GOF - GOF: The Premium Has Come Down On Opportunistic Credit

2023-11-01 12:04:35 ET

Summary

- Guggenheim Strategic Opportunities Fund aims for an 18% current distribution rate by hedging against credit risk and utilizing leverage.

- GOF's portfolio is predominantly fixed income with a minimal equity allocation.

- The fund has historically traded at a 26% average premium, but is now at 4%, offering a potentially short window of opportunity.

Introduction

In an uncertain and bloody credit market, which is still wary of the Fed's direction, the best defense for many income investors is to very heavily screen their investments.

Using an opportunistic approach, hedging against credit risk, allocating to both alternatives and fixed income products, and applying leverage to enhance returns, the Guggenheim Strategic Opportunities Fund ( GOF ) has currently set its sights on a dazzling 18% current distribution rate doing just that.

Brief Overview

At a glance:

- Price : $12.14

- Distribution Rate :18.00%

- Premium/Discount : 4.30%

- Dividend Per Share : $2.0515

- Weighted Average Duration : 3.79yr

- Beta : 0.81

- Volatility (1Y) : 26.08%

- 30-Day Trading Volume : 17,568,595.24

- Market Cap : $1,885,986,860

Description: As per Guggenheim -

"[ GOF ] is a diversified, closed-end management investment company. The Fund’s investment objective is to maximize total return through a combination of current income and capital appreciation. The Fund pursues a relative value-based investment philosophy, which utilizes quantitative and qualitative analysis to seek to identify securities or spreads between securities that deviate from their perceived fair value and/or historical norms. The Fund’s sub-adviser seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies. The Fund’s investment philosophy is predicated upon the belief that thorough research and independent thought are rewarded with performance that has the potential to outperform benchmark indexes with both lower volatility and lower correlation of returns as compared to such benchmark indexes."

Figure 1, above, shows GOF's 10yr total return against High Yield US bonds ( HYG ), which is a comparable passive index of other high yield instruments. You can see the out performance in return, especially before this year, but it appears as though the managers have not lived up to their end of the bargain when it comes to volatility.

Figure 2, below, shows the levels of volatility expressed as standard deviation. We learn several things from this chart:

- The fund managers did not beat out on volatility. This partly has to do with the historical premium. More on that in its own section.

- GOF's overall volatility is an amplified version of high yield bonds', as they move mostly together. This is partly due to the leverage GOF takes on.

Portfolio

The fund managers have taken a value-based approach to portfolio construction, overweighting securities they believe are mispriced by the market. This is the "opportunistic lens" I mentioned earlier; the managers sort through the market and are not constrained to any sort of requirement on market weights or asset allocations.

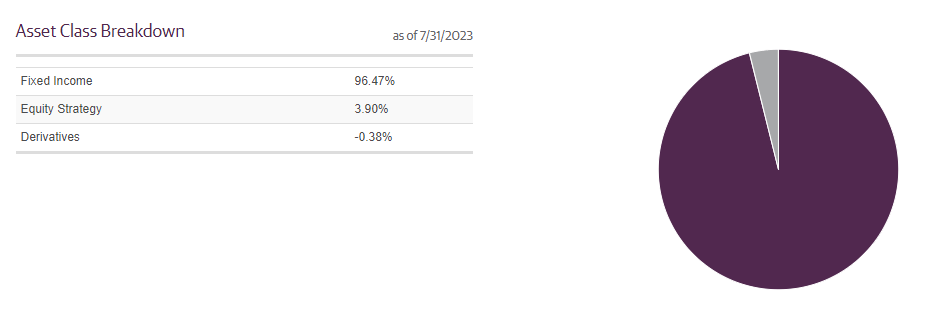

The fund is predominantly fixed income, and that is typical. The equity allocation almost never goes above 5%.

{kind=link}

{kind=link}

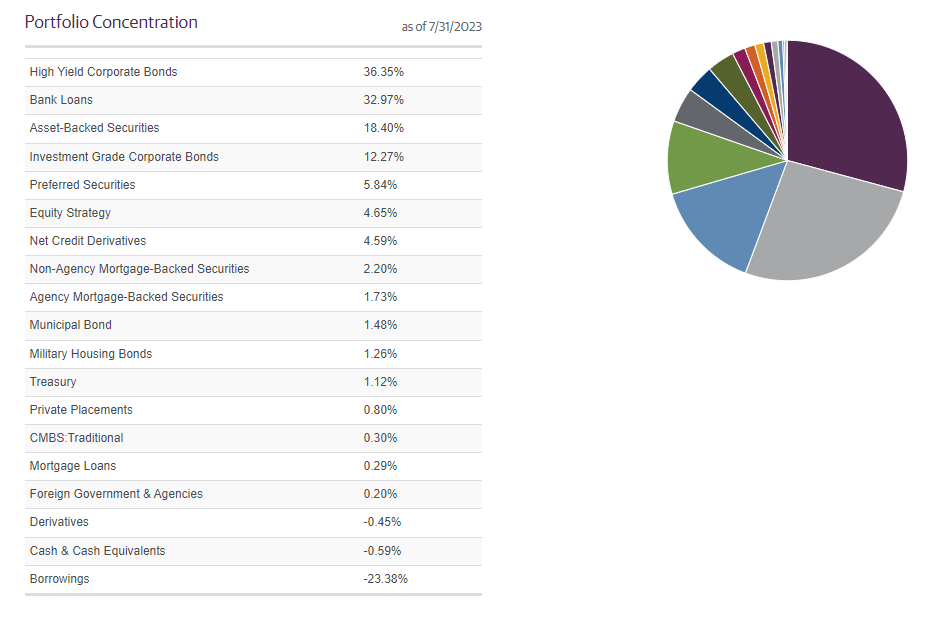

Note Figures 3 and 4 above show the breakdowns of these loans. The high concentration of high yield corporate debt and bank loans give us insight into the manager's views of credit in our current market:

- Bullish on quality corporate debt, overweighted

- Bearish on mortgages agency and non, underweighted

- Cautious of credit risk, signaled by their overweighting of asset backed securities and reluctance to venture into C and below-grade debt

- Bullish on senior bank loans, overweighted

I won't go into detail about bank loans here. Check out my article on DSU, a bank-loan CEF for more detailed information on the thesis behind senior bank loans.

These ABS positions are broken down into:

Figure 5 (Guggenheim Investments)

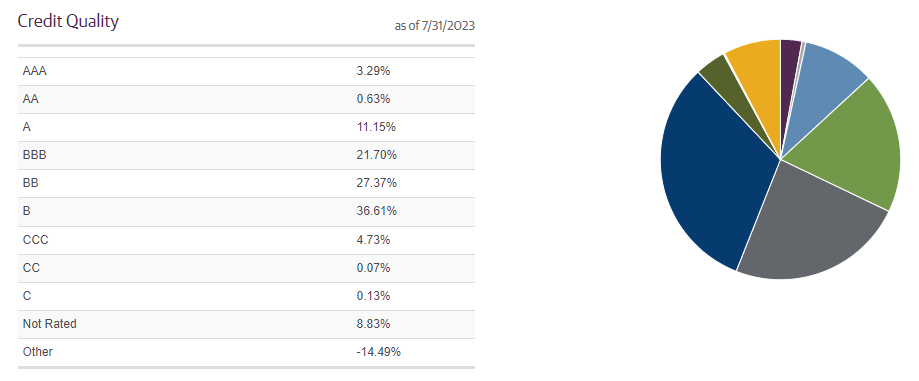

There is very little dabbling at the lowest end of the credit spectrum and less than 10% of the fund is not rated debt. Most of the debt is below investment grade, but still in the higher tiers of the BBB-B grades.

{kind=link}

Premiums & Discounts

One of the most distinguishing features of CEFs when compared to ETFs is how they trade at premiums and discounts. While both have the ability to have a current price different from the fund's NAV, CEFs tend to have lengthy and exacerbated premium and discount periods.

That steep decline in discount is what brought me to GOF. Initially, when I first saw this fund a few years ago, I scoffed at the insane premium. The average premium for the last 52-weeks is 26.07%!

Coming down so much closer to NAV has made this leveraged fund far more interesting. Note that it's rare for GOF to trend into discount territory, but it has happened. The last time there was any sustained discount was 2017, however.

Figure 8, below, shows this last month. Coming off of 22% premium, we've flirted with a discount several weeks ago, and now looking at a premium in-line with some mutual fund sales charges. This has become far, far more attractive of an investment at this point.

Allocation

GOF is a buy from me, but only for the aggressive investors who are looking for CEFs to help increase portfolio yield via leverage, which they should hold no more than 5-10% of their portfolio in a single CEF, or for the moderately risk-adverse investor who will allocate 2% or less of an income portfolio to this position.

The best use of this fund in an income portfolio is alongside other opportunistic strategies to get a variety of manager performance. I would pair this with other funds such as OPP or an ETF like CRDT .

Counterpoints

It is important to highlight the downsides to any fund that I do positive analysis for. Here are several of the potential issues investors may have with GOF.

-

CEF market prices have no guarantee of returning to NAV, and there is no guarantee that any premium, currently 4.30%, will not shrink or turn to a discount after the purchase of shares. The 52-wk average premium is 26.05% as shown in Figure 7.

-

Lower credit ratings present higher risk than investment grade bonds, and including leverage, GOF uses 29% leverage as of the time of writing; this may be above some income investor's risk tolerance and can lead to steep declines in periods of market turbulence (see above chart in 2020).

-

Floating interest rates create variability in payouts, which could pose a risk to investors requiring a more stable income stream. GOF's distributions have not always been consistent and could leave some investors lacking necessary income if a large rate cut happens.

-

The management fee comes out to 1.4% of net assets, requiring GOF to outperform the passive index by that amount just to break even. This is a risk as well and can potentially drag returns.

Conclusion

Closed-end fund GOF has come down from a multi-year, staggering premium. Today, it presents itself at a far more reasonable price that should offer investors far more downside protection than the fund historically has.

At an eye-watering 18% distribution rate, GOF is also tempting for its ability to juice up a portfolio's yield, but be wary of potential risks that may await CEF shareholders such as falling into discount territory again, or taking on too much risk with leverage and the increased beta it provides.

For further details see:

GOF: The Premium Has Come Down On Opportunistic Credit