AZUL - Gol: Despite A Quant Top Pick I Remain Neutral

2023-07-12 15:21:49 ET

Summary

- While Gol Linhas Aéreas Inteligentes' shares have received a phenomenal quant rating, it's important to exercise caution and avoid getting too carried away.

- Gol underwent a significant debt restructuring in February, easing short-term cash pressures and leading to a rally of over 170% in its shares.

- Despite positive growth, Gol's high leverage and reliance on the domestic market could pose challenges, particularly in light of projected economic slowdowns.

The airline industry has successfully weathered one of the most severe crises in its history, brought about by the recent global pandemic.

Despite now under better circumstances, the Brazilian airline industry continues to face significant hurdles, including high debt levels, exchange rate fluctuations, and volatile oil prices. However, amidst these adversities, the resilience of companies like Gol Linhas Aéreas Inteligentes ( GOL ) in sustaining operations amidst a substantial decline in demand and limited financial resources without relying on government aid is truly commendable.

And the market appreciated it so much that shares of Gol jumped an incredible 117% since March this year following topline growth and reduced liquidity risk in the short term.

Considering the significant reliance of Gol's revenues on domestic economic growth, the current short-term macro perspective hinders me from adopting a more optimistic outlook.

Short-term liquidity risk reduced, and a quant top pick.

In February this year, Gol announced a significant debt restructuring, which allowed the company to ease short-term cash pressures. More importantly, the deal also corroborated the position of Grupo Abra, which became the company's controlling shareholder, in one of the largest private debt restructurings in Latin America, totaling US$1.4 billion.

Grupo Abra's investment was made through senior secured notes due 2028 and also senior secured notes to be guaranteed by Smiles - Gol's loyalty program company - valued at US$3.7 billion. According to the company's statement, the Abra Group has agreed to invest $400 million in Gol and receive the bonds due in 2028. After the closing, Abra will be GOL's largest creditor.

The deal made Gol shares fly high (pardon the pun), engaging a rally of over 170% to its peak in early July.

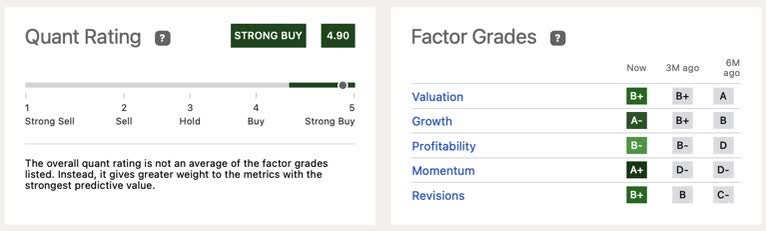

It is no wonder that Gol came to be among the top stocks overall because of its Quant rating on the Seeking Alpha platform as a "strong buy," driven mainly by an A+ momentum and an A- growth potential.

{kind=link}

Seeking Alpha

According to growth estimates , Gol has estimated forward revenue growth of 43%, currently about 420% above its industry peers and 340% above the company's historical average revenue growth over the past five years.

Forward operating cash flow growth at 82% versus an industry average of 16.4% also looks appealing, a 353% hike compared to Gol's historical average over the past five years.

However, the analyst consensus for revenue growth this year stands at 31% compared to last year, which guarantees a forward price-to-sales ratio of 0.26 - about 80% below the industry average.

But it's not all blue skies.

Although Gol's shares have already yielded excellent returns for its shareholders this year, the current valuation, while necessarily stretched, leaves room for an interpretation of being unattractive, especially compared to some of its main peers and Gol's historical performance.

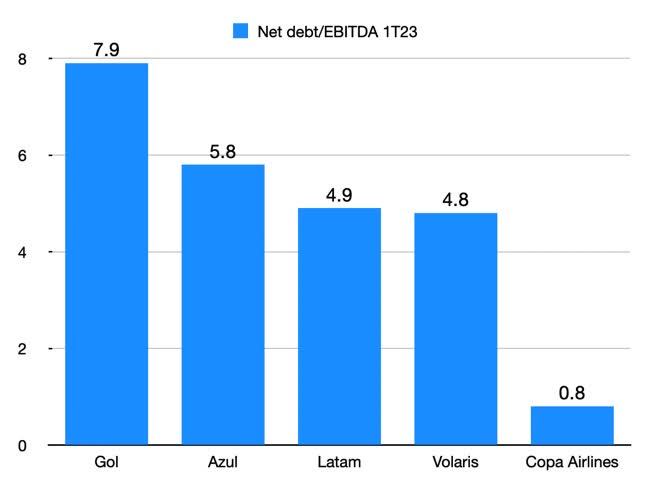

After the strong performance of its shares this past year, Gol is currently trading at an EV/EBITDA of about 18 times versus an average of 12 times over the past five years. These multiples are way ahead of their other Latin American peers, such as Azul ( AZUL ).

Despite the deal with Grupo Abra, which significantly reduced Gol's leverage by 22% year-on-year, Gol still has high leverage, trading at 7.9 times its net debt/EBITDA, compared to an average of 4.8 times for Latin American peers. This also shows signs of overvaluation in peer comparison.

{kind=link}

Chart compiled by the author using company quarterly results.

In the most recent quarter, Gol has demonstrated a positive trajectory in its traffic, although slightly below its annual guidance . This growth can be attributed to the impact of rising fuel prices and an improvement in corporate customers. Notably, the company achieved an 11% increase in Available Seat Kilometers (ASK) and a 14% growth in Revenue Passenger Kilometers (RPK).

However, it's important to note that Gol's operations are predominantly focused on the domestic market, with approximately 88% of its revenues generated from domestic flights. In contrast, its main domestic competitors, Azul and Latam, have a more diversified presence on international routes. Consequently, Gol is more susceptible to potential economic downturns or uncertainties within Brazil's economy, which can challenge its performance and growth prospects.

According to the latest release of the Brazilian Central Bank's Focus report , GDP is projected to grow by 2.19% in 2023 and 1.22% in 2024. Thus, based on the domestic market, I see less room for more exacerbated growth ahead.

The guidance given by Gol for 2023 is that the ASK should increase by 15% to 20%, which should still set up a 6% gap from pre-pandemic levels. The company's occupancy rate should stand at 81%, revenues generated should be 19.5 billion by the end of this year, and EBITDA should stand at a margin of 24%, which would be an amount of R$4.29 billion.

Preliminary June ASK results reported ahead of Gol's Q2 earnings, however, proved that the company has been meeting guidance by a hair, as it posted a 15.4% year-over-year rise.

While the projected revenue growth for 2023 stands at an impressive 31%, the outlook for 2024 and 2025 appears more challenging. Analyst consensus suggests that revenue growth for those years is expected to be 8.8% and 8.5%, respectively. This raises concerns about the company's ability to expand its demand in a potentially more adverse macroeconomic environment. Given the prevailing market conditions, the company may have lower expectations for growth.

Conclusion: Gol has already taken off this year

Considering the above data, it is pretty likely that a buy rating on Gol makes sense, given the company's broad advances over the year, especially with its major debt restructuring.

However, I remain reluctant to adopt a bullish stance now, considering the macro slowdown that could come ahead. On top of that, despite the recent short-term cash relief the Grupo Abra deal provided, the company's leverage remains high at higher levels than its domestic peers.

Gol valuations are not at stretched multiples. The company's 2023 EBITDA forecast of R$ 4.29 billion can estimate a forward EV/EBITDA of 5.92 times. It is not bad but is slightly above its prominent peer Azul, for example, at 5.52 times.

But it is prudent to consider that due to Gol's cyclical nature, the macroeconomic scenario may alter this projection looking further ahead, especially considering the sizable jump in the company's share price this year.

I expect Gol to continue its solid performance and achieve growth that aligns with market expectations in the upcoming quarter when it releases its results at the end of July.

However, when assessing the medium to long-term outlook, I perceive a potential macroeconomic disadvantage for Gol relative to its peers. With approximately 90% of its revenues derived from the domestic market, Gol faces increased vulnerability compared to competitors with a more diversified revenue base. This aspect is particularly noteworthy when considering a potential long-short trade strategy with Azul. Gol might be positioned on the short side of the trade as part of a risk-reduction approach in cyclical market conditions.

Given these considerations, it may be prudent for those who have missed out on Gol's strong performance throughout the year to adopt a cautious approach and observe from a distance.

For further details see:

Gol: Despite A Quant Top Pick, I Remain Neutral