VIASP - Going Against The Grain - Recent Additions To My Income Compounder Portfolio

2023-09-21 12:51:13 ET

Summary

- Retirement planning is crucial as thousands of people reach retirement age every day.

- The decumulation phase requires a shift in mindset towards generating sustainable income.

- I shares my method of holding high-yielding securities to continually grow the future income stream.

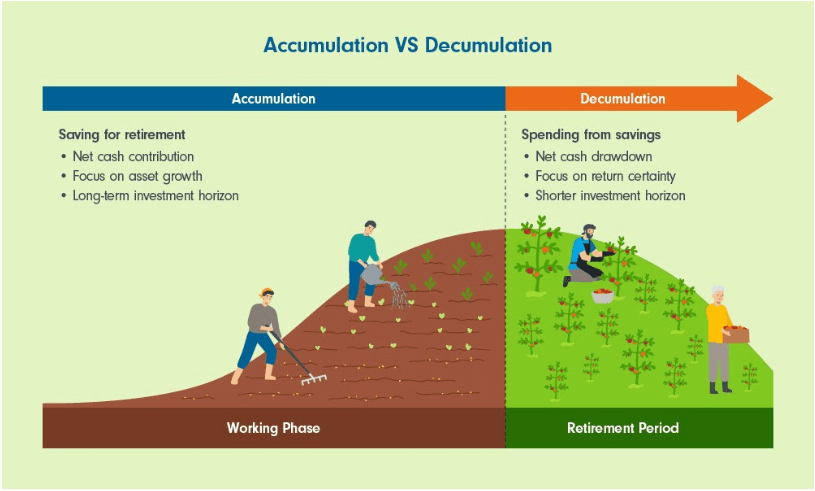

It seems like every day I read multiple articles about saving for retirement, or planning for a financial future in retirement, and how much money do you need to retire? If that sounds like an exaggeration (or perhaps due to my age, which is nearing 65, the “typical” retirement age in the US), consider the fact that about 10,000 Baby Boomers are expected to reach retirement age every day between now and 2030! If you are one of those and you have not yet saved enough to last you for the next 20 to 30 years of your life, you may be interested in a method to increase your future income so that you will have a long and satisfying life during the decumulation phase of your retirement years, as illustrated in this graphic from Fidelity.

{kind=link}

During their working years, most people save for retirement and work to accumulate wealth, and thus spend many years in the accumulation phase. But once you are retired and no longer have a steady income from employment, you begin to spend that accumulated wealth and need to ensure that your wealth will last you for a shorter period (most likely, unless you retire early), but one that is more uncertain. Instead of net cash contributions, you will likely be making net cash drawdowns of your savings, so that you can sustain the quality of life that you desire. As you go through the different stages of retirement , moving from accumulation to decumulation, you need to adjust your mindset as well.

“Today, given the prospect of a long retirement, you might still need a little growth in your portfolio,” Sadowsky said. “During the accumulation phase it’s about saving, but the decumulation phase is more about generating sustainable income. It’s a pivot to generating cash flow to avoid running out of money.”

One method that I have discovered is one that I call my Income Compounder, or IC portfolio, and it is modeled after the suggestions of other contributors on Seeking Alpha who I have followed over the years including Rida Morwa, Steven Bavaria, Nick Ackerman, and others. The basic idea behind my portfolio construction is to hold high yielding (generally 8-10% or higher) securities that offer regular monthly or quarterly dividends that I reinvest to continually grow my future income stream. I last published an update on my IC portfolio in June which you can read about here .

In my personal situation, I have been accumulating wealth in my employer’s 401k plan and in an IRA for the past 15 years or so (after recovering from bankruptcy in 2008). I also just recently retired, rolled over my 401k savings, and received a pension in the form of a monthly annuity and partial lump sum payout that I will also be investing into my IC portfolio. For now, I am still in the accumulation phase of building wealth but with the intention of having a passive supplemental income stream from my investments for future needs.

I also have other sources of regular income including Social Security, and an emergency fund with cash reserves currently earning about 5% interest. Once I begin taking cash out of my portfolio for living expenses at some point in the next few years, I will still reinvest my regular distributions but at less than 100%. Depending on how much income I wish to withdraw, I may reinvest only 75% of my distributions, for example, and take the remaining 25% as cash.

With that in mind, and understanding that I have a higher risk tolerance than most retirees or near retirees, I am willing to accept more risk to achieve a higher reward (i.e., higher yield) in the holdings that I invest in. And if the unrealized value of my investments drops because the underlying prices of my holdings drop, I am not overly concerned as long as the distributions continue to be paid at a reasonable yield based on my cost to acquire. I can also purchase more shares at lower cost to further increase my future income stream as I explained in a recent article that I wrote, XFLT: DRIP At A Discount To Stream Your Income Into A River Of Cash.

While the overall market appears to be looking for a direction over the past month, my income holdings continue to pay me to acquire more shares. I have also been doing some buying of new holdings that look appealing to me at current prices with the rollover funds that I recently added to my IC portfolio. In this article, I wanted to review several new holdings that I have added over the past few months. In addition to increasing my future income stream, I also have the goal of further diversifying my holdings to include some non-traditional assets or securities that may perform differently under current market environments (e.g., rising interest rates and inflation) than they might otherwise.

These suggestions are simply that, suggestions for further research and not necessarily recommendations for buying. Your risk tolerance and investment objectives may differ substantially from mine. My goal is to sustain and enhance future income, not necessarily total return in terms of growth in overall portfolio value, although that should occur anyway due to reinvesting.

Now, with all those caveats in mind, let’s proceed!

USOI

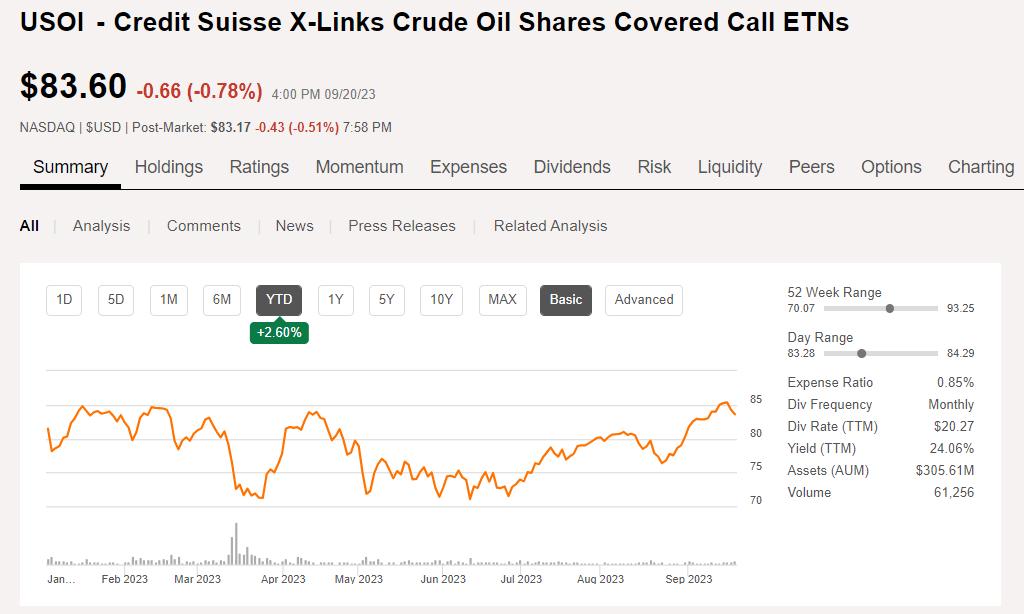

Back in June when oil prices appeared to be bottoming at around $70 and a few months after the collapse of Credit Suisse, I recognized an opportunity to purchase shares of Credit Suisse X-Links Crude Oil Shares Covered Call ETN (USOI). I made my first purchases in June for an initial position in the mid $70 range and then added a few more shares in the following weeks as the price dropped to the low $70s. The ETN has paid me 3 months cash dividends since I made my initial purchase and now trades for $83.60 as of 9/20/23 with a current TTM yield of about 27%. The distribution is variable so there is no guarantee that it will be that high going forward.

{kind=link}

With oil prices continuing to rise and inflation not yet fully contained, I expect to see a further increase in capital appreciation and no issues in paying the high yield distribution for the foreseeable future. Although the price of oil has retreated slightly in recent days, some still Goldman hikes Brent crude forecast to $100 but most of the rally 'behind us' $100 oil by 2024. The UBS takeover of the CS assets has been completed and no changes have been made to the ETN, so that helps to remove some of the fear and uncertainty around that situation. I am holding about a 5% position in this fund and do not plan to increase my holding unless oil prices dip below $80 again. I take the dividends paid each month in cash and look to reinvest that cash in whatever holding looks like it is on sale at the time.

VIASP

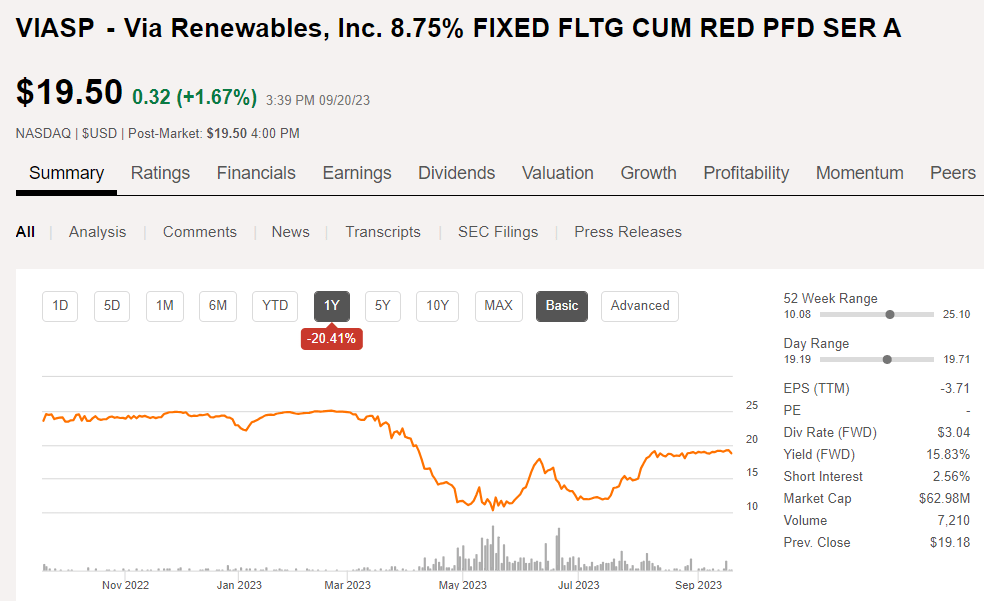

Back in May, I was alerted to a unique opportunity to take advantage of some market mispricing of the preferred shares ( VIASP ) of Via Renewables (VIA), thanks to an Via Renewables Preferred: Better Luck Expected In 2023 For This 26.5% Yielder (VIA) published by Richard Lejeune. Via had some unlucky events that hurt them in 2021 and 2022 and appeared to be poised to recover in 2023 due to their hedging strategy. At the time his article was published the share price of VIASP had been punished to as low as $11 with a par value of $25. I was able to purchase shares in multiple transactions for as low as $10.45 with a total cost basis of around $12. The yield on the shares at the time he wrote the article was above 26% when the shares were trading for around $11. Furthermore, the shares converted to floating rate after June and the quarterly dividend has since increased to $0.7592 per share as of July 20. The share price has also increased and now trades at $19.50.

I took some profits and trimmed a few shares and now hold a small position with a large unrealized gain and still look forward to a quarterly dividend yield that amounts to about 15.5% on an annual basis if the dividend remains the same. However, with interest rates set to potentially increase again, the amount of the dividend in future quarters may increase further. Meanwhile, the share price of VIA has stabilized. The company does not appear to be in any dire straits so the preferred shares should be safe for now.

{kind=link}

NXG

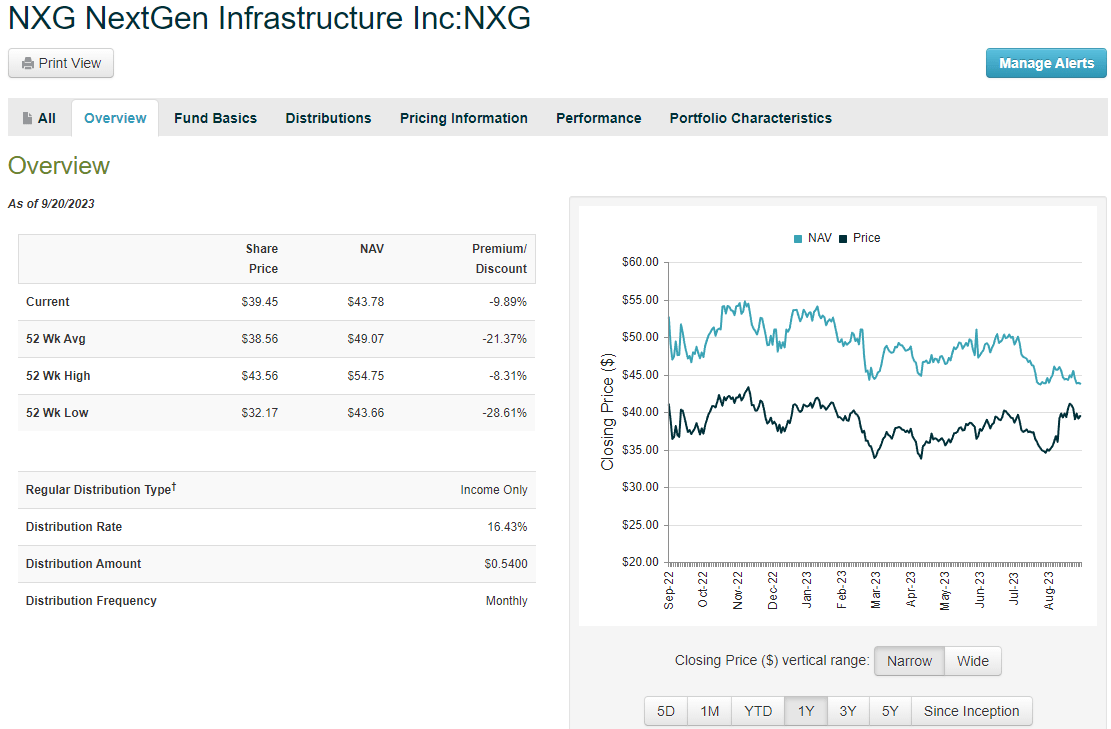

One of my favorite analysts on SA for identifying unique CEFs (closed end funds) that offer a high yield and special situations is Nick Ackerman. Because I follow Nick, I was alerted to a dividend raise by a fund from NXG Investments, the NXG NextGen Infrastructure Income fund (NXG). The fund managers did not just increase the distribution, they doubled it! In a similar vein to another fund from NXG that I previously covered , NXG Cushing Midstream Energy fund (SRV), NXG was trading at a substantial discount to NAV with a much lower yield that is suddenly very appealing for both the increased distribution and the potential to narrow the discount, which is exactly what happened with SRV.

At the time that Nick published the article on September 1, the dividend was raised from $0.27 per month to $0.54 per month, representing a forward yield of about 16.5% at the current market price. The price of the fund has moved up slightly in the couple of weeks since the increase was announced while the overall market has declined a bit. I began to build a position for around $39.50 and it currently makes up about 2% of my total income holdings. It is still too soon to determine whether it will have the desired effect of narrowing the discount but that appears to be the trend so far.

The monthly dividends are declared through November, so I plan to hold my shares at least until then and decide at that time whether to continue holding into next year. I expect that a significant amount of the increased distribution will be paid using ROC and that may not be sustainable for more than just a few months, depending on what happens with the underlying holdings.

Using CEFconnect, the chart shows the discount narrowing to just under -10% where over the past year the fund’s average discount has been closer to -21%.

{kind=link}

I am not as confident that NXG will be a good long-term investment like SRV has turned out to be, but the strategy worked well before, and if it helps to stabilize NAV then it could work with this fund, too.

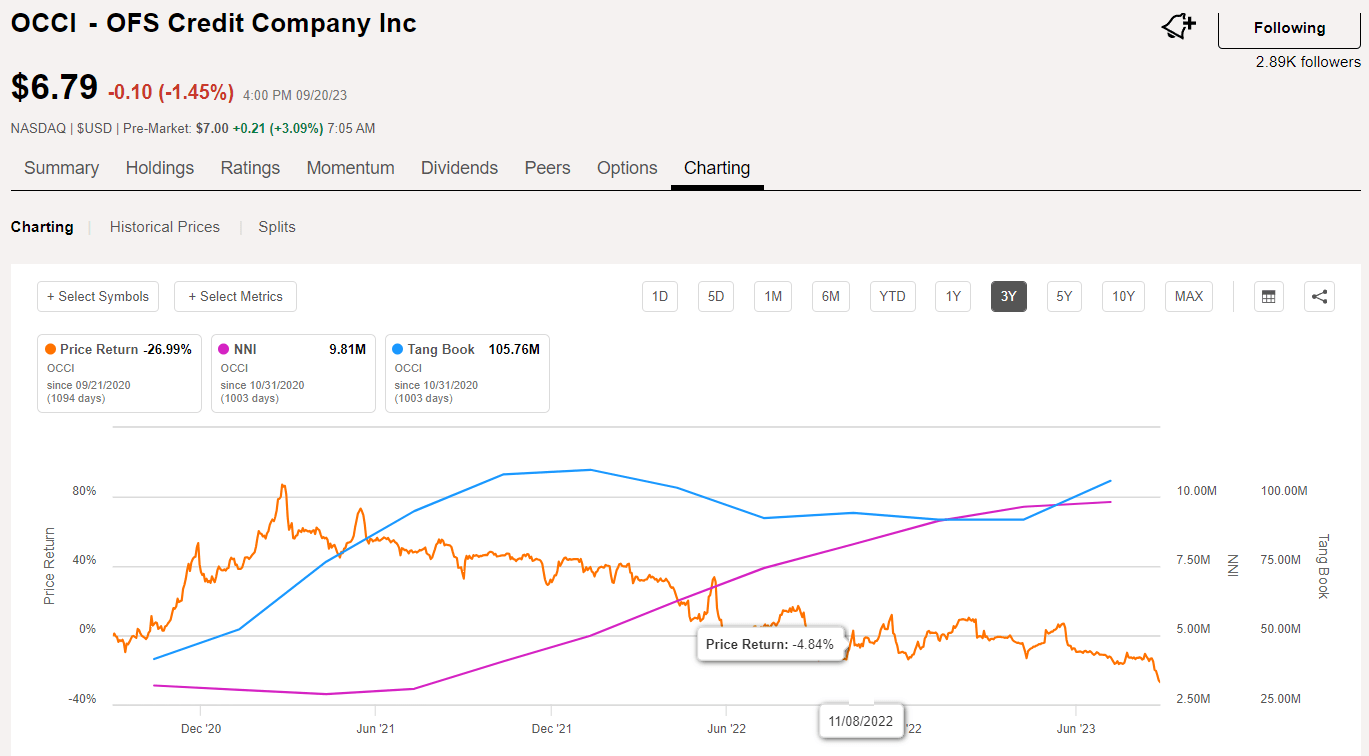

OCCI

One additional new holding in my IC portfolio is another non-traditional security, OFS Credit Company, Inc. (OCCI). OCCI is a CEF that holds mostly CLOs, primarily in the equity tranches and to a lesser extent the debt tranches of CLOs, which are essentially pooled portfolios of US senior secured loans. Although the market price of OCCI has been in a downward trend for most of the past 3 years, both the NAV and NII have been showing positive upward momentum, offering investors who are willing to reinvest shares an opportunity to generate high yield income.

{kind=link}

The reason why many investors are attracted to OCCI is because of the very high yield that it offers. Currently, the distribution is $0.55 per quarter, which works out to an annual yield of about 32%. However, the downside is that the distribution is limited to 20% cash in the overall distribution with the remainder issued in reinvested shares. What this means is that most investors who select the cash option will receive approximately 30% of the distribution in cash with about 70% issued as new shares. For those income investors who are not interested in accumulating more shares, this may be a deterrent. In my case, I like the idea of growing a position and eventually taking some of the cash if needed for living expenses while continuing to grow the accumulated shares.

The core NII reported of $0.59 on June 6 more than covered the $0.55 distribution for Q2. The NAV reported in July was estimated between $7.97 and $8.07. On September 1 the company declared another $0.55 quarterly distribution. Then on September 8, Q3 results were reported with core NII of $0.62 per common share as of July 31, again more than covering the declared distribution.

Core net investment income (“Core NII”) of $7.0 million, or $0.62 per common share, for the fiscal quarter ended July 31, 2023. Core NII increased $1.0 million, or $0.03 per common share, from the prior quarter. The increase in Core NII was primarily due to an increase in CLO equity issuers making their initial cash distribution payments.

On September 15, the latest NAV OFS Credit estimates NAV per share increased in August for August was released and came in at between $8.08 and $8.18, or about $0.11 higher than the previous month. At the same time, the market price dropped from a recent high of about $8 per share to under $7 as of September 20. This situation offers a unique opportunity to purchase mispriced shares at a discount in a CEF that offers a well-covered high yield distribution with the potential for some price appreciation.

Over the past year the price has fluctuated mostly in a range of between $7 to $9 per share. After hitting a 52-week low of $6.72 the market price is back up to $7 in pre-market trading today, September 21, and will likely resume its rise back up to $8 or more in the coming months. CLOs are in a sweet spot right now with the general US economy looking at a “soft landing” and as evidenced by the rise of new CLO funds as highlighted in this JBBB & CLOZ: Safer, Higher-Rated CLO Debt Paying In The Double-Digits (CLOZ) from Steven Bavaria earlier this year.

OCCI is not the “safest” investment in CLO funds and is probably not suitable for widows or orphans, but if you are willing to actively manage your investments, it may be suitable for a small holding in an income-oriented investment portfolio like mine.

Summary

Although I have now officially retired and am nearing the decumulation phase of retirement, I am still accumulating wealth in my investment portfolio and compounding my future income stream by reinvesting at lower prices to add more shares of high yield securities. I do not intend to withdraw any cash for living expenses for at least another 2 to 3 years and still have cash on the sidelines waiting for new opportunities to take advantage of. I am in a fortunate situation with my retirement and that is in large part due to my transition from growth investing to investing for income.

There is no need to “time the market” with this approach and no need to sell your core holdings in a downturn to raise cash. The cash is generated on a regular basis, monthly in many instances, and those regular distributions can be partially or wholly reinvested to continue to grow my future income stream for the day that I need that income for my living expenses.

For further details see:

Going Against The Grain - Recent Additions To My Income Compounder Portfolio