GLQ - GLQ: Latest Distribution Cut Highlights A Deeper Hole

Summary

- GLQ is an actively managed closed-end fund that invests primarily in equities while utilizing leverage.

- Our data shows that GLQ has been among the worst-performing equity CEFs in the market over the past year.

- Despite an 11% distribution yield, we recommend avoiding this fund.

The Clough Global Equity Fund ( GLQ ) invests across a diversified mix of global stocks with the flexibility to tilt across U.S. companies or into more of an international exposure. Like many other closed-end funds, GLQ has been challenged by the macro backdrop, while its particular strategy utilizing leverage has been further pressured amid rising interest rates.

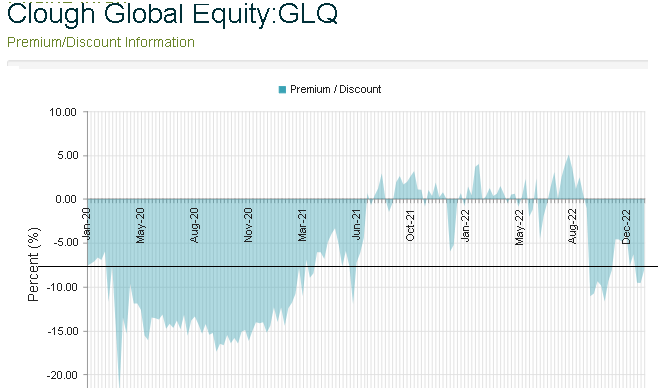

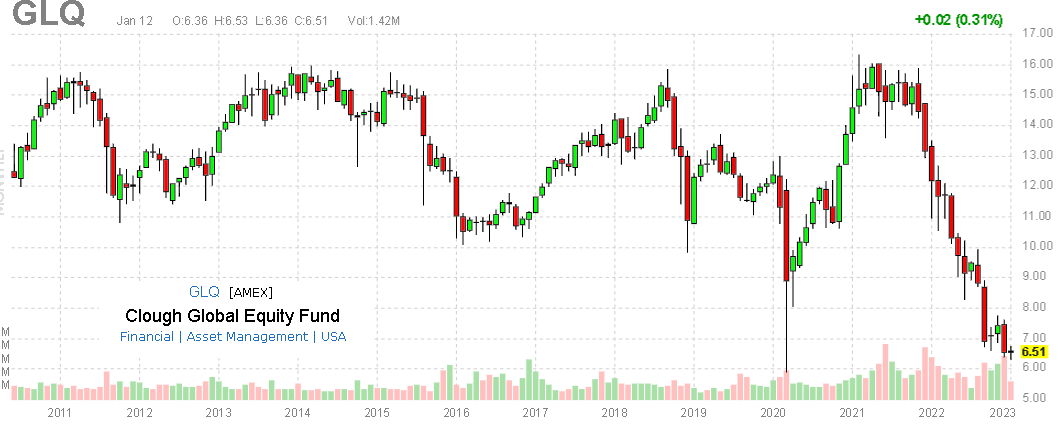

Indeed, shares of GLQ have lost more than 40% over the past year which is in the context of the broader market selloff along with a widening discount to NAV. The latest blow is the announcement of a large distribution cut to a new monthly rate of $0.0599 per share, aligning the payout with its depressed net asset value.

With the fund currently trading near an all-time low, the outlook isn't very encouraging. In our view, the problem is that GLQ has been a perpetual underperformer, standing out with a combination of weaker historical returns, and now a reduced yield compared to some alternative CEFs. Other than capturing the wave of a possible market-wide rebound, our call here is to avoid GLQ and its 11% yield.

What is the GLQ Fund?

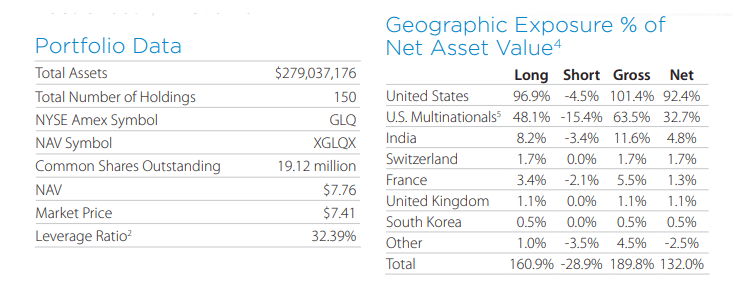

A key point with GLQ is that the strategy is actively managed, meaning the portfolio is not intended to follow any underlying index, but instead with an open-ended objective of "delivering a high level of total return".

From the current holdings, the strategy here can be described as long-short with the portfolio of equities balanced with a smaller short position on stocks representing approximately 20% of total assets. The idea, in theory, is to improve risk-adjusted returns as part of the portfolio management process.

The cash position is further collateralized with treasuries supporting further borrowing under an existing credit facility leading to a net leverage ratio of 32% at the end of November. By this measure, the net exposure is long stocks.

{kind=link}

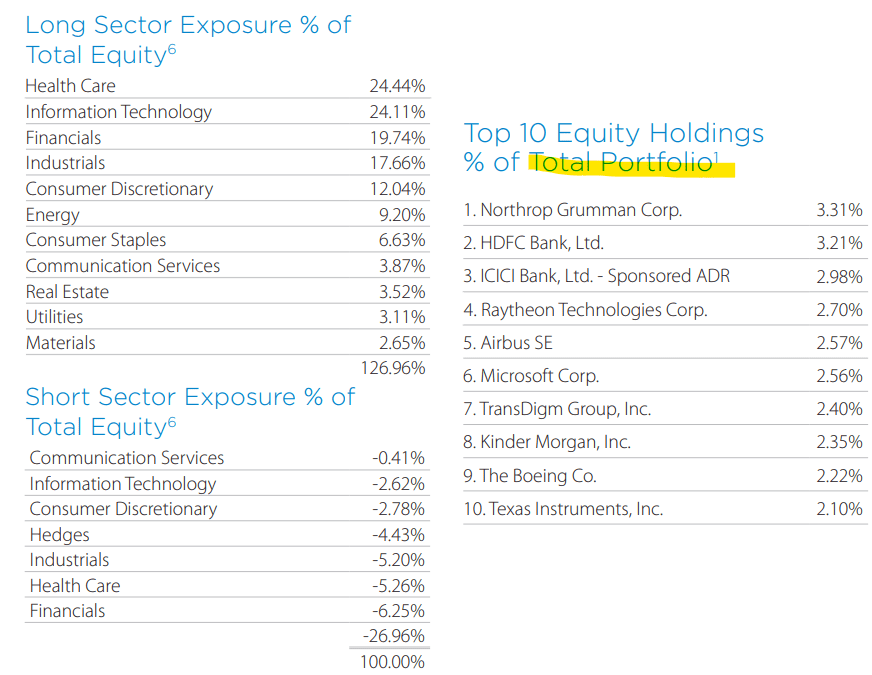

Going through the current holdings, there's an otherwise good variety of companies across different sectors. Healthcare and Tech sectors represent approximately 40% of the net long exposure while there are also large positions in the Financials, Industrials, and Consumer Discretionary sectors.

At the company level, aerospace and defense leader Northrop Gruman Corp. ( NOC ) is noted as the large position with a 3% weighting with its industry peer Raytheon Technologies Corp. ( RTX ), and Airbus SE (EADSF), and Boeing Co. ( BA ) all among top 10 positions. Down the list, several mega-cap market leaders like Microsoft Corp. ( MSFT ), Amazon.com, Inc. ( AMZN ), and Tesla, Inc. ( TSLA ) are also represented. Among foreign companies, the exposure is modest, representing less than 10% of the net long exposure.

{kind=link}

GLQ Poor Performance

Thus far, outside what we would consider high leverage and also a stretched expense ratio of 4.39% inclusive of the management fee and interest on debt, the profile is otherwise standard fare among CEFs. That said, as great as the setup may be on paper, the execution has left a lot to be desired.

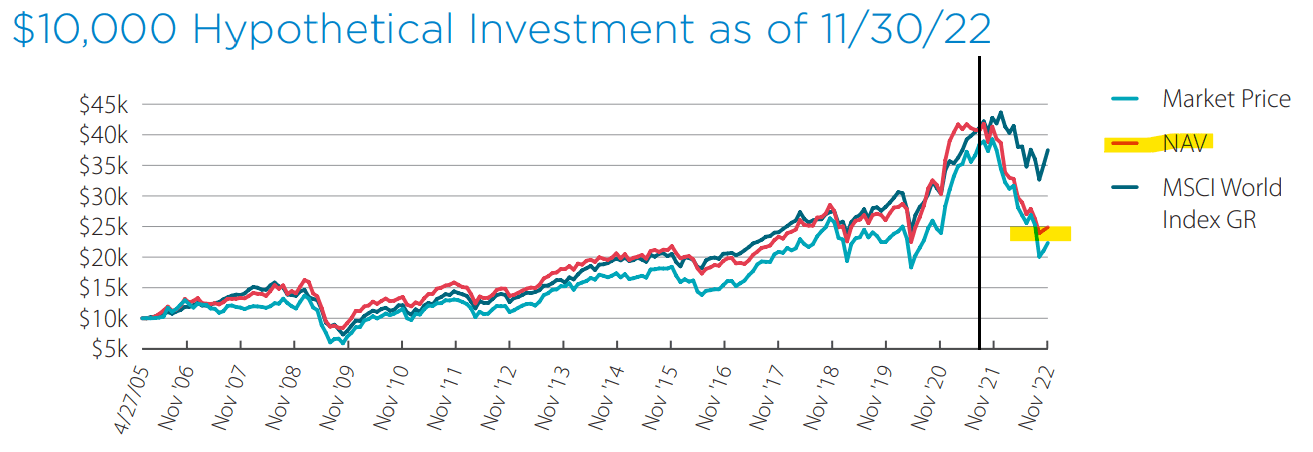

GLQ utilizes the MSCI World Index as a performance benchmark, which tracks the performance of global equities as an asset class from developed markets. What we find is that while GLQ managed to perform roughly in line with the benchmark historically, the correlation became disconnected particularly since late 2021.

{kind=link}

For comparison purposes, we'll use the iShares MSCI World ETF ( URTH ) as a reference point, which tracks the same index. Over the past decade, investors would have been better off just holding the ETF. The dynamic becomes more evident looking at the fund's -36% total return over the past year at NAV opening up a large spread to the -14% correction in the MSCI World Index.

It's true that GLQ's use of leverage explains some of this weakness as it has amplified the volatility, although the sense is that more could have been done to adjust the exposure to avoid this type of tracking error. Again, the expectation here is for GLQ to outperform its "passively managed" vanilla benchmark through a more sophisticated strategy which hasn't been the case.

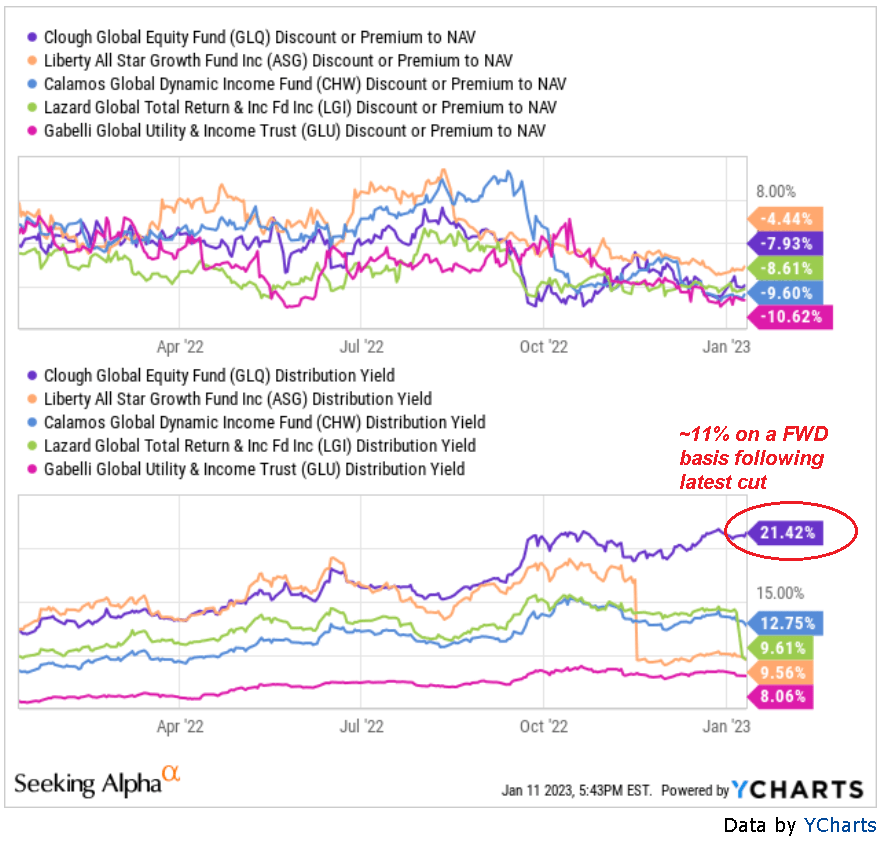

What's more concerning is that from the data we're looking at, GLQ is simply one of the worst-performing CEFs in its class. We're looking at a group that includes Liberty All-Star Growth Fund ( ASG ), Calamos Global Dynamic Income Fund ( CHW ), Lazard Total Return & Income Fund ( LGI ), and Gabelli Global Utility & Income Trust ( GLU ) which we've selected here because each are CEFs with an equity-focused allocation strategy that utilize leverage. At the NAV level, it appears the group began to recover in October while GLQ curiously continued to lag.

The pattern extends over a longer time frame. In the last five years, GLQ has generated a cumulative -16% decline, while ASG and LGI both managed a positive return closer to 40%

The point here is that say that CEF investors looking for a fund that offers a distribution yield of around 10% while trading at a discount to NAV have several options. From the same group above, GLU, CHW, and LGI all trade at a larger discount to NAV.

{kind=link}

With CEFs, it's often a balancing act between many different pros and cons considering risks and objectives like a higher or lower income, balanced by a higher or lower total return potential. For us, GLQ misses the mark on most measures.

Expanding our comparison to include some alternative high-profile "diversified equity CEFs", it's hard to find a fund that has done worse over the last several years. The takeaway for us is that something may be broken in GLQ's particular strategy.

What's Next For GLQ?

GLQ cross our radar given the latest distribution rate cut where the monthly amount was reduced by -49% to $0.0599 per share with confirmed payments through March. Oftentimes, a cut like this could signal a turnaround opportunity with shares selling off on the news beyond their implied value.

In this case, we can't recommend GLQ because we believe the fund should continue to underperform. We also expect its discount to NAV to further widen, reflecting reduced demand for the vehicle, with investors shunning the performance history and lack of any evidence towards alpha.

Even if the underlying portfolio recovers through a broad market rally in equities overall, the share price of GLQ could lag with the market assigning a structurally wider spread. The fund traded at a discount greater than 15% back in 2020, meaning there is some precedence for a further selloff.

{kind=link}

Final Thoughts

To conclude, GLQ is a disappointing fund that faces an uncertain future. There are several different types of corporate actions that will keep the fund going, but it is simply not worth it in our opinion. Investors would be better served in several other equity CEFs that can provide a similar or greater level of regular income while delivering a higher total return with potentially lower risk.

{kind=link}

For further details see:

GLQ: Latest Distribution Cut Highlights A Deeper Hole