GFI - Gold Fields: A Solid Fundamental Outlook But The Price Just Isn't Right

2024-01-05 17:21:54 ET

Summary

- Gold Fields Limited's initial gold production from Salares Norte in Chile is delayed until April 2024, concurrently diminishing the asset's production outlook.

- The firm revealed underwhelming production results in Q3, with declines in South Africa, Ghana, and Australia. However, we think lower costs and higher gold prices will come into play soon.

- Unfortunately, Gold Fields' stock is overvalued. Moreover, technical indicators suggest mean reversion is en route.

- Gold Fields is a solid dividend opportunity. Nevertheless, its recent price action shows that its income-based return component can be overshadowed by overzealous price action.

Today's article dials in on Gold Fields Limited (NYSE: GFI ), which is a stock we covered approximately nine months ago. Fortunately for us, our readers, and Gold Fields' investors, the firm's stock has performed staggeringly well ever since. However, material events such as a revised Salares Norte production outlook and an uncertain full-year outlook for materials stocks mean it's time for revision from our end. As such, we collated a few of our latest findings on Gold Fields to communicate an updated outlook to our audience. Herewith are a few matters to consider if you're a current or prospective Gold Fields investor.

Previous GFI Rating (Seeking Alpha)

Salares Norte Production Update

Gold Fields released an unwanted bit of news at the end of last month, declaring that it expects its initial gold production from Salares Norte in Chile to materialize later than initially anticipated. According to Gold Fields' statement, the project is 99.3% complete but only due to produce in April instead of its previous set date of December 2023. Moreover, Gold Fields lowered its Salares Norte gold production outlook to 220,000 – 250,000 thousand ounces from a previous 400,000 - 430,000.

Gold Fields blamed the delay on pre-commissioning safety aspects, personnel availability, and manufacturer equipment configurations. Even though the mentioned events are part of mining and bound to happen at times, Salares Norte has dragged on quite a bit over the past few years. In fact, as we communicated in our previous coverage of Gold Fields, the Salares Norte project had experienced previous delays related to commissioning.

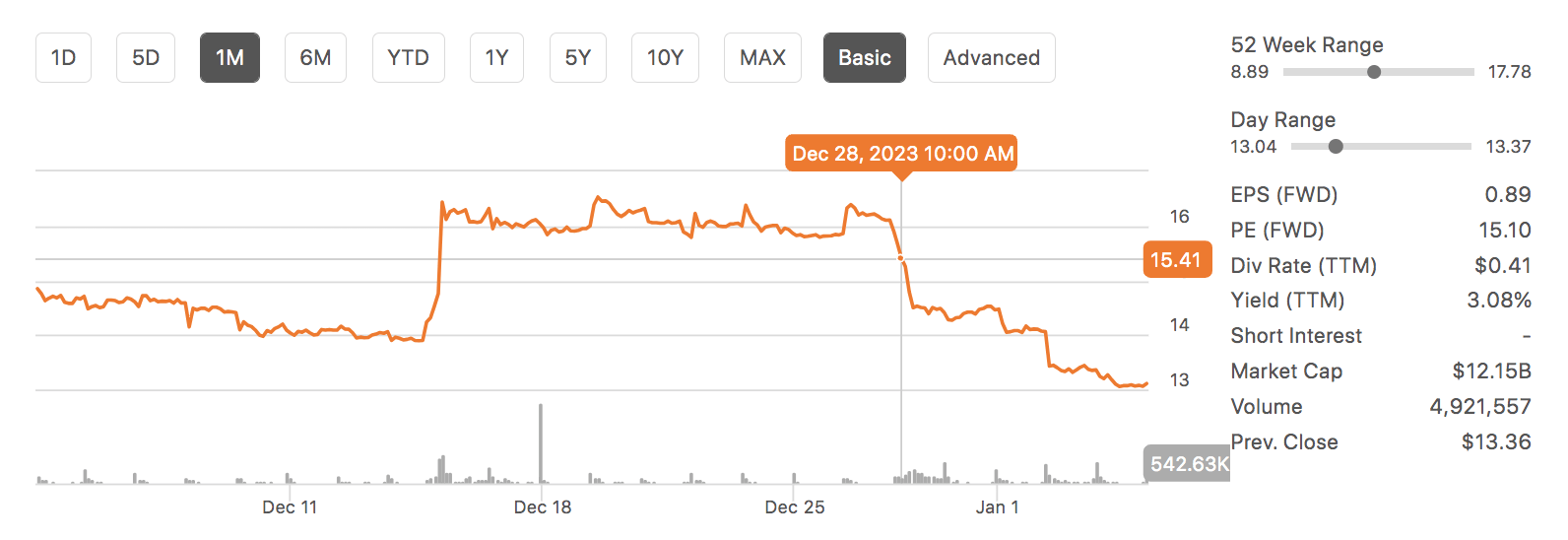

As mentioned in our previous article, the Salares Norte project is deemed highly lucrative as it has the potential to drop Gold Fields' cost basis and deliver high-quality material. However, the market's reaction after Gold Fields' production announcement suggests continuous delays have become a material event. Further delays could be priced very negatively by the market.

GFI stock's reaction to the announcement (Seeking Alpha)

{kind=link}

November Production Report & Outlook

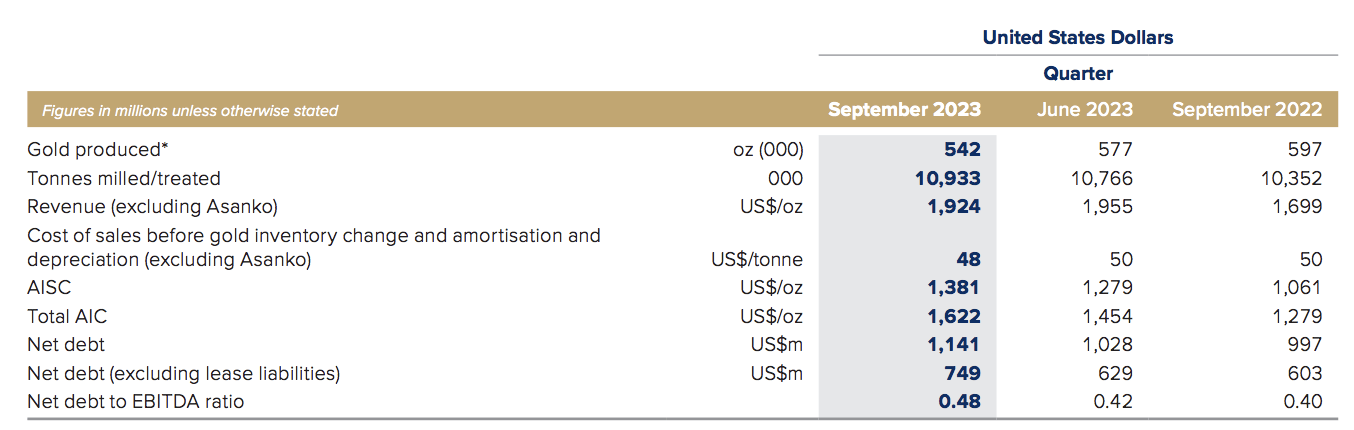

Gold Fields released its third-quarter production report back in November, revealing underwhelming results as production tapered and costs rose. Nevertheless, Gold Fields maintained its outlook, phasing out some of the negative rhetoric. Let's run through the salient features of its report and our commentary on each.

Q3 Report - Released in November (Gold Fields)

{kind=link}

Gold Fields' broad-based gold production fell by 9% a year earlier as a 14% drawdown from its Ghana operations was accompanied by an 8% decline in South Africa and a 5% decline in Australia.

In our view, the firm's South Deep Mine in South Africa could see robust performance in 2024. Well, at least from a relative point of view. South Deep was encumbered by regional labor concerns and grid issues in 2023. Moreover, grades declined between Q2 and Q3. However, we anticipate Eskom's load-shedding hours to decline into 2024 as South Africa is entering an election year and local municipal strikes have mostly ended. Furthermore, all-in-sustaining costs increased by 11% as per Q3, which is likely to flatline from now on, given lower regional inflation . The grade isn't something we can predict for you; however, it might be worth noting that reef grades at South Deep are among the best in the world and are likely to remain that way in the long term.

We are unsure what to make of Gold Fields' Ghana exploits. Production is tapering at Damang due to a narrowing pit width, implying that the mine is aging. Moreover, Tarkwa suffered from heavy rainfall in Q3, diminishing quarterly production by 13% to 129,000 ounces. Although Tarkwa is likely to revert to mean under normal conditions, Gold Fields decided to dispose of its 45% share in Asanko for $171 million . The disposition frees up capital for Gold Fields, but it brings regional synergies into question and makes the outlook for regional exploits opaque.

Lastly, a final material event relates to Australia, where Grueyere's 17% increase in quarterly production (to 88,700 ounces) was countered by substantial decreases in production from Granny Smith (down 12% to 64,000 ounces), St Ives (down 15% to 78,200 ounces), and Agnew (down 10% to 57,200 ounces). Lower grades across the board had a significant impact, as did inventory sequencing. We see no material reasons why Gold Fields' Australian production will be disrupted in early 2024, especially with El Nino phasing out the risk of rainfall. Moreover, Australian inflation is tapering, allowing growth in all-in-sustaining costs to abate.

Gold Price Outlook

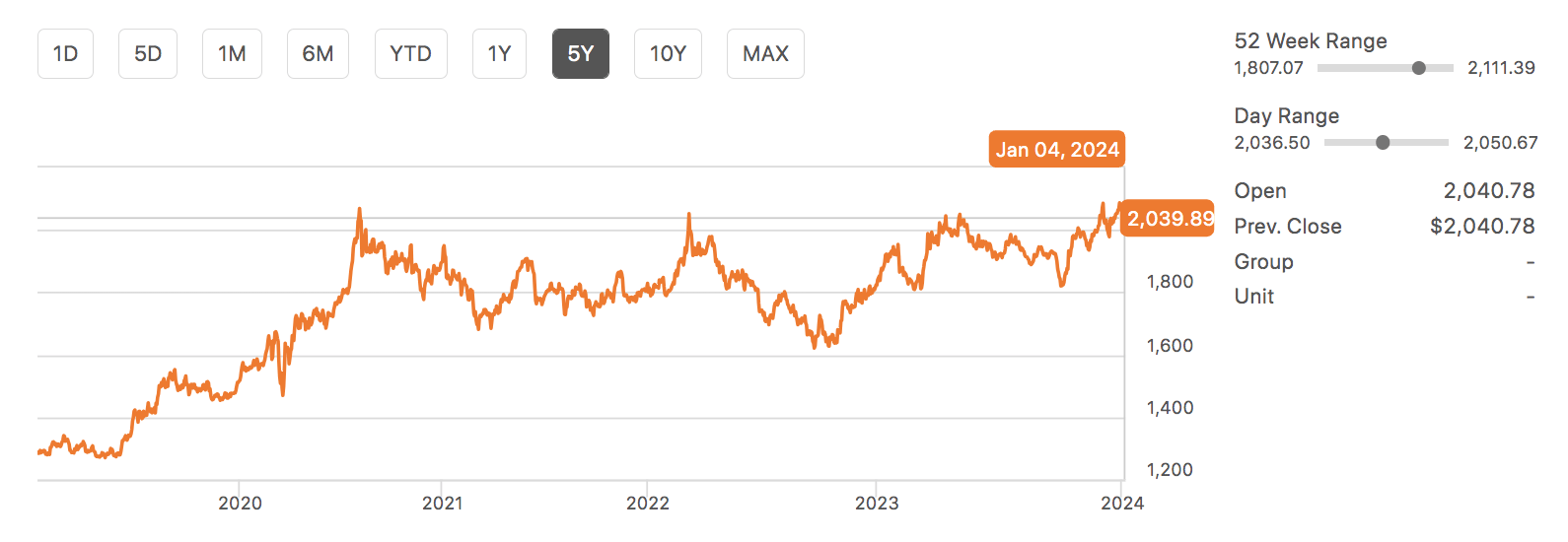

Gold prices will be pivotal to Gold Fields' new year performance. Let's traverse into a brief discussion of our outlook on gold.

{kind=link}

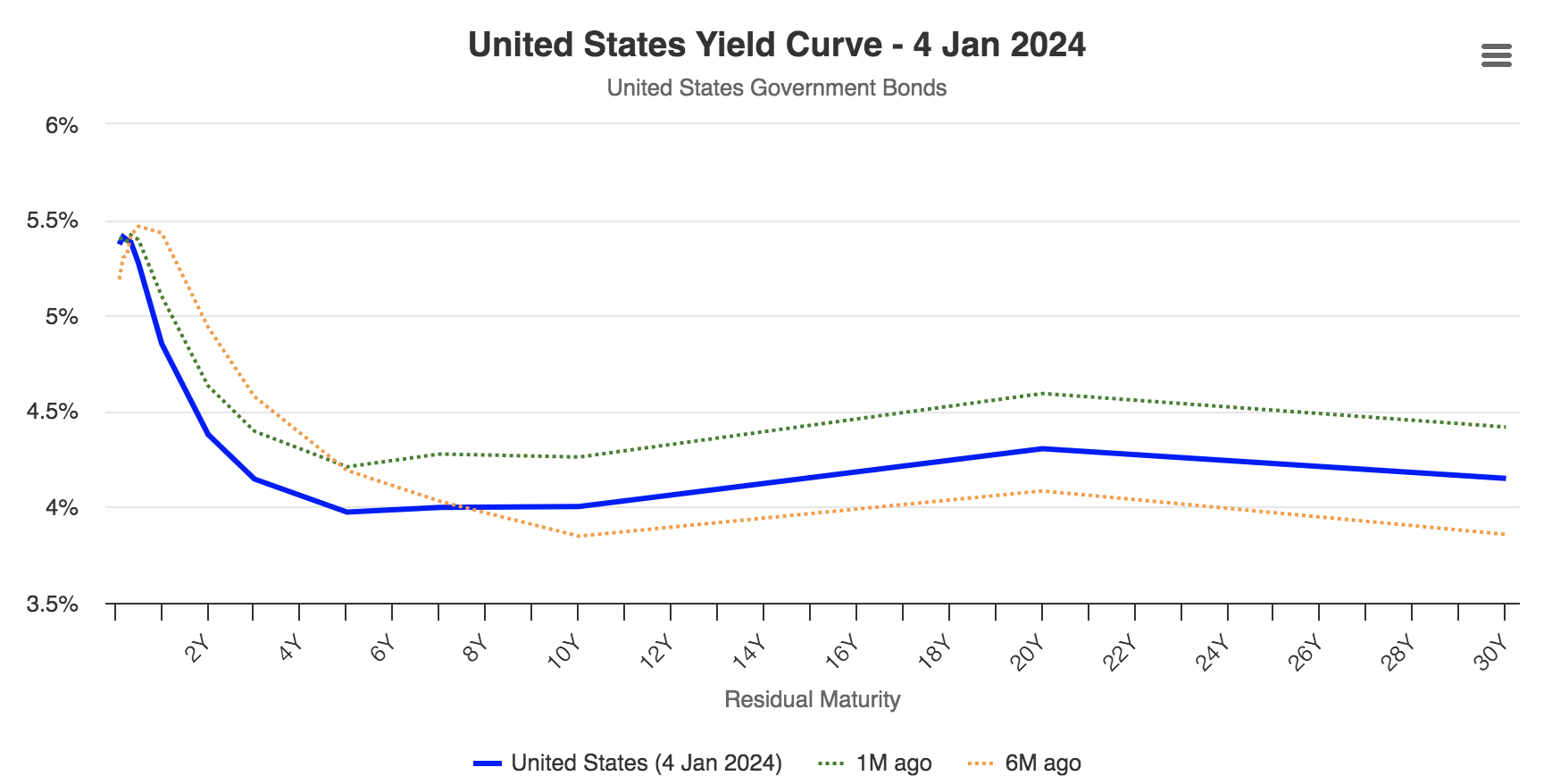

We think gold will rally soon, which we base on two factors. Firstly, the U.S. yield curve implies lower U.S. interest rates are en route, which might lower the U.S. dollar's value and concurrently provide support to gold as a reserve currency proxy. Moreover, gold is often utilized as a safe haven asset, which could come into play once interest rates drop as recession risk usually mounts whenever aggressive rate cut policies are implemented. As such, we see nothing but an increase in gold spot prices occurring in 2024.

U.S. Yield Curve (worldgovernmentbonds.com)

{kind=link}

Stock Price Level and Dividends

Although we believe gold prices and fundamental stealth will assist Gold Fields in the near term, a faultline exists in the stock's valuation, and its technical price level is worrisome.

Gold Fields has a forward price-to-book ratio of 2.67x , suggesting its stock is grossly overvalued, as mining investors usually emphasize price-to-book values. Lower interest rates paired with other factors like increased gold prices and higher industry M&A activity could spark an increase in Gold Fields' book value via measurement. However, it would take some doing to get it back into range. In addition, apart from its price-to-earnings ratio, many of Gold Fields' other primary price multiples are at cyclical premiums, adding fuel to the fire.

| Metric |

| Value |

| Versus 5-year AVG |

| FWD P/E |

| 15.10 |

| -21.95% |

| FWD EV/EBITDA |

| 5.51 |

| +10.98% |

| FWD P/CF |

| 7.48 |

| +27.50% |

| FWD EV/Sales |

| 2.98 |

| +19.74% |

Source: Seeking Alpha

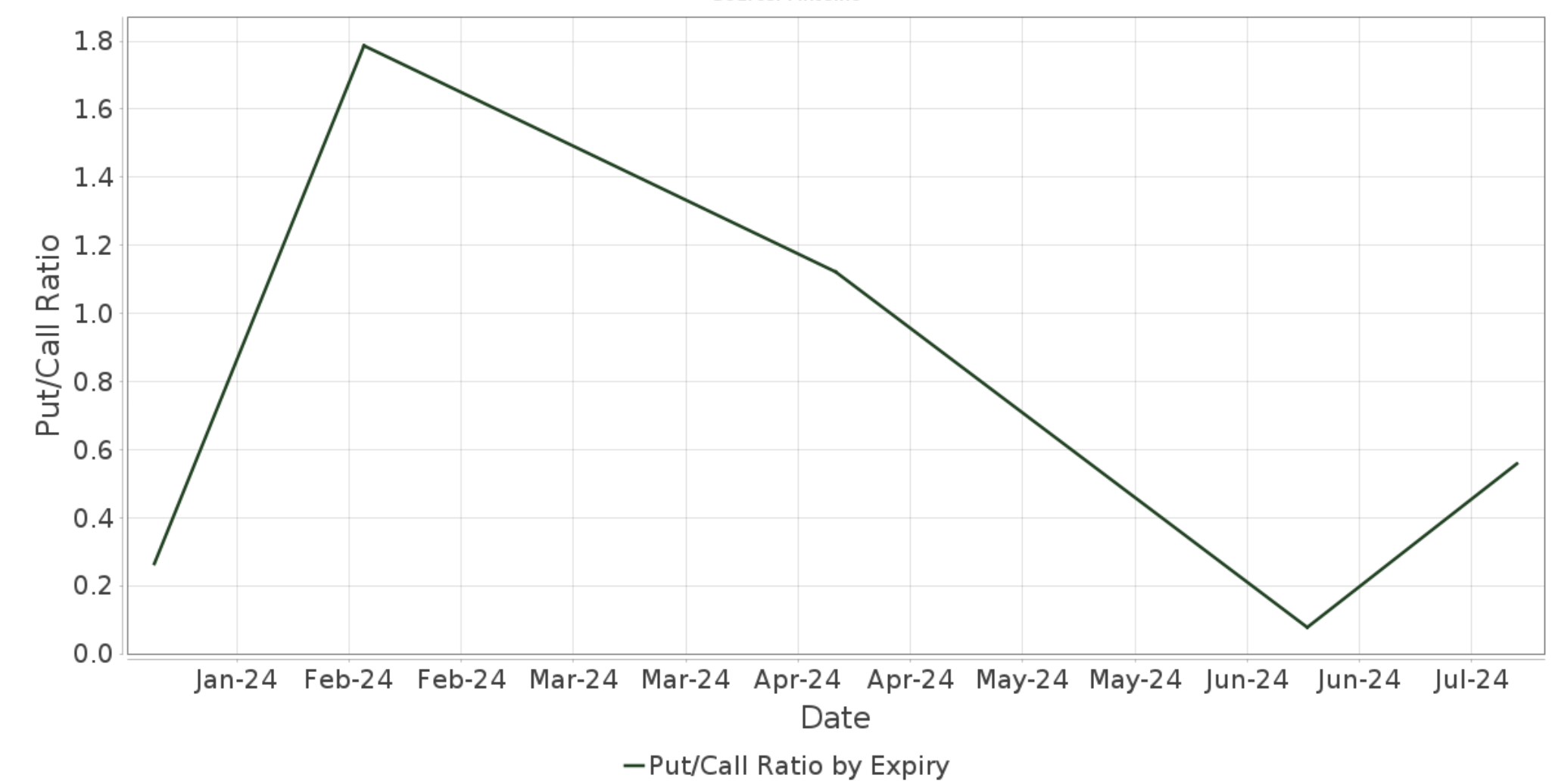

Furthermore, Gold Fields' stock seems overbought from a technical perspective. The stock's put-call ratio of 0.32x conveys bullish sentiment from options traders. However, the put-call ratio is usually utilized as a countercyclical metric, suggesting mean reversion is likely. Moreover, Gold Fields' 10-, and 50-day moving averages have dipped below its long-term 100-day moving average, which we consider the start of a bearish trajectory.

{kind=link}

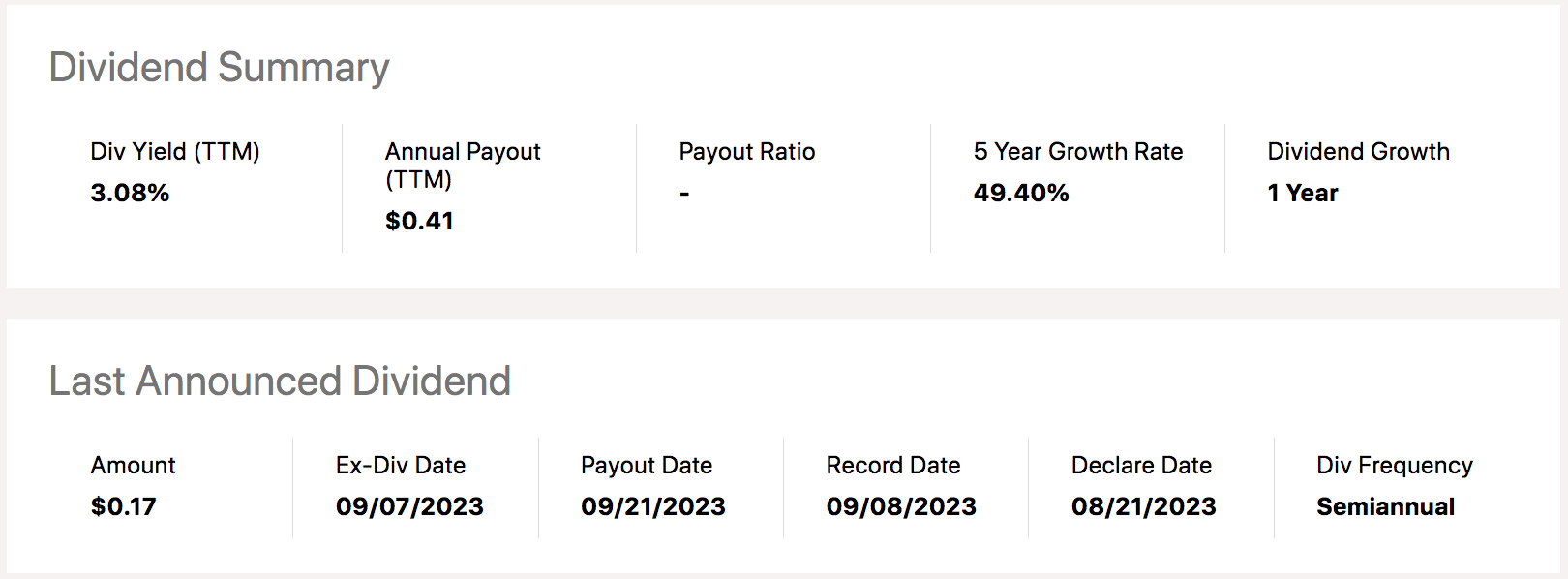

Lastly, let's look at Gold Fields' dividends.

The firm's policy for 2023 was to pay out between 30% and 45% of its normalized earnings, which largely explains its compelling dividend yield of 3.08%. The firm has delivered nine consecutive years of dividends to its shareholders and possesses a 10-year dividend CAGR of 17.57% . As such, it needs little introduction as a sustainable dividend stock. However, as shown by its recent price action, Gold Fields' dividend return component can be overshadowed by stock volatility, which is a worthwhile consideration for dividend-seeking investors.

{kind=link}

Final Word

Our analysis shows that Gold Fields' fundamentals could rebound this year after its production and costs acted unfavorably in recent months. However, as illustrated by valuation and technical indicators, the stock's latest surge has sent it into a territory that leaves it vulnerable to mean reversion.

Although we think the market has already priced adverse events at Salares Norte, our updated outlook downgrades the stock to hold from a previous strong buy due to a lack of embedded value within the stock.

For further details see:

Gold Fields: A Solid Fundamental Outlook, But The Price Just Isn't Right