GOF - GOF: Credit Markets May Be Turning For The Worse

2023-03-20 11:52:37 ET

Summary

- GOF is a levered credit fund offered by Guggenheim Investments.

- The fund is paying an eye-watering 17.5% of NAV distribution.

- Trading at a 30% premium to NAV, investors risk 15% downside if the premium simply returns to the long-term average.

- I fear we may be starting to see cracks in the credit markets due to contagion risk from bank failures. This could cause significant mark-to-market losses on credit funds like GOF.

A few months ago, I wrote a cautious article on the Guggenheim Strategic Opportunities Fund ( GOF ), arguing that the fund was paying an unsustainably high distribution yield. Every month, the GOF fund pays a $0.1821 / share distribution, which yields an eye-popping 17.5% on current NAV of $12.47.

The timing of my article was poor, as the article was published near the October market lows, and GOF shares proceeded to rally ~5% in the subsequent 6 months. Combined with distributions, GOF delivered 12% total returns, outperforming the S&P 500's 6.1% returns (Figure 1).

Figure 1 - Prior article on GOF was poorly timed (Seeking Alpha)

While I concede that the market action in GOF shares was unexpected, I believe my criticism of GOF's distribution yield remains valid.

The biggest issue for GOF is that while its market price has rallied 5% since my article published, its fund returns have not kept pace with its distribution. In fact, its current NAV of $12.47 is 1.9% lower than the $12.71 NAV on September 26th 2022, confirming my fear the GOF fund does not 'earn' its distribution, and has to liquidate NAV to cover the shortfall.

Why Investors Should Avoid Amortizing NAV Funds

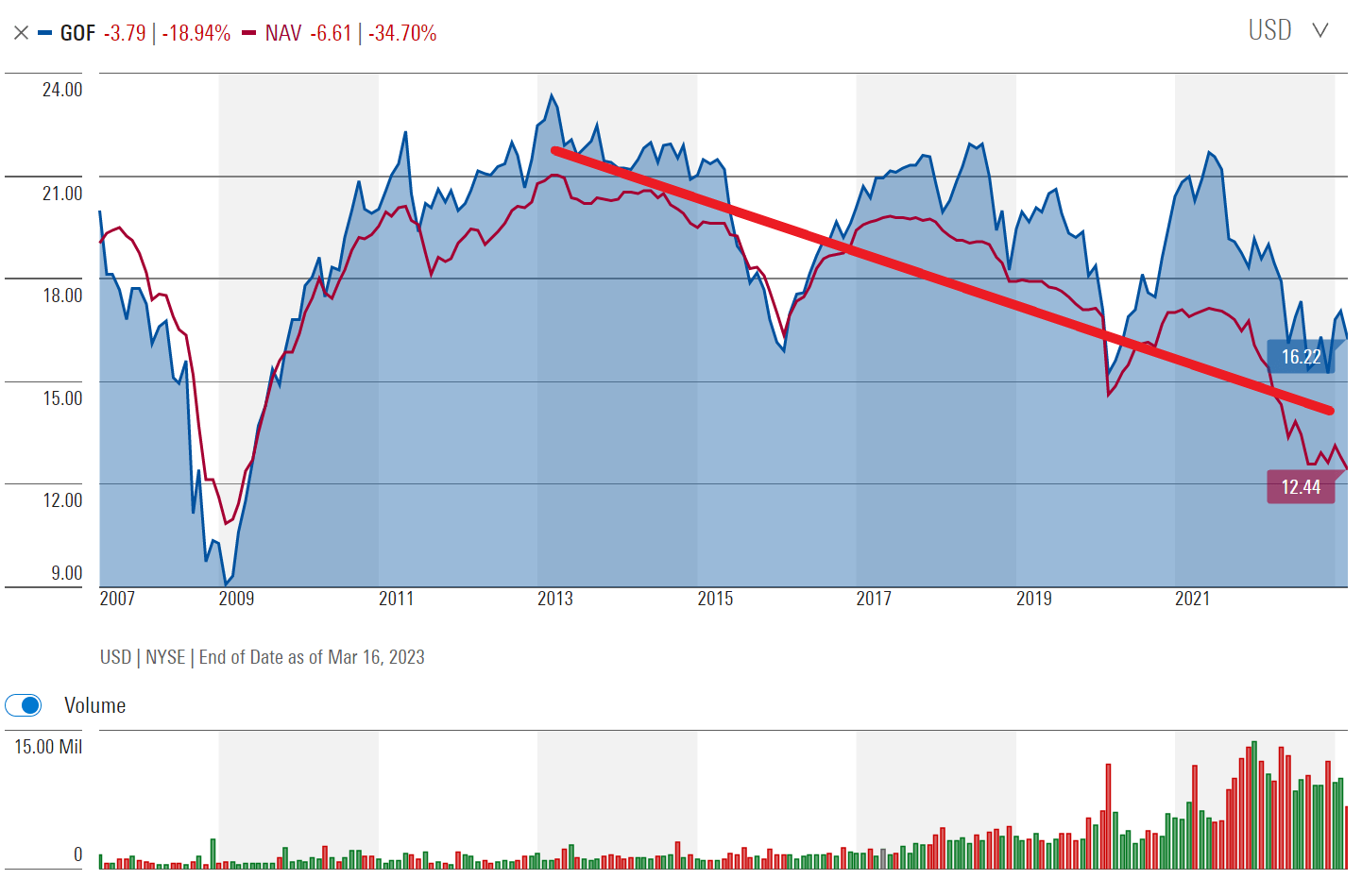

Funds that do not earn their distributions are called 'return of principal' funds and are characterized by long-term amortizing NAVs, as assets are liquidated to fund a high distribution rate. For example, figure 2 shows that GOF's NAV has amortized from over $21 a decade ago to roughly $12.50 today because it has continued to fund its too high distribution rate.

Figure 2 - GOF has a long-term declining NAV (morningstar.com)

{kind=link}

I often see readers comment that they do not care about NAV amortizations, because they do not plan on ever selling their holdings. As long as the funds continue to pay their generous distribution yields, these readers are happy to hold on 'forever'.

While 'return of principal' funds can continue to pay out their generous distributions for months, even years in the case of GOF, the proverbial can is simply being kicked down the road and can come back to bite investors in my view.

A simple analogy may better illustrate the problem with 'return of principal' funds. Imagine John Doe is a retiree living off a 5% savings rate on a $240,000 savings account balance, which translates into $1,000 a month in retirement income (i.e. GOF earns 5Yr average annual returns of 5.2%). Unfortunately, he has large monthly expenses of $3,500 (GOF currently pays a 17.5% of NAV distribution yield).

In any given month, the overspending does not look like a big issue, as John has ample savings to cover the difference. However, over long periods of time, John's savings will be depleted by the constant overspending. For example, after a year, his savings account balance will be ~$209,000 and his monthly income will have declined to ~$870. After 2 years, John's account balance will be ~$177,000 and his monthly income will have declined to ~$740. In our simple example, John would run out of money after about 8 years (Figure 3).

Figure 3 - Illustrative example of overspending (Author created)

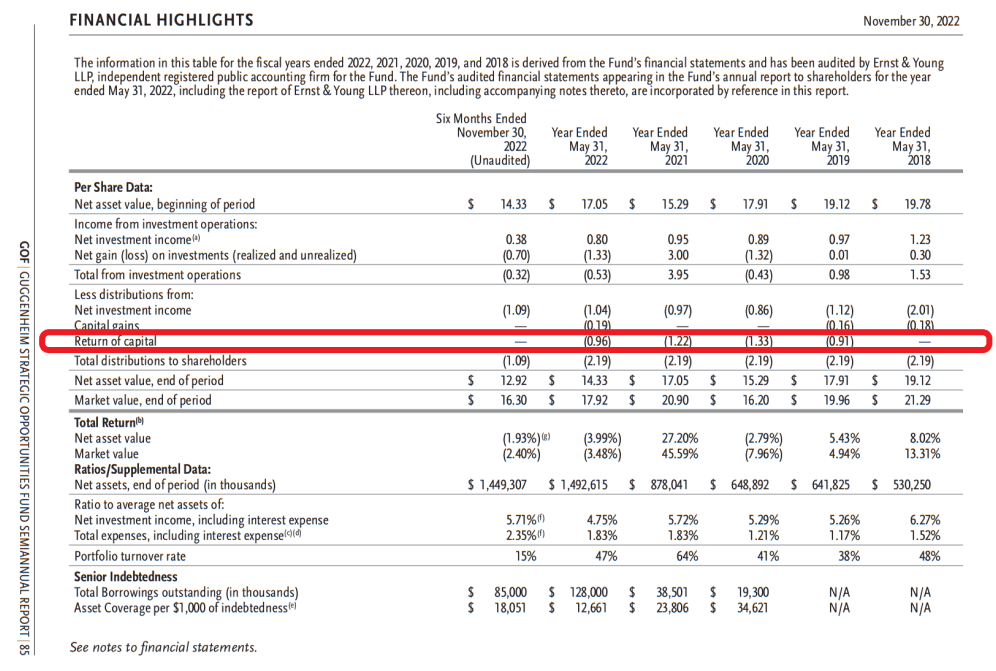

While the analogy above is simplistic, it does illustrate the real risk of an increasing portion of GOF's distribution being funded by returning investors' own principal to them through the distribution, as amortizing NAV depletes income earning assets. For example, in fiscal 2018, GOF was able to fund its distribution from net investment income ("NII") and capital gains, but 41.5% of fiscal 2019's distribution came from return of capital ("ROC") and 55.7% of fiscal 2021's distribution was from ROC (Figure ).

Figure 4 - Increasing proportion of GOF's distribution is funded by ROC (GOF 2022 annual report)

{kind=link}

What Happens At The End Of A Credit Cycle?

The other big issue with a 'return of principal' fund like GOF is that it has a serious NAV amortization problem during one of the longest economic expansion cycles in history, from roughly 2009 to the present (the COVID recession more of a blip, as the Fed quickly backstopped almost all markets with unlimited liquidity). What will happen when the economy inevitably turns towards contraction and credit events start occurring?

Unfortunately, I fear we may soon find out, as cracks are beginning to appear in the global banking systems with the failures of regional banks in the U.S. and the distress of Credit Suisse (CS).

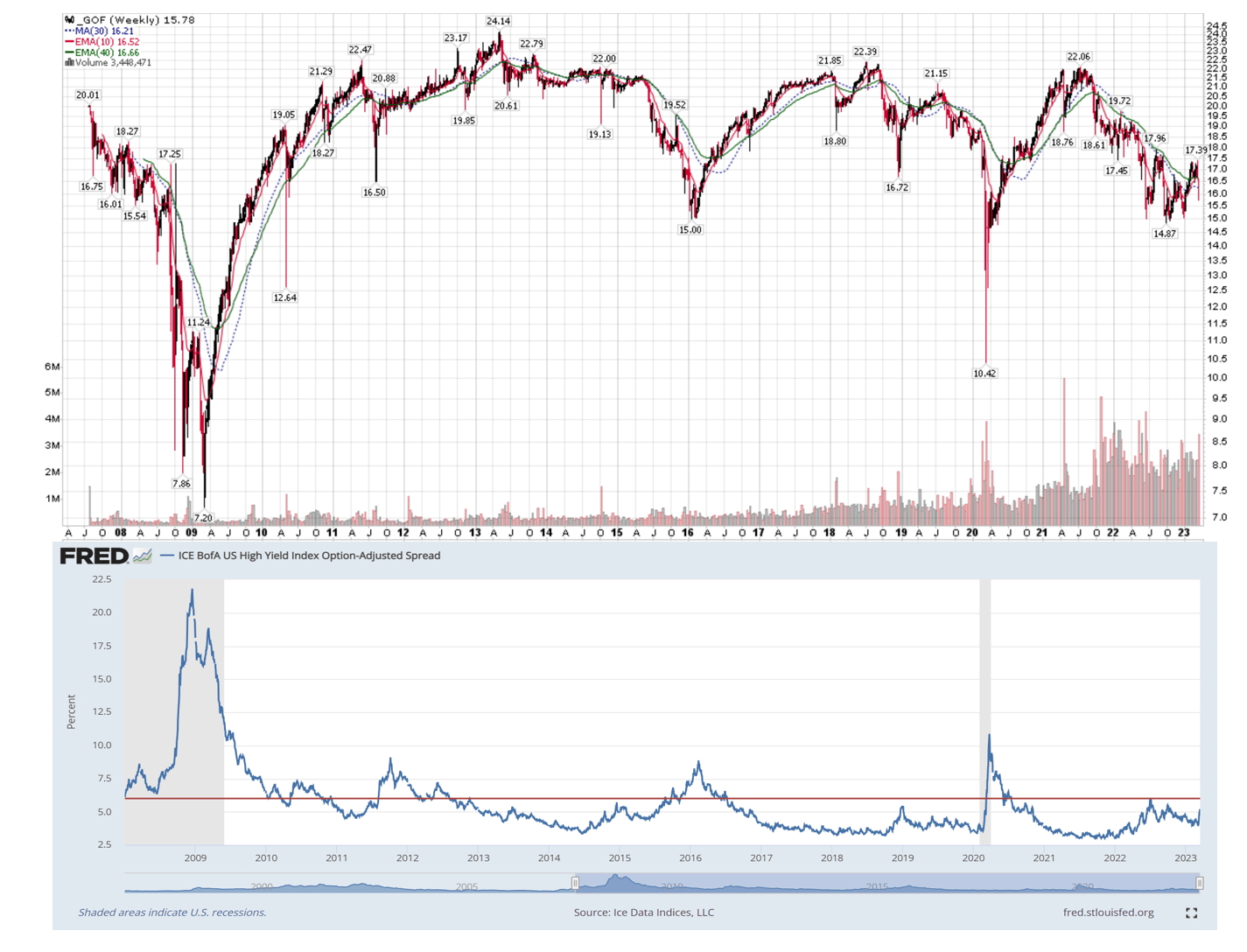

Although still relatively benign, high yield credit spreads have been widening rapidly in recent days due to the banking system fears mentioned above. Investors should watch fixed income markets closely in the coming weeks, as any additional weakness in the banking sector could cause contagion and spark a serious bout of economic weakness.

Historically, high yield spreads above 6% signaled serious economic risks that required some sort of central bank intervention to resolve (2008 Great Financial Crisis; 2010 and 2011 Euro crisis, 2015 global growth scare, 2020 COVID pandemic). We narrowly avoided entering this level of stress in 2022 and it appears credit markets may be trying to make another run towards it in 2023 (Figure 5).

Figure 5 - GOF NAV vs. high yield credit spreads (Author created with price chart from stockcharts.com and credit spreads from St. Louis Fed)

{kind=link}

For investors in levered credit funds like GOF, they need to understand that periods of credit stress can cause large mark-to-market losses. For example, in 2008/2009, the GOF fund had a 60%+ drawdown in its NAV. Even in a non-recessionary growth scares like in 2015, GOF's NAV suffered a 30% drawdown.

Investors Seem Oblivious To The Risks

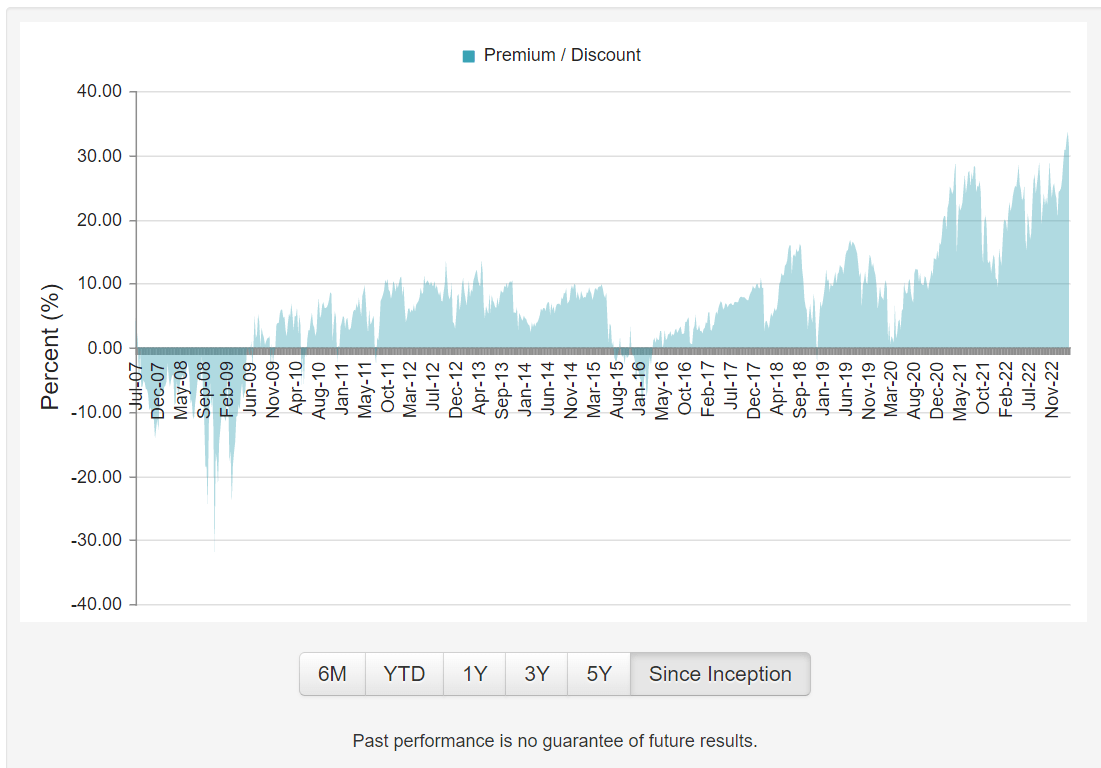

Interestingly, investors in GOF appear oblivious to the risks embedded in the fund. Since my article in September, GOF's NAV premium has expanded further, from 23% to an all-time high of 30%+ (Figure 6).

Figure 6 - GOF NAV premium has expanded to 30%+ (cefconnect.com)

{kind=link}

Even if my caution on the economy is unwarranted and GOF performs swimmingly well in the coming quarters, I fear this level of premium is unjustified and unsustainable. If GOF simply returns to its long-term average premium of ~10%, investors could be faced with a 15% loss in their investments.

Conclusion

Although investors continue to support the GOF fund, increasing its premium to NAV to 30%, I believe the risks to the fund have continued to increase. Not only is there a 15% price-risk if GOF returns to its long-term average premium to NAV, the 17.5% of NAV distribution rate also becomes increasingly unsustainable every month. Most importantly, I fear credit markets are turning right before our eyes and investors in levered credit funds like GOF may suffer material mark-to-market losses in the coming months.

For further details see:

GOF: Credit Markets May Be Turning For The Worse