XHB - GMS Stock: Mixed Q2 Results Keep Us On The Fence

2023-12-14 16:16:04 ET

Summary

- GMS reported Q2 results, which beat expectations, balanced by a soft growth outlook.

- The company has benefited from resilient activity in multi-family and commercial construction, while lower steel prices has pressured sales for framing products.

- The company has overall solid fundamentals but we see limited upside for the share price through 2024.

GMS Inc ( GMS ) recently reported its latest quarterly results, with revenue and EPS coming in above expectations. The company recognized as a leading manufacturer of wallboard, ceilings, and steal-framing installations has benefited from the resilient construction activity despite the volatile macro backdrop over the past year. Indeed, the stock is up more than 40% in 2023.

The recent momentum here considers some enthusiasm for a resilient economy and stabilizing interest rates into 2024, as supporting residential and commercial building markets.

That being said, we highlight an otherwise soft growth outlook and lingering uncertainties for the housing market as potential headwinds for shares to keep climbing going forward. With GMS trading near an all-time high, we expect the upside to be limited from the current level over the next few quarters until we get some evidence that operating and financial trends are rebounding.

GMS Earnings Recap

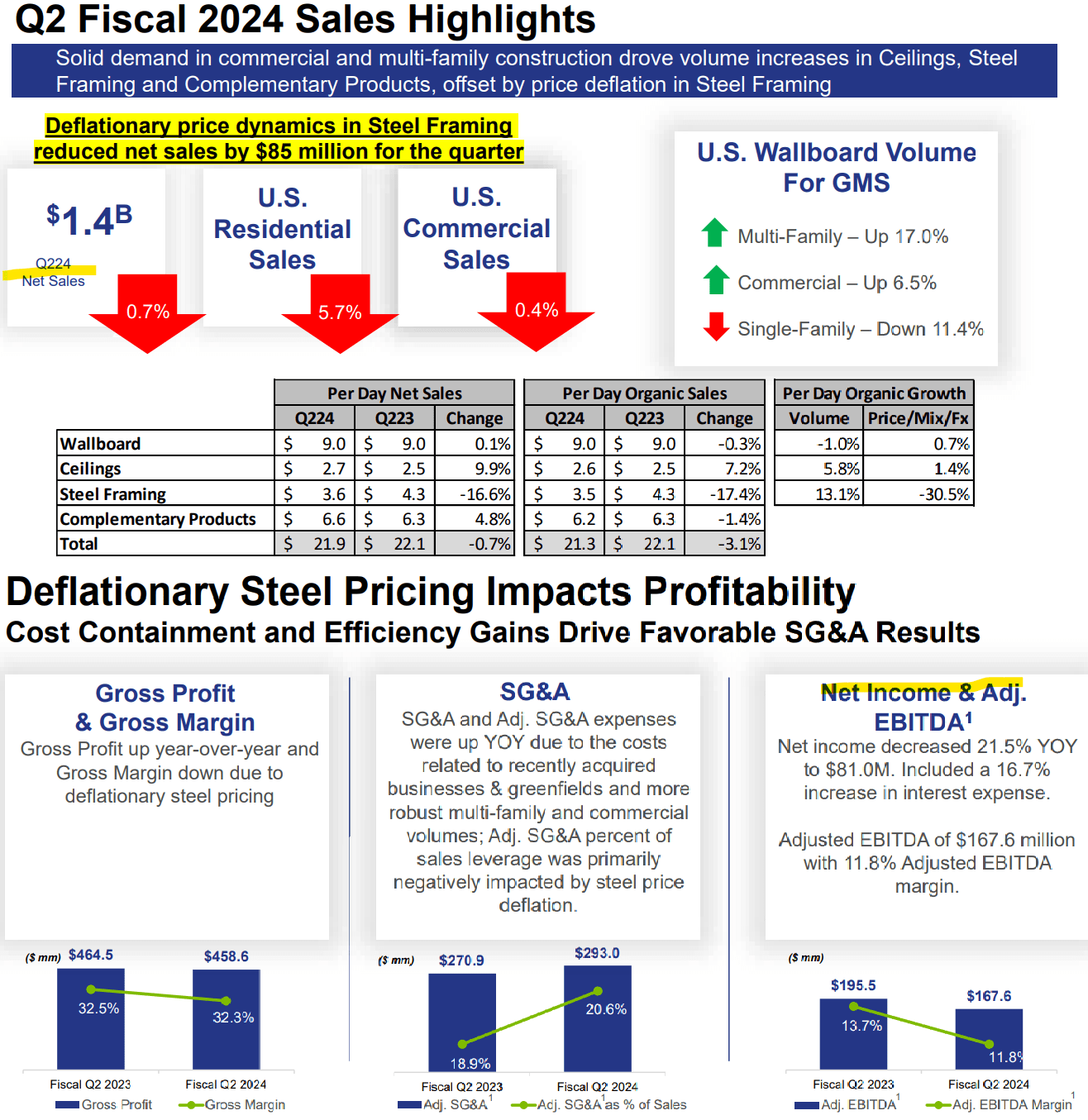

GMS fiscal 2024 Q2 non-GAAP EPS of $2.30, beat the consensus estimate by $0.04, although still down from $2.79 in the period last year. Revenue of $1.4 billion declined by -0.7% y/y but was also slightly ahead of estimates.

The context here considers a shifting sales mix and uneven levels of activity in key end markets. At a high level, the theme for the company is "solid demand" among multifamily construction and commercial markets, balancing weaker demand from single-family home construction particularly in wallboard.

In terms of organic volume growth, the core wallboard segment saw a -1% y/y decline balanced by higher pricing. Ceilings have been stronger with a 5.8% y/y volume gain alongside a 1.4% price increase.

On the other hand, steel framing is the one area of weakness where a -30.5% decline is related to deflationary dynamics at the commodity pricing level. This resulted in organic steel framing sales down by -17.4%, reducing the firm-wide net sales by $85 million, or nearly 700 basis points.

Putting it all together, the gross margin at 32.3% ticked lower by 20 basis points from last year, which combined with the top-line weakness, flowed through a -22% decline in net income. Adjusted EBITDA at $167.6 million is also down by -14.3% y/y.

{kind=link}

source: company IR

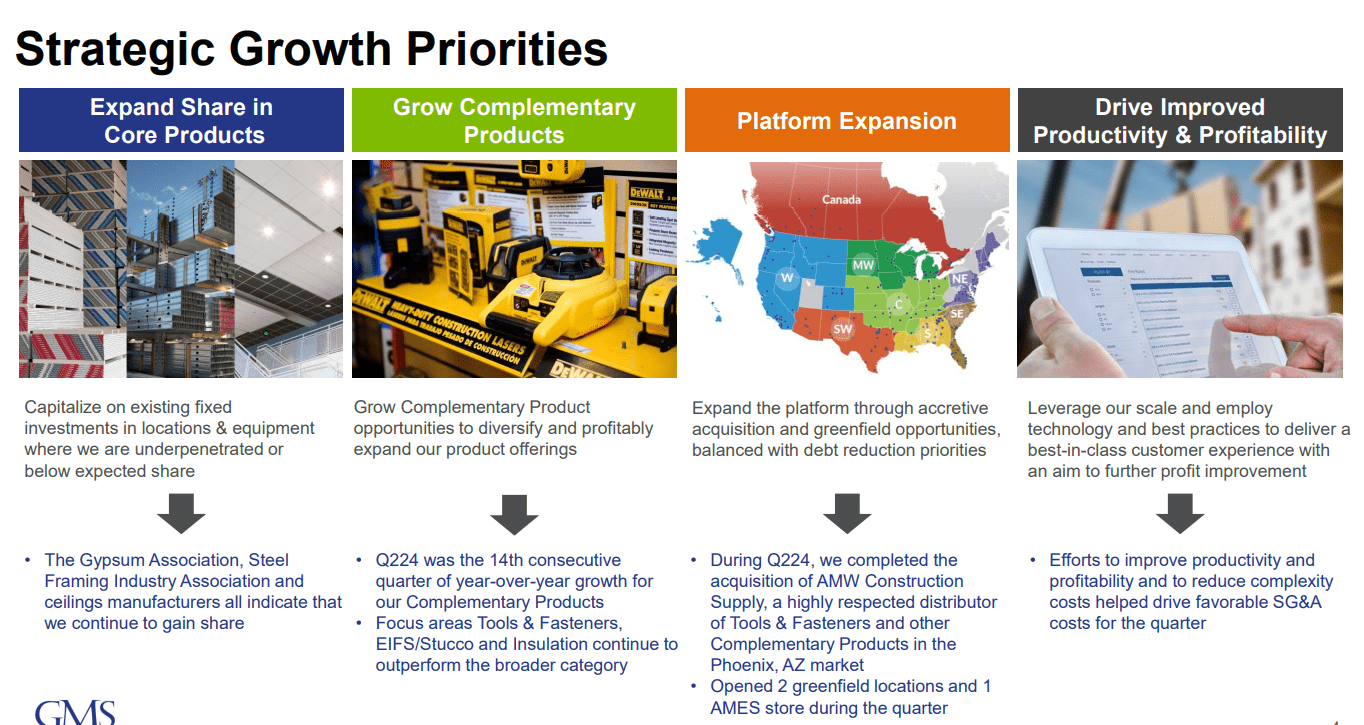

The takeaway here is that there are several moving parts with the steel framing pricing pressure overshadowing the marginally positive net sales gain from wallboard, ceiling, as well as complementary products. Acquisitions are a major strategy component of the business and recent deals have supported growth but also added to SG&A as a headwind on margins.

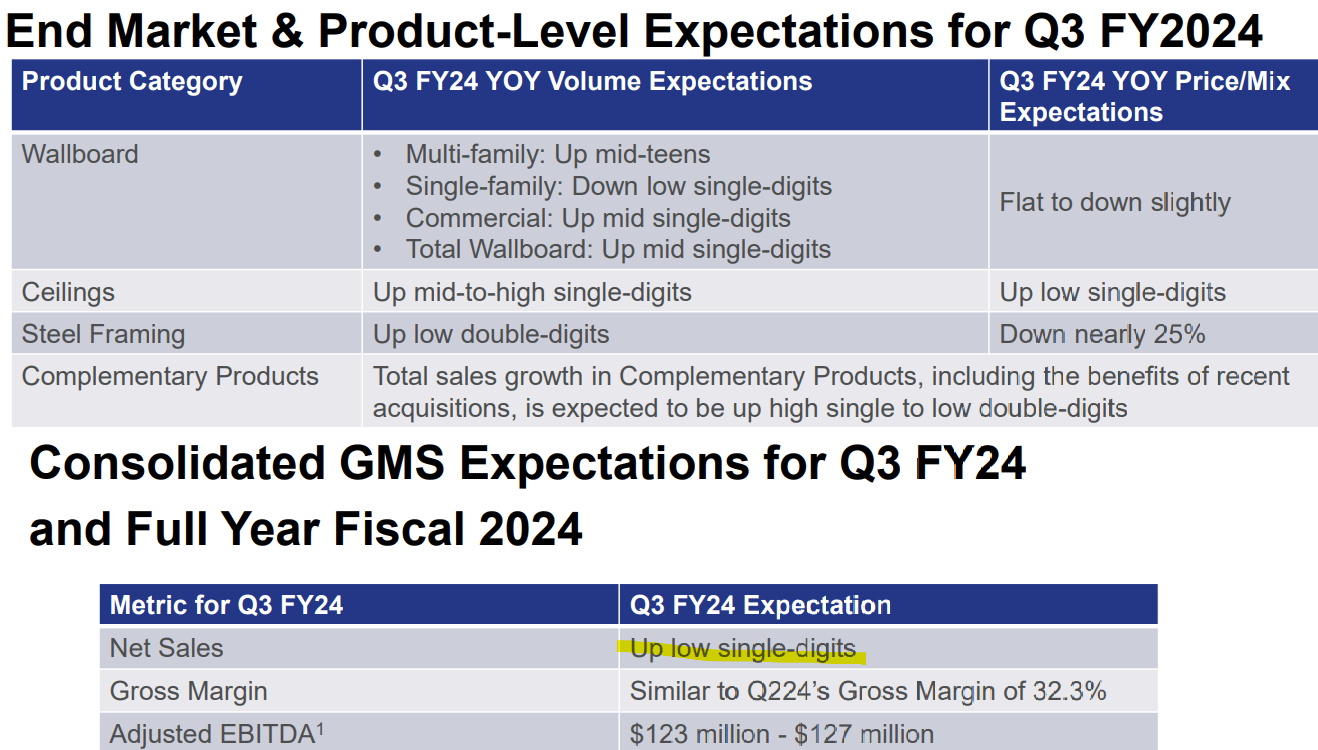

As for guidance, the company expects more of the same into the current quarter, with a target for net sales "up in the low single-digits". The forecast for adjusted EBITDA between $123 and $127 million, if confirmed at the midpoint, represents a decline of -11% from $140.8 million in the period last year.

Finally, we can mention that GMS maintains a solid balance sheet. The company ended the quarter with $77 million in cash on hand against total debt of $1.1 billion. Considering $636 million in adjusted EBITDA over the last twelve months, we view the net leverage of 1.5x as stable and a strong point in the company's investment profile.

{kind=link}

source: company IR

What's Next For GMS?

GMS has cyclical exposure, following trends in building construction and broader economic activity. The good news is that indications are that the U.S. remains on firm footing with GDP growth and even a new round of positive sentiment towards trends in 2024.

The idea here is that with room for interest rates to fall going forward as inflation trends lower, the setup should keep real estate including residential and commercial construction supported. While it's hard to see a strong rebound in this segment over the near term, a sense of stability points to at least room for steady growth on the volumes and sales side.

By this measure, indicators across new housing starts, building permits, consumer sentiment, and mortgage rates all play into the operating environment for GMS as monitoring points for the stock going forward.

In the long term, GMS highlights several growth initiatives, with a focus on consolidating its market share in core products. The company continues to expand across North America with an eye on targeted acquisitions, while also adding complementary products in categories like tools and fasteners that have synergies with the existing portfolio.

{kind=link}

source: company IR

While all that is positive, we can point out that the consensus outlook for the stock leaves a lot to be desired with forecasts for revenue growth averaging just 2% over the next two years while the EPS forecast into fiscal 2026 at $9.04 is below the record level from fiscal 2023 when GMS reached $9.29 in earnings per share.

{kind=link}

Seeking Alpha

So while this growth outlook is weak, the other side of the conversation is that shares appear at least reasonably priced, trading at a 9x forward P/E and just 0.5x sales.

Compared to a peer group of building materials stocks, GMS stands out as generally less profitable and generating lower margins compared to peers. This helps explain its discount compared to a group average P/E closer to 15x across names like Eagle Materials Inc ( EXP ), James Hardie Industries PLC ( JHX ), Simpson Manufacturing Co., Inc. ( SSD ), Masco Corp ( MAS ), and Builders FirstSource, Inc. ( BLDR ).

It's fair to say that GMS has some compelling "value" but the argument there is that it becomes more difficult to justify a convergence higher with a major expansion of the valuation multiples unless we get growth and earnings to rebound stronger.

{kind=link}

Seeking Alpha

Final Thoughts

We rate GMS as a hold, reflecting a neutral view on the stock price for the next 6 to 12 months. The company is fine fundamentally, but we're not seeing enough to take a convincingly bullish position, particularly following to big rally in shares just over the past month.

On the upside, stronger indications of construction activity between residential and commercial markets could provide some room for current estimates to outperform expectations. An uptick in steel framing prices would also provide a lift to sales trends in that segment. The risk to consider would be that economic conditions deteriorate, pressuring demand for building materials, which would likely drive sales lower.

For further details see:

GMS Stock: Mixed Q2 Results Keep Us On The Fence