GOF - GOF: Premium To NAV Reset But Fundamental Issue Remains

2023-11-07 21:04:10 ET

Summary

- Guggenheim Strategic Opportunities Fund has seen its premium to net asset value (NAV) collapse to zero, resulting in paper losses for recent investors.

- GOF historically delivers solid returns but it has a high distribution rate that is unsustainable, leading to a depletion of its NAV.

- The fund's immediate downside risk has been reduced with its premium to NAV reset, but if the distribution policy is not addressed, the premium could widen again in the future.

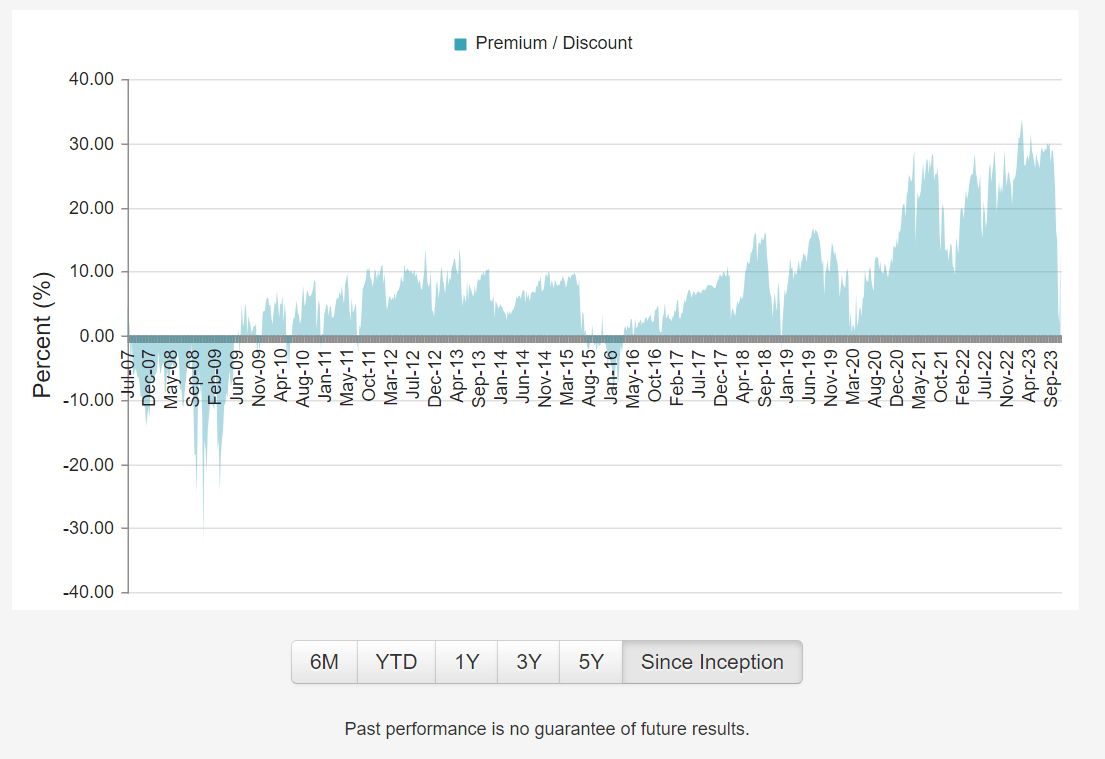

I have been warning for months on the elevated premium to net asset value ("NAV") of the Guggenheim Strategic Opportunities Fund ( GOF ). From my analysis, the GOF fund was paying a 17%+ distribution yield on NAV while only earning 5-8% average annual return, so GOF's NAV was being depleted every month to fund its distribution. In my last article, I noted that investors "appear oblivious to the risks embedded in the fund", with its premium to NAV expanding to over 30%. "If GOF simply returns to its long-term average premium of ~10%, investors could be faced with a 15% loss in their investments."

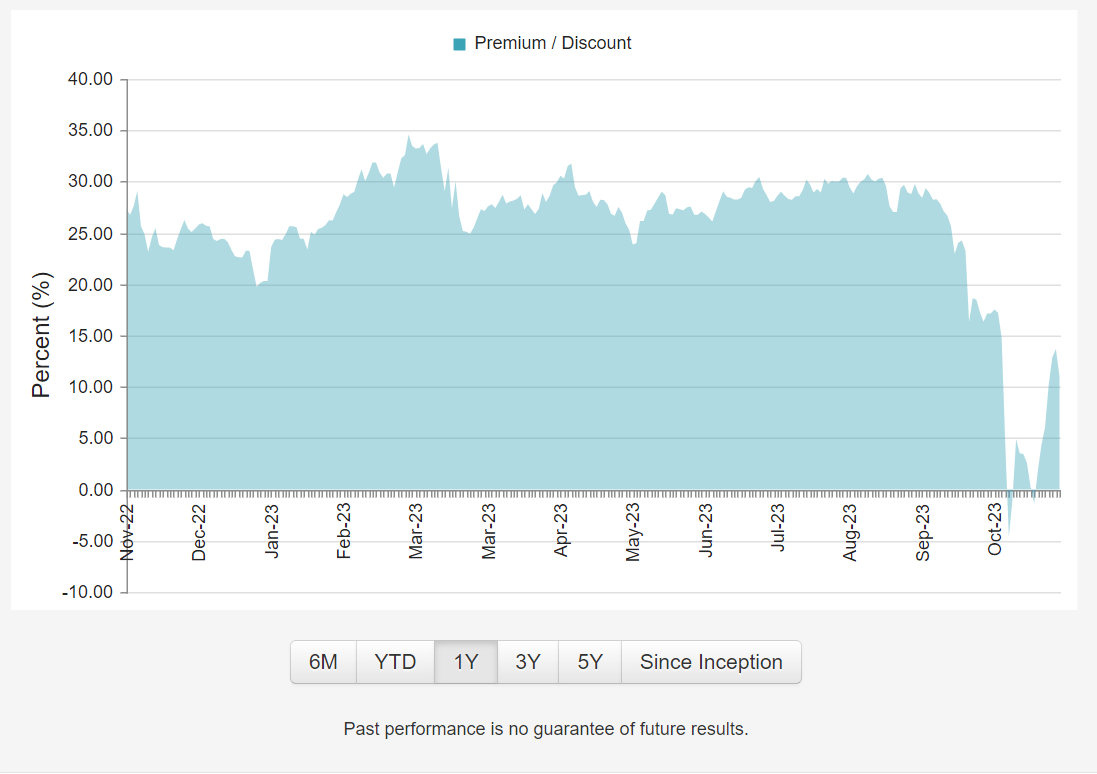

Unfortunately, that is exactly what happened as GOF's premium to NAV recently collapsed to zero in a span of a few weeks, leaving many recent investors with paper losses on their investment (Figure 1).

Figure 1 - GOF's premium to NAV recently collapsed to zero (cefconnect.com)

{kind=link}

With GOF's premium to NAV now more normalized at ~10%, is there still immediate downside to GOF's shares?

Brief Fund Overview

The Guggenheim Strategic Opportunities Fund is a closed-end fund ("CEF") focused primarily on generating income from bonds and other fixed income instruments.

The GOF fund was formerly lead managed by Scott Minerd , the charismatic Chief Investment Officer ("CIO") of Guggenheim Partners ("GPIM") who unfortunately passed away late last year. Since Mr. Minerd's passing, management duties on the GOF fund has been passed on to a team of portfolio managers led by Anne B. Walsh, the current CIO of GPIM.

The GOF fund has historically employed a range of strategies including investing in SPACs, high yield bonds, mortgage bonds, CLOs, and even selling covered calls on equities. So arguably, the GOF fund is an unconstrained hedge fund wrapped in a closed-end fund structure.

The GOF fund is one of the larger CEFs in the market with close to $2 billion in managed assets while charging a steep 2.88% expense ratio.

Solid Historical Returns...

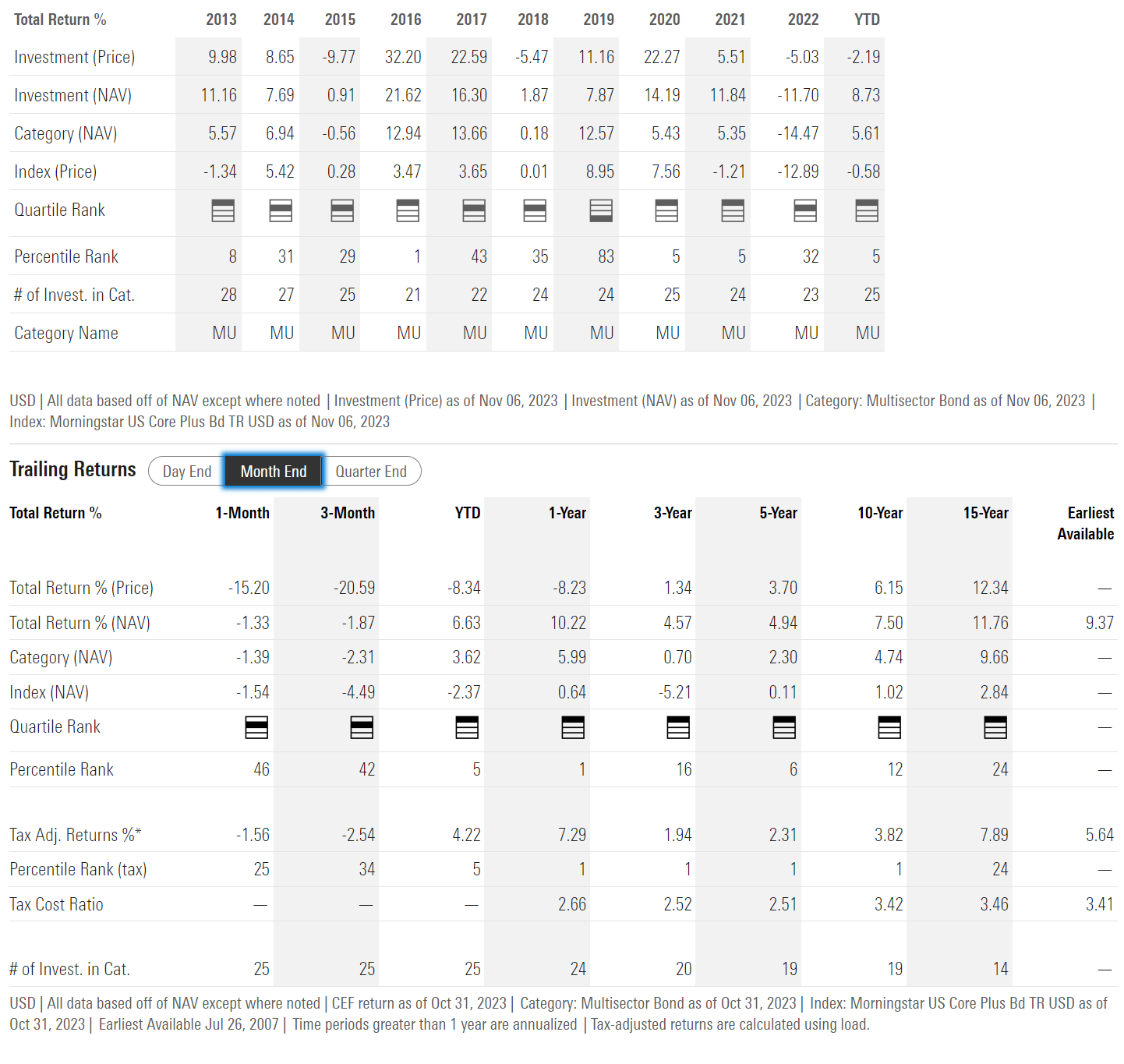

Historically, the GOF fund has delivered solid returns for a credit fund, with 3/5/10 year average annual returns of 4.6%/4.9%/7.5% respectively to October 31, 2023 (Figure 2).

Figure 2 - GOF historical returns (morningstar.com)

{kind=link}

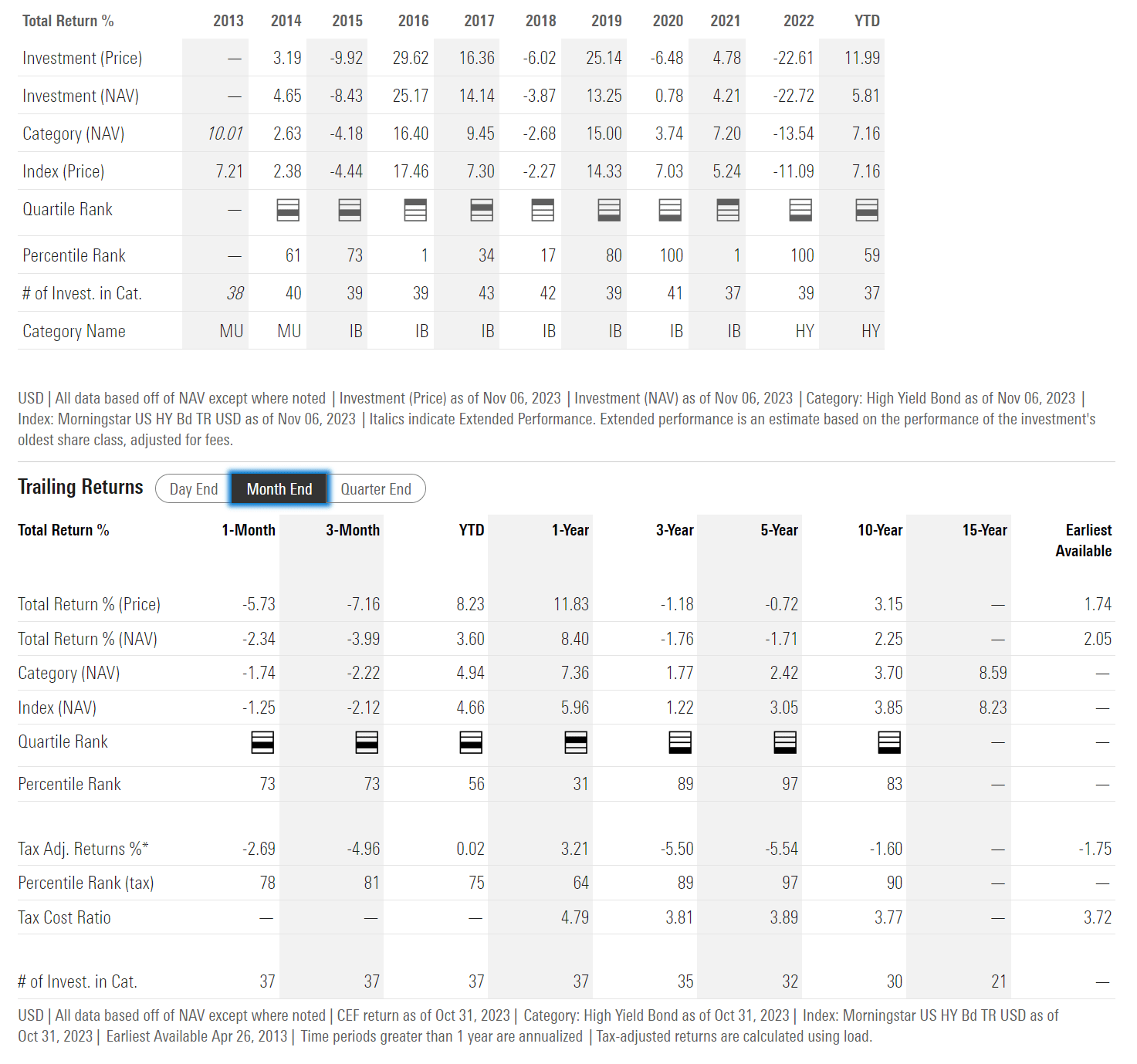

The GOF fund actually outperformed in 2022, as it only declined by 11.7%, in contrast to other levered credit funds managed by 'star' managers like the DoubleLine Income Solutions Fund ( DSL ) managed by Jeff Gundlach, which plunged by 22.7% in 2022 (Figure 3).

Figure 3 - DSL historical returns (morningstar.com)

{kind=link}

In fact, in terms of total returns, the GOF fund is ranked top quartile from 1 to 15 years, which is quite an achievement.

...Insufficient To Fund High Distribution Rate

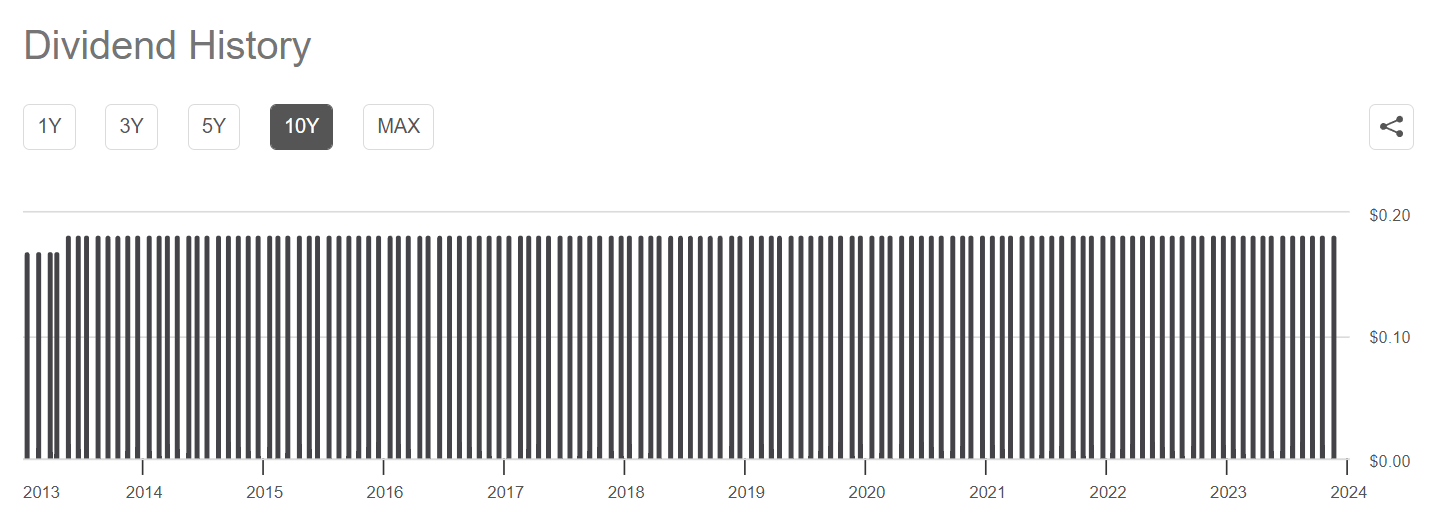

My issue with the GOF fund is its distribution rate, currently set at $0.1821 / month, which has been maintained since 2013 (Figure 4).

Figure 4 - GOF distribution has been maintained at constant rate since 2013 (Seeking Alpha)

{kind=link}

As a % of NAV, GOF's distribution is currently yielding 18.4%, which is more than double the fund's long-term earnings power.

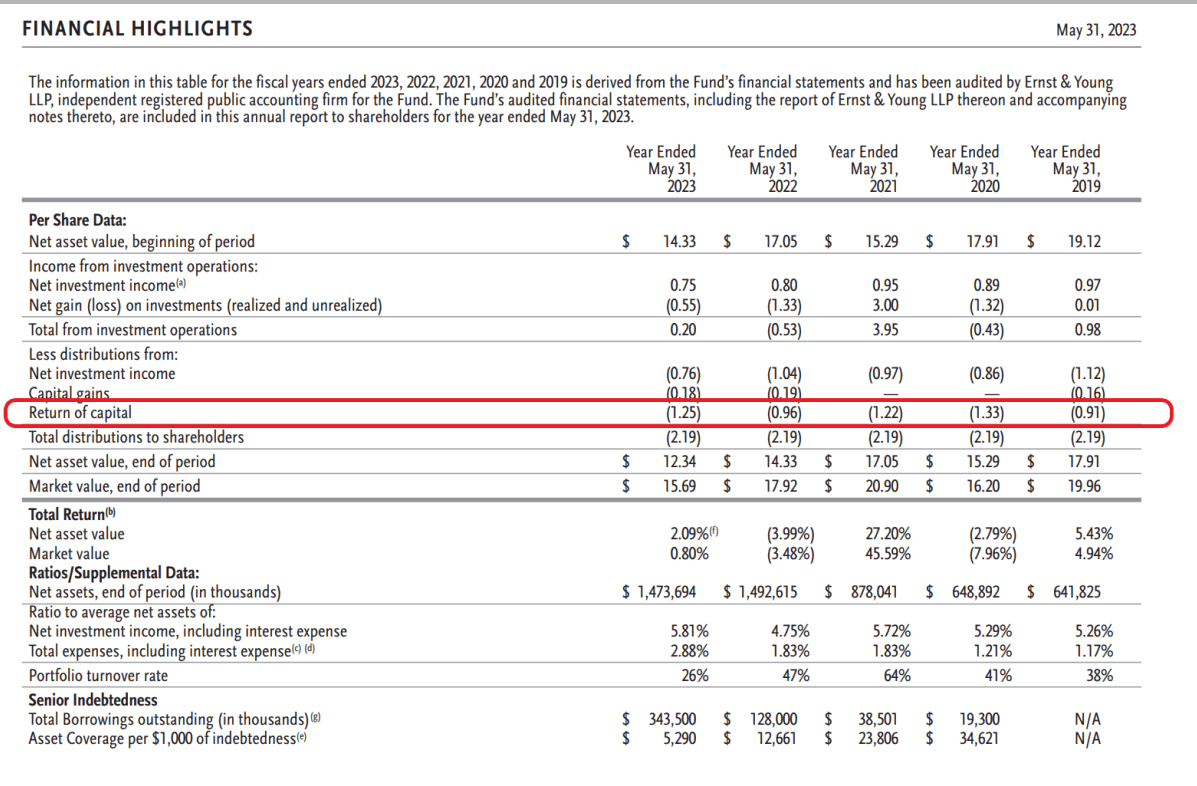

The GOF fund has been supplementing income shortfalls with return of capital ('ROC') in its distribution (Figure 5).

Figure 5 - GOF has been returning capital to shareholders (GOF annual report)

{kind=link}

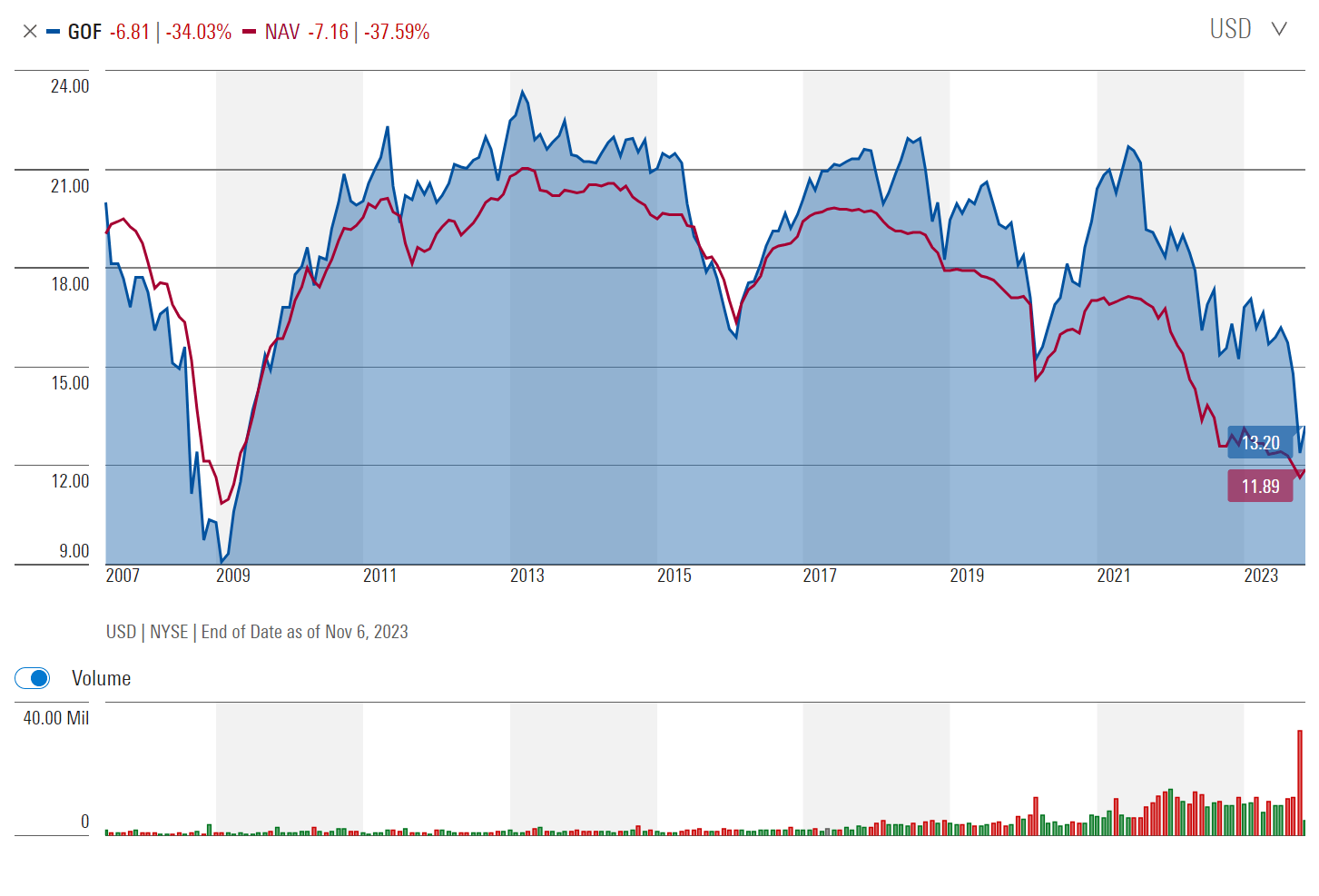

This has led to a gradual erosion of the fund's NAV, from over $21 / share in 2013 to less than $12 currently (Figure 6).

Figure 6 - Leading to an eroding NAV (morningstar.com)

{kind=link}

The problem with an amortizing NAV is that over time, a fund's market price tends to track its NAV. As we can see clearly in Figure 6 above, GOF's share price has declined from over $23 / share in 2013 to ~$13 share currently, mimicking the decline in NAV.

Look For Premium To Widen Again On Amortizing NAV

With GOF's premium to NAV reset to ~10%, roughly the long-term average, the GOF fund's immediate downside risk has been reduced (Figure 7).

Figure 7 - GOF long-term premium / discount to NAV (cefconnect.com)

{kind=link}

However, since the GOF fund has chosen to maintain its $0.1821 / month distribution rate, investors should expect the premium to NAV to mechanically widen in the coming months and quarters as it must sell assets to fund its distribution.

For context, even if we assume the GOF fund earns 8% per year, which is a respectable result for credit funds, the current 18.4% of NAV distribution rate means the fund must supplement its income shortfall by liquidating 10% of its NAV per year. As NAV shrinks, the amount it must supplement increases. So if nothing changes, in a year's time, GOF's premium to NAV will once again be over 20%.

GOF Should Cut Its Distribution

As an outsider, it is frustrating to see a clearly top quartile fund shooting itself in the foot with an idiotic distribution policy. While a reset of GOF's distribution to a lower rate will no doubt upset many long-term shareholders, it is in everybody's best interest that the GOF fund reset its distribution policy to a rate that is long-term sustainable.

Better yet, the GOF fund should convert to a managed distribution yield, for example, a trailing 7% annualized yield like the Royce Value Trust ( RVT ). This ensures investors receive an attractive distribution yield without suffering the potential principal loss from an amortizing NAV.

Conclusion

With the GOF fund's valuation reset to a ~10% premium to NAV, near-term downside for the GOF fund appears limited. However, investors are cautioned that if the fund does not address the fundamental issue of paying a higher yield than it earns, the premium will widen at an accelerating pace and we could see another sharp decline in a few quarters' time.

I would avoid the GOF fund until this distribution issue is addressed.

For further details see:

GOF: Premium To NAV Reset, But Fundamental Issue Remains