GOL - Gol Linhas Aéreas Inteligentes: Q3 Earnings Not Enough To Turn Bullish

2023-11-23 23:00:52 ET

Summary

- The Brazilian airline Gol reported upbeat third-quarter results, with significant increases in revenues and EBITDA.

- The company's performance is influenced by factors such as fuel prices, exchange rates, and the ability to pass on costs to tickets.

- GOL faces risks related to fleet projections, aircraft deliveries, fuel prices, and ongoing efforts to restructure liabilities.

- Gol's valuation shows mixed metrics compared to domestic peers like Azul and LATAM Airlines.

My thesis on Brazilian airline Gol Linhas Aéreas Inteligentes ( GOL ) has been clouded by uncertainties, as highlighted in my recent articles. These uncertainties stem from its competitive disadvantage compared to domestic and Latin American peers and a less favorable macroeconomic environment that could significantly impact Gol's performance.

In my view, the optimal scenario for investing in Brazilian airlines is during falling exchange rates (US dollar vs. Brazilian real) and declining fuel prices. The period from July to October presented the opposite scenario. However, over the last two months, the decline in the price of Brent Crude Oil, coupled with the US dollar to Brazilian real below R$5, is beginning to make the scenario more intriguing.

Notably, the performance of Gol's shares has demonstrated an inverse relationship to the movements in Brent and the exchange rate.

Amidst these circumstances, Gol reported upbeat third-quarter results, demonstrating resilience in high fuel costs. However, its Yield indicates a growing challenge in passing on costs to tickets despite the expansion of the corporate client base and a higher occupancy rate in the third quarter of 2023.

Given the highly uncertain scenario, I perceive investing in Gol as extremely risky and speculative. This assessment is influenced by macroeconomic uncertainties surrounding the aviation sector, operational risks associated with the company's fleet projections, and the reduction of its revenue projection for 2024.

While I acknowledge the possibility of a favorable macroeconomic scenario in Q4, marked by a sustained drop in fuel prices and a weaker dollar against the Brazilian real, I prefer to maintain a wait-and-see position for a while longer.

Gol's 3Q23 Earnings Results Overview

Despite the company falling short of market consensus with reported EPS of -$1.37 compared to an estimated $0.03 and a slight miss in revenues by R$300 million, the third-quarter results for Gol indicate smooth sailing for the Brazilian airline.

Revenues for the quarter reached R$4.7 billion, marking a significant increase of 16.4% year-over-year and a notable 12.5% quarter-over-quarter. Meanwhile, reported EBITDA stood at R$1.25 billion, reflecting an impressive surge of 163.6% year-over-year and a solid 32% quarter-over-quarter. The Yield (fare per kilometer flown) for the third quarter of 2023 was 46.99 cents, showing a modest increase of 4.5% year-over-year but a marginal decline of 0.2% quarter-over-quarter.

Gol's IR

Reported EBIT and EBITDA margins also demonstrated strength, standing at 17.7% and 26.8%, respectively. Much of this improvement in profitability can be attributed to increased occupancy rates, leading to a more significant dilution of costs.

The reported CASK (Cost per Available Seat Kilometer) was 35.52 cents, reflecting an 8% year-over-year decrease. Meanwhile, CASK Ex-Fuel and CASK Fuel were 22.5 (an 18% year-over-year increase) and 13 (a 25.2% year-over-year decrease) cents, respectively. Despite the rise in costs excluding fuel, the substantial drop in the price of aviation kerosene (QAV) compensated, resulting in a decrease in the total cost in relation to seat supply.

Seasonality in the third quarter improved naturally compared to the second quarter of 2023, leading to increased take-offs and passengers. This logically boosted revenue per kilometer flown (RPK). Additionally, deflationary price adjustments announced by Petrobras ( PBR ) during the second quarter were fully accounted for, contributing to improved profitability and margins comparable to 2019.

Despite factors suggesting a potential increase in the fare per kilometer flown (Yield), a slight decrease in Yield was observed from the second to the third quarter of 2023. This deviates from the historical pattern, typically showing an increase during this period. The decrease in Yield signals a growing challenge in passing on costs to tickets despite the growth of the corporate client base and a higher occupancy rate in the third quarter of 2023.

Gol's IR

Corporate demand continues to improve, with corporate passengers rising by approximately 17.3% compared to the previous quarter, surpassing pre-pandemic levels.

Noteworthy are the positive performances of Smiles and Gol Log revenues, which, although still below pre-pandemic levels in relative terms, demonstrated another strong quarter in nominal terms. Gol projects a doubling of the fleet dedicated to logistics operations in 2024, potentially benefiting this segment.

Closing off the highlights for the quarter, cash generation remains a positive aspect. Gol reported operating cash generation of R$676 million, indicating a robust increase of 50.4% year-over-year. However, a significant portion of this cash was utilized for lease and debt payments. It's worth noting that excluding new borrowings and considering only the operating cash generated for debt payments, Gol would have consumed approximately R$29 million of its money.

Gol's IR

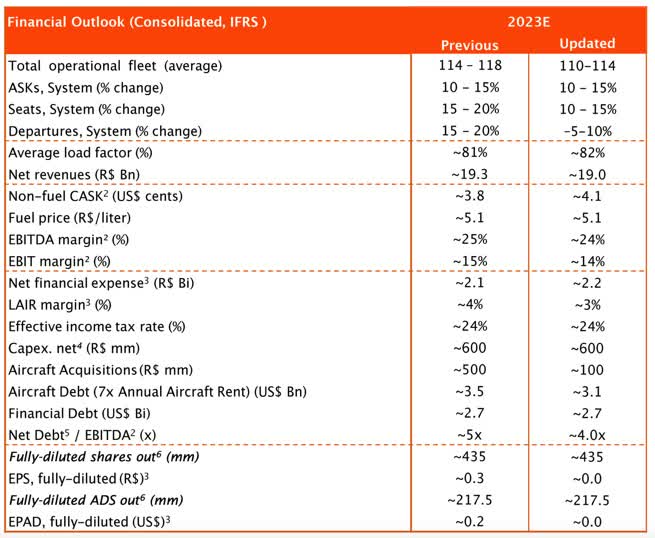

Finally, Gol updated its guidance for 2024, marginally reducing revenue projections by approximately R$300 million. This adjustment impacted the company's EBIT and EBITDA margins, decreasing one percentage point. It also updated the operating cost per available seat per kilometer ex-fuel, rising from 3.8 cents to 4.1 cents, and the pre-tax margin decreasing from 4% to 3%. Notably, the company maintained its fuel forecast at R$5.1/liter.

{kind=link}

Risks

Gol reported receiving only one of the fifteen aircraft scheduled for delivery this year in its third-quarter earnings call. The delay in the arrival of these new units, all 737 Max-8s, has compelled the company to revise its fleet projections. Gol operates with 108 aircraft, seven fewer than in the third quarter of 2019, before the onset of the COVID-19 pandemic.

Alongside adjustments to the balance sheet, the company anticipates ending the year with an operational fleet ranging from 110 to 114 aircraft, a reduction from the previous estimate of 114 to 118.

Gol's CEO, Celso Ferrer, emphasized the close relationship with its supplier, Boeing ( BA ), stating that four additional units are expected to be delivered by the end of this year. There is also a possibility that the remaining ten units will arrive in the first half of 2024.

The delivery schedule holds significance for the company's aircraft return plan. Four units were returned to lessors this year, and there is potential for another three to be replaced by the end of the fourth quarter, according to Gol, which currently has 20 aircraft in this situation. However, the return of these aircraft to service is contingent on potential delivery delays.

The returns and the retention of inoperative aircraft in the fleet contribute to increased costs for the company. Delays in new aircraft deliveries also pose challenges for Gol in expanding its capacity, a goal management aims to achieve with cost discipline. The company's forecast for the average occupancy rate in 2023 has increased from 81% to 82%.

In the absence of new aircraft arrivals, Gol is exploring alternatives. One strategy involves increasing the number of flight hours per plane to boost seat supply. Currently, aircraft flight time is 11.3 hours, down from an average of 12 hours before the pandemic.

Another factor of concern is fuel prices. Petrobras adjusted QAV prices in September and October by 21.4% and 5.6%, impacting the next quarter's results.

Despite the rise in fuel prices, the robust seasonality of the third quarter, even as the strongest of the year, is expected to mitigate the effects. However, escalating geopolitical conflicts remain a critical factor that could further increase oil prices, potentially impacting airline profitability when fares remain favorable.

Finally, a key risk factor is Gol's ongoing efforts to restructure its liabilities to address pandemic-related challenges. The company has released a new payment schedule, with most payments postponed to 2025. While this is a positive development, macroeconomic uncertainties in the aviation sector may pose a future risk of dilution. Additionally, uncertainties about the role of minority shareholders in the capital structure could be significant concerns for Gol.

Valuation

A notable disparity emerges in its trading metrics when comparing Gol to its primary domestic counterparts, Azul ( AZUL ) and LATAM Airlines ( LTMAY ). Gol exhibits a significantly higher forward EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization) than its peers. However, when contrasted with Azul, Gol trades at a substantial discount regarding the forward P/E (Price to Earnings) ratio.

Seeking Alpha

Given the capital-intensive nature of the airline industry and the inherent financial risks associated with economic cycles and external shocks, a balance sheet comparison becomes imperative. In this context, it becomes evident that Gol and Azul share a similar and delicate liquidity situation, featuring notably weak current and quick ratios below those of LATAM Airlines.

Seeking Alpha

Consequently, the valuation of Gol does not seem to offer a distinct advantage compared to its peers. Gol's EV/EBITDA for the trailing twelve months is 43% above the aviation industry average and 55% above its historical average over the past few years.

Despite the company's strong recovery this year, I perceive considerable risk, which prevents the identification of any glaring asymmetry based on the current valuation.

The Bottom Line

Gol reported favorable results in the third quarter of this year, characterized by significant improvements in unit revenue and positive free cash flow ((FCF)). Effective management of the balance between occupancy and fares and lower fuel costs has notably contributed to maximizing the company's profitability.

The operational advancements came at an opportune moment. However, one aspect that caught my attention was the marginal drop in Yield compared to the second quarter of 2023. Historically, there has been an upward trend from Q2 to Q3, which was not replicated in 2023. Observing a lower Yield gives the impression that passing on prices is becoming increasingly challenging.

In addition to this, Gol has modestly revised its guidance for 2023, with slightly lower revenue projections and increased costs.

Considering that I find the company's valuation less attractive than its peers, coupled with the risks the company will likely face in the short term, I maintain a neutral outlook.

For further details see:

Gol Linhas Aéreas Inteligentes: Q3 Earnings, Not Enough To Turn Bullish