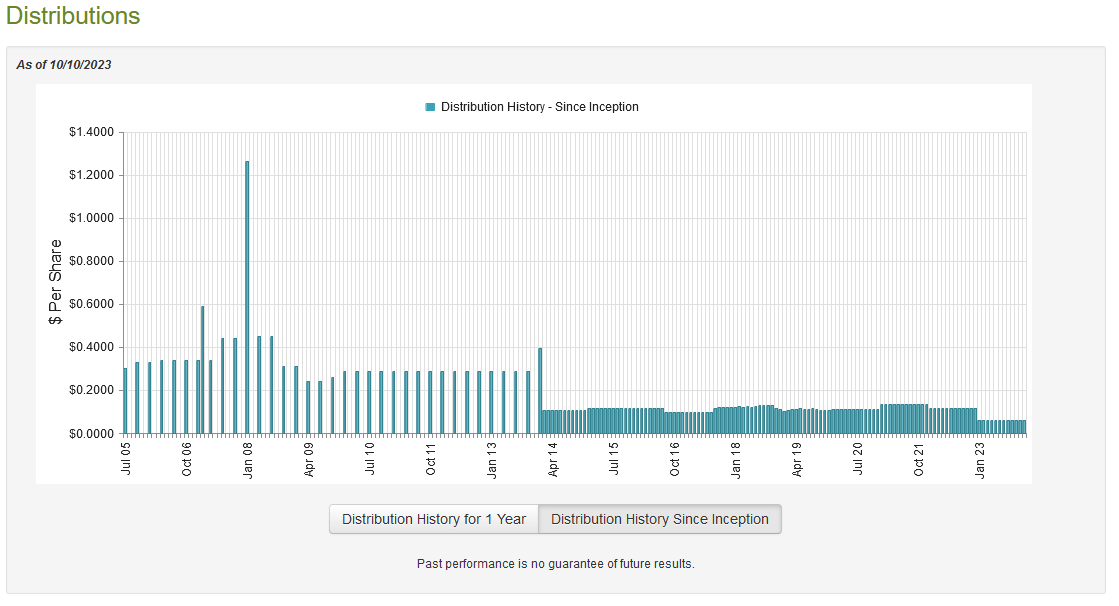

This is indeed the case, as the Clough Global Equity Fund currently pays a monthly distribution of $0.0599 per share ($0.7188 per share annually), which gives it a 12.93% yield at the current share price. This is easily in line with the best fixed-income funds available, and it is better than most equity funds. Unfortunately, the fund has varied its distribution considerably over the years:

{kind=link}

This considerable variation in the fund’s distribution over time will almost certainly reduce its appeal in the eyes of those investors who are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. It is not really surprising to see this from an equity fund though, as many of them do alter their distributions with the passage of time in order to reflect the investment performance of their underlying portfolios. After all, the goal here is to keep the fund’s net asset value relatively stable over time while paying out the investment profits to the shareholders. Equity investors typically tolerate fluctuating returns from indices and such so there is no reason why a fluctuating distribution from a fund following the above strategy should be an instant rejection.

As is always the case, we should have a look at the fund’s finances in order to determine exactly how it is paying for its distribution. After all, we do not want the fund to be depleting its asset base by paying out a distribution that is too high based on its investment performance. That is a sure way to cause the fund’s share price to deteriorate with the passage of time.

Fortunately, we do have a reasonably recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on April 30, 2023. While this report will not include information about the fund’s performance over the past few months, it is still (obviously) newer than the one that we had available to us the last time that we discussed this fund. It is also fairly nice for the time period that it covers. After all, the first half of 2023 was characterized by a very optimistic market that was expecting a rapid pivot in the Federal Reserve’s interest rate policy and driving up asset prices accordingly. This could have given the fund the potential to earn some capital gains by selling shares in this strong market.

During the six-month period, the Clough Global Equity Fund received $1,469,206 in dividends along with $1,340,656 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $2,836,064 during the period. It paid its expenses out of this amount, which left it with a $1,366,224 loss. This is quite concerning as the fund’s investment income was not sufficient to cover its expenses, let alone provide for a distribution to the shareholders. Despite this, the fund paid out $9,026,821 to its investors. Obviously, this was not covered by net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to afford its distributions. For example, it could have had some capital gains that can be paid out to the investors. The fund, unfortunately, had mixed results at this task. It reported net realized losses of $21,420,212 but this was fully offset by $22,518,087 net unrealized gains. That was still not enough for the fund to cover its distributions though, and its net assets declined by $9,295,170 during the period. That comes on the heels of a $119,805,080 net asset decline over the course of the prior year. This definitely explains why the fund had to cut its distribution, as it has clearly been paying out much more than it has been able to earn from the portfolio. It is unclear whether or not the fund will manage to cover its distribution at the new lower level, though. We will have to wait until the fund releases its annual report in a few months. I will admit that I am not especially optimistic about its prospects though, considering the severity of the weakness that we have seen in the equity market over the past two months.

Valuation

As of October 10, 2023 (the most recent date for which data is currently available), the Clough Global Equity Fund has a net asset value of $6.82 per share but the shares currently trade for $5.55 each. This gives the fund’s shares an 18.62% discount on net asset value at the current price. That is in line with the 18.57% discount that the shares have had on average over the past month, so the current price is quite reasonable. In addition, a double-digit discount is generally a good buying price for any closed-end fund.

Conclusion

In conclusion, the Clough Global Equity Fund is a globally focused closed-end fund that is very heavily invested in the United States. This is not necessarily the best situation for American investors, as most of them would be better off reducing their exposure to their home country and obtaining some international diversification. In addition to this, the fund’s strategy is an inherently high-risk and high-reward strategy as its substantial trading activity and use of leverage expose the fund to severe losses during periods of market weakness. This punished it during the 2022 bear market. It had to cut its distribution as a result of this, but Clough Global Equity Fund has still failed to cover its payout over the past eighteen months, and it is uncertain whether or not it can cover it at the new lower level. The fund does trade at an attractive discount, but it might be best to look elsewhere given the risks here.

For further details see:

GLQ: Best To Look Elsewhere Given The Risks Of This CEF