GLV - GLV: Caution Is Advised With This Highly Levered CEF

2023-04-03 07:15:12 ET

Summary

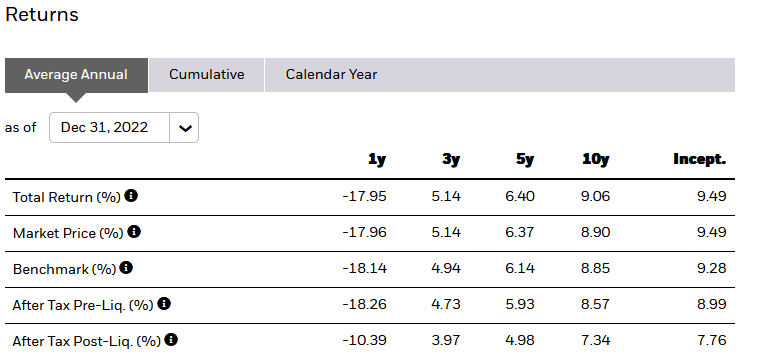

- GLV claims to invest in a globally-oriented portfolio of stocks and bonds in order to provide its investors with a high level of total return.

- Most American investors are far too heavily exposed to the United States, which has serious financial problems that will be a drag on economic performance.

- GLV does not do a particularly good job at achieving international diversification, as nearly all of its portfolio is invested in the United States.

- The fund offers a very nice 12.57% yield, but this may not be sustainable.

- The fund is currently trading at a very attractive discount.

Many American investors today have an outsized proportion of their portfolios invested in the United States. This is certainly understandable, as the American market has outperformed most others over the past decade, but it is also a very real risk. In particular, the investor is going to be too exposed to problems in the United States. If an investor has their assets sufficiently diversified globally, there is less of a reason for concern over problems that only affect one specific country. As the United States is currently facing significant political and fiscal problems, there are certainly some reasons to expect that foreign markets may deliver better performance over the next decade. As such, it could be a good idea to spread your assets around the world in order to take advantage of these opportunities and reduce your exposure to the problems facing the United States.

One method through which we can obtain exposure to foreign markets is by purchasing shares of a globally-oriented closed-end fund. These funds are generally not very well followed in the investment media and many financial advisors are not familiar with them. That is a shame because they offer a number of advantages over traditional mutual funds, such as the ability to boast a substantially higher yield. They are also able to use certain strategies not available to open-end funds, which can have the effect of substantially boosting their returns.

In this article, we will discuss the Clough Global Dividend and Income Fund ( GLV ), which is one such globally-oriented closed-end fund. As of the time of writing, this fund yields a remarkable 12.57%, which could be concerning. This is because any yield in the double-digits is a sign that the market expects that the fund will cut its distribution in the near future. We will be sure to investigate that risk in this article. I have discussed this fund before, but as a few months have passed since that time, obviously a great many things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund's financial condition.

About The Fund

According to the fund's webpage , the Clough Global Dividend and Income Fund has the stated objective of providing a high level of total return. This is not particularly surprising considering that the name of this fund implies that it will invest primarily in common equities. In fact, approximately 96.54% of the fund's portfolio consists of common equity:

CEF Connect

The negative weighting to cash comes from the fact that this fund employs leverage as part of its strategy. We will discuss this in greater detail later. The important takeaway for the moment is that this is a common equity fund. This is why the focus on total return is not particularly surprising, as common equity is by its nature a total return instrument. After all, we typically purchase common equities with the intent of receiving dividend income and capital gains as the issuing company grows and prospers. This fund's name implies that it is seeking out dividend-paying common stocks from around the world in pursuit of this objective.

The name of the fund sponsor is Clough Global, so the name of the fund alone does not actually indicate that this is a global fund. However, the summary of the fund's strategy provided by the fund sponsor does support this conclusion. According to the fund's webpage,

Searching globally for the most opportunistic investments in the capital markets, the Fund's investment objective is to provide a high level of total return. The Clough Global Dividend and Income Fund seeks to pursue this objective by applying a fundamental research-driven investment process and will invest in equity and equity-related securities as well as fixed-income securities, including both corporate and sovereign debt, in both U.S. and non-U.S. markets.

That description clearly indicates that this is a global fund. However, a look at the largest positions in the fund reveals something quite different. Here they are:

{kind=link}

Of this list, only Airbus SE ( OTCPK:EADSY ) and Medtronic ( MDT ) are foreign companies. The rest of these are American firms. In fact, an overwhelming percentage of the fund is invested in the United States:

Clough Global

This was the same thing that we saw the last time that we looked at the fund, and it is quite disappointing to see. As I have pointed out in various previous articles, most global funds have about a 60% weighting to the United States, but this one goes far beyond that. In fact, this fund is best thought of as a domestic equity fund with token foreign exposure. Thus, it will not do a pretty good job of protecting us against regime risk. Regime risk is the risk that some government or other authority will impose some law or take some action that has an adverse impact on a company in which we are invested. When we consider that American investors already tend to have outsized exposure to the United States, this fund clearly provides little help in reducing the overall exposure of your portfolio to domestic risks.

Achieving international diversification is something that could prove critical today due to the very poor state of America's government finances. According to the World Bank , once a country's debt-to-gross domestic product gets above 77%, it experiences a slowdown of economic growth. This effect is cumulative. The World Bank study found that each percentage point of debt above 77% costs the country 0.017% in economic growth. The United States currently has a debt-to-gross domestic product ratio of 122% and the latest budget presented by the Biden Administration has this ratio getting much worse over the next decade. The Congressional Budget Office is sounding a warning as to how this will affect economic growth. The agency projects that real gross domestic product growth will not exceed 3% ever again, and it will steadily decline after 2025:

{kind=link}

That will eventually have an impact on the stock market since no company can indefinitely sustain growth that is higher than gross domestic product growth. It is worth noting that the projections above also assume that the Federal government will not engage in any new spending programs, which seems incredibly optimistic. Thus, the actual performance of the United States will likely be worse than this over the long term. This is not the case globally, though, as there are numerous countries with much better long-term fundamentals that should be included in a portfolio.

One other thing that we notice from looking at the fund's largest positions above is that it has substantially changed its portfolio in just the three months since we last looked at it. In addition to reducing its bond allocation in favor of common stocks, the fund also changed numerous companies:

| Removed Companies |

| Added Companies |

| Merck & Co. ( MRK ) |

| Morgan Stanley ( MS ) |

| Starwood Property Trust ( STWD ) |

| Bank of America ( BAC ) |

| American Tower ( AMT ) |

| Home Depot ( HD ) |

| Kinder Morgan ( KMI ) |

| Broadcom ( AVGO ) |

| HDFC Bank ( HDB ) |

| Medtronic |

The fact that so many positions have changed over the past three months is a sign that this fund may have a very high turnover. That is certainly correct, as the Clough Global Dividend and Income Fund had a 199.00% annual turnover in 2022, which is the highest level that I have ever seen an equity fund possess. The reason why this is important is that it costs money to trade stocks or other assets, which is directly billed to the shareholders of the fund. This creates a drag on the fund's performance and makes management's job more difficult. This is because the fund's managers need to generate sufficient excess returns to both cover these extra expenses as well as still deliver a return that satisfies the investors. There are few management teams that can accomplish this consistently, which results in most actively-managed funds underperforming their indices. This fund has certainly not been an exception to this, as shown here:

{kind=link}

There is admittedly not a perfect index to compare to this fund, but this performance was consistently worse than the S&P 500 Index ( SPY ) over the same period. It was also consistently worse than the MSCI World Index ( URTH ) over any given period:

{kind=link}

The Clough Global Dividend and Income Fund does have a higher yield, but in the end, it is the total return on net asset value that matters the most, and as we can see, investors would have been better off with an index fund.

Leverage

As stated in the introduction to this article, closed-end funds such as the Clough Global Dividend and Income Fund have the ability to deliver a higher yield than any of the underlying assets possess. One method that is employed to accomplish this is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase stocks, bonds, and other assets. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, then the strategy works pretty well to boost the total return of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. Thus, when the market declines, the fund will lose more money than it would if it had no leverage. This could be one reason for the poor performance over the past year relative to the indices, although it does not explain why the fund underperformed during strong markets. Due to this added risk, we want to ensure that the fund does not employ too much leverage since that would expose us to too much risk. I generally do not like to see any fund have leverage above a third as a percentage of its assets for this reason. Unfortunately, the Clough Global Dividend and Income Fund's levered assets currently comprise 47.25% of its portfolio. That is the highest leverage that I have ever seen a closed-end fund employ and it is indicative of a high-risk, high-potential reward strategy. As the fund is failing to beat the indices even in good years, it is not accomplishing the high reward part of this dynamic very well. The high leverage, therefore, is a very real concern.

Distribution Analysis

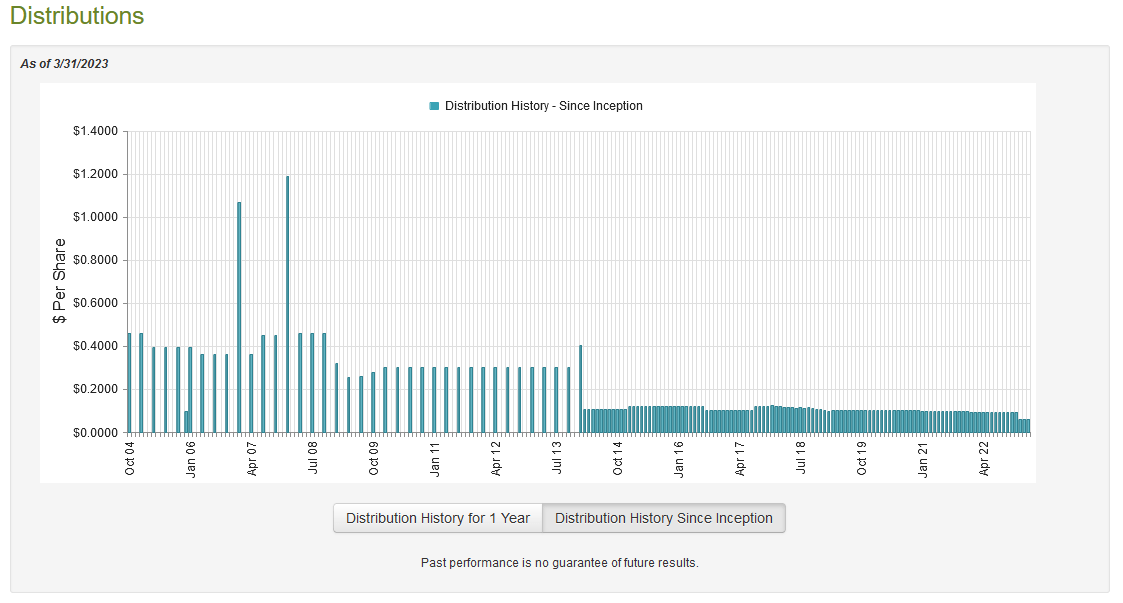

One of the biggest reasons why people purchase shares of closed-end funds is the incredibly high yields that many of these funds possess. In fact, the goal of most closed-end funds is to maintain a reasonably flat share price while paying out all of their investment profits (dividends and capital gains) to the investors. This is one reason why these funds tend to have very high yields compared to just about everything else in the market. The Clough Global Dividend and Income Fund is certainly no exception to this as the fund pays out a monthly distribution of $0.0597 per share ($0.7164 per share annually), which gives it a 12.57% yield at the current price. Unfortunately, the fund has not been particularly consistent about its distribution over the years and reduced its payout back in January:

{kind=link}

The fact that the fund's distribution has varied so much over the years could prove to be a bit of a turn-off for those investors that are seeking a safe and secure source of income to use to pay their bills or otherwise finance their lifestyles. The fact that the fund currently has a double-digit yield adds to these concerns as the market apparently believes that the fund will not be able to maintain its distribution even at the new lower level. Let us have a look at this since we obviously do not want to be the victims of another distribution cut, as that would reduce our incomes and almost certainly cause the fund's share price to decline further.

Fortunately, we do have a relatively recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the full-year period that ended on October 31, 2022. Although this report will not include information from the past few months, it is still a newer report than we had available the last time that we reviewed this fund and as such will give us a much better idea of how well the fund weathered the challenging market conditions of 2022. During the full-year period, the Clough Global Dividend and Income Fund received $1,855,737 in dividends and $1,784,110 in income from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund reported a total of $3,670,590 in income during the period. It paid its expenses out of this amount, which left it with a negative $184,420 available for the shareholders. Obviously, that is not enough to pay any distribution, yet the fund still distributed $13,197,196 to its investors. At first glance, this is certain to be concerning as the fund is not able to cover its distribution out of net investment income.

However, a fund has other means that can be used to obtain the money that is needed to cover the distribution. For example, it might have capital gains. As could be expected from the challenging conditions in 2022 though, the Clough Global Dividend and Income Fund failed miserably at that task during the period. The fund had net realized losses of $13,494,914 and another $17,283,546 million of unrealized losses over the year. Overall, its assets declined by $31,201,479 after accounting for all inflows and outflows. The fact that the fund's assets went down despite the fact that it raised $12,228,308 of new shares is concerning. It appears that the fund paid its distributions out of the new money that it raised, which is not sustainable over any sort of extended period. This certainly explains the distribution cut, but if the fund cannot reverse its fortunes, it will have to cut the distribution again. Thus, there could be cause for concern here and we should keep a close eye on the fund's finances over the coming months.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Clough Global Dividend and Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of March 31, 2023 (the most recent date for which data is available as of the time of writing), the Clough Global Dividend and Income Fund had a net asset value of $6.91 per share but its shares only traded for $5.78 per share. This gives the fund a discount of 16.35% at the current price. That is a very attractive discount that is much better than the 11.34% discount to net asset value that the shares have averaged over the past month. Thus, the price appears acceptable today.

Conclusion

In conclusion, the Clough Global Dividend and Income Fund is not using a strategy that would be expected. This is not a buy-and-hold fund; instead, it heavily utilizes the trading of assets as a critical part of its strategy. Unfortunately, this also results in the fund having incredibly high costs that have made it difficult for the fund to beat any of the indices. The fund also lacks global exposure, despite the name. That is a real shame because the United States has some serious problems that make it critical for investors to have sufficient foreign exposure. The fact that the distribution may not be sustainable overshadows the fact that the yield is fairly nice, and the fund has a very attractive valuation. Overall, caution is strongly recommended here.

For further details see:

GLV: Caution Is Advised With This Highly Levered CEF