GOF - GOF: Opportunity To Generate High Monthly Income

2023-12-13 00:26:11 ET

Summary

- Guggenheim Strategic Opportunities Fund focuses on generating high yields through fixed-income securities, with limited exposure to equities.

- GOF has a current dividend yield of over 16% and pays on a monthly basis.

- There are some concerns over the sustainability of the dividend.

- Lack of transparency in reporting makes this a tough recommendation despite its consistent track record of returns.

Overview

The Guggenheim Strategic Opportunities Fund ( GOF ) operates as a closed-end fund with a primary focus on generating high yields for investors through exposure to predominantly private fixed-income securities. While theoretically able to invest without limitations in fixed-income securities rated below investment grade, GOF has set threshold levels for international exposures (up to 10%) and equities (up to 50%).

Despite having the flexibility to invest in equities, GOF appears to strongly favor fixed-income products. This aligns with the fund's objective of delivering high-yielding current income streams to unitholders. The dividend history indicates that GOF has effectively maintained a stable and predictable high-yielding distribution. The current dividend yield sits at 16.22% and the distributions are paid out monthly. Something that has helped establish GOF's popularity is that they've never cut the distribution. They have been paying the same monthly distribution since 2013.

However, there are some downsides that I will discuss with GOF. For example, there is a lack of transparency in their reporting on levels of net investment income and Return on Capital ((ROC)). Despite this, the fund has managed to provide an average annual return of 10% since inception.

Guggenheim

Structure

{kind=link}

As you can see from the asset class breakdown, GOF is primarily a fixed income vehicle. One critical factor to consider is GOF's use of additional leverage, currently supporting around 22% of the total asset base. This external leverage enhances the fund's inherent yield from fixed-income positions.

Analyzing GOF's allocations, it becomes evident that more than half of its exposure lies in below-investment-grade credit. This riskier stance aligns with the fund's objective of providing an attractive dividend. The allocations help capitalize on active management strategies to find value with attractive yields. Despite the risk, GOF maintains a well-structured diversification, with only 1 position taking up more than 1% of its allocation.

In terms of taxes for 2022, the breakdown on the fund website reveals that about 43% of the distributions are characterized as Return of Capital for the entire year. This might be advantageous for investors holding GOF in taxable accounts, like myself.

{kind=link}

The distributions over the past year seem to be made up of approximately 37% Net Investment Income ((NII)) and 63% Return of Capital ((ROC)). I don't see management conducting a rights offering to raise capital or anything along those lines. This makes me believe that over time the distribution will need to be reduced because of the extended period of time where the distributions have been majority funded by ROC. I don't have a crystal ball or anything but paying a majority of your distribution out as ROC doesn't sit well with a lot of people for a few reasons. The term "Return Of Capital" can get a bit confusing and I see the definition often flipped around here on SA.

The definition as per Investopedia :

Return of capital occurs when an investor receives a portion of their original investment that is not considered income or capital gains from the investment. Note that a return of capital reduces an investor's adjusted cost basis . Once the stock's adjusted cost basis has been reduced to zero, any subsequent return will be taxable as a capital gain.

Return Of Capital

The source of confusion lies in the language used, particularly the statement that an "investor receives a portion of their original investment." Many investors interpret this as a return on their own money. While this interpretation seems logical, it really all depends on the fund.

ROC isn't always detrimental to a fund. Simply because a fund classifies some or all of its distribution as ROC doesn't imply that it didn't legitimately earn what it distributed. It's imperative to dissociate ROC from a fund's performance and recognize it as a tax classification. However, in the case of GOF, there is room for concern here with the ROC. After searching through many different sources, there seems to be a lack of transparency on this front. It's been difficult to try and determine exactly how much of NII. The latest report I was able to locate was a summary between 2017 and 2021 from the prospectus . I imagine this gave other authors some trouble as well because I failed to locate it amongst the other analyses here that I've recently published.

{kind=link}

I believe that the consistent levels of ROC are why we can see a shrinking NAV over time. Continuous reliance on ROC may lead to a decline in the fund's Net Asset Value. The tax implications of ROC can also be different, potentially resulting in higher capital gains taxes when shares are eventually sold.

Finally, a CEF consistently paying out a substantial portion as ROC may be perceived negatively by the market, with investors interpreting it as the fund returning its own capital rather than generating income through its investment activities. It is essential for investors to carefully consider the impact of ROC on their investment strategy, tax implications, and income expectations.

Risk Profile

{kind=link}

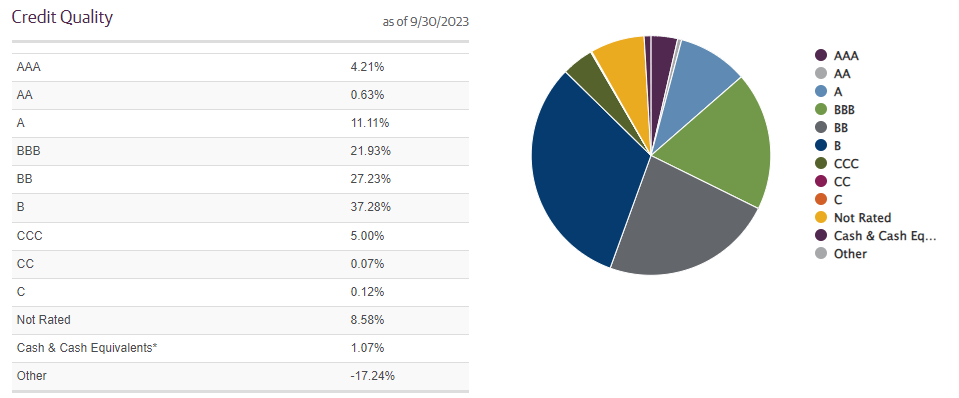

The credit quality breakdown of GOF provides valuable insights into the fund's risk profile and historical safety. The distribution across credit ratings reflects a diverse portfolio, which can be analyzed to assess the potential default risk associated with each category.

The majority of GOF's portfolio falls within the investment-grade spectrum, with ratings of AAA, AA, A, and BBB collectively constituting 37.88% of the total. Notably, AAA and AA-rated securities, representing 4.21% and 0.63% respectively, are considered the highest quality and historically exhibit low default rates. The next tier, comprising A and BBB-rated securities at 11.11% and 21.93% respectively, still falls within the investment-grade range. Historically, these ratings have demonstrated moderate default rates, but their inclusion in the portfolio indicates a balanced risk approach.

Moving into the high-yield space, BB-rated securities make up 27.23% of the portfolio. While these securities are considered below investment grade, or "junk", they have a historically low level of default. The largest proportion of GOF's portfolio, 37.28%, is in the B-rated category. These securities are at the lower end of the high-yield spectrum and come with a higher default risk compared to their higher-rated peers. However, the allocation makes sense as the objective here is to provide enhanced yields. Further down the credit spectrum, CCC-rated securities constitute 5.00% of the portfolio, reflecting a small exposure to highly speculative and distressed securities. The negligible percentages in CC and C ratings, at 0.07% and 0.12%, respectively.

The allocation to Not Rated securities, at 8.58%, introduces an element of uncertainty, as these instruments lack a formal credit rating. However, this allocation might include private placements or other non-rated securities that are subject to thorough due diligence.

{kind=link}

While a large portion of the credit falls within the "below investment-grade" ratings, I want to take a moment to emphasize how low the historical default rate is for a majority of the portfolio. The AAA, AA, A, and BBB ratings collectively make up 37.88% of the total portfolio and the default levels here are small. AAA-rated bonds have a 1.19% chance of defaulting over a 15-year time span. BBB-rated bonds have a 4.19% chance of default.

For reference , over the period from 2001 to 2022, the default rate for investment-grade corporate bonds was 0% in 14 out of 22 years. Even during the global financial crisis in 2008, considered one of the most challenging economic periods, the highest annual default rate for these bonds was merely 0.75%.

On the lower end of the spectrum, approximately 60% of the portfolio is allocated to below investment-grade bonds, rated BB - CCC.

BB: 7.02% chance of default over a 15-year period

B: 15% chance of default over a 15-year period

CCC: 34% chance of default over a 15-year period.

The only area here that concerns me is the CCC-rated portion of the portfolio but even then, the exposure that GOF has to that rating class is quite low at only 5%.

High Yield

As of the latest declared monthly dividend of $0.1821, the current yield sits at 16.2%. As previously mentioned, they've paid out the same monthly distribution for over a decade now. The high level of distributions helps fuel a solid history of total returns. You'd be looking at a 319% return since inception despite the price being relatively flat or down the entire time. I've been holding a small position size of GOF and collect $50 every month which is then reinvested to continue the income snowball.

Despite the lack of transparency, management has been able to maintain the distributions. I caution investors to start a position here without the proper due diligence. The income has been so reliably consistent that it seems the price continues to trade at a premium over NAV. It seems that investors are willing to pay the premium for reliability.

Valuation

Closed-end funds can trade at a discount to NAV primarily due to their market pricing mechanism. Investor sentiment, demand for the fund's shares, and the balance between buyers and sellers can lead to discounts. Market perceptions of management, the fund's strategy, and holdings' liquidity can also impact whether a CEF trades at a discount or premium to its NAV.

With this in mind, it is understandable as to why GOF consistently trades at a premium over its NAV. At the beginning of the year, we saw the premium peak at about 35% over NAV and the price has since come down. The current premium over the NAV sits at 10.68%. For reference, the average over the last 3 years has been a premium of 22.32% over NAV. This could signal slight undervaluation when compared to the average price relationship.

{kind=link}

Takeaway

In conclusion, the Guggenheim Strategic Opportunities Fund operates as a closed-end fund, primarily focusing on high yields through exposure to fixed-income securities. While GOF exhibits a consistent track record of delivering stable and predictable high-yielding distributions, there are concerns about the extensive reliance on Return of Capital ((ROC)) and a lack of transparency in reporting.

The fund's allocations, particularly in below-investment-grade credit, carry risks, but the historically low default rates in higher-rated segments provide a reassuring perspective. The premium trading over Net Asset Value reflects investor confidence, despite occasional fluctuations.

For further details see:

GOF: Opportunity To Generate High Monthly Income