GOF - GOF: An Unsustainable 16% Yielder

2023-12-07 06:45:55 ET

Summary

- Guggenheim Strategic Opportunities Fund focuses on providing high yield through exposure to private fixed-income securities.

- The Fund heavily favors fixed-income products over equities to match its objective of delivering high-yielding income.

- Currently, it provides a very attractive yield of 16%, which in the context of relatively acceptable performance since early 2022 when the Fed started to hike makes a sound investment case.

- The issue, however, is that almost two-thirds of the existing dividend is funded by the already paid-in capital, which, in turn, is subject to considerable credit risk and mark-to-market losses.

- GOF is also externally leveraged, which renders the dividend story more unsustainable as each incremental downturn would produce magnified consequences.

Guggenheim Strategic Opportunities Fund ( GOF ) is a closed-end fund, which puts a considerable focus on providing high yield to its investors through exposure to primarily private fixed-income securities.

Theoretically, GOF may invest without any limitations into fixed-income securities rated below investment grade. There are, however, some threshold levels set on international exposures and equities (up to 10% and 50%, respectively).

Guggenheim Investments

Despite the flexibility to invest in equities, it seems that GOF strongly prefers fixed-income products, which makes perfect sense in the context of the Fund's objective to deliver high-yielding streams of current income to its unitholders.

{kind=link}

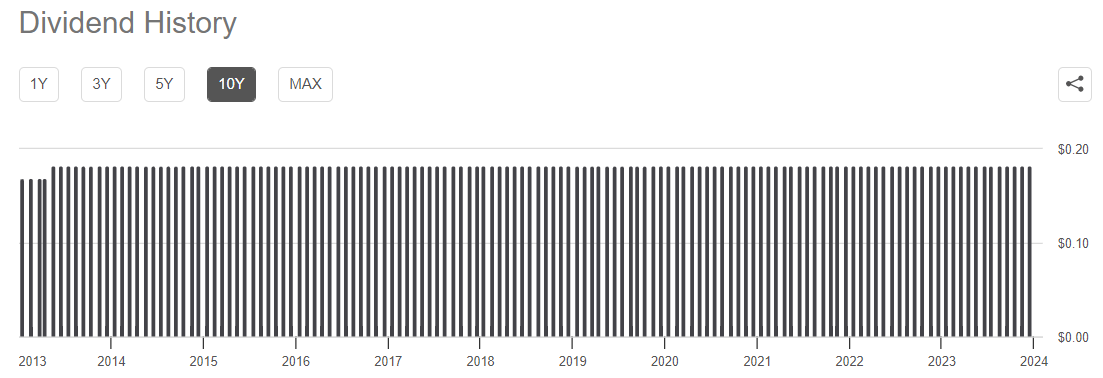

As we can see in the chart above, GOF has succeeded in accommodating the high-yielding dividend in a very stable and predictable fashion. So, it is in the best interest of GOF to concentrate the AuM in fixed-income securities as much as possible in order to match the characteristics of its asset base (i.e., cash flows) with the distribution profile.

Guggenheim Investments

If we peel back the onion a bit, we can clearly see that more than half of the exposure lies in credit, which is rated below investment grade level. Again, given that GOF is a closed-end fund with an objective to provide rather attractive dividend, it should not come as a surprise that there is a notable skew towards riskier segments of fixed-income securities. This way, the Fund can really utilize its active management strategy and find value in conjunction with sufficiently attractive yields.

In terms of diversification, GOF is well structured as the largest position constitutes ca. 1% of the total portfolio and there is a rather even distribution among the top segments of fixed income (i.e., high-yield bonds, bank loans, and asset-backed securities).

Finally, what is critical to factor in is the presence of additional leverage that GOF applies. Currently, ~22% of the total asset base is supported by external leverage, which helps elevate the inherent yield that stems from the fixed-income positions.

Thesis

Now, once we have established an understanding of GOF's key positions and allocations, let me explain why, in my opinion, investors should be very careful before deciding to go long on GOF.

{kind=link}

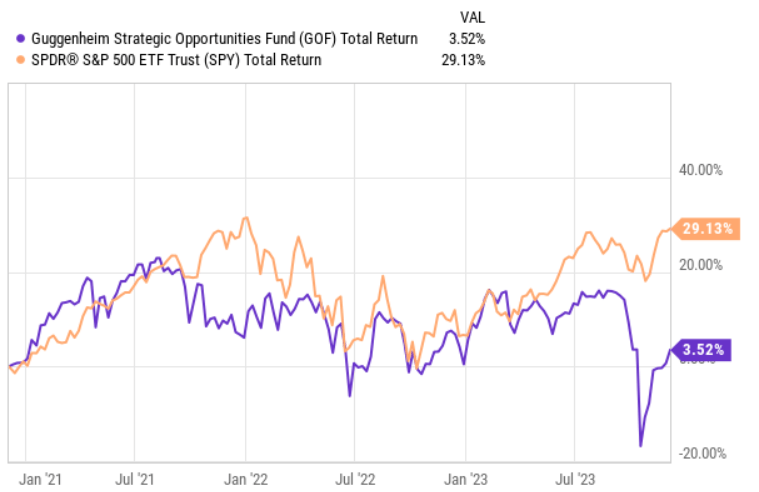

From the chart above we can see that GOF has delivered somewhat neutral results despite the surge in SOFR in early 2022. The fact that the delta in performance between GOF and the S&P 500 is so narrow and that GOF has achieved relatively flat results might seem impressive. Theoretically, there should be a more pronounced downside registered given how the overall credit has responded to higher interest rates and also considering the presence of external leverage, which per definition magnifies the rate of change in GOF's asset base.

In my view, there are a couple of reasons why GOF has navigated these headwinds so well:

- The high-yielding dividend serves as a floor as to how low the Fund's price could go until the demand from yield-chasing investors kicks in.

- Almost the entire GOF portfolio is located in private markets, where some parts do not get repriced in the same manner as the public securities, thereby relaxing some of the pressure on the NAV base.

- Bank loans, asset-backed securities, and private credit allocations tend to embody SOFR-based components, which greatly mitigates the duration risk.

Besides the third reason (which is relevant for only a part of GOF's portfolio), I do not find any meaningful argument that could justify why GOF has not lost more value in this high-interest rate environment.

With that being said, I could easily accept the argument that GOF is structured for dividend-seeking investors and the (potential) downside volatility in the NAV is not that crucial.

Nevertheless, if we analyse GOF's fundamentals a bit deeper, the dividend itself does not look too good.

First, the weighted average YTM (even with the extra leverage) that currently stems from GOF's securities is 10.69% , while the dividend level is 16.17%. This means that GOF has to fund the gap from paid-in capital or from direct divestitures of its portfolio.

Second, the most recent dividend (or distribution), which was made in November 2023, was only 37% funded by the generated income, while 63% of this distribution was backed by a return of the paid-in capital. And here we have to understand the following:

- The actual yield earned by investors is much less than what is reflected as the overall dividend yield of GOF (~5.9%). Most of the yield is just a return on investors' capital.

- To fund the latter part of dividend, GOF has to sell parts of its portfolio. Now, given that GOF's value (on paper) has greatly held against the pressures of higher interest rates, it is highly likely that by selling unlisted securities GOF will have to recognize losses, which at the end of the day should contribute to a more proper pricing (i.e., that is more in line with how high yield credit has responded, especially considering external leverage on top of that). In my opinion, the fact that GOF's premium over NAV is currently ~55% below the 52-week average premium is a direct testament to that.

Third, we have to be very cognizant of GOF's exposure to B and below-rated securities, which together comprise ~40% of the portfolio.

B rating per definition implies that there is a material risk of default risk with a very limited margin of safety remaining, where the case of any negative changes in the economy or business would most probably lead to a default. For CCC and below it is even worse.

Against the backdrop of looming recession risk, ~22% of additional leverage in GOF, and the pressure to continue divesting portfolio having so huge concentration in speculative risk category seems just too aggressive.

The bottom line

In my humble opinion, GOF will have to sooner or later cut its 16% yielding dividend to put away the pressure on divesting parts of its portfolio that entails a risk of recognizing losses and experiencing illiquidity discounts as the lion's share of portfolio is placed in private/unlisted securities.

Roughly 40% concentration in B and below rated credit instruments in conjunction with the presence of external leverage that inherently magnifies the risk (and return) seems rather speculative considering the prevailing macroeconomic backdrop and the reliance on paid-in capital.

For further details see:

GOF: An Unsustainable 16% Yielder