GORO - Gold Resources Is In A Tight Spot

2023-03-30 08:50:33 ET

Summary

- Gold Resources has been producing but declining multimineral mines in Mexico and a questioned gold project in Michigan.

- The company is facing the decline of its profit-generating center and is currently unable to cover corporate expenses and the development expenses of the Michigan project.

- Exploration in adjacent Mexican properties has not been successful, and the Michigan project is several years away.

- Further, the company assumed significant liabilities when acquiring the Michigan project, which could eventually lead to recourse on a key asset.

- Under these conditions, the company is too risky for a long-term investment.

Gold Resource Corp ( GORO ) is an American mining explorer, developer, and producer. Its revenue-generating properties are in Oaxaca, Mexico, and it has an exploration project in Michigan.

The company features a history of mining exploration successes, with the discovery and profitable exploration of the current mines in Mexico and spun-off properties in Nevada, now Fortitude Gold ( OTCQB:FTCO ).

However, the company is now led by a different team, the Mexico properties are losing steam, and the company acquired a project in Michigan with serious development risks at a significant price.

Given the company's current status, I consider the stock too risky for future opportunities to compensate them.

Note: Unless otherwise stated, all information has been obtained from GORO's filings with the SEC .

Business description

A history of mining success : GORO was IPO'd in 2006 to explore property mines in Oaxaca, Mexico. The company's first mine operated in 2011 in the same region (the Arista mine). In 2015 the company purchased exploration properties in Nevada that were producing by 2019. In 2020, GORO spun off the Nevada properties to form Fortitude Gold.

This has been a relatively successful story for the short time the company has existed, marked by a period of depressed prices.

Historical management change : The management team that led the company for the aforementioned period moved to FTCO in 2020, and a new managerial team arrived. The main actors of the story (CEO, COO, Chief Exploration Officer, and Chief Business Development Officer) all went to FTCO.

Declining Don David mines : GORO's only revenue center is the Don David mines complex.

The Arista mine, located in Oaxaca, Mexico, produces most of the company's revenues and was the company's first mine. The mine is declining, with its open pit closed in 2021 and no new discoveries despite significant investments in exploration. Proven reserves are only 1/10th of the reserves in 2018 .

The company is currently producing and exploring at another mine as well, the Alta Gracia mine (previously named Mirador), but the development is not generating the same results as in Arista. This mine is also declining, with one-third of the proven resources listed in 2018.

The complex produces gold, silver, copper, lead, and zinc. Gold and zinc have historically represented more than 60%, and today more than 75% of the mine's revenues.

The complex includes three other properties, but exploration is only in the initial stages. The most explored of these properties (called El Rey, with 5 kilometers of drills) has been stopped since 2012 because of problems with the local communities.

The company's declining production can be observed in the lower gross margins, despite higher commodity prices, particularly for gold and zinc.

A risky acquisition : In December 2021, under the new managerial team, GORO decided to acquire Aquila, a company with a single project in Michigan called the Back Forty Project.

The B40 project is a sufficiently explored open pit gold mine project in Menominee County, Michigan. The mine was preparing to issue feasibility studies, but a Michigan judge revoked the water license of the mine based on the claims from the Menominee Tribe of Wisconsin , WTI.

The tribe considers that the lands are sacred, that the development is too close to the Menominee river, and that it should not be allowed. The Tribe is also trying to add a portion of the mine to the Register of National Historic Places and for the U.S. Army Corp of Engineers to mark the Menominee river as navigable, requiring the B40 project to receive approval from the Army Corp of Engineers as well .

The last mine approval in Michigan was in 2011, and before that, 1912 . Further, Eagle Mine, approved in 2011, is an underground mine, not an open pit mine. The original B40 project was an open pit mine, but now the company is considering an underground mine (more expensive).

GORO spent $9 million in 2022 to prepare a new feasibility study for the B40 project but has concluded that it is too expensive. The project is extremely risky.

The acquisition was pricy : Aquila was acquired in a shares-based deal valued at $24 million in GORO shares, but the actual cost of the company could be as high as $80 million because of the liabilities of the company.

In particular, Aquila had received $37 million in revenue streams from Osisko Bermuda Limited (Osisko). In exchange for that money, Aquila committed to selling future gold and silver supplies from B40 at a deeply discounted price to Osisko. The agreement indicates that 85% of silver production has to be sold at $4/oz. and 18% of gold has to be sold at 30% of the market price of gold with a ceiling of $600/oz.

In the agreement for the gold sales , the commercial commencement date is redacted, but Osisko has recourse to the project's assets and to claim back the revenue streams, plus interest of 10% from the CC date. Today the original $37 million already represent a $43 million liability, which elevates the Aquila acquisition price to $67 million.

Aquila also owed a contingent consideration of $4 million to its previous partner Hudbay Minerals ( HBM ). If the contingencies are not met, or the payment is not made, HBM has the right to reacquire its stake in B40. GORO's management has disclosed that it plans to pay the $4 million to HBM.

Finally, Aquila had deferred tax liabilities for $16 million and cash and securities for $5 million. The all-in purchase consideration is $82 million, not $24 million.

Valuation

Exploration and development projects : Currently, GORO has three purely exploratory properties in Mexico and the B40 project in Michigan. The Mexico properties have barely been explored and are not worth much.

The B40 project, on the other hand, has been explored, and ore deposits found, but its final authorization is questioned. The company's management has been ambiguous regarding timelines in its latest earnings call . According to management, costs are too high. The company will probably not spend as much on B40 next year.

When GORO decides to move on, it still has to fill a new authorization process (which may take years) and, if approved, start the investment process. Production from B40 is several years away, and much of the production is already committed to Osisko at loss-generating prices.

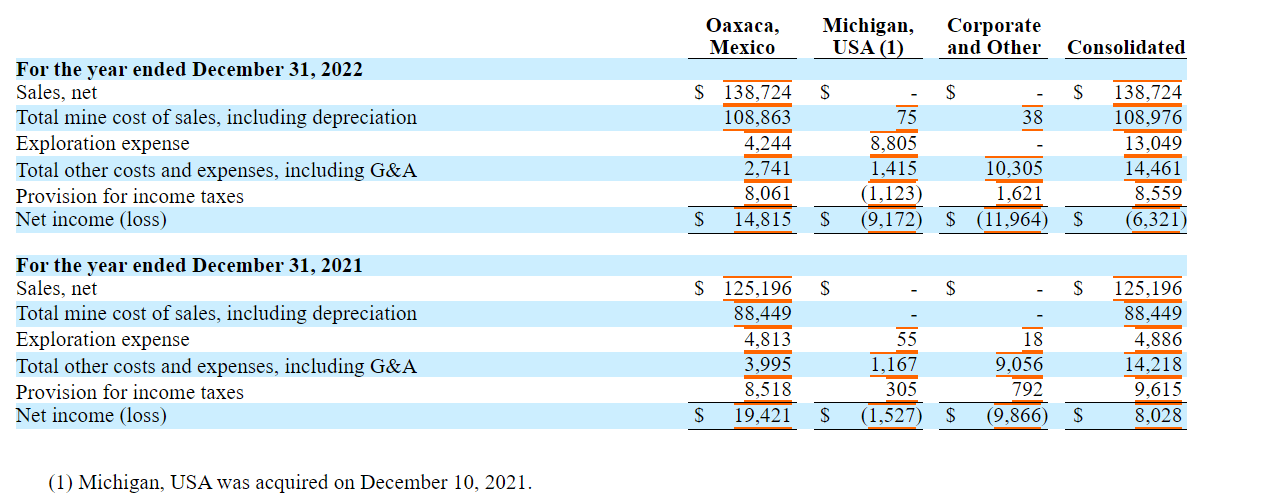

The Don David mines : These mines are productive but decreasing. The company milled 500 thousand tons of ore in FY22, and total reserves are only 1.5 million tons, meaning only a few years of production unless more veins are found.

Further, the mines must cover substantial corporate expenses of as much as $10 million in FY22 ($4 million alone in managerial compensation). In FY22, most of the mine's net profits (after accounting for 37.5% income taxes in Mexico plus 10% withholding taxes on dividends) were consumed in corporate expenses.

GORO's profit and cost centers FY22 and FY21 (GORO's FY22 10-K)

{kind=link}

Liabilities : The company will have to pay $4 million to HBM in November 2023 because, otherwise, HBM will own the right to repurchase 50% of the B40 project.

If the (undisclosed) commercial commencement date of the stream sale agreements with Osisko is reached and the B40 project is not producing, GORO may face an event of default on the $43 million owed to Osisko. Osisko would at least have recourse to the B40 assets and maybe also to some of the company's other assets.

Conclusions

GORO is in a difficult position, the company's main profit center is decaying, and recent exploration is not revealing more resources. Most of the profits generated by the Oaxaca mines are consumed at the corporate level, and the company is not implementing cost containment measures.

The company's future is significantly tied to the authorization of the B40 project in Michigan. Local communities heavily combat the project, and it is unclear if it will ever reach commercial operation. If it does, it will take years to generate revenues and many more to generate profits (because of the Osisko stream agreements).

Further, the company took significant liabilities as part of the B40 project acquisition, which has compromised its future capacity to invest in this or other projects.

Finally, the managerial team that led GORO's relatively successful decade between 2008 and 2020 is now leading FTCO, and GORO's managerial team does not have such a track record.

I do not believe GORO represents an opportunity under these conditions.

For further details see:

Gold Resources Is In A Tight Spot