GLQ - GLQ: Revisiting A 20% Yielding CEF

Summary

- Clough Global Equity Fund (GLQ) is a 60/40 CEF with leverage on top.

- 60/40 portfolios are having the worst annual performance since 1974, and GLQ has not been spared.

- Given its managed distribution policy, the fund now exhibits a 20% yield.

- This article covers CEFs from our suite of products - we focus on macro portfolio allocation, CEFs and yield generating options strategies, targeting overall yearly portfolio returns of 9%+.

Thesis

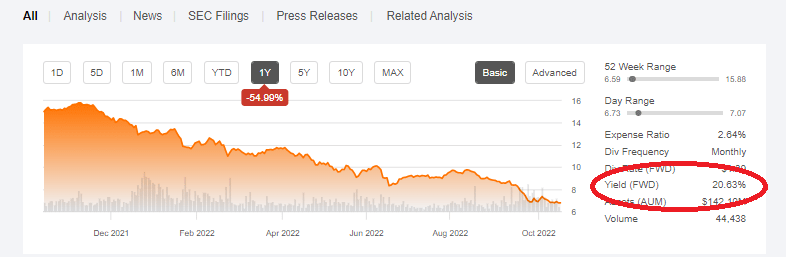

Clough Global Equity Fund ( GLQ ) is a 60/40 equities/debt CEF. The fund invests in global equities, but retains only U.S. government debt for its fixed income sleeve. The vehicle runs a very high leverage ratio, which is currently in excess of 50%. The worst year since 1974 for 60/40 portfolios, coupled with its high leverage, have resulted in GLQ posting a year to date return exceeding -40%. The decreasing NAV coupled with its managed distribution policy have resulted in a dividend yield of 20%:

Dividend Yield (Seeking Alpha)

{kind=link}

We expect this to be cut at year end, and result in a forward dividend yield sub 10%.

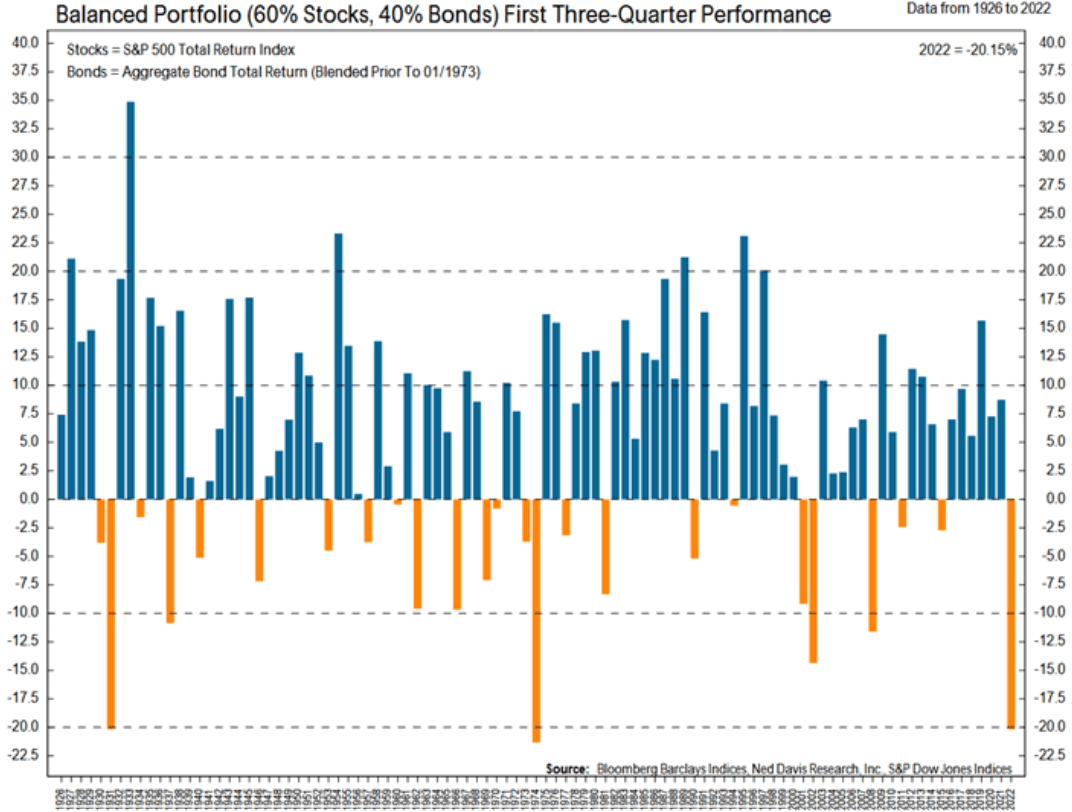

It has been a very tough year for 60/40 portfolios, with the current drawdown the largest since 1974:

60/40 Portfolio Performance (Data)

{kind=link}

When you add leverage on top as GLQ does, you get a -40% year to date performance. On the positive side, we can notice that such a drawdown is always followed by a number of years with strong positive returns. Do we expect history to repeat itself? Indeed, we do. Deconstructing the GLQ vectors for 2022: a) bond move, b) equity returns. On the bond side, we expect rates to peak in 2022, somewhere close to 5%. Once peak rates are in, we should expect a 5%+ annual performance for bonds, with longer duration ones posting higher gains. On the equity side we do not think we have seen capitulation, but once the current drawdown is over, we should expect a normalization of returns, which have historically been in the 6% to 12% per annum.

2022 has been a very unusual historic period through the lens of return drivers - inflation has caught the Fed unprepared, and in a bid to stem the tide they have raised rates at an unprecedented pace. This vertical rise in yields has produced a deep bear market for both bonds and equities. The reasons are not with the rate rises themselves, but with the velocity of the move. The same shift up in the yield curve, if it had occurred over a period of say 24 months, would have resulted in a very different outcome for the bond and equity markets.

We expect the rest of 2022 to be tough for GLQ, with peak rates not here yet and a final capitulation in equities still expected. However, 2023 will be a much better year for the CEF, as we can expect history to repeat itself and the fund to post consecutive years of strong growth after an abysmal 2022.

Holdings

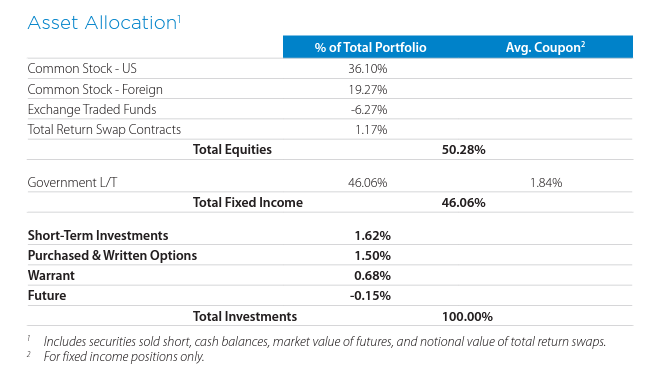

The portfolio has a 60/40 composition with leverage on top:

{kind=link}

On the equity side, the largest bucket is constituted by U.S. common stocks. The sectoral breakdown favors industrials and technology:

Sector Exposure (Fund)

On an individual name basis, the top holdings are a mix:

Top Holdings (Fund)

The top holding is Raytheon Technologies Corporation ( RTX ), an American multinational aerospace and defense conglomerate. RTX is set to do well on the back of the Russia / Ukraine. We can notice other defense companies in the top holdings, coupled with energy names.

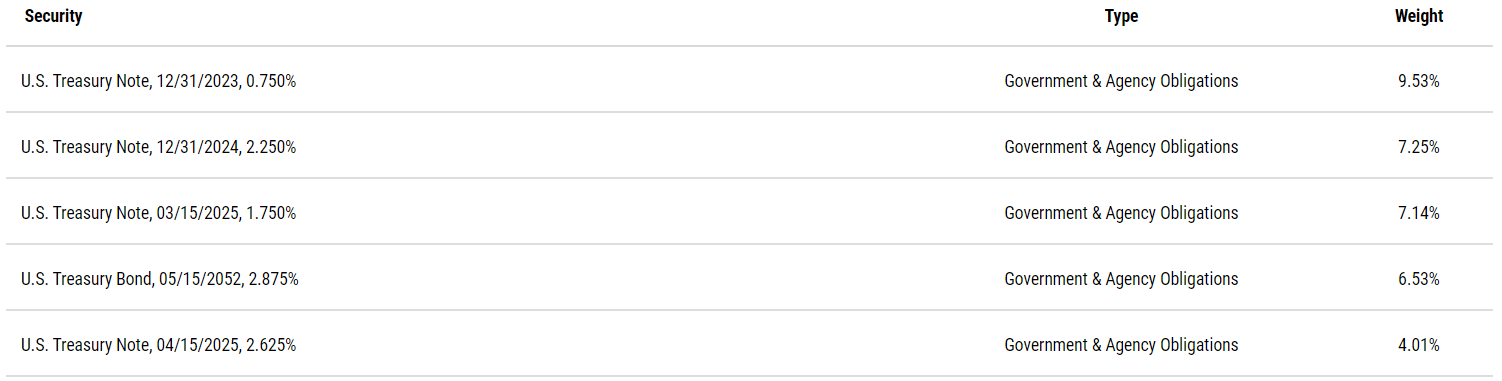

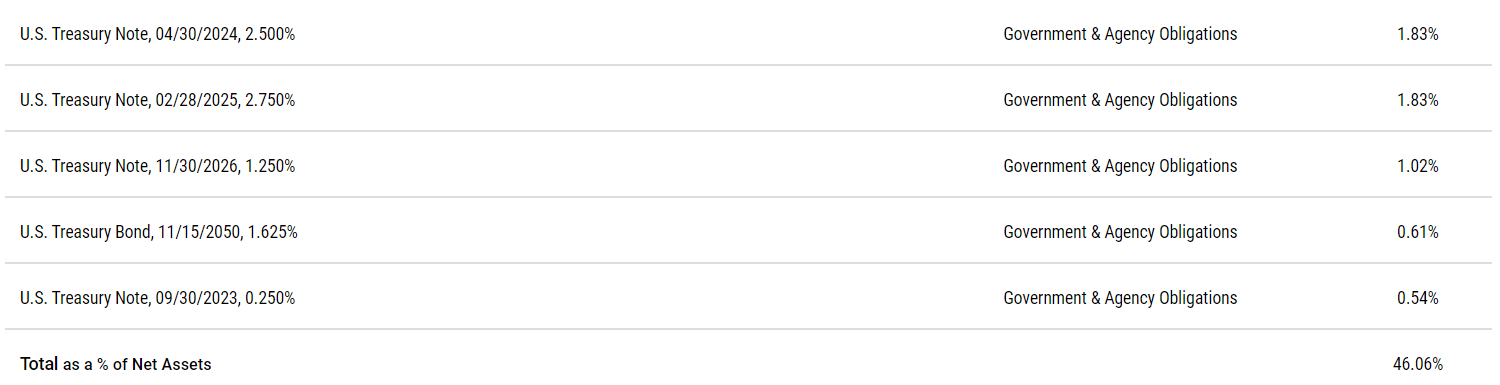

On the bond side, the CEF only holds U.S. government securities, with a laddered maturity profile:

Bond Sleeve (Fund) Bond Sleeve Table 2 (Fund)

{kind=link}

{kind=link}

We can see that the fund does not buy just one maturity in terms of government bonds. Instead, the CEF purchases Treasury notes that fall in the short term, intermediate and long term maturity buckets. By taking this action, the fund is giving itself exposure to the entire treasury curve, not just one tenor. This year has been a tough one for both bonds and equities. For a CEF which adds leverage on top of this structure, the result has been devastating.

Performance

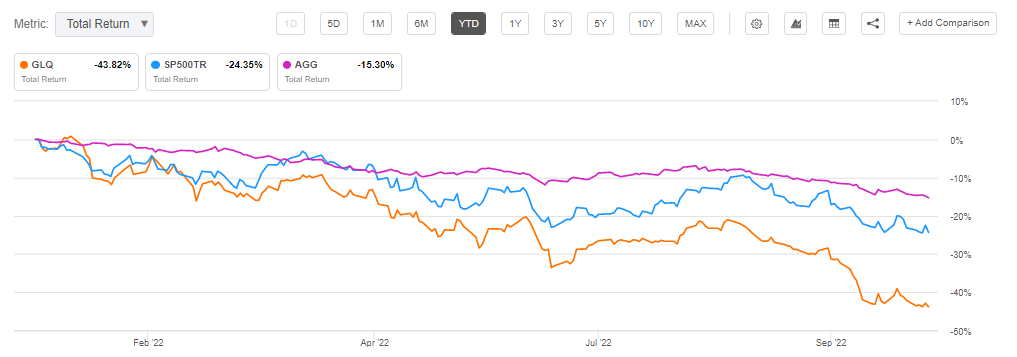

The fund is down more than -40% year to date:

YTD Performance (Seeking Alpha)

{kind=link}

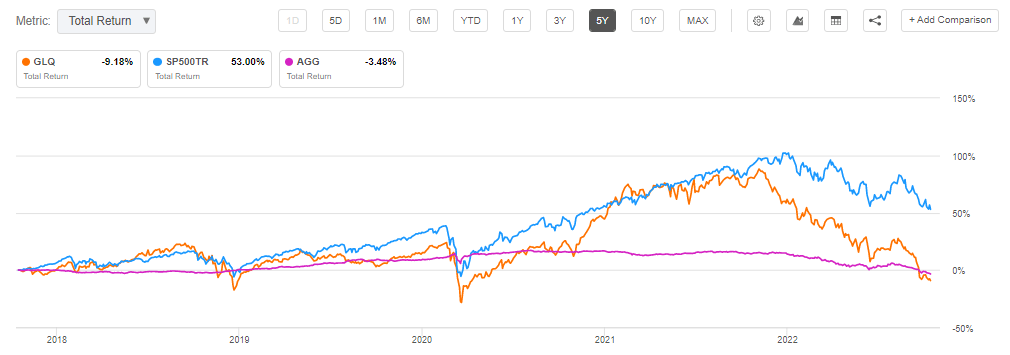

Today's tough environment has wiped out more than 5 years' worth of returns:

5Y Total Return (seeking alpha)

{kind=link}

It is disappointing when return profiles show this type of behavior. Investors should be mindful of cyclical or very leveraged funds that tend to significantly magnify down-moves, because years of returns can be wiped out fairly fast.

Premium / Discount to NAV

The fund's discount to NAV held fairly well around a flat level until recently:

It is fairly impressive to see that the fund was able to maintain a close to fair value market price throughout the 2022 turmoil.

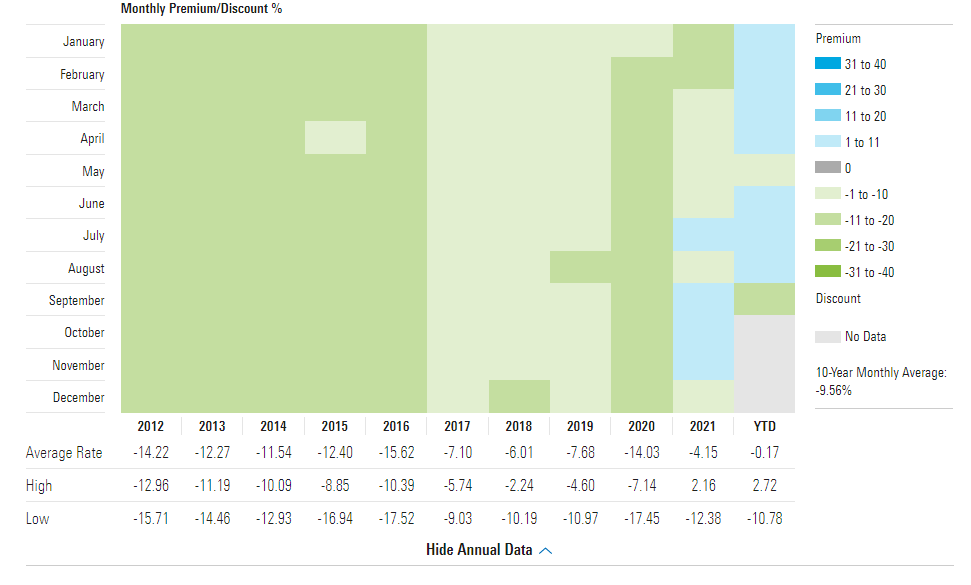

The fund usually trades at a discount to NAV:

Premium / Discount (Morningstar)

{kind=link}

We can see that, in the past, the CEF traded at an average -10% discount to net asset value.

Distributions

The fund has a managed distribution plan:

Distribution Plan (Annual Report)

{kind=link}

The vehicle pays 10% of the past year NAV. Given the significant drop in NAV in 2022 expect the distribution to fall accordingly.

Given where NAV is now, the distribution going forward once the re-set occurs should be close to $0.7 monthly

Given its performance, the fund is utilizing a significant amount of ROC to sustain the current artificial dividend:

{kind=link}

We can see that for the September distribution, 100% of the dividend is ROC, while for the current fiscal year approximately 33% is ROC and rising. As we said before in other articles, when the underlying assets in a CEF are not performing, then an investor should expect ROC. Cash needs to be generated either via interest income or capital gains, thus when the collateral underperforms the vehicle will resort to return of capital.

Conclusion

GLQ is a 60/40 CEF. The fund holds U.S. Treasuries for the fixed income sleeve and global equities for the stock bucket. The CEF is down more than -40% year to date given the worst year since 1974 for 60/40 portfolios, and the large leverage (over 50%) the fund runs. Leverage magnifies moves both on the upside and the downside. The fund has a managed dividend distribution policy that aims to return 10% of year end NAV. This policy, coupled with the NAV decrease this year, has resulted in a 20% current dividend yield. The yield is not supported, being paid currently exclusively from ROC. We expect the dividend to be cut early next year to the managed policy level. The rest of 2022 will be tough for GLQ, with peak rates not here yet and more equity weakness to come. However, as history shows us, the following years from such a vicious drawdown always display very robust results. We expect a much brighter 2023 for the fund as rates peak and equities rebound.

For further details see:

GLQ: Revisiting A 20% Yielding CEF