AZUL - Gol Linhas: Positive Q2 Yet Fragility Amid Macro Headwinds

2023-09-19 18:31:58 ET

Summary

- Brazilian airline Gol Linhas Aéreas had a favorable first half of 2023 due to lower fuel prices, a weaker U.S. dollar, and increased passenger demand.

- The airline reported strong financial results in Q2, including a robust EBITDA margin and reduced leverage.

- Challenges may arise in the second half of the year with potential increases in fuel costs and a stronger U.S. dollar, which could impact Gol's performance.

The Brazilian airline Gol Linhas Aéreas Inteligentes ( GOL ) enjoyed a highly favorable first half of 2023, benefiting from a macroeconomic landscape characterized by lower fuel prices, a weaker U.S. dollar, and a resurgence in passenger demand.

In its recent Q2 report, the Brazilian low-cost carrier achieved noteworthy results across several key aspects. Notably, it reported a robust EBITDA margin and generated sufficient cash flow to reduce its debt.

However, there is a shift in the macroeconomic environment, with potential increases in fuel costs and a stronger U.S. dollar expected in the latter half of the year. This shift may pose challenges for Gol in maintaining demand as the airline grapples with the difficulty of passing these heightened costs onto passengers through fare increases.

In a previous article about the company from July, I highlighted Gol's competitive disadvantage compared to its domestic and Latin American peers and rated it a Hold. This disadvantage is particularly pronounced in a less favorable macroeconomic environment that could significantly impact Gol's performance. As this situation worsens and Gol's outlook for the year's second half becomes less optimistic, I still do not see compelling reasons to invest in the company.

Although I view Gol as a potential short-selling opportunity within a long-short trading hedge strategy involving its peers, such as Azul ( AZUL ), the company's improving fundamentals, as demonstrated in its recent financial results, and the positive preliminary demand trends observed in August, prevent me from adopting a more bearish stance towards Gol.

Positive Signs in Recent Results

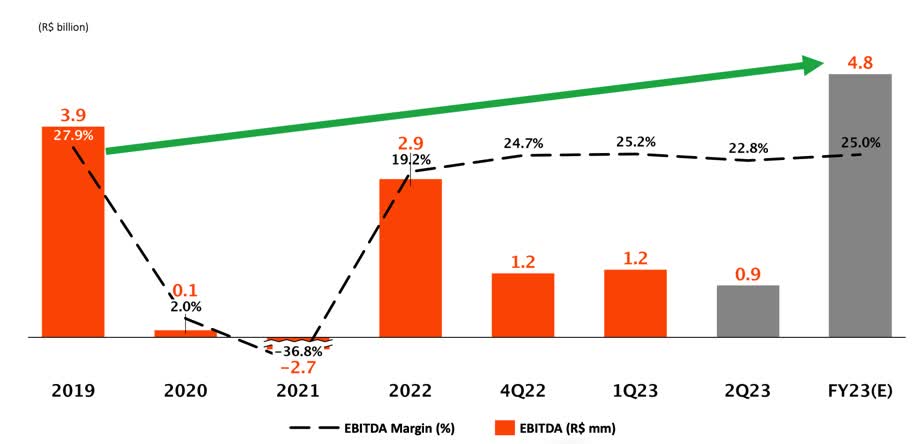

Gol's most recent second quarter results revealed several noteworthy points. EBITDA grew by 115.8% year-over-year, although it experienced a 23.5% quarter-over-quarter decline. Revenues increased by 27.9% year-over-year but fell by 15.7% quarter-over-quarter. Additionally, Gol reported a yield of 47.07 cents, reflecting a 9.5% year-over-year increase and a 3% quarter-over-quarter decrease.

Gol's IR

The standout positive aspect was the EBITDA margin at 22.8%, which, despite the drop compared to the first quarter of this year, remained at elevated levels and approached the levels reported in 2019. While Gol continued to report strong figures in Yield and RASK (Revenue per Available Seat Kilometer), these achievements were somewhat overshadowed by relatively high fuel costs, approximately 60% higher than the pre-pandemic period of 2019.

{kind=link}

For comparison purposes, if we consider the same average price paid per liter of QAV (Jet Fuel) in the second quarter of 2019 at current fare levels, the reported EBITDA would have been just over 50% higher than the current quarter's figure. In this scenario, the EBITDA margin would have been approximately 35%, significantly exceeding any levels observed previously.

Gol reported a profit of R$556 million, primarily driven by a favorable foreign exchange result resulting from the decline in the average exchange rate compared to Q1 2023 by approximately 5%.

In terms of leverage (IFRS), the company reported a ratio of 5x for the quarter, representing a decrease of approximately 1x compared to Q1 2023. This reduction stemmed from a decline in net debt of around R$850 million and a more substantial EBITDA base, which now excludes Q1 2022, a relatively weak quarter.

Gol's IR

In support of the belief that demand will remain robust, Gol revised its guidance for 2023. Despite a 5% reduction in its capacity projection, leading to an estimated revenue decrease of R$200 million, the company anticipated a 1% improvement in its EBITDA margin due to an expected reduction in the price of QAV throughout the year.

The latest preliminary results indicated that total demand (RPK) for Gol flights increased by 11.6% year-on-year in August. Flight supply (ASK) grew by 7.7%, and the load factor increased by 3.0 percentage points to 84.4%. In August, the total number of seats increased by 21.7%.

In the domestic market, the company's supply grew by 9.4%, and demand increased by 13.7%, resulting in a load factor of 84.6%, up by 3.2 percentage points year-on-year. Meanwhile, Gol witnessed a 7.4% decline in demand for international flights, with supply decreasing by 7.8% in August.

Leverage and Competitive Disadvantages

With the devaluation of the dollar and a decrease in fuel prices, cost pressures in Latin America's airline industry have eased. Passenger traffic has returned to pre-pandemic levels, creating a favorable environment for recovering profit margins. However, this optimism is not universal among all airlines, particularly in the case of Brazilian carriers.

To illustrate this point, both Gol and Azul experienced the most significant declines in the Brazilian stock market (Ibovespa) in August despite making progress in managing their debts and achieving solid operational results. The dollar's sharp appreciation against the Brazilian real in the past month has directly impacted Gol's debt.

Nevertheless, it's important to note that, despite these recent challenges, both airlines have still posted substantial gains in their share prices year-to-date.

Despite Gol's evident sequential improvement in profitability, marked by increasing revenues and cost reductions, the company still grapples with high leverage, even after reducing its net debt.

Gol remains optimistic about the potential for achieving higher profit margins than pre-pandemic levels in the coming years, thanks to the prospect of cheaper fuel. Recent results reflect a cautious approach, with only a partial transfer of cost savings to fare prices.

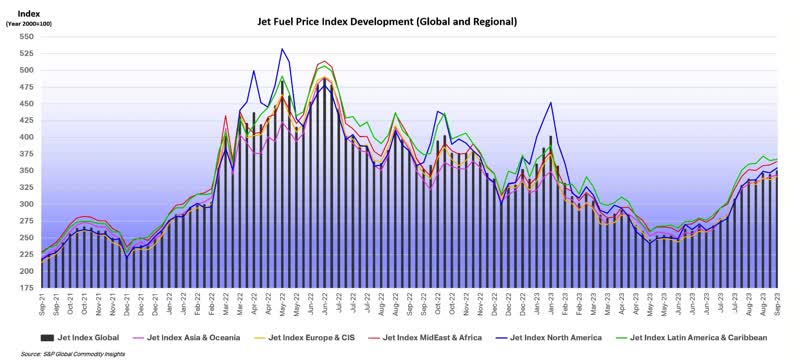

However, when considering the broader macroeconomic landscape in Latin America, it becomes apparent that other players in the aviation market maintain more favorable balance sheets with lower leverage levels. This is especially critical in a volatile macroeconomic environment with jet prices increasing. The graph below illustrates an upward trend in global jet fuel prices since May.

{kind=link}

One such airline is Copa Holdings ( CPA ), based in Panama. Copa is potentially better positioned to capitalize on the decline in fuel prices and may have less of a need to pass on aviation kerosene cost reductions to fares due to its strategic hub location. Copa's Panama hub reduces competition on its routes, granting the airline greater pricing power than its main competitors.

Gol's domestic peer, Azul, which effectively operates on 80% of its routes without significant competition, also holds an advantage in an adverse macro scenario. This enables Azul to adjust ticket prices to address these conditions more easily.

In terms of Gol's capital structure, the company holds a higher debt-to-equity ratio than Copa, specifically in the context of a net debt-to-EBITDA ratio of 0.5x for Copa, 4.2x for Azul and 5x for Gol. Concerning valuation, both companies are trading at similar multiples, with Azul slightly discounted.

The fuel situation in Brazil serves as a warning sign, a point emphasized by Gol CEO Celso Ferrer during the Q2 earnings call. Ferrer expressed his concerns about the continued volatility in the fuel and exchange rate scenario expected for the third quarter.

" Fuel prices have been fluctuating, and while they have decreased somewhat, they remain one of the most expensive in the world when compared to other countries, such as the United States, with a 49% higher cost," Ferrer stated. "In fact, it's more expensive than in all the neighboring countries in the region. "

Despite these challenges, Gol is committed to maintaining a pricing model featuring "very low" fares, as evidenced by the numerous promotions the company has been running. The expansion of promotional fares has been reflected in recent inflation indices. Nevertheless, Gol proceeds cautiously due to the unpredictable price fluctuations and the lag effect of exchange rates and fuel costs on fares.

Dilution's Impact on the Thesis

In mid-August, Gol made significant announcements regarding the potential dilution of shareholders through the issuance of warrants.

It's worth recalling that in March, the airline's board of directors had approved the conversion of $1.4 billion in senior secured notes subscribed by the Abra Group into Exchangeable Senior Secure Notes (ESSN).

As part of this arrangement, the company disclosed its intention to issue up to 1.891 billion warrants at an exercise price of R$5.84 per Gol shares (GOLL4 traded in the Brazilian stock exchange). Shareholders have until September 26 to exercise these warrants. These warrants can be converted into Gol shares at R$5.84 until March 2, 2028. Each shareholder will have the right to exercise 4.52 preferred shares for each Gol share.

Additionally, the controlling shareholder is transferring 991.951 million warrants, free of charge, to GOL Equity Finance, a subsidiary referenced in ESSNs (exchangeable senior secured notes).

Despite the favorable operating environment, Gol's involvement with the Abra Group, its stake in the Colombian airline Avianca, and the planned large-scale bond issue present significant challenges for minority shareholders.

The Bottom Line

The first half of the year has been notably positive for Gol, thanks not only to reduced fuel costs but also to the recovery in air traffic and the depreciation of the dollar against the real. However, it's crucial to acknowledge that this currency exchange rate trend has shifted in the last two months.

During this period, Latin American airlines have expanded their profit margins, allowing them to charge fares above the average. This leads me to believe that if fuel prices continue to rise, the aviation sector may face challenges in passing further cost adjustments to consumers, potentially leading to a squeeze on profit margins.

In a less favorable scenario, Gol's vulnerability to exchange rate fluctuations and higher fuel costs compared to similar peers in Latin America diminishes its attractiveness, in my view. This becomes especially evident when considering its valuation, which closely aligns with companies boasting a more favorable balance sheet, such as Copa Holdings and even Azul.

Given Gol's recent Q2 results and the outlook for a potentially more challenging macroeconomic environment in the latter part of the year, I remain cautious and opt to stay on the sidelines regarding Gol.

For further details see:

Gol Linhas: Positive Q2, Yet Fragility Amid Macro Headwinds