GFI - Gold Fields: A Tough Q3 With Labor Issues Persisting

2023-12-01 07:09:51 ET

Summary

- Gold Fields' Q3 production declined by 9% due to lower output from all geographies and all of its managed mines.

- Meanwhile, costs soared year-over-year to $1,381/oz, with AISC margins lower despite the benefit of a higher average realized gold price.

- In this update we'll dig into the Q3 results, the stock's valuation after its recent ~45% rally, and whether the stock is worthy of investment at current levels.

Just over two months ago, I wrote on Gold Fields (GFI), noting that while the stock's valuation was improving it looked likely that the stock would retreat to below US$11.00 given the negative momentum for the stock and continued margin declines from sticky inflationary pressures. Since then, the stock suffered a 15% plus drawdown and slid back towards the US$10.00 level, but has recovered nicely since its early October lows. This can be attributed to improving sentiment in the sector with gold recovering back to just shy of all-time highs, in addition to excitement about Salares Norte where first production is expected by year-end (albeit with 2023 output below previous estimates and 2024 guidance also reeled in). In this update we'll dig into the Q3 results, the stock's valuation after its recent ~45% rally, and whether the stock is worthy of investment at current levels.

{kind=link}

Q3 Production & Sales

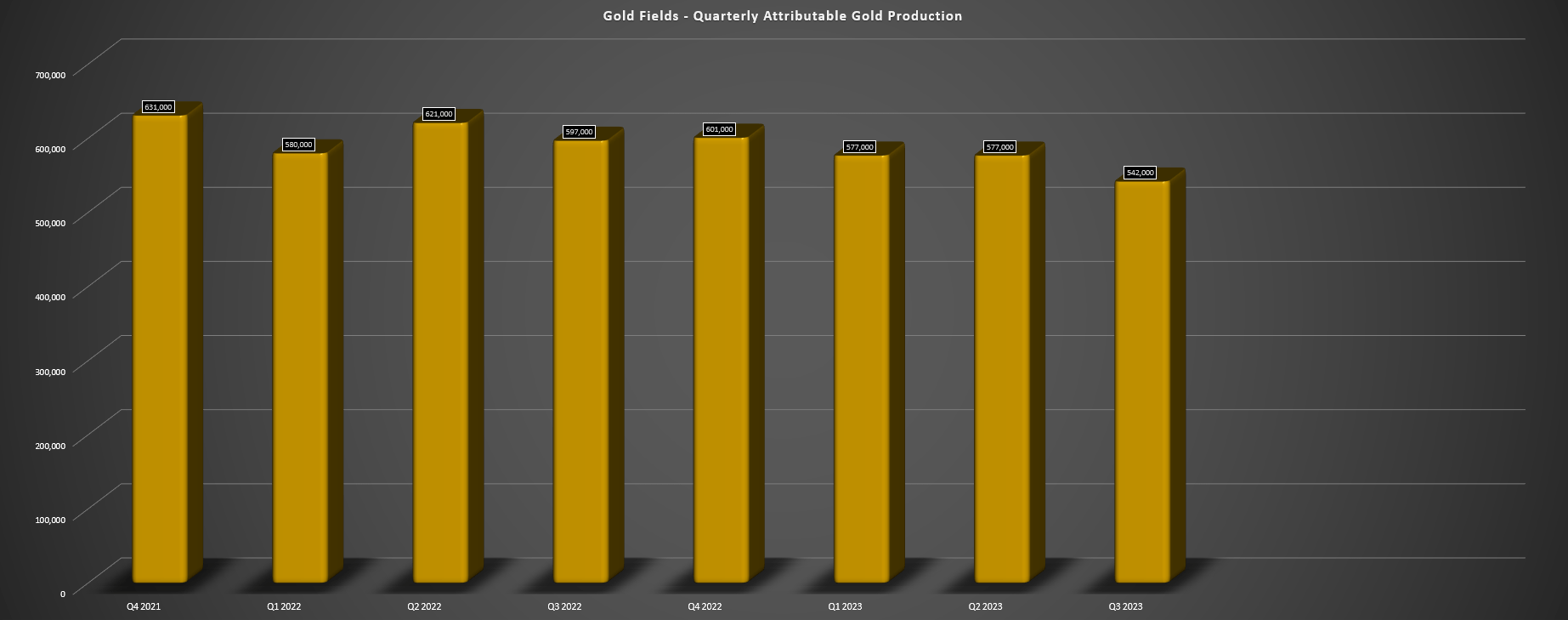

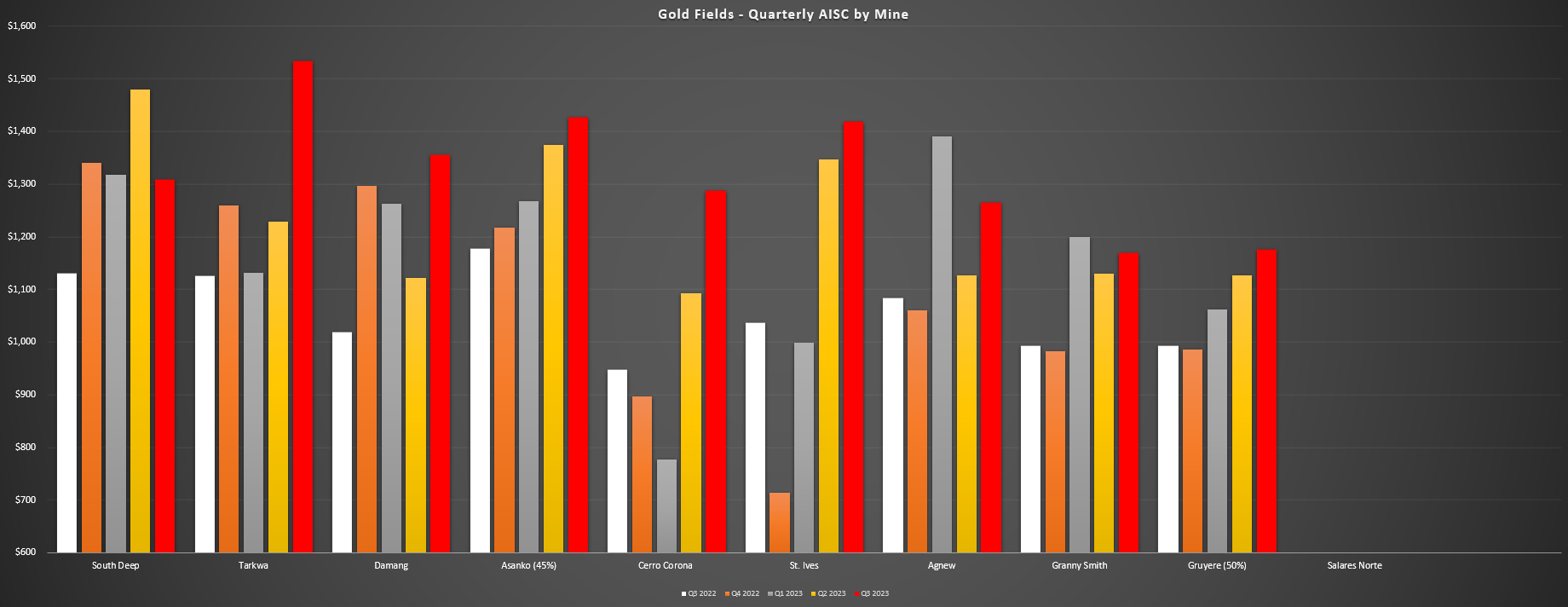

Gold Fields released its Q3 results earlier this month, reporting quarterly attributable production of ~542,000 ounces of gold, a ~9% decline from the year-ago period. This significant decline in output was related to lower output from all of its geographies (Australia, South Africa, Ghana, South America), with the largest year-over-year declines at Damang, Cerro Corona, South Deep, and Granny Smith. The result was that Gold Fields' production is sitting just below 1.7 million ounces of gold year-to-date, with a strong Q4 needed to deliver above its guidance mid-point of ~2.27 million ounces of gold (ex-Asanko). Unfortunately, costs were also up across the board at its operations, with all-in sustaining costs [AISC] soaring to $1,371/oz (Q3 2022: $1,044/oz), resulting in margin compression despite easy comps as it lapped a realized gold price of $1,699/oz in the year-ago period.

Gold Fields - Quarterly Attributable Gold Production - Company Filings, Author's Chart

{kind=link}

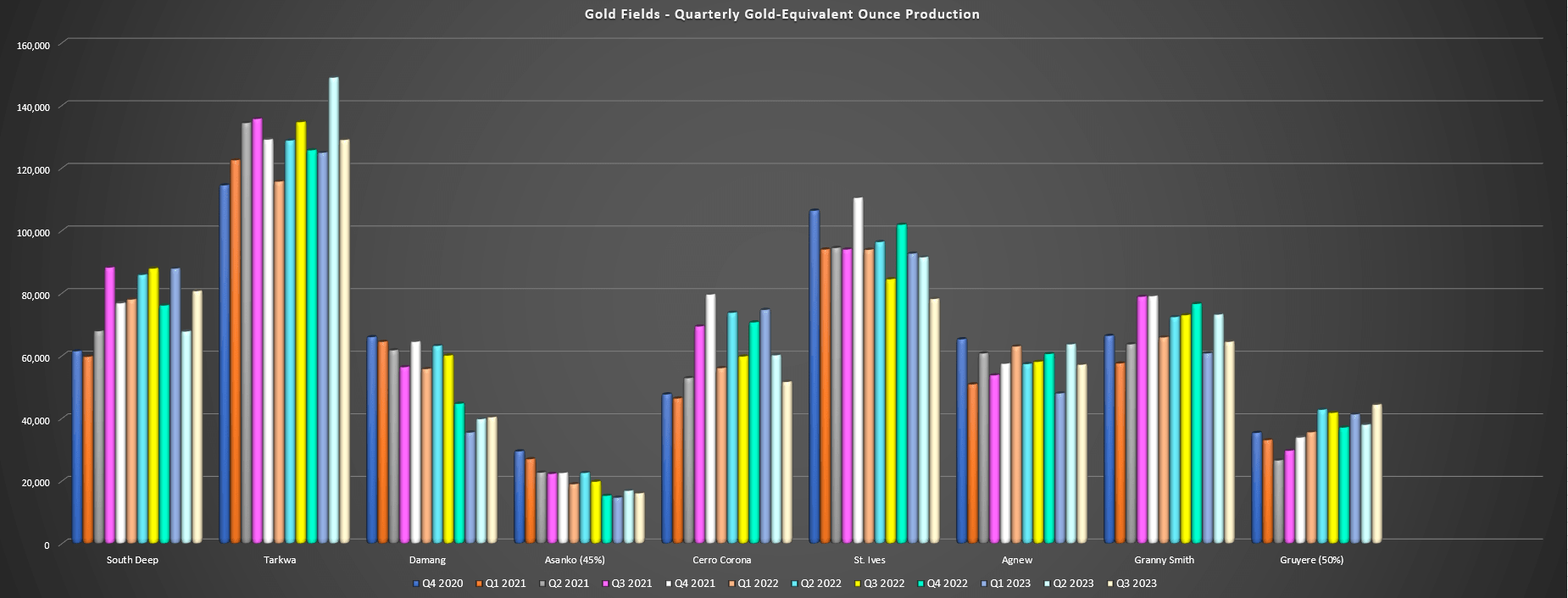

Digging into the operations a little closer, Damang's production was impacted by lower grades (1.02 grams per tonne of gold vs. 1.55 grams per tonne of gold) as the main pit nears the end of its life, with just ~1.18 million tonnes mined at an average grade of 1.17 grams per tonne of gold. The result was the production of just ~40,400 ounces (Q3 2022: ~60,100 ounces), and a sharp increase in all-in sustaining costs to $1,355/oz. Elsewhere in Ghana at the company's largest Tarkwa Mine, production slid to ~129,000 ounces (Q3 2022: ~134,700 ounces) with higher throughput offset by lower grades with a greater reliance on stockpiles vs. the year-ago period. Like Damang, all-in sustaining costs rose here as well to $1,533/oz from $1,126/oz, partially impacted by fewer ounces sold and a gold in-process charge of $28 million.

Gold Fields - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

Moving over to Australia, production was down ~5% year-over-year to ~244,000 ounces, with higher production at Gruyere (50%) offset by lower production at its St. Ives, Agnew, and Granny Smith mines. Meanwhile, all-in sustaining costs for its operations jumped to $1,272/oz (Q3 2022: $1,029/oz), with Gold Fields processing lower grades on balance and calling out a shortage of skilled labor that's expected to remain a headwind for its Australian segment. The most significant decline in output was at Granny Smith (~64,500 ounces vs. ~73,000 ounces) with the higher milled tonnes offset by lower grades due to vent-related restrictions which resulted in mining lower-grade material from upper mine areas. Fortunately, the mine is now back on track with full access to lower areas of the mine, but this led to a meaningful increase in costs for the operation despite the weaker AUD/USD ($1,169/oz vs. $992/oz). Elsewhere at St. Ives, production was also down with higher costs (~78,200 ounces at $1,419/oz) due to lower grades in line with the mining sequence at Hamlet/Invincible.

{kind=link}

As for South Deep in South Africa, production was down meaningfully at this South African mine as well. As highlighted in the prepared remarks, the increased throughput of ~782,000 tonnes was offset by lower grades of 3.21 grams per tonne of gold (Q3 2022: 3.66 grams per tonne of gold), with lower underground grades year-over-year. This translated to a much higher AISC of $1,309/oz and Gold Fields noted that attracting and retaining key skills (including artisans and long-hole stoping rig operators) has " continued to impact fleet availability and utilization and consequently performance at South Deep ". This is certainly not an ideal development when combined with a tough labor situation in Australia, suggesting that it's best to be more conservative modeling unit costs in 2024/2025 even when factoring in a new high-margin asset coming online in Salares Norte.

Finally, at the company's Cerro Corona Mine in Peru, production slid 14% year-over-year to ~52,000 gold-equivalent ounces [GEOs] and costs rose from $948/oz to $1,288/oz. The company noted that this was impacted by lower grades and recoveries, with slightly lower gold recoveries and lower copper recoveries of 86.8% (Q3 2022: 89.6%) more than offsetting the slightly higher throughput year-over-year. On a positive note, Gold Fields has finally appointed a new CEO in Mike Fraser (effective January 2024), with Mike Fraser previously being COO of South32 ( OTCPK:SOUHY ) for its Aluminum, Nickel, SA Manganese and Energy Coal businesses, and currently CEO of AIM-listed Chaarat Gold Holdings, a company with a construction-stage project (Tulkubash) in the Kyrgyz Republic, and a large underground refractory project (~300,000 ounces per annum potential) called Kyzyltash. Finally, the company had a small operating polymetallic mine in Armenia which was recently sold.

Overall, Gold Fields' performance was below my expectations, but it's nice to see a permanent CEO in place and while Salares Norte won't produce as much as expected this year, the mine is on track to have a massive year in 2024 (400,000+ gold-equivalent ounces) at industry-leading margins. Let's take a closer look at its Q3 costs and margins below:

Costs & Margins

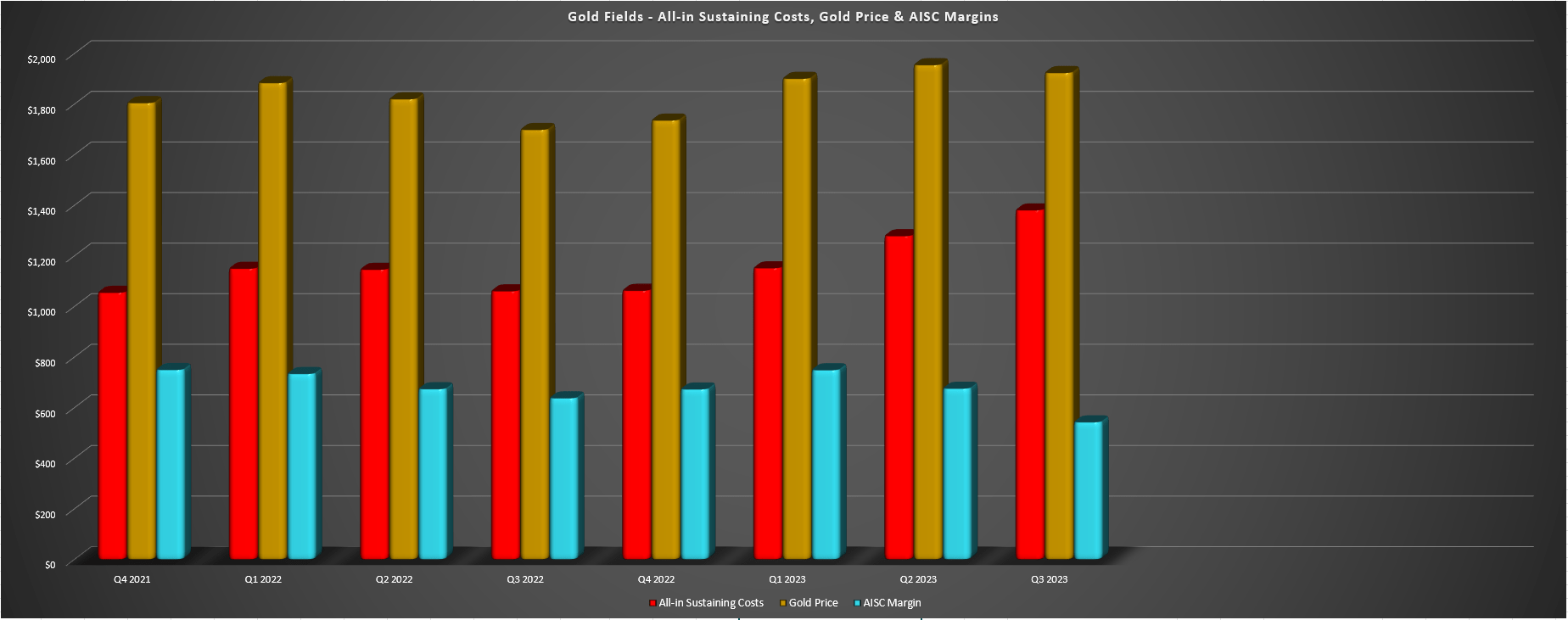

Moving over to costs and margins, Gold Fields reported all-in sustaining costs of $1,381/oz (including Asanko), a significant increase from the year-ago period. As noted previously, this was related to higher costs across the board with group-weighted effective mining cost inflation remaining elevated at ~5.9% vs. an initial estimate of ~5% and on top of 10.7% inflation last year (led by Australia, Ghana, and Peru). The chart below highlights that these unit cost increases were broad-based and given the significant increase in unit costs with a further impact from a shortage of skilled labor in Australia/South Africa, AISC margins actually fell 15% year-over-year to $543/oz despite the benefit of a much higher average realized gold price, partially impacted by higher sustaining capital spend in the period and of course fewer ounces sold. Plus, while Salares Norte was previously expected to provide some production in Q4 (15,000 to 35,000 GEOs), this estimate has been revised to just 1,000 GEOs, with the project 97% complete as of the most recent update.

Gold Fields - AISC, Gold Price & AISC Margins - Company Filings, Author's Chart Gold Fields Quarterly AISC By Mine - Company Filings, Author's Chart

{kind=link}

{kind=link}

On a positive note, Gold Fields has two high-margin projects in the wings that are set to move into commercial production in Q3 2023 and Q3 2026, respectively (assuming timely receipt of EIA at Windfall). These two assets are expected to contribute ~700,000 GEOs combined at sub $800/oz all-in sustaining costs (inflation-adjusted basis) near peak production levels, more than offsetting lower production from Damang and helping to pull down Gold Fields's elevated AISC after three years of well above-average inflationary pressures. The other positive is that while costs are likely to remain elevated in Q4, the company will at least have the benefit of a higher average realized gold price sequentially with gold averaging ~$1,955/oz quarter-to-date. That said, the significant benefit from a margin standpoint won't arrive until H2 2024, and Salares is now expected to see just 400,000 to 430,000 GEOs in FY2024, down from ~500,000 previously (providing less of a tailwind for margins).

To summarize, while Gold Fields may have a very strong pipeline with 50% of a top-3 undeveloped gold asset in Canada from a margin standpoint and a Tier-1 scale asset with industry-leading margins nearly completed, costs at core operations were above my expectations in Q3 and it's unfortunate that these headwinds are expected to persist in Australia. Hence, while we should see a very different margin profile in H2 2024 (especially if the gold price continues to cooperate), I wouldn't expect to see much better results in Q4 and the company will need to work on its safety performance with another fatality at Tarkwa in Q3 (in addition to one in Q1), on top of a fatality at St. Ives in October 2022. Let's look at the stock's valuation:

Valuation

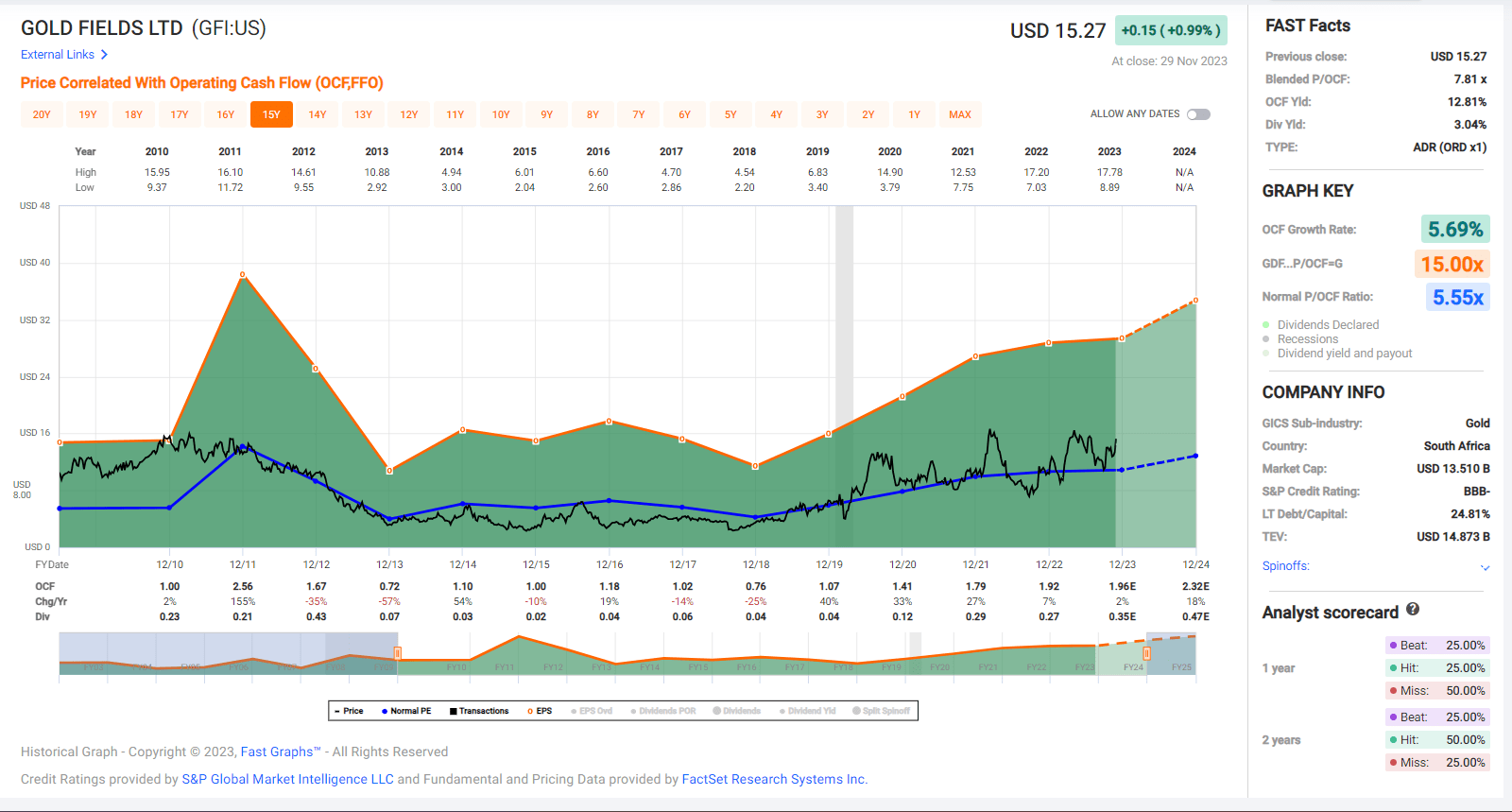

Based on ~894 million shares and a share price of US$15.30, Gold Fields trades at a market cap of ~$13.7 billion and an enterprise value of ~$14.8 billion. This valuation continues to leave Gold Fields at nearly double the valuation of Kinross ( KGC ) despite a ~40% higher production profile assuming ~2.8 million ounces in 2025 and despite Kinross having a better jurisdictional profile with a greater proportion of ounces coming from Tier-1 ranked jurisdictions (plus no South Africa exposure). Plus, as the chart below shows, GFI is now back above its long-term average from a cash flow multiple standpoint after its recent rally. And using what I believe to be a fair multiple for the stock of 7.2x cash flow (45% premium to 10-year average given its improving jurisdictional profile and addition of a Tier-1 scale asset at Salares Norte), I see a fair value for GFI of US$16.90, pointing to an 11% upside from current levels.

{kind=link}

Although this does suggest there could be more upside in the current rally, I am looking for a minimum 35% discount to fair value to justify starting new positions in large-cap producers. So, while I see long-term upside in GFI once Windfall and Salares Norte are in commercial production and the company should look quite different by H2 2026 with a better jurisdictional profile and higher margins, the ideal buy zone for the stock comes in at US$11.00 or lower, where I highlighted the stock would move into a low-risk buy zone in my previous article. Hence, if this rally were to continue on the back of improved sentiment sector-wide, I would view any rallies above US$17.10 before February as an opportunity to book some profits.

Summary

Gold Fields had a mediocre Q3 and commentary was mixed overall, with Salares Norte remaining on track for production by year-end but the labor situation not improving much in two of its key jurisdictions, suggesting further pressure on labor costs. In addition, although Gold Fields will have a better FY2024 with the benefit of a high-margin operation in production, the slower-than-planned ramp-up vs. initial estimates has led to production estimates being curtailed and less than six months of commercial production vs. my estimate of closer to nine months previously. Hence, although costs should decline year-over-year and cash flow will improve with significant capex rolling off at Salares Norte, the real margin turnaround should occur in 2025 (a full year of commercial production). Hence, with another mediocre quarter or two on deck (barring a further rise in gold prices), and a less attractive valuation from a relative standpoint, I continue to see more attractive bets elsewhere in the sector.

For further details see:

Gold Fields: A Tough Q3 With Labor Issues Persisting