GLYC - GlycoMimetics Has Few Risks Great Outlook In Leukemia

2023-04-04 08:35:08 ET

Summary

- Its lead drug candidate is in Phase 3 development for multiple leukemia indications.

- Mechanism has utility in other cancer and non-cancer diseases.

- Perceived trial delays punished the stock.

- Delays actually raise the odds of greater survival with treatment vs. known standard of care.

- Pivotal trials are more likely than not to succeed, leading to approvals and future sales of several multiples over current cap.

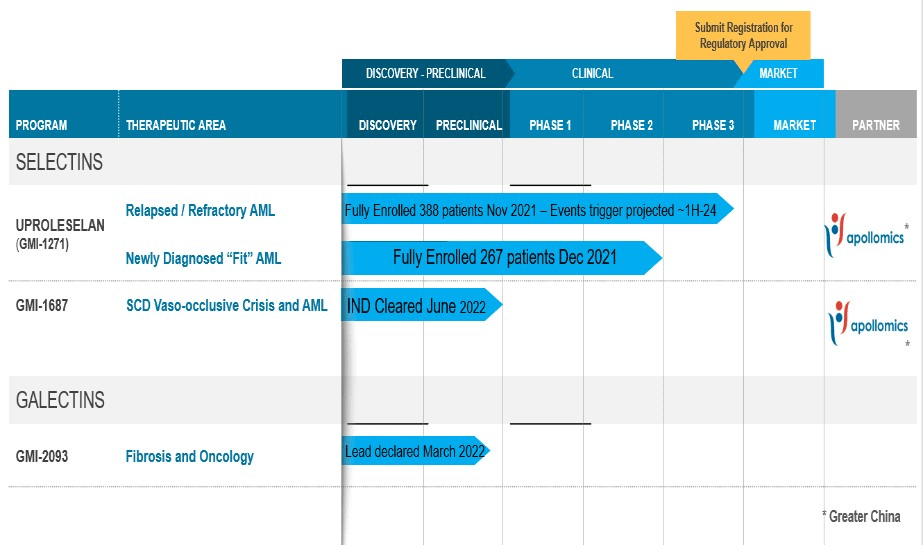

GlycoMimetics ( GLYC ) is a microcap (~$80 million) late clinical-stage biotechnology company developing glycobiology-based therapies for cancers and inflammatory diseases. On February 15, the stock tanked 62% as the independent Data Monitoring Committee (DMC) recommended the pivotal Phase 3 study GMI-1271-301 of uproleselan (yoo’ pro le’se lan or UPRO for short) in relapsed/refractory (R/R) acute myeloid leukemia (AML) continue to the originally planned final overall survival (“OS”) event trigger, dashing investor hopes that the DMC would find compelling enough efficacy data to stop the trial early. The company also disclosed selling 11,776,784 shares of common stock under its existing “at-the-market” (ATM) sales facility. During the runup, prices ranged from $2.42 to $4.16, so the company did well in averaging $3.01 and raising $28.7 million in net proceeds to add to $47.9 million cash as of December 31, 2022, although the shareholders suffered a 22% dilution. While some investors may be discouraged by a seemingly longer wait to 2024 (Figure 1), there are hidden catalyst events.

Figure 1. GlycoMimetics Pipeline

{kind=link}

AML and UPRO

As of 2019, there were 69,700 people living with AML in the U.S. and an incidence rate of 4.1 per 100k population, meaning approximately 13,700 are diagnosed annually, not all of whom are medically fit for chemotherapy. For the 80% who do get treatment , at least 40-50% of patients relapse . Therefore, the total addressable market ("TAM") with the current population increases by around 5,500 new R/R cases per year. One tumor microenvironment drug resistance mechanism of cancer cells is to bind to E-selectin (aka CD62E) in bone marrow, making them less susceptible to chemo. UPRO is a first-in-class, E-selectin antagonist (Figure 2) that blocks cancer cell adhesion and spreads them back into the blood; in theory, this bunker-buster will improve chemo response rates, duration of remissions and survival.

Figure 2. UPRO Mechanism of Action

Apollomics

UPRO has received the following designation statuses:

- Fast Track designation from the FDA for treatment of adult patients with relapsed or refractory AML and elderly patients aged 60 years or older with AML

- Breakthrough Therapy designation from the FDA and the China National Medical Products Administration Center for Drug Evaluation for treatment of relapsed/refractory AML

- Orphan Drug designation from the FDA and EMA Committee for treatment of patients with AML

UPRO in R/R AML

The clinical basis for confidence that Study 301 will be positive mainly comes from GMI-1271-201 (Study 201). Study 201 was a Phase 1/2 multicenter, open-label, dose-escalation trial to establish the recommended Phase 2 dose (RP2D). Patients in the R/R cohort were given UPRO with mitoxantrone, etoposide, and cytarabine (“MEC”). In 54 patients who received the RP2D of 10 mg/kg, the median OS was 8.8 months , while the rate of complete response or complete response with incomplete blood count recovery (CR/CRi) was 41%, with most responses being the preferred CRs (35%) in this difficult-to-treat group.

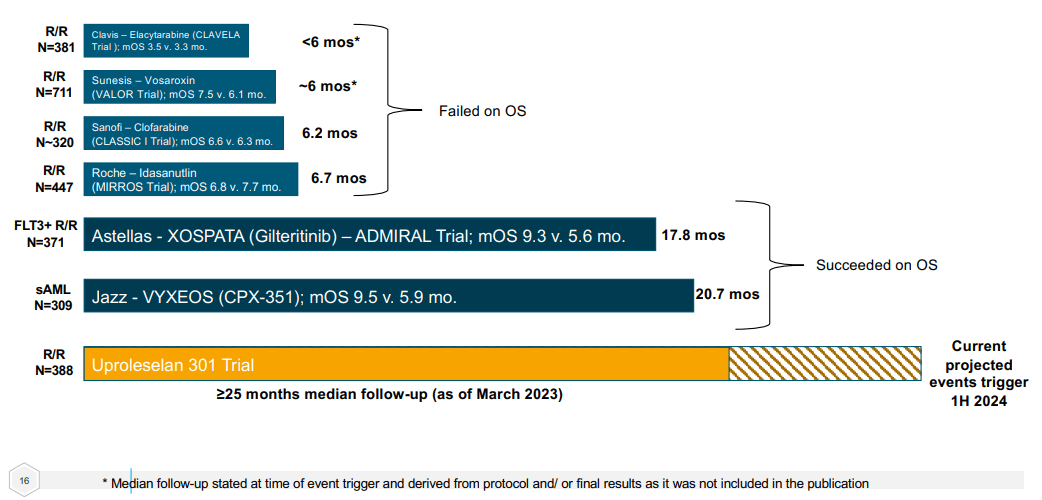

Study 301 is double-blind, randomized, placebo-controlled trial (“RCT”) evaluating UPRO in addition to a traditional high intensity chemo regimen, either MEC or fludarabine, cytarabine, granulocyte colony-stimulating factor and idarubicin (FLAG-Ida), with a primary endpoint (“PEP”) of OS. With participants living longer than expected, the median follow-up prior to primary analysis will be an unheard of 35-40 months in the R/R setting (Figure 3). Aside from these RCTs, there was a large retrospective analysis of 259 European R/R AML patients who received FLAG-Ida with or without Pfizer’s ( PFE ) MYLOTARG. After a median follow-up was 2.1 years (25 months) , the OS in either group were no different, at 0.7 years.

Figure 3. Duration of Follow-Up and Outcomes in Key AML Trials

{kind=link}

UPRO in Frontline AML

Everybody’s been asking about the National Cancer Institute’s ("NCI") Phase 2/3 clinical trial (A041701) evaluating UPRO, with or without standard “7 + 3”, in 267 newly diagnosed older adults with AML who are fit for chemo. The 7 + 3 is named for the number of days on daunorubicin and cytarabine, respectively. A planned interim analysis of the event-free survival (“EFS”) Phase 2 PEP is upcoming. Chief Business Officer Armand Girard said, “What they’re trying to show is that if the combination arm of upro plus 7 and 3 achieves a hazard ratio better than 0.831 , then the study will proceed to Phase 3. And if the hazard ratio is better than 0.64, that’s what they would classify as overwhelming efficacy.” If so, UPRO could be used in the frontline setting, encompassing all fit AML patients.

The above projections are likely based on the pivotal 280-patient ALFA-0701 trial of MYLOTARG. After 5 years, a hazard ratio of 0.84 was calculated for its EFS PEP. MYLOTARG was approved as a combination regimen with 7 + 3 for newly-diagnosed CD33-positive AML, even though there was no statistically significant difference in survival or CR/CRi with 7 + 3 alone. After a median follow-up of 43 months in alive patients, the OS in the treatment group of 27.5 months vs. 21.8 months in the control group (p=0.16).

The A041701 interim analysis for 1-year EFS rate has good odds to be positive because the study completed enrollment in November 2021 when recruitment was suspended and passed the initial futility analysis earlier that year. Those events mean that median follow-up is over 15 months and counting and HR is unlikely to go over 0.83. The primary (not final) analysis of ALFA-0701 had an overall (not just in alive patients) median follow-up of 14.8 months , with the median EFS of 15.6 months vs. 9.7 months (0.58 HR, p=0.0003) favoring the MYLOTARG combo. Study 201 had a small newly diagnosed cohort also using 7 + 3. In 25 patients who received the RP2D, the median OS was 12.6 months, EFS was 9.2 months, and CR/CRi was achieved by 72% of patients (52% CR).

Apollomics Catalysts

GlycoMimetics hasn’t mentioned Apollomics ( APLM ) at all on any 2022 earnings calls or reported any developments on the China front, and no analyst has inquired. People may forget GlycoMimetics is eligible for $179 million in development, regulatory and commercial milestone payments, as well as tiered royalties ranging from the high single digits to 15% based on net sales. Things may be moving quicker than some realize. A Phase 3 double-blind RCT of UPRO (APL-106) administered with MEC versus MEC alone with OS as PEP is estimated to complete in October , and unless something was lost in translation, that means not just enrollment completion, but topline results as early as Q4.

Apollomics also licensed GMI-1687, the more potent follow-on E-selectin antagonist suitable for subcutaneous administration, which was cleared for human trials last June. A University of California Davis/NCI Phase I trial of frontline UPRO in combination with Bristol Myers Squibb’s ( BMY ) ONUREG and AbbVie’s ( ABBV ) VENCLEXTA in 8 older or unfit AML patients saw 75% achieve CR/CRi . In an interview, lead investigator Dr. Brian Andrew Jonas said UPRO has the potential to treat patients with AML across any stage of disease (0:23 in the video). Apollomics may have been inspired and plans to explore GMI-1687 with these agents in AML as well as other combinations in multiple myeloma. One of the milestone payment triggering events is the initiation of the first GMI-1687 clinical trial for each indication in Greater China. Finally, the company just went public, possibly leading to more information from their side of the ocean.

Risks

GlycoMimetics is a biotech, which investors should know come with typical risks. The company has only one drug candidate in late-stage clinical studies; if any of those fail, it essentially spells the end of the business. AML is a deadly disease and patients in UPRO arms have died, although those weren't attributed to the drug; heretofore unknown safety issues may arise. Covid-19 may have or could disrupt the trials. If GlycoMimetics mistimes the ATM sale on the anticipated price surges on positive readout and approval, they may raise less money than needed for a go-it-alone launch, but management has been judicious so far. There are some competitors targeting certain mutations, but UPRO has broad application. Collaborators such as Apollomics may decide to abandon their partnerships, or in the case of GMI-1687, decide the AML trial is too expensive. Even if UPRO is approved, the company itself hasn't marketed any products, may not be able to differentiate their product or educate enough prescribers, so sales may not meet expectations. Only the last two have some probable chance of happening. Note that several senior leaders have substantial commercialization experience, including President and Chief Executive Officer Harout Semerjian.

Financials and TAM

Net loss in 2022 was $47.4 million with a lower $10.6 million burn in Q4. Therefore, it is reasonable to believe management claims that it can fund operations at least to the end of 2024, including the potential marketing authorization application submissions to the FDA and EMA. The extended Phase 3 durations can only be good for GlycoMimetics, as it gets more and more unlikely that chemo can keep up with UPRO, and even a few long-lived patients on placebo won’t be enough to skew the median. Furthermore, Chief Medical Officer Edwin Rock said, “Blinded pooled data show that the transplant rate in the study is above the 31% transplantation rate observed in the preceding Phase 1/2 trial.” Finally, UPRO seems to lower the risk of mucositis, the most common and distressing toxicity caused directly by AML chemo, occurring in 20-40% of recipients . Mucositis lowers quality of life by impairing patients’ ability to eat, swallow and talk. Astonishingly, Grade 3 (severe or medically significant but not immediately life-threatening) mucositis was seen in only 2% of Study 201 subjects, a factor in none of them discontinuing the trial due to any adverse effect.

If approved, a low estimation of future sales could be modeled from Astellas Pharma’s ( OTCPK:ALPMF ) XOSPATA, which is only indicated for R/R AML. The kinase inhibitor is mutation-targeted therapy; therefore, UPRO should easily least top its U.S. launch (Table 1). Even if the efficacy ‘eye test’ let's XOSPATA keep its preferred spot in the guidelines, the FLT3 mutation only occurs in about 30% of AML . But Study 301 takes all comers, making UPRO a direct competitor and initial TAM stays around 19,500. R/R AML has the best supportive evidence, but a positive A041701 doubles the TAM (the trial excludes FLT3) to about 39,000 plus 7,500 annually.

Table 1. XOSPATA Product Sales (in $ millions, assuming 1¥ = $0.0075)

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 15 |

| 78.75 |

| 116.25 |

| 141.75 |

Takeaways

To conclude, UPRO has demonstrated encouraging efficacy and safety data across several studies and study populations in AML that bode well for the pivotal trials. It has a novel mechanism that rationally complements any standard chemo regimen and opens up the pipeline to broader use of selectins in AML, other cancers and even non-oncological indications. If approved, UPRO should command six-figures as an orphan drug. This means that at a bargain $100,000 a pop, it only takes a mere 4% penetration of current fit the R/R AML market to break $80 million the first year as a base case (only 2% needed if frontline ). Because a conservative 5% of frontline patients rakes in nearly $200 million after a couple of years, obviously there's a real chance at blockbuster status just on U.S. sales if it gains wide enough acceptance.

All these factors indicate GlycoMimetics should not be languishing under a $100 million cap even with dilution. The protection against mucositis alone would be a decisive competitive advantage in the market, making other AML treatments more tolerable, not to mention profitable. Perhaps enough for a bigger company wanting to keep the combo exclusive to itself through licensing or M&A.

For further details see:

GlycoMimetics Has Few Risks, Great Outlook In Leukemia