GFIOF - Gold Fields: Earnings Upside Expected Shares May Test The High Teens Soon

2023-11-08 03:10:51 ET

Summary

- Gold miners have outperformed physical gold in the past year, suggesting a potential bull market for gold and gold miners could be in store.

- Gold Fields Limited (GFI) is a recommended buy, with upcoming production data and a decent value and EPS growth trajectory.

- GFI has mixed valuation metrics but is cheap considering its growth potential, and its technical chart shows potential for gains.

- I outline key price levels to watch ahead of production data due out next week.

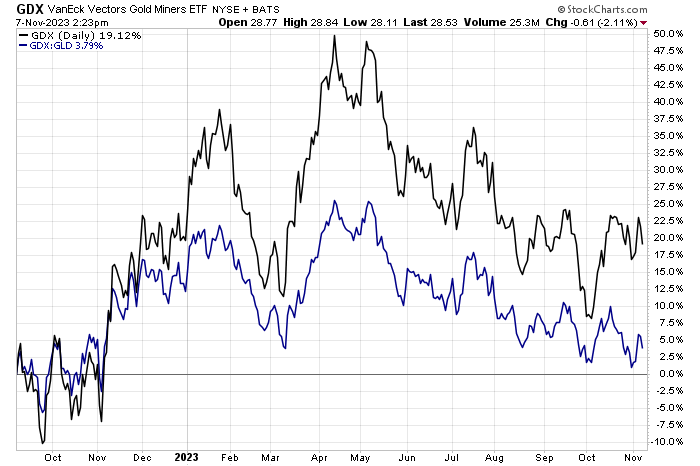

Gold miners have performed well against the precious metal over the past year-plus. The VanEck Vectors Gold Miners ETF (GDX) is up 19% in total return since September 2022 while the physical gold ETF (GLD) is up by just 15%. There's momentum here and there with the miners, and with gold now approaching its all-time highs amid geopolitical uncertainty , a new gold and gold miner bull market could be in the works.

I reiterate my buy rating on Gold Fields Limited (GFI). With key production data due out next week, volatility could be in store toward year-end, and the stock appears as a decent value with a robust EPS growth trajectory.

Gold Miners Beating Gold Since Q3 2022

{kind=link}

According to Seeking Alpha, Gold Fields operates as a gold producer with reserves and resources in Chile, South Africa, Ghana, West Africa, Australia, and Peru. The company also explores for copper deposits. It holds interests in nine operating mines, as well as gold mineral reserves and mineral resources. BofA notes that its big project, Salares Norte in Chile, is scheduled to commence commercial production in 2023 and produce c.450kozpa gold equivalent at one of the lowest AISC in the industry.

The South Africa-based $12.5 billion market cap Gold industry company within the Materials sector trades at a near-market 19.2 trailing 12-month GAAP price-to-earnings ratio and pays a 3.0% trailing 12-month dividend yield. Ahead of key data due out next week, shares trade with a high 42% implied volatility percentage.

Back in August, there was drama with GFI. 1H23 earnings were weaker than expected. Net profits verified at $458 million versus more than $508 million in the same period a year earlier. Headline EPS tumbled from $0.58 to $0.51, but that was merely in line with guidance. Along with declaring an interim dividend of $0.17, CFO Paul Schmidt announced his retirement after 27 years with the firm. The stock fell hard on the earnings date, but shares are higher since then, though not before notching a multi-month low a month ago.

Shortly after GFI bottomed out on the price chart, analysts at JPMorgan upgraded the gold producer to Neutral given the bank's bullish stance on where it sees gold prices headed over the coming 12 months.

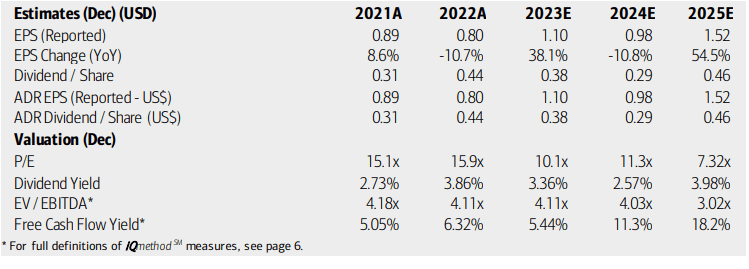

On valuation , analysts at BofA see earnings near $1.10 this year before per-share profit growth returns in the out years. The current consensus outlook calls for $1.26 of FY 2024 operating EPS and $1.58 in '25, suggesting sequential growth. Dividends, meanwhile, are expected to vary with earnings, so income investors should take that into account when analyzing this international firm. The forward earnings multiple profile on GFI continues to look favorable, particularly considering its improved balance sheet. Moreover, free cash flow is seen as rising considerably in the coming periods.

Gold Fields: Earnings, Valuation, Dividend, Free Cash Flow Forecasts

{kind=link}

If we apply the stock's 5-year historical average P/E and assume 2024 EPS of $1.26, then we are talking about a stock price that should be near $26. Of course, higher interest rates put pressure on the earnings multiple, but gold near $1970 per ounce with positive technicals could auger for a more premium P/E.

I assert that a high-teens P/E is more appropriate, particularly given the company's healthy earnings growth outlook. Finally, on an EV/EBITDA basis, GFI does not look all that pricey. Putting it all together, given these generally decent valuation metrics, a stock price in the high teens is fair in my view. High volatility in the challenging gold industry makes me hesitant to suggest the stock should be north of $20.

GFI: Mixed Valuation Metrics, Cheap Considering Growth

Seeking Alpha

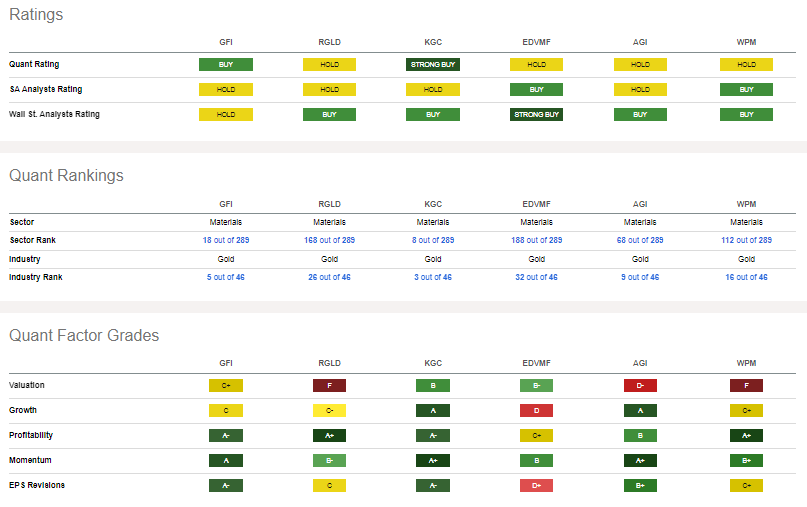

Compared to its peers , GFI features a relatively positive quant factor grade. As detailed earlier, the valuation is mixed, but the growth picture is sanguine in my view given strong earnings trends ahead. With a history of robust profitability and generally positive share-price momentum trends, there are reasons to like this slice of the gold miner market. Finally, EPS revisions have been strong following a pair of semi-annual earnings beats.

Competitor Analysis

{kind=link}

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2023 interim production release date of Thursday, November 16. The next earnings date is for 2H23, but that is not until late February.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

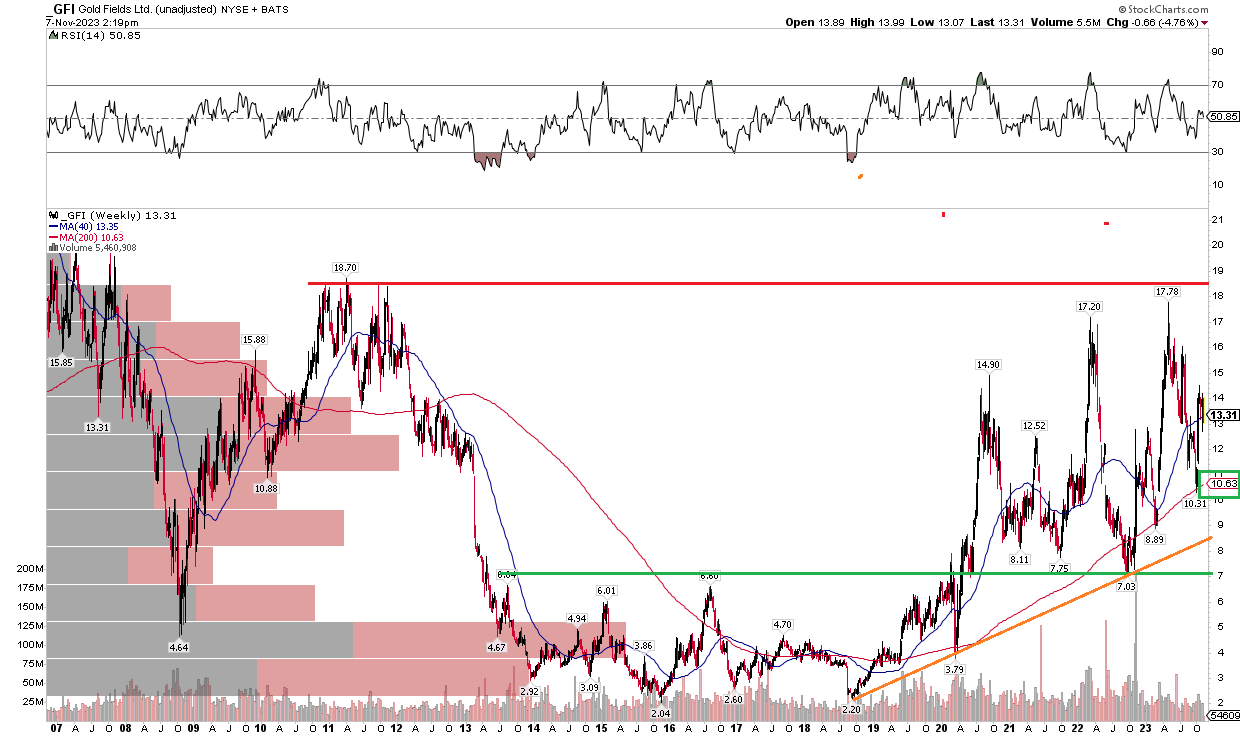

Readers know that I typically home in on the last three years of a stock chart to assess technical trends. In this case, I went back many years and used the weekly zoom. Notice in the chart below that shares have a very wide trading range that has persisted since 2020. I see support near $7 while resistance appears at the $18 mark.

The positive aspect here is that the long-term 200-week moving average has been a decent spot to enter GFI from the long side - the stock touched that trend indicator just a few weeks ago. I would not be surprised to see shares test the high over the coming months based on the broad uptrend off a low notched in 2018. For now, long with a stop under $7 would make sense, but that is a lot of risk to be put on the table. A better idea is to use the October low of $10.31 as your bogey - a top under $10 is a more risk-focused way to own this one, but gains should still be harvested in the upper teens.

Overall, the trend over the last few years is higher while a longer view of GFI shows clear resistance near $18 that should be acknowledged by the bulls.

GFI: Long-Term Trading Range Between $7 and $18

{kind=link}

The Bottom Line

I reiterate my buy rating on GFI. The valuation is fair today, and a robust earnings growth trajectory makes this risky stock appear undervalued to me. Furthermore, the chart is not particularly bad with relatively strong momentum.

For further details see:

Gold Fields: Earnings Upside Expected, Shares May Test The High Teens Soon