HYG - GOF: Valuation Comes Down (Rating Upgrade)

2024-01-04 10:59:27 ET

Summary

- Guggenheim Strategic Opportunities Fund and Gabelli Utility Trust have struggled since our prior coverage.

- The GOF closed-end fund's valuation has improved but still lacks distribution coverage, making it susceptible to future losses but not enough to warrant a "Sell."

- A distribution cut for GOF is still an overhanging risk, but after the valuation deflation, the risk should be more muted.

Written by Nick Ackerman, co-produced by Stanford Chemist.

In September 2023 , I highlighted two closed-end funds, or CEFs, that seemed like they were ripe for a fall. They were the Guggenheim Strategic Opportunities Fund (GOF) and Gabelli Utility Trust (GUT). Both of these funds collapsed shortly after the posting, but admittedly, it was very fortunate timing. The overall market collapsed and hit correction territory about a month later, in October 2023.

Since then, the market has rallied back, but both of these funds have remained down quite considerably from the time of that prior publication. GUT remains at an egregious premium and continues to remain susceptible to generating massive losses for its shareholders.

On the other hand, GOF's valuation, after actually touching a discount, bounced significantly but still remains at a more normal premium than its historical level. I believe that warrants an upgrade from a "Sell" to a "Hold" rating. Still, the lack of distribution coverage has not and does not look set to remain solid, which means it is still susceptible to setting up for losses in the future from a distribution cut. At the very least, the amount of damage that would be done should be more muted now.

The original publication was first posted to our Investing Group members on September 26, 2023. Below is the performance of the funds since that article, and I've also included the SPDR® S&P 500 ETF Trust ( SPY ) and iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) for some context.

Ycharts

GOF and GUT didn't perform particularly badly or anything in terms of a total NAV return basis. However, since the funds were at shockingly high premiums, they seemed destined to underperform. I didn't think it would be so fast from the original publication, but again, the overall broader market also took a dive as risk-free rates hit highs not seen since the Global Financial Crisis. As soon as these rates receded as the Fed announced its pivot in November, everything came rushing back higher.

Today, the premium for GOF might still be uncomfortable for me given the precarious distribution coverage, but it is certainly more digestible relative to where it was previously. In fact, the premium is actually below the fund's since-inception average, but then again, if we took away the last few years, that average would naturally be much lower.

Ycharts

In that September article, we were looking at GOF at near all-time high premiums. Mix that with an unsustainable distribution, and we already saw what happened to several other funds in that situation in 2023; that was the main risk, in my opinion. The two examples we used for our prior article were this:

Here are two recent examples of funds that were paying out distributions that were way too high for far too long but were trading at elevated premiums: Brookfield Real Assets Income Fund ( RA ) and Duff & Phelps Utility and Infrastructure Fund ( DPG ). Upon announcing their overdue distribution cuts, the share prices were met with a brisk drop off a cliff.

Ycharts

A now more manageable premium relative to its historical level and unsustainable distribution means we aren't hit with a double-whammy. Instead, a distribution cut could lead to a much more muted response.

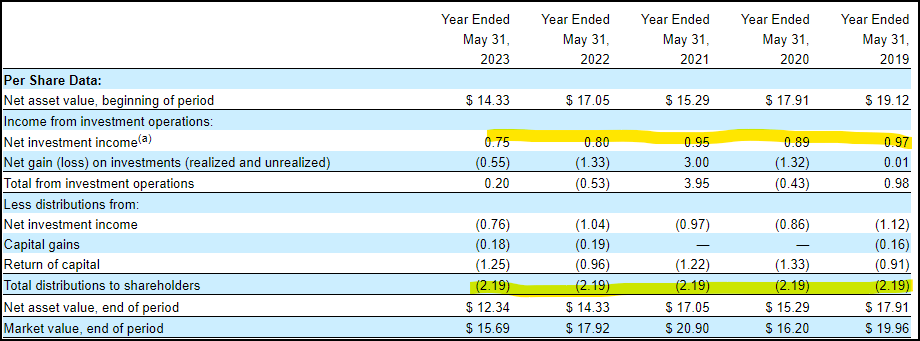

Of course, the fund has continued to pay out the same distribution since that article, too. We hadn't even received the distribution cut that I believe comes sometime in the future. The fund's NAV distribution rate is still pushing near 18%, so we need a considerable amount of recovery to occur, which would indicate potential capital gains that could be used for the distribution. As a mostly fixed-income fund, we would like to see net investment income cover the entire payout.

For that, we are still quite far away. Even if we went back to a zero rate environment, we would be looking at NII of something similar to $0.89 or $0.95, as we saw in 2020 and 2021. That would improve coverage, but not nearly enough, and the fund would still be susceptible to NAV erosion.

GOF Financial Highlights (Guggenheim (highlights from author))

{kind=link}

With rates receding, that did help push GOF's NAV higher, and we've seen somewhat of a recovery, as we would expect. The fund is also able to issue new shares through its DRIP and at-the-market offering, and when done at a premium that is accretive. That should further help limit the NAV erosion.

Still, even all along through the zero-rate environment we had prior to the Fed raising rates rapidly in 2022, the NAV trend is fairly clearly lower. We got those sharp recoveries in 2016 and after Covid.

Ycharts

Now, this latest rebound is likely to continue to recover some of the NAV. However, it is quite clear that in each event, the NAV never really got back to where it was previously. This is really why I believe that a distribution cut is still inevitable. It is never really a question of if but more a question of when. It could be next month, or they could put it off for many more years. They are kind of stuck in a situation where they can't escape. They know they are depleting the NAV, but if they do cut, they know that premium will all but be guaranteed to disappear. That would mean not being able to issue those new shares in an accretive manner.

Conclusion

GOF and GUT have taken a tumble since our prior update. However, GUT remains absurdly overvalued. GOF, on the other hand, has fallen enough to where I'd feel comfortable not seeing it as a "Sell." For an investor that was quick in October, I believe it was probably even a decent buy candidate for an ever-so-brief period when it touched a discount.

That said, I believe that the Guggenheim Strategic Opportunities Fund distribution is still unsustainable over the long term. That poses a risk to shareholders, albeit a significantly reduced risk at this time after the near all-time high premium popped.

For further details see:

GOF: Valuation Comes Down (Rating Upgrade)