AEM:CC - Gold Royalty Corp.: Exploration Success Continues At Key Royalty Assets

2023-12-03 02:36:58 ET

Summary

- Gold Royalty Corporation reported better Q3 results with a lower net loss, higher total revenue & land agreement proceeds, and a large increase in its royalty portfolio.

- Just as importantly, the company looks like it will benefit from a much higher realized gold price as it enjoys hockey-stick like growth in attributable GEO production.

- In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies.

The Q3 Earnings Season has come to an end and one of the first companies to report its results was Gold Royalty Corporation ( GROY ). Overall, the company had a better quarter sequentially with a lower adjusted net loss and much higher total revenue and land agreement proceeds, as well as an ~11% increase in total royalties (SOQUEM, Cozamin + royalty generation). Just as importantly, we saw several positive developments across its royalty portfolio, and the company is in the favorable position of benefiting from a record average realized gold price just as it starts to see a ramp up in attributable gold-equivalent ounce [GEO] production. In this update, we'll dig into the Q3 results, recent developments, and whether the stock is still in a low-risk buy zone.

All figures are in United States Dollars.

{kind=link}

Granite Creek Mine Portal & Mineralization (GROY 10% NPI) - i-80 Gold Website

Q3 Results

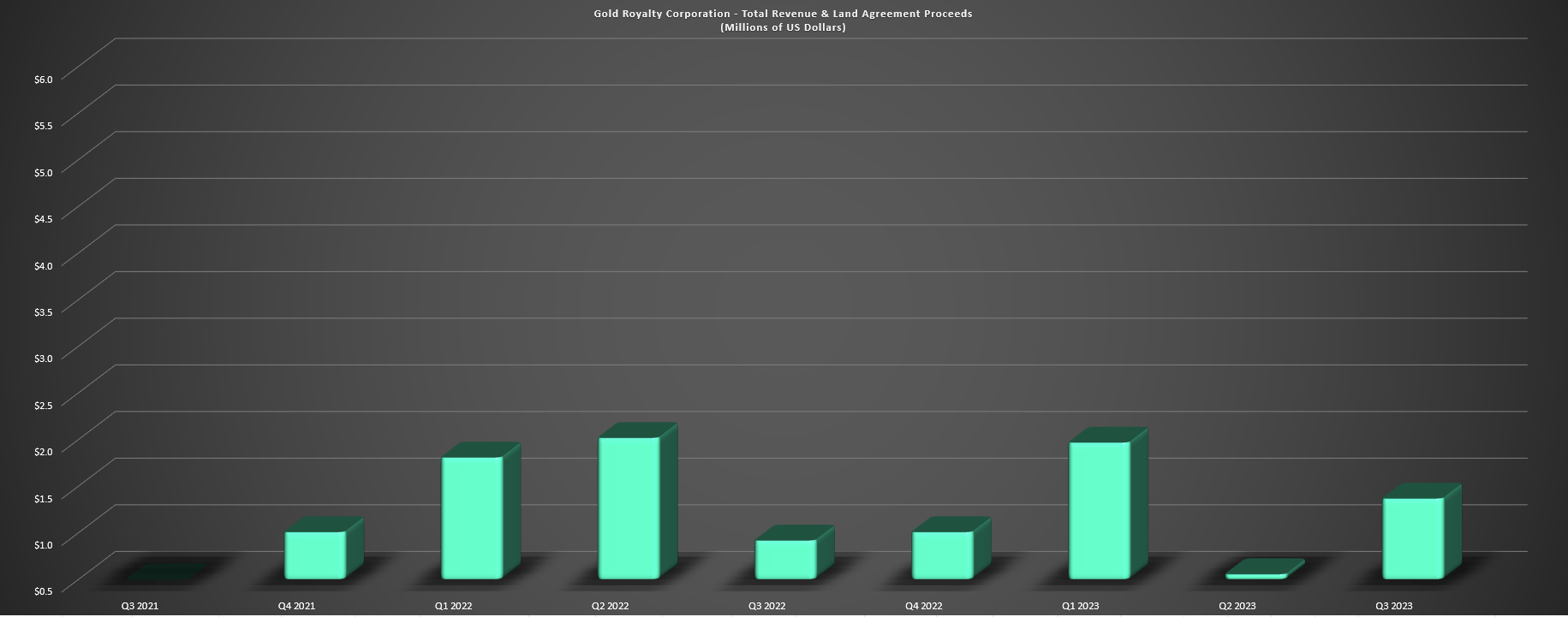

Gold Royalty Corporation ("GRC") released its Q3 results last month, reporting slightly lower quarterly revenue of ~$0.8 million year-over-year (Q3 2022: ~$0.90 million), but 48% growth in total revenue and land use agreement proceeds. This was driven by new revenue from Cozamin in the period (~$440,000) offset by no revenue from Jerritt Canyon (care & maintenance) where the company had to lap a ~$130,000 headwind in the period (asset was producing last year). On a positive note, this increase in revenue and land agreement proceeds also translated to an improvement in operating cash flow before working capital changes which was [-] ~$0.9 million vs. [-] ~$2.7 million in the year-ago period. The company noted that it has worked to reduce costs, including a $0.1 million improvement in office/technology expenses (streamlining administrative activities) and a $0.40 million decline in investor communication/marketing expenses by " a refocus on select higher value-added market activities ".

{kind=link}

Gold Royalty Corp - Total Revenue & Land Agreement Proceeds - Company Filings, Author's Chart

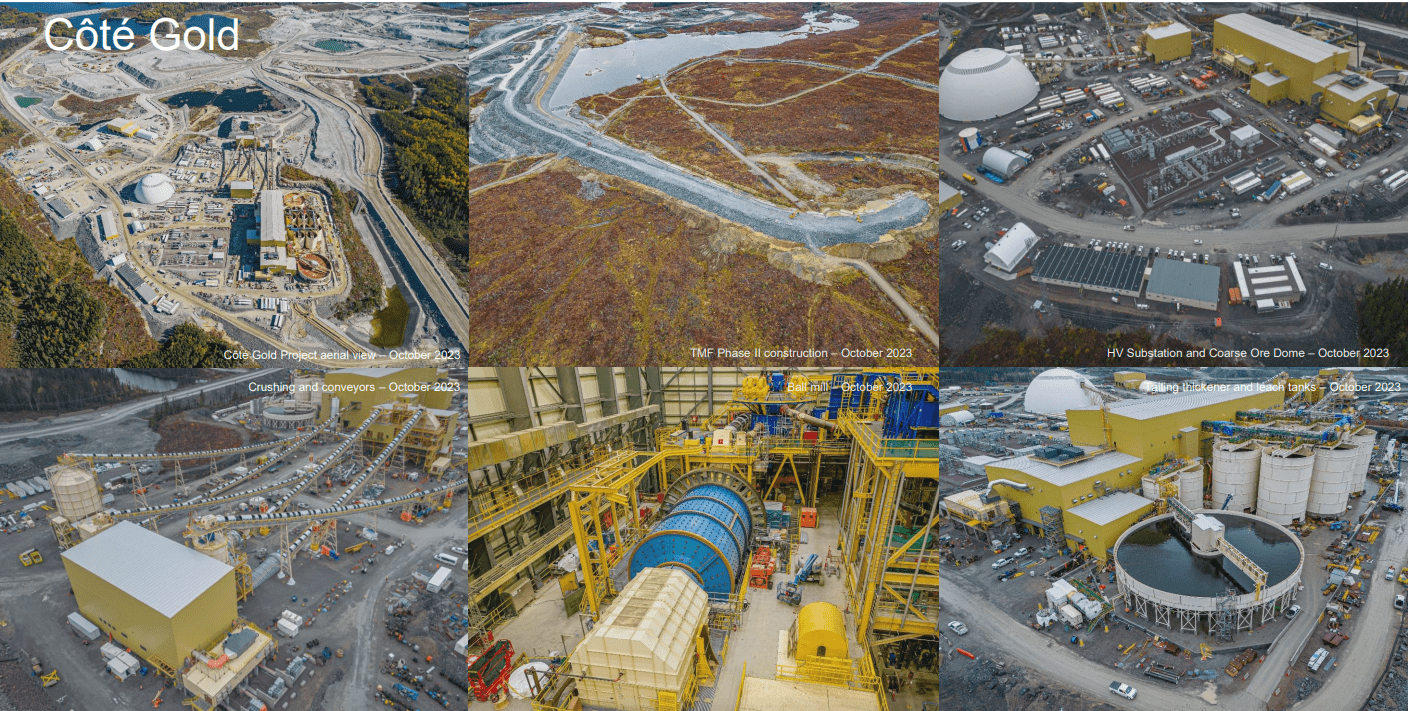

In a period where larger royalty companies are generating considerable cash flow per quarter like Osisko Gold Royalties ( OR ) with ~$33 million of operating cash flow in Q3, GRC's results might leave a lot to be desired, and it's not ideal to see the company still reporting net losses. However, its financial metrics are finally trending in the right direction and 2024 will mark an inflection point for the company. This is because Cote Gold is progressing well (92% complete as of the end of Q3) with over four million tonnes of stockpiles to de-risk the ramp up as of October, with first production in early 2024. For those unfamiliar, GRC has a 0.75% NSR on the earlier and higher-grade portion of the mine life which will lead to significant growth in GRC's annual revenue, cash flow, and attributable GEOs earned per share in 2024 and especially 2025 (full year of contribution). Plus, GRC will also benefit from a full year of production from Cozamin in 2024 and a meaningful step-up in contribution from the Canadian Malartic Complex if internal zones can continue to deliver.

{kind=link}

Cote Gold Construction Progress - Iamgold Presentation

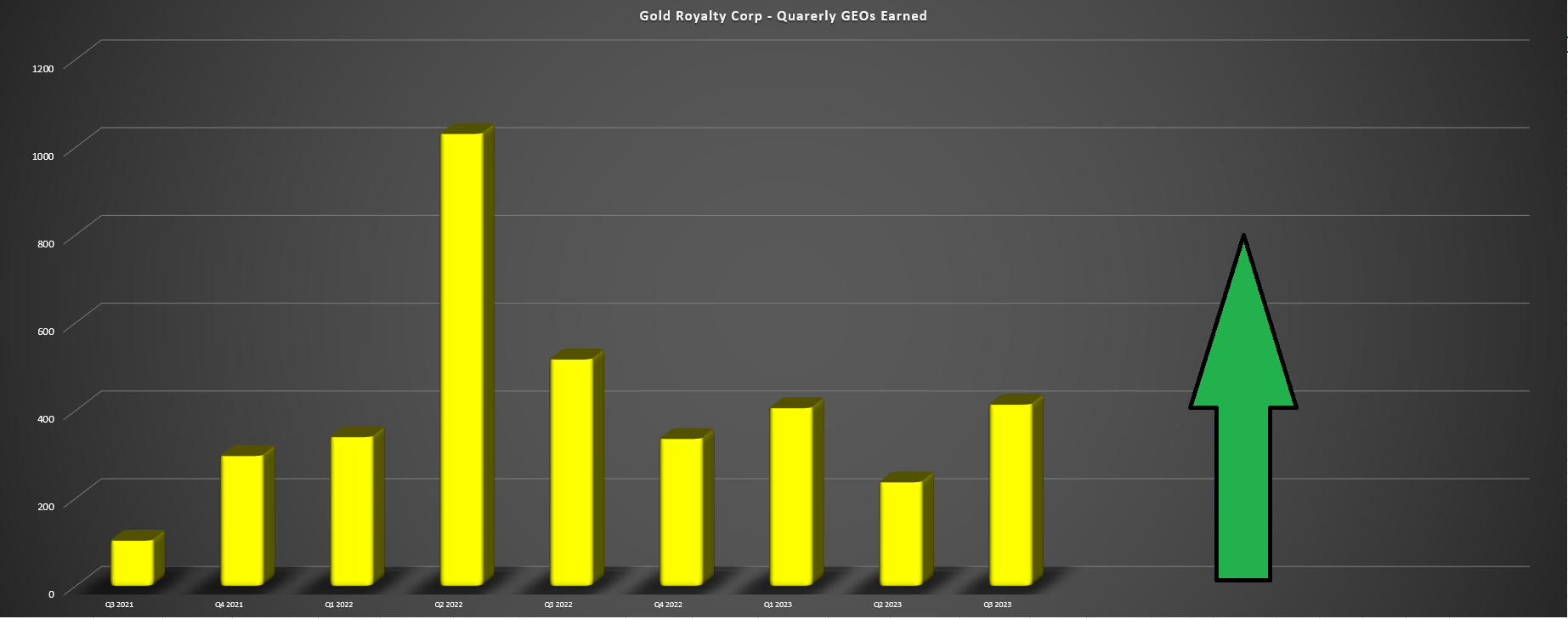

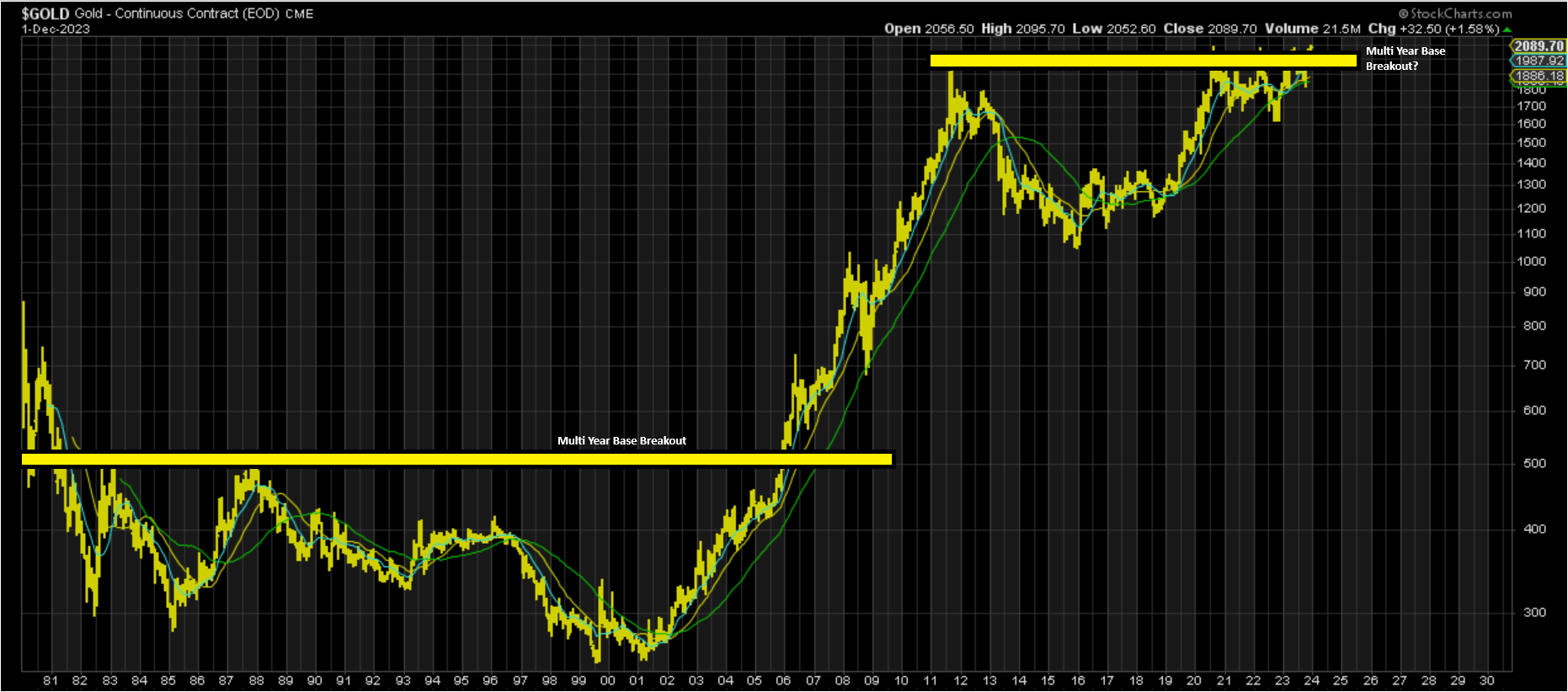

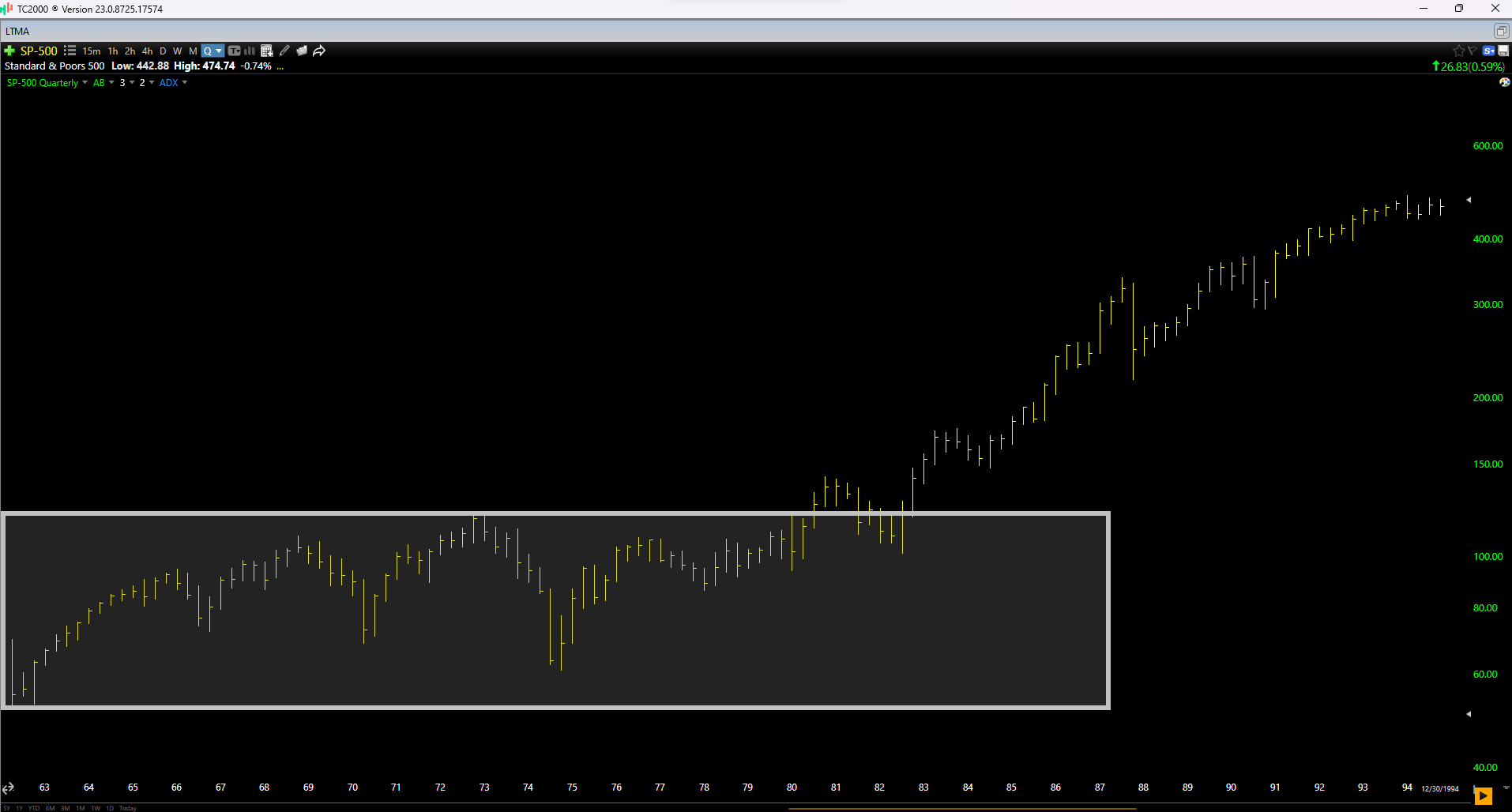

Based on the higher average realized gold price (Q3 2023: $1,927/oz and $1,931/oz year-to-date) and this significant increase in attributable GEO production, with further growth in 2025, which should ultimately translate to ~$7.0 million in cash flow in operating cash flow in 2025. And while this still leaves GRC trading at a high double-digit P/CF multiple on two-year forward estimates, the company certainly has a tailwind in the gold price that could improve this figure. This is because the price of gold is working on a multi-year base breakout which is the most significant since its 2006 breakout, and one of the largest base breakouts for an asset class coupled with new all-time highs since the S&P 500's ( SPY ) breakout in 1980 (this preceded a re-test of the highs and then a 15+ year bull market). Hence, if the gold price can see follow-through to this breakout, we could certainly see a meaningful beat on these estimates of $7.0 million in 2025.

{kind=link}

Gold Royalty Corp - Quarterly GEOs Earned - Company Filings, Author's Chart

{kind=link}

Monthly Gold Price - StockCharts.com

{kind=link}

S&P-500 Quarterly Chart - Worden

Although this is positive news, investors in smaller royalty/streaming companies should pay the most attention to exploration results, development progress, and resource/reserve growth given that positive developments here can really move the needle from a future attributable GEO production and NAV standpoint. And in the case of GRC, it continues to see significant dollars spent on assets where it holds royalties, with its royalties being on #1 and #2 assets for several operators (Cote, Cozamin, Carlin Complex, Canadian Malartic Complex, Granite Creek, County Line, Railroad-Pinion) and with most of these assets in Tier-1 ranked jurisdictions. This is a favorable position to be in given what we recently saw from Franco-Nevada ( FNV ) which is a potential massive hit to cash flow near-term and NAV with Cobre Panama going into arbitration with the contract deemed unconstitutional.

Recent Developments

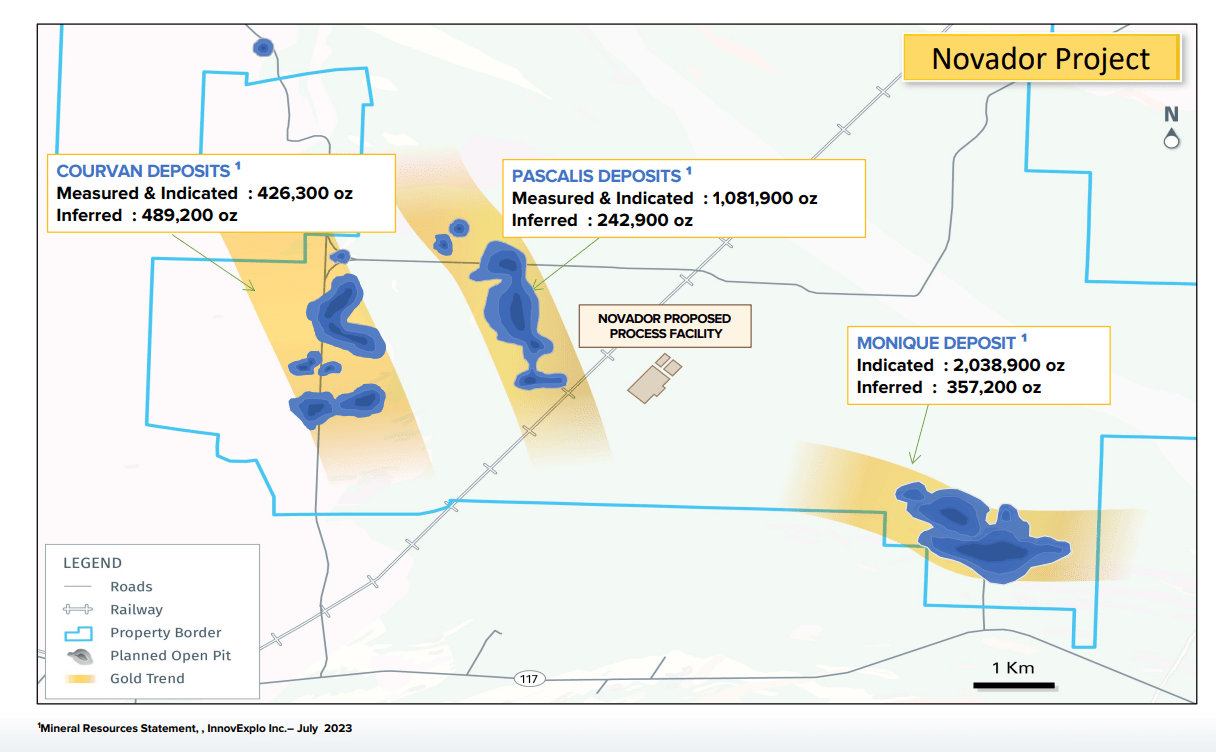

As for recent developments, GRC added 22 new royalties to increase its royalty exposure in Quebec during Q3 with the SOQUEM portfolio with most of these assets being either early exploration or advanced exploration. The company paid just ~$0.7 million to acquire this portfolio which translates to ~$31,000 per royalty paid with GRC shares (plus a milestone payment of ~$0.7 million if a PEA is completed on the Detour Project owned by Probe Gold PROBF). One of the more attractive royalties within the SOQUEM portfolio include Monique (0.38% NSR) which is the largest future pit on part of Probe Gold's ( PROBF ) larger Novador Project (~4.6 million ounces of gold), and it's worth noting that total potential buyback and milestone payments on the portfolio total ~$13 million, with SOQUEM entitled to 50% of buybacks proceeds received. Hence, in a best-case scenario, the buybacks and milestone proceeds will pay for the acquisition 2-3x over while the optionality on these royalty assets is free.

{kind=link}

Novador Project - Probe Gold

Canadian Malartic Complex

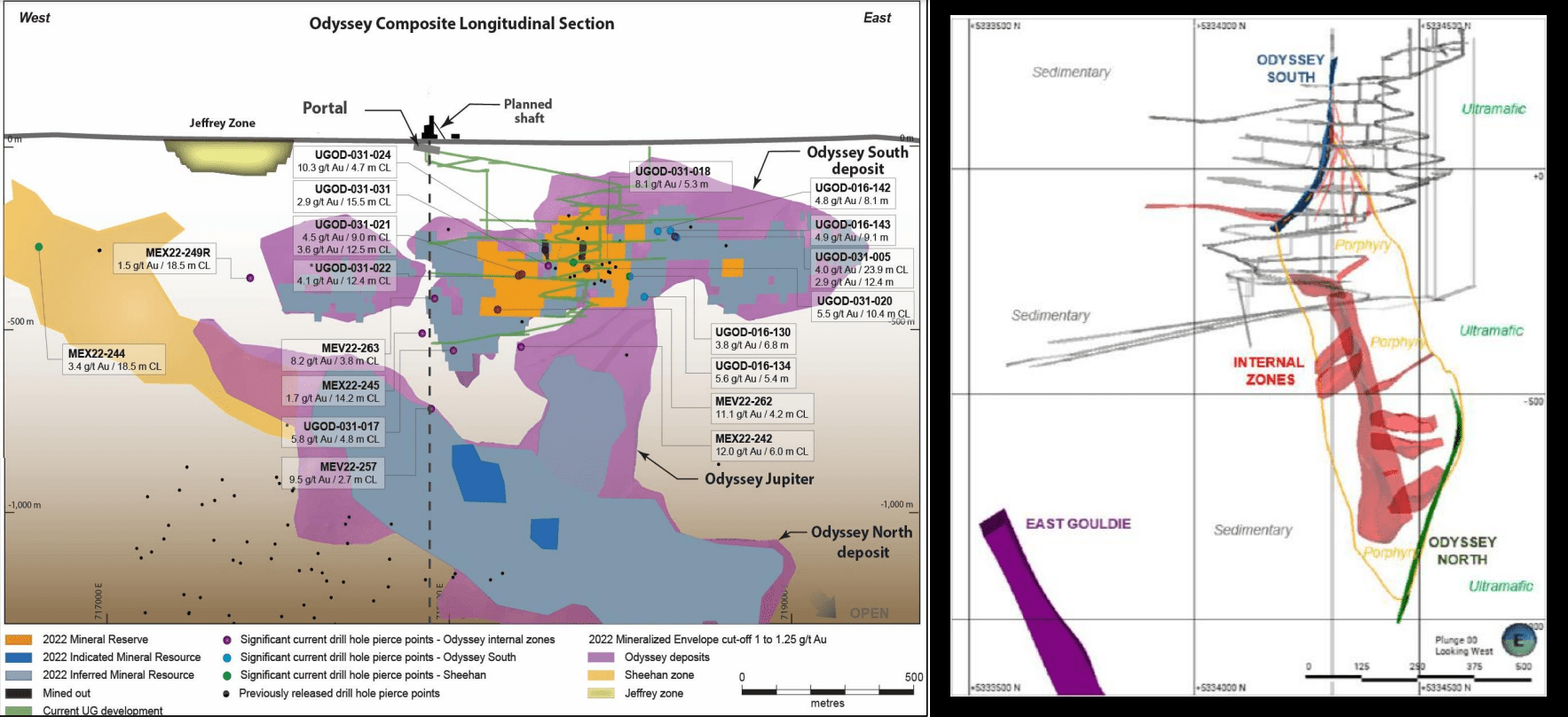

Moving over to assets in production/development, Agnico Eagle ( AEM ) continues to make progress at its massive and growing Odyssey Underground (Canadian Malartic Complex), with the paste plant commissioning on track for Q3 (allowing for a ramp-up to 3,500 tonne per day mining rates) and surface construction for Odyssey is 60% complete. To date, shaft sinking is at 130 meters and ramp development was ahead of schedule at ~650 meters, and Agnico is confident it can achieve 1,200 meter monthly development rates next year. The other positive update for GRC is that Agnico has enjoyed an 18% positive reconciliation in its first four stopes at Odyssey and is drilling to better model internal zones which could provide upside from a grade/tonnage standpoint at Odyssey South. This is excellent news for GRC as it could increase attributable GEOs earned in the 2024-2028 transition period (switch from open-pit to solely underground mining) and provide bonus cash flow ahead of the eventual ramp-up to ~19,000 tonnes per day.

{kind=link}

Odyssey Long Section & Internal Zones - Agnico Eagle Website

Granite Creek & Nevada Royalties

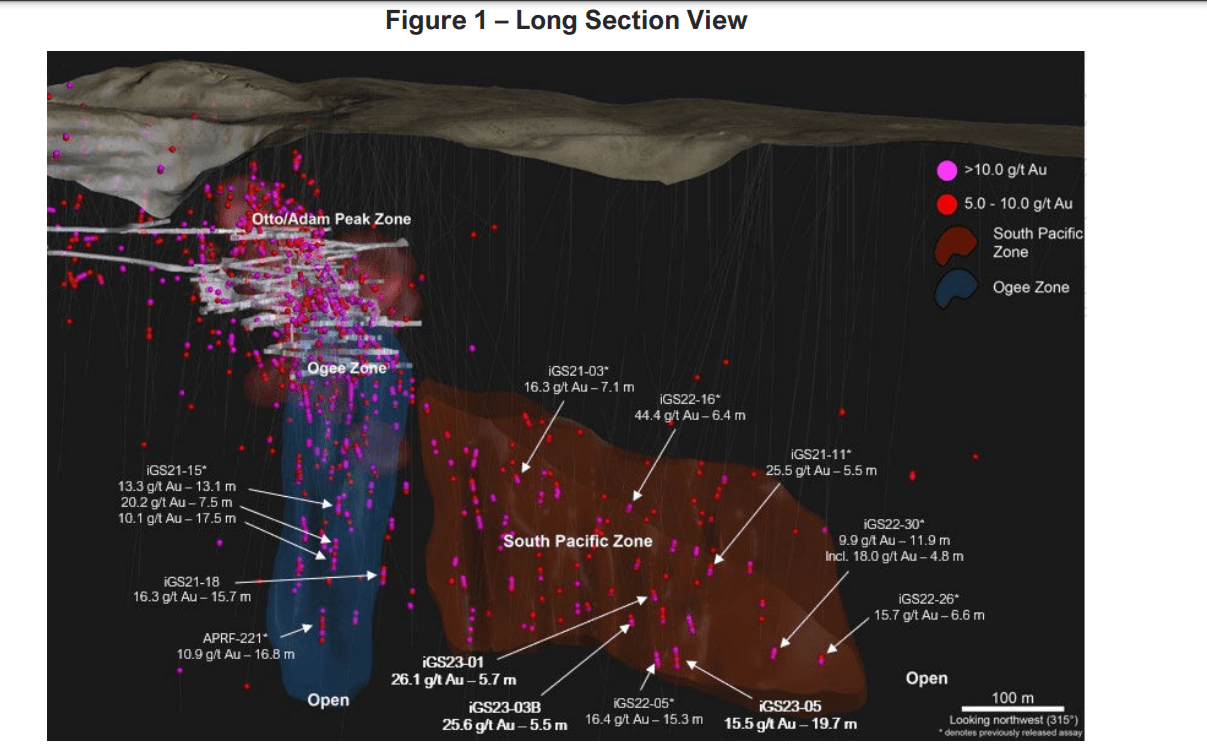

As for Granite Creek which is held by i-80 Gold ( IAUX ) where GRC has a 10% NPI after the 120,000 ounce production threshold is met, there's lots to be excited about here as well. In regards to development, the sixth level is now under development with positive grade reconciliation in the first two levels mined to date, and i-80 Gold is targeting first stope ore in Q1 2024 at the South Pacific Zone [SPZ]. For those unfamiliar, the SPZ has better continuity, is primarily sulfide, and appears to have more favorable ground conditions, in addition to 10.0+ gram per ton grades. So, assuming a successful ramp-up to 700 ton per day mining rates by H2-24, we should see up 50,000+ ounces produced next year company-wide, improving to 75,000+ ounces in 2025 (full year of higher mining rates), resulting in meaningful cash flow to GRC in 2025 assuming gold prices stay at or above spot levels.

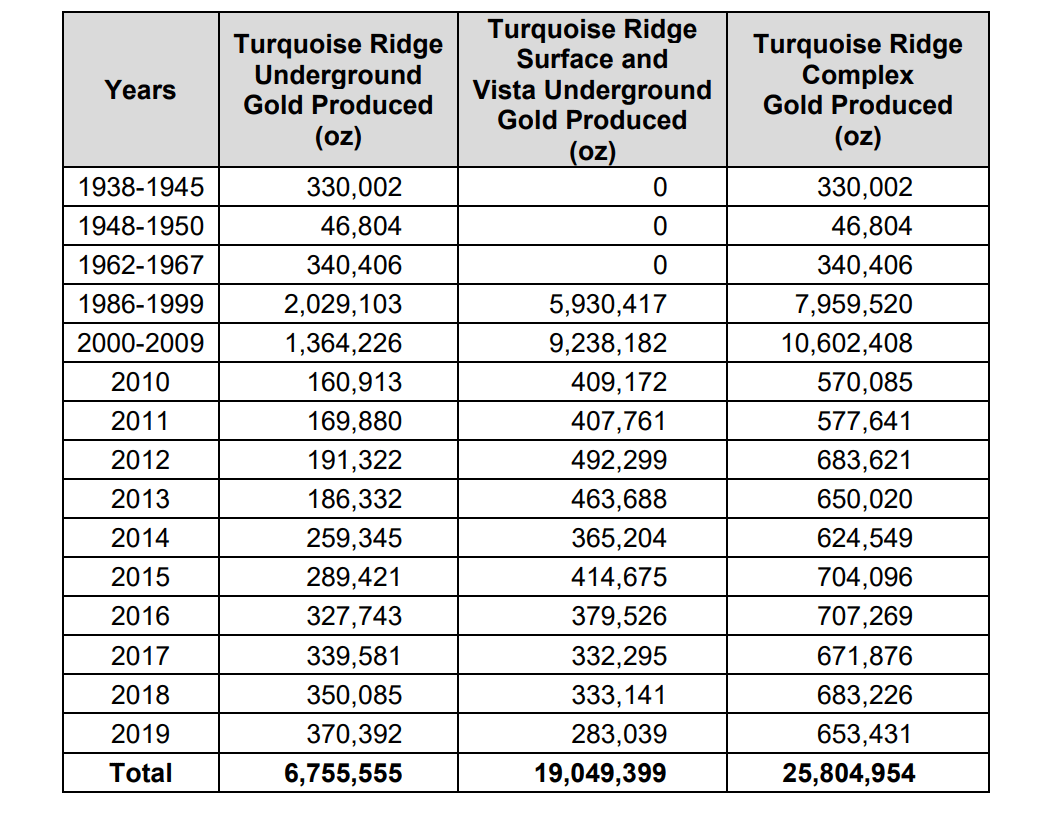

Notably, recent drilling hit an impressive 5.7 meters at 26.1 grams per tonne of gold, 5.5 meters at 25.6 grams per tonne of gold, and 15.5 meters at 19.7 grams per tonne of gold, and August was a record month with ~18,400 tons mined or 592 tons per day. Not only are these results among the best grades at Granite Creek to date, but they de-risk mining at South Pacific with confirmation of continuity of mineralization and the South Pacific Zone is wide open to the north towards the massive Turquoise Ridge Complex (historical underground only production of 7.0+ million ounces to date). Hence, I ultimately think there's the potential for Granite Creek to grow from a ~500,000 ounce resource to 1.9 to 2.5 million ounces by year-end 2026 (resulting in a substantial reserve base) which would give GRC a nice payback on its 10% net profits interest once it starts paying.

{kind=link}

Ogee Zone & South Pacific Zone - i-80 Gold

{kind=link}

Turquoise Ridge Historical Production Up To 2019 - 2020 TR

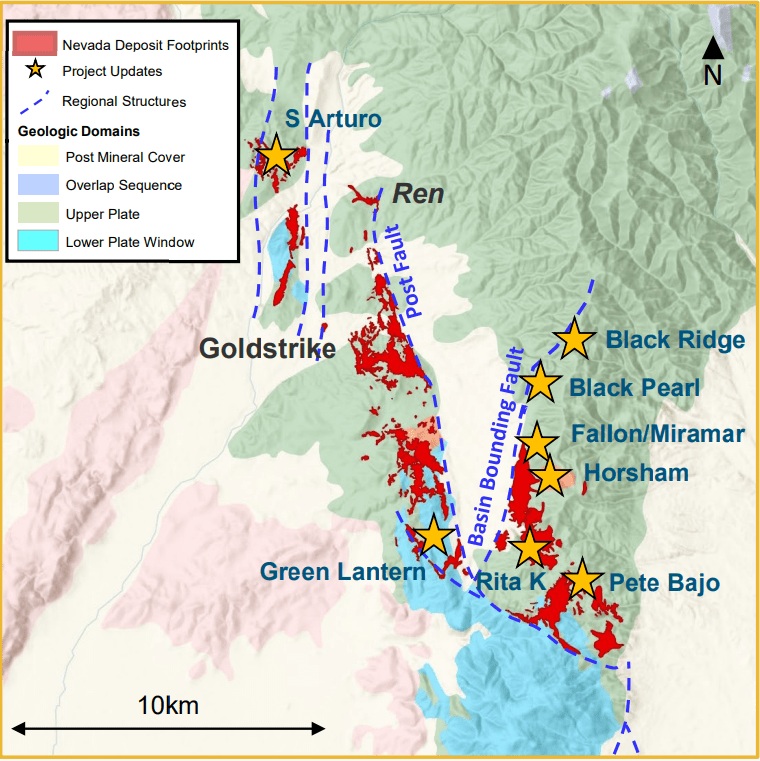

Finally, while Gold Rock has likely been pushed out by Calibre ( CXBMF ) if it succeeds in its recent takeover offer, the addition of ~200,000-ounce asset will ultimately increase Calibre's cash flow and give it significantly more capital to drill aggressively and ultimately look to build a larger operation in Nevada to diversify itself away from Nicaragua. So, although this may impact Gold Rock's start date near-term, I don't see this development as a negative for GRC's royalty on Gold Rock from a bigger picture standpoint. And while in Nevada, the issues in Panama for Franco-Nevada may lead to Orla ( ORLA ) directing more exploration/development dollars to Mexico/Nevada, ultimately benefiting GRC's royalty on Railroad-Pinion which should begin production by 2027. Last, but certainly not least, REN could head into production by the end of the decade with the West Barrel layback pulled forward to support infrastructure and a PFS expected in 2026. The latter will be a positive catalyst for GRC if the details are closed as it will make modeling this asset easier and allow analysts to better estimate future cash flows from GRC's 3.5% NPI and 1.5% NSR.

{kind=link}

REN Project (Carlin Complex) - Nevada Gold Mines

Valuation

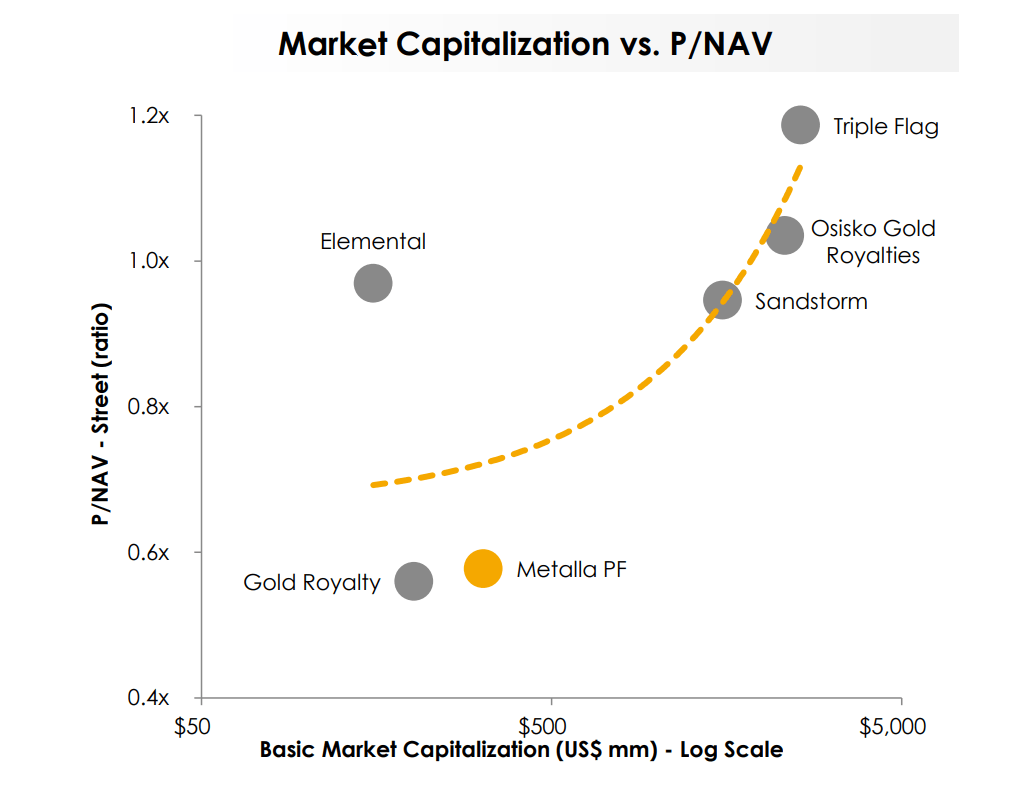

Based on an estimated ~155 million fully diluted shares (year-end 2024, excluding warrants) and a share price of $1.60, Gold Royalty Corporation trades at a market cap of ~$250 million and an enterprise value of ~$265 million. This makes it one of the lower capitalization names within its peer group, partially justified by its relatively low revenue generation with the company on track to generate less than $7.5 million in revenue and land agreement proceeds this year. That said, the company's 2023 do not do the company justice, and a better way to value smaller royalty/streaming companies that are waiting to scale is on P/NAV vs. trailing revenue. And with an estimated net asset value of ~$415 million (conservative value of royalty assets minus net debt and corporate G&A), GRC is trading at ~0.60x P/NAV which is one of the lowest multiples sector-wide. This is especially true given that GRC resembles Osisko Gold Royalties ((OR)) more than any of its peers, with its flagship asset being royalties on Agnico Eagle's future largest mine once optimized (Canadian Malartic Complex) and a most of its NAV and production coming from Tier-1 ranked jurisdictions.

{kind=link}

Smaller Royalty/Streaming Companies Market Cap vs. P/NAV Multiple - Metalla Presentation

Using what I believe to be a more conservative multiple of 0.90x NAV to reflect the fact that most of its assets are in the development stage and that GRC is a much smaller name by scale, I see a fair value for the stock of ~$374 million which translates to a fair value of US$2.42 per share. Hence, despite the recent rally in the stock, I continue to see a 52% upside to fair value. Plus, it's worth noting that fair value estimate is likely going to prove conservative if gold continues its upward trajectory given that we saw small-cap royalty/streaming companies like Ely Gold Royalties and Metalla ( MTA ) trade above 1.50x NAV ahead of their peaks, and there's upside to GRC's NAV if we start to model $1,950/oz gold price assumptions long-term being the more likely reality. To summarize, while I see 55% upside to fair value from current levels, a case can certainly be made for GROY to trade back above US$3.00 in a gold bull market.

So, is the stock a Buy?

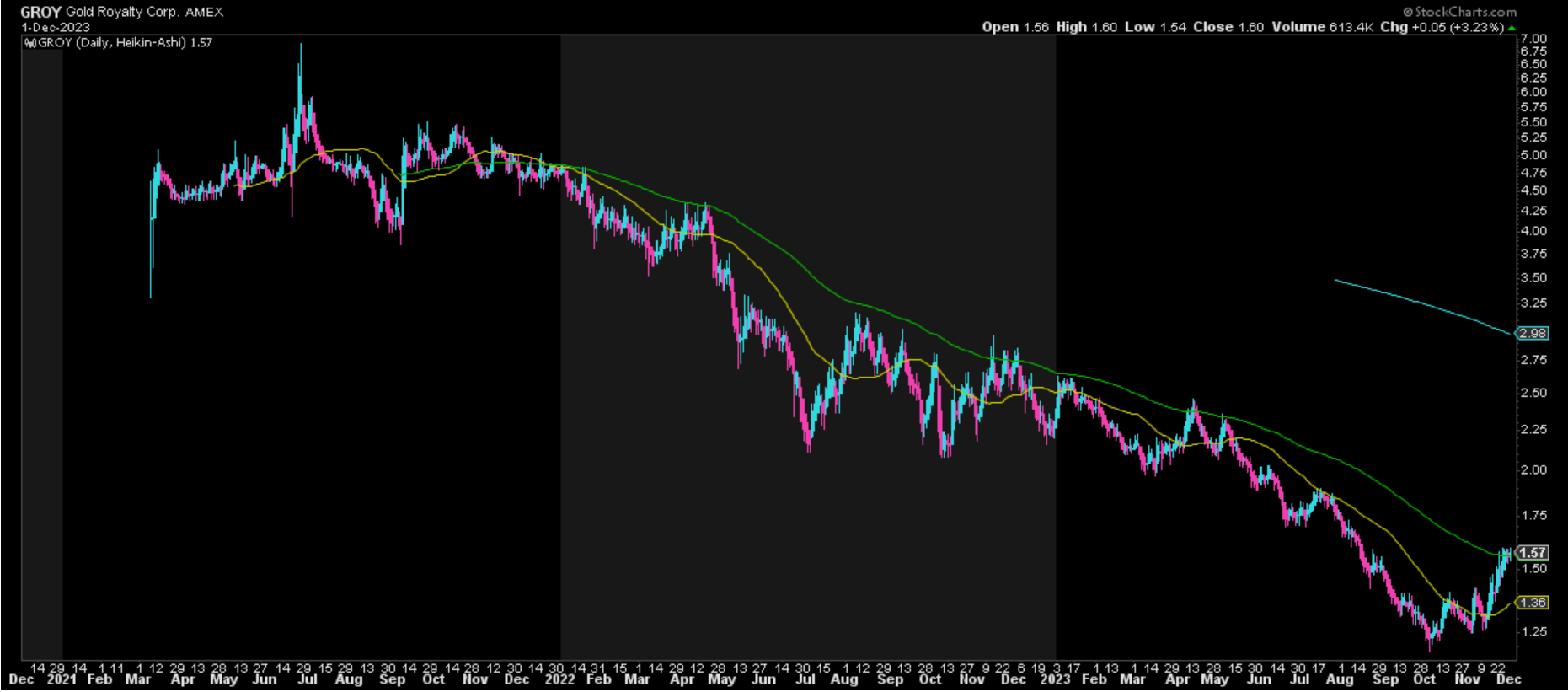

As highlighted in my previous update, I am looking for a minimum 40% discount to conservative fair value to justify starting new positions, and applying this discount results in an ideal buy zone for GROY of US$1.46 or lower. Therefore, while the stock's technical picture has improved and there looks to be a high probability that the lows are in, I would only be looking to start a new position on a retracement. Obviously, the risk is that the stock does not retrace, but I prefer to buy at the right price or pass entirely, and while GROY has a bright future, that level looks to be US$1.45 or lower.

{kind=link}

GROY Daily Chart - StockCharts.com

Summary

Gold Royalty Corp had another solid quarter in Q3, adding a new producing royalty on Cozamin and adding 24 other new royalties (SOQUEM: 22, royalty generation: 2) for limited share dilution which has helped to grow its NAV per share and its number of royalties per share. However, the real story is that we're now less than six months from seeing initial contributions from Cote Gold (a chunky royalty on a ~360,000 ounce per annum mine that is front-end weighted), and the company will be cash flow positive next year, not only helping to improve its ability to be valued on a P/CF basis, but also its ability to grow its royalty set up on track improve further in 2025 and with a major step change in 2027 as production ramps up from the Malartic Complex. Hence, for patient investors looking to get in on the ground floor of a Tier-1 royalty/streaming company at a depressed valuation, I continue to see GROY as a Speculative Buy at US$1.45.

For further details see:

Gold Royalty Corp.: Exploration Success Continues At Key Royalty Assets