OBNNF - Gold Fields Acquires 50% Of Windfall: A Fair Deal Or A Bargain?

2023-05-03 08:37:17 ET

Summary

- Gold Fields will acquire 50% of the Windfall project for total consideration of over C$600 million.

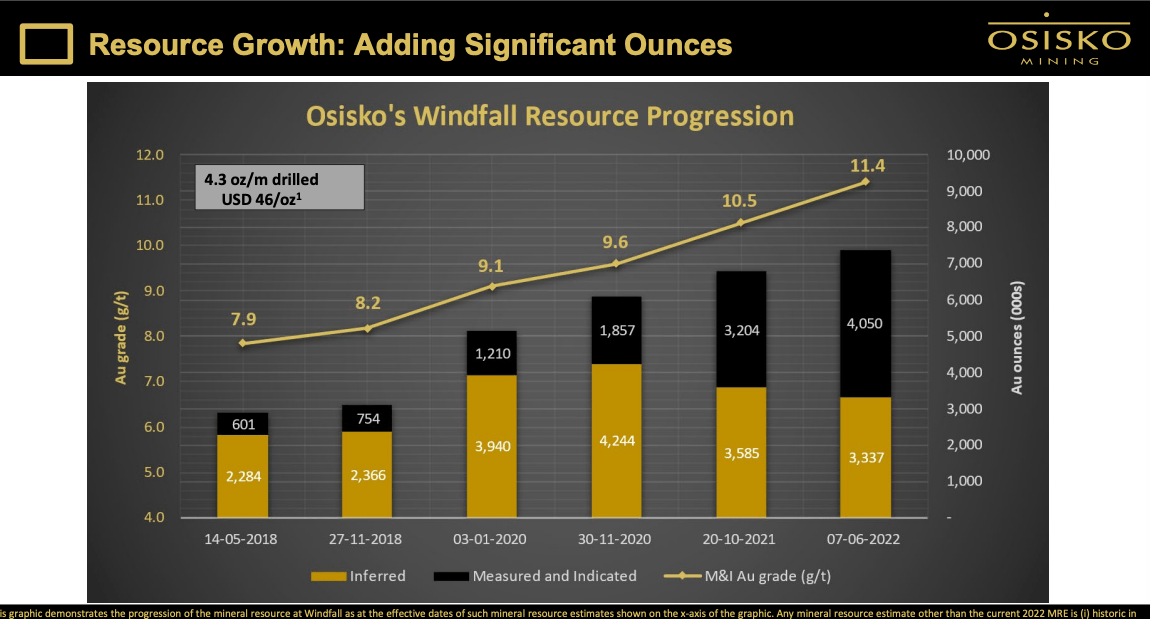

- Windfall boasts a large, high-grade resource of nearly 7 million ounces of gold at grades over 10 g/t, placing it among the top 10 projects worldwide.

- The move diversifies Gold Fields reserves and production into a low-cost asset in a top-tier mining jurisdiction.

- Who is getting the better end of the deal?

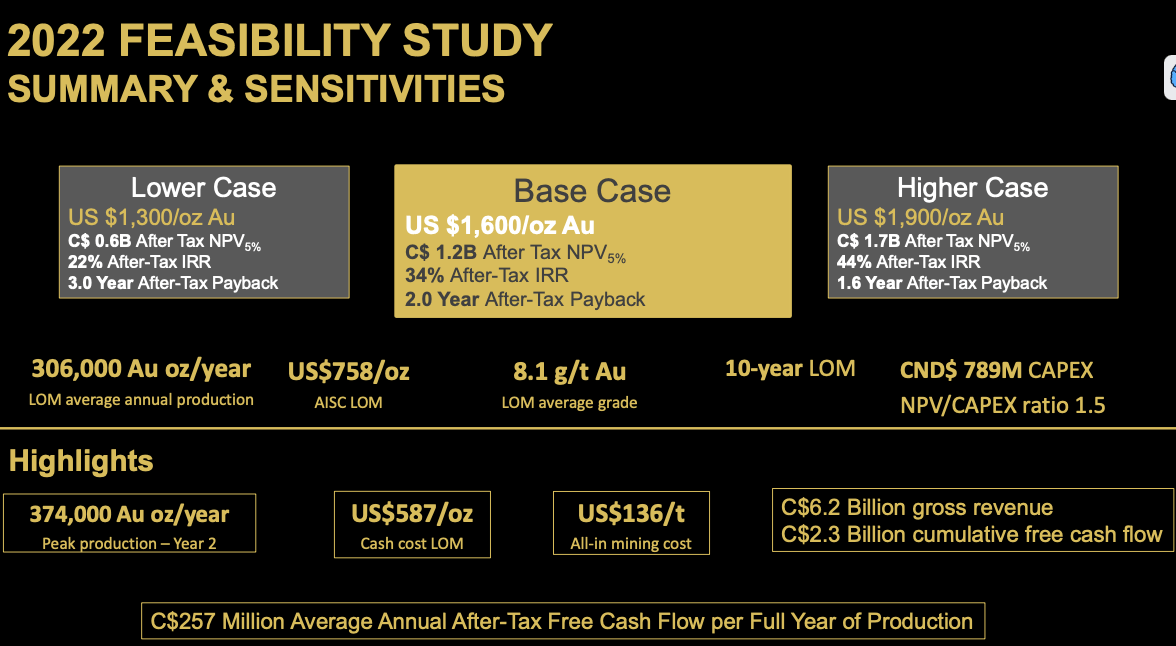

Gold Fields (GFI) has agreed to buy half of Osisko Mining's (OBNNF) Windfall project for total consideration of over C$600 million. This represents half of Windfall's post-tax value of C$1.2 billion (using a $1,600/oz gold price), according to its feasibility study. So, Gold Fields is paying fair market value for its 50% ownership stake based on this valuation.

While it appears Osisko Mining is getting a great deal here, I believe Gold Fields is getting the better end of the bargain, as I argue below.

Osisko's Windfall Project: A Quick Overview

Windfall is an impressive gold project that has attracted interest from gold mining industry players for years.

It's easy to see why: Windfall boasts a large, high-grade resource of nearly 7 million ounces of gold at grades over 10 g/t, placing it among the top 10 projects worldwide for gold deposits expected to produce at least 100,000 oz Au per year.

{kind=link}

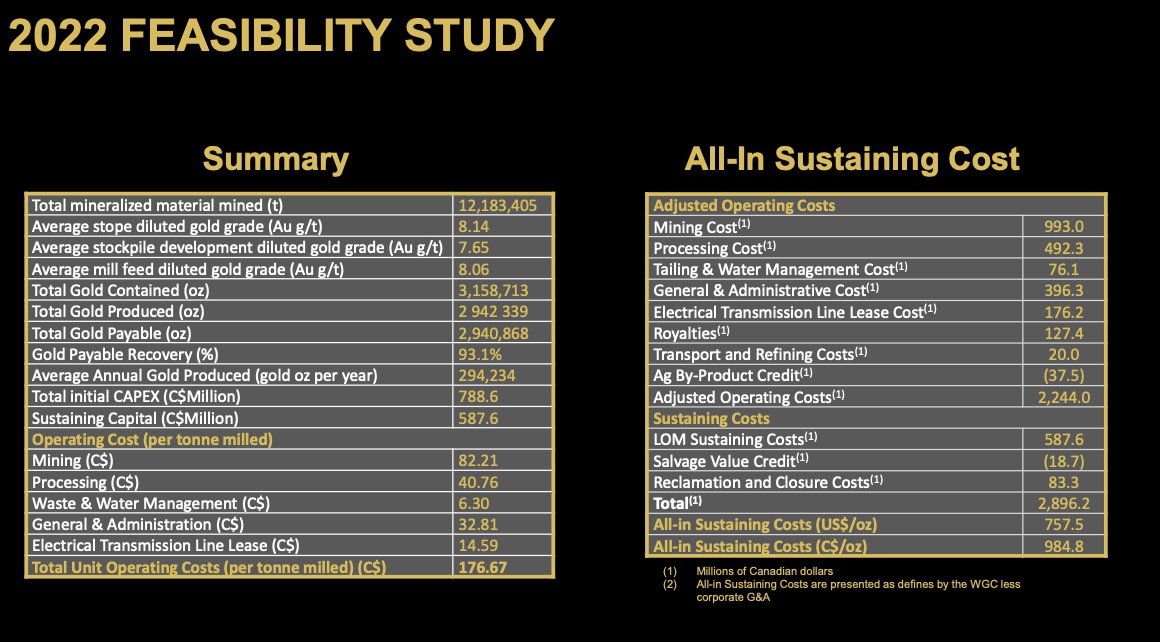

According to its feasibility study released in 2022, the project will produce an estimated 2.95 million ounces of gold over an initial 10-year mine life, averaging around 300,000 oz Au per year at industry-leading all-in sustaining cash costs of US$758/oz.

This type of deposit, with its large size and high grade, is extremely rare in the mining industry. Also note that the project's favorable location in Canada reduces permitting risk, providing an added bonus.

Furthermore, the feasibility study estimates that the project will produce around 3 million ounces of gold, which may be a very conservative estimate given Windfall's resource size (7 million ounces) and exploration potential. It's no surprise that Gold Fields, a senior producer operating in several higher-risk jurisdictions, was eager to secure this deal.

Not surprisingly, Gold Fields is not the first company to try to acquire Windfall. Previously, Northern Star Resources discussed a joint venture with Osisko, but those talks were canceled when the parties couldn't agree on funding terms.

Osisko and Gold Fields Deal: A Breakdown

Now Gold Fields steps up to the plate and acquires an interest in Windfall. Here's a summary of the news today:

-

Osisko Mining has announced a 50/50 joint venture with Gold Fields Limited on its feasibility-stage Windfall gold project.

-

Goldfields will pay a total consideration of C$600 million to acquire its interest, plus it agrees to fund C$75 million in exploration, and an additional C$34 million payment to reimburse Osisko for items it has already incurred on construction.

-

Going forward, Gold Fields and Osisko will share all pre-construction costs on a 50/50 basis.

-

When you factor in Gold Fields' contributions to construction costs and its payments to Osisko, the company has agreed to invest ~C$1.2 billion on Windfall.

-

But ultimately, the deal values the asset as its fair value based on the feasibility study results (more details below).

Why It's Not the Best Deal for Osisko

Windfall has a near-$2 billion valuation using spot gold prices. (Osisko Mining)

{kind=link}

There are some benefits to this deal from Osisko's perspective - such as the cash payments of over C$600 million combined with existing liquidity that will easily fund its capital expenditure requirements on Windfall and likely leave the company with some cash for other ventures.

Additionally, I think landing Gold Fields as a partner is a benefit, as this is a senior gold miner ($14+ billion market cap) with a proven track record. I believe Gold Fields has the deep pockets and the technical expertise to ensure Windfall not only gets into production, but succeeds as Canada's next high-grade gold mine.

While the cash payment of C$600+ million and landing Gold Fields is a win for Osisko, I feel that Gold Fields is getting the better of the deal.

First, while Gold Fields is paying fair market value for its 50% stake (based on paying 1.0X NAV, and a C$1.2 billion value for the project), this is based on an analysis that uses a long-term gold price of US$1,600/oz.

Of course, the price of gold is more than 20% higher than that, trading over US$2,000/oz, as of writing on May 2. Gold bulls like myself expect gold to trade considerably higher over the next 5-10 years, and do not like to see project's valued at much lower gold prices.

Using a long-term gold price of US$2,000/oz actually gives Windfall a valuation closer to C$2 billion, which means Gold Fields should be paying closer to C$1 billion for its 50% stake, not the approximately C$600 million it has agreed to pay. Essentially, Gold Fields is getting the asset at a 40% discount when you consider this logic.

Secondly, in my opinion, the feasibility study results seem very conservative (which is not surprising, as a feasibility study tends to be far more conservative than a PEA or PFS). The study estimates that only 2.94 million ounces of gold will be produced over a 10-year mine life.

However, this estimate is based on Windfall's current probable mineral reserves (3.15 million oz) and does not factor in any potential expansion.

{kind=link}

Given that Windfall has a resource estimate of over 7+ million ounces (and growing every year), and has consistently delivered positive infill drilling results (which "proves up" resources into reserves), it appears likely that its reserves will grow over time.

The point I'm making here is that Gold Fields is paying below fair market value for this asset at current spot gold prices, and will also benefit from the free exploration upside - which is very likely, given Windfall's past and current exploration successes.

Osisko Mining: The Final Word

I feel that Osisko Mining is giving up half of its ownership in a prime gold project at a discount. Its shares were down around 3% today on a positive day for gold miners ( GDX ) as a whole. Meanwhile, Gold Fields shares shot up by more than 5%. This stock performance leads me to believe that other investors agree with my sentiment here.

I feel that Osisko Mining's upside is somewhat limited following this deal. On the other hand, Osisko Gold Royalties ( OR ) is another clear winner from the transaction as it stands to benefit from Windfall getting to production, given its ownership of a 2-3% NSR royalty on Windfall.

For further details see:

Gold Fields Acquires 50% Of Windfall: A Fair Deal Or A Bargain?