AEM - Gold Royalty Corporation: Valuation Beginning To Improve

Summary

- Gold Royalty Corporation was one of the worst-performing gold miners in 2022, declining 50% for the year and massively underperforming the Gold Juniors Index.

- The poor performance can be attributed to the stock heading into the year at a very lofty valuation combined with weaker metals prices that dented sector-wide sentiment.

- However, the company is heading into 2023 at a more reasonable valuation, and its portfolio continues to look better, with one of the better pipelines in the royalty/streaming segment.

- At a share price of US$2.45, I still don't see a low-risk buying opportunity yet, but I do think the story has improved immensely, and it's a name worthy of keeping an eye on if we see further weakness.

While the Gold Miners Index ( GDX ) has enjoyed a sharp rally off its lows and names like Franco-Nevada ( FNV ), Royal Gold ( RGLD ), and Osisko Gold Royalties ( OR ) have raced higher, Gold Royalty Corporation ( GROY ) has unfortunately been left in the dust. This is despite the stock massively underperforming its peer group and suffering a 50% plus drawdown last year, double that of its peer group. I would argue that the underperformance last year is not surprising, with the stock entering the year at a frothy valuation, as I warned in October 2021 at US$5.40 per share.

The good news for investors who have patiently sat on the sidelines is that this significant underperformance has reset the major valuation divergence vs. peers, which impeded its share price performance last year, leaving it more reasonably valued as we begin 2023. Meanwhile, its portfolio has never looked better, and one could argue that Gold Royalty Corporation ("GRC") has one of the better-looking development portfolios within its peer group, plus two solid cornerstone assets where it's partnered with top-3 operators and benefits from meaningful royalties (2-3% NSR, 1.5% NSR, 3% NPI). Let's take a closer look at the stock below following its FY2022 results:

Granite Creek Mine (GRC 10% NPI) (i-80 Gold Corporate Presentation)

{kind=link}

FY2022 Results

GRC released its fiscal Q4 results in late December, reporting quarterly revenue and option income of $0.9 million and $5.7 million for its year ended September 30th, 2022, or ~2,200 gold-equivalent ounces [GEOs] on a full-year basis. This was a beat vs. its guidance of $5.0 million in revenue for FY2022, but the major news was the significant upgrades we've seen to the portfolio. In fact, GRC now has over 200 royalties and seven producing royalties (up from ~190 and six last year, respectively), and revenue increased ~2,000% year-over-year to $3.94 million, up from $0.19 million in FY2021.

Although this revenue figure is still well behind other junior royalty/streaming peers like Elemental Altus Royalties ( OTCQX:ELEMF ), we have seen considerable progress across GRC's royalty portfolio in 2022, and the company has entered 2023 much stronger than where it sat following its IPO debut. This includes announcing an updated resource estimate at Fenelon (~3.95 million ounces at ~3.15 grams per tonne of gold), the acquisition of Gold Standard by Orla ( ORLA ), which pushes ahead development at Railroad-Pinion with a well-capitalized operator owning the project and anxious to drill for new ounces, and most importantly, continued exploration success at two key assets: Canadian Malartic and REN.

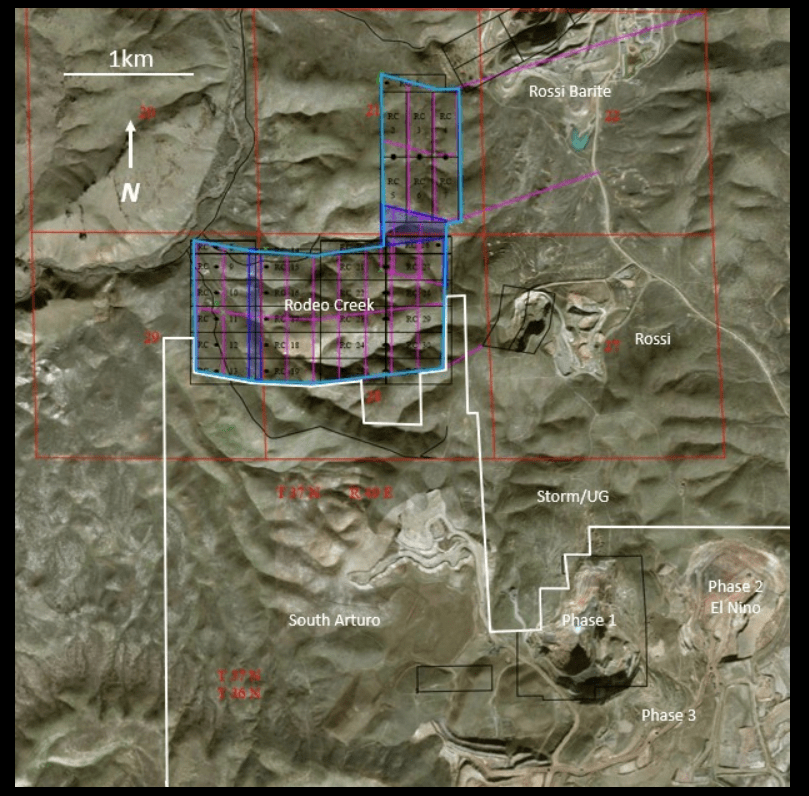

Rodeo Creek Property Location (GRC 2% NSR) (Premier Gold News Release)

{kind=link}

In addition to this, Nevada Gold Mines' acquired Rodeo Creek in an asset change, adding new ground north of South Arturo at the massive Carlin Complex; Calibre Mining ( OTCQX:CXBMF ) completed its acquisition of Fiore which could push ahead development at Gold Rock, and while a relatively low royalty rate (0.2%), SSR Mining ( SSRM ) continues to release phenomenal oxide intercepts from Trenton Canyon, which could provide future feed for its Marigold operations. Finally, and as discussed in a previous update , GRC added a new producing asset in Granite Creek Underground and incremental long-term upside from i-80 Gold's ( IAUX ) high-grade open-pit project next door.

These developments obviously did not show up in the company's FY2022 revenue, nor will most of these developments show up in FY2023 or FY2024 revenue either. However, these are all positives for the GRC story, with the potential for GRC to ultimately grow its producing asset base to 15+ royalties by the end of this decade, even without accounting for any future acquisitions and assuming Isabella Pearl heads offline. Some of these opportunities include Granite Creek Open Pit, Gold Rock, Railroad-Pinion, Lincoln Hill, Trenton Canyon, and Fenelon, with the latter potentially being a significant contributor, with the potential to contribute ~3,800 GEOs per annum in its first five years or ~$7.4 million in revenue at a $1,900/oz gold price.

The ~3,900 GEO per annum estimate at Fenelon for the first five years assumes a throughput rate of 6,000 tonnes per day and an average diluted grade of 2.8 grams per tonne of gold with a 95% gold recovery rate with slightly higher grades in the earlier years of the mine life.

Two Cornerstone Assets Operated By Top Producers

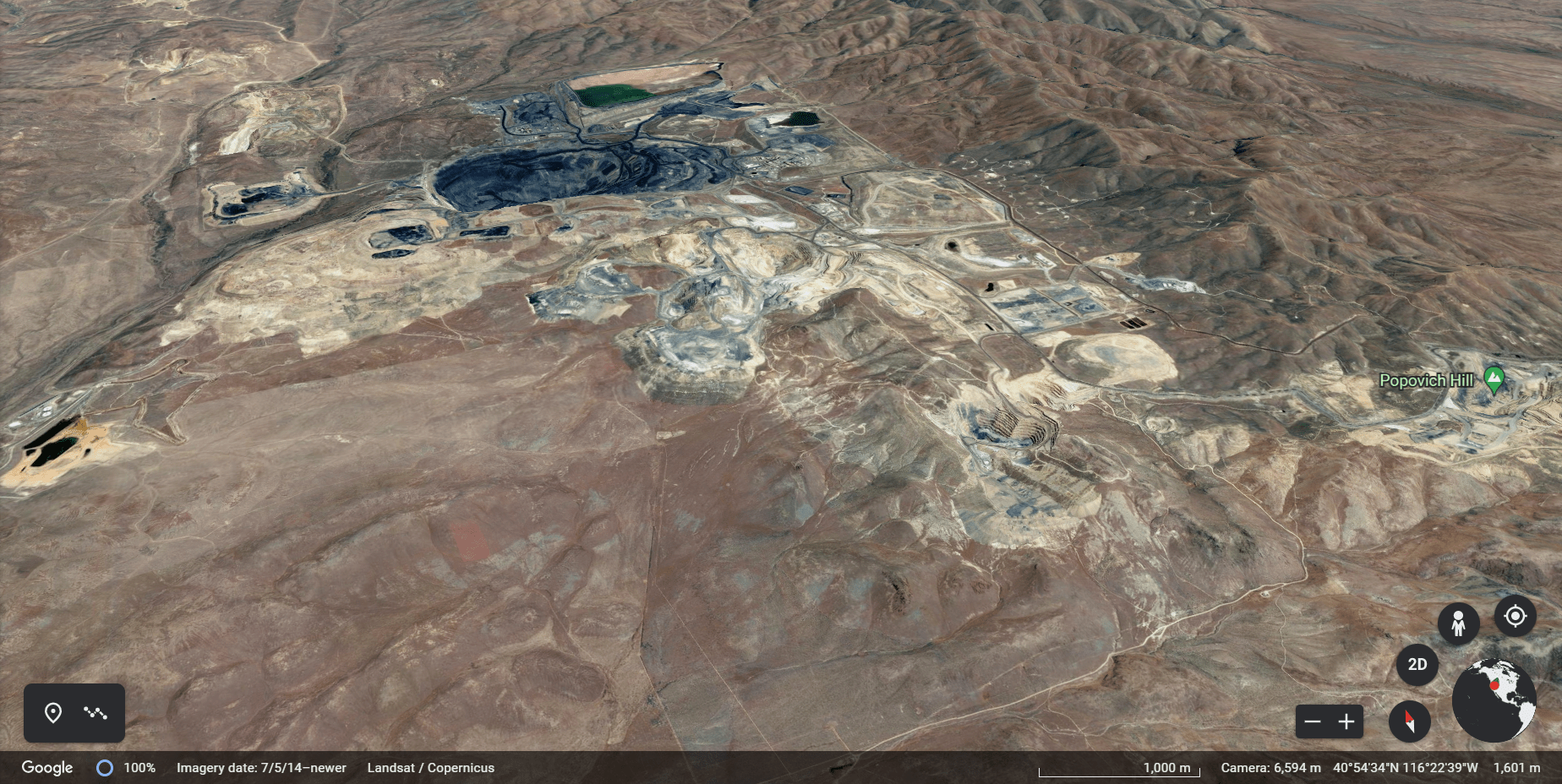

Although the recent developments on other exploration and or development assets are exciting and may have been missed by some investors, the two assets that will really move the needle are Nevada Gold Mines' REN Project (the northern extension of Goldstrike at the Carlin Complex), and Agnico Eagle's ( AEM ) Odyssey Project in Quebec. Beginning with REN, Barrick ( GOLD ) continues to discuss this asset in its quarterly updates. The most recent update was its discussion of REN as a future growth opportunity (along with Rita K, North Leeville, and Horsham) at its Carlin Complex, which is the backbone of its Nevada operations, which is currently home to ~20.0 million ounces of reserves at a grade of 3.5 grams per tonne gold.

Carlin Complex, Nevada (Google Maps)

{kind=link}

Barrick noted in its Investor Day Presentation that it had brought the West Barrel layback forward at the Goldstrike open pit to support REN infrastructure and to open up new exploration areas. Plus, an updated mineral resource is planned in Q1 of this year. As it stands, REN is home to ~1.25 million ounces of gold at 7.4+ grams per tonne of gold, and resource growth looks likely with a new Western mineralized corridor identified, Corona. The continued exploration success here and positive exploration results suggest that REN is a clear priority for Nevada Gold Mines and points to a high likelihood of it moving into production before 2030 to support the company's 10-15 year growth plan at the Carlin Complex.

While REN obviously isn't anywhere near the size of Canadian Malartic, having a 1.5% NSR and 3.5% NPI on a project owned by a joint venture between two companies with a combined market cap of $70 billion at their largest mining complex is certainly an enviable position to be in and a differentiator vs. most peers of its size. And, given the exploration budget of the joint venture, their decades of operating experience in the state, and the fact that Barrick appears bullish on the opportunities north of Goldstrike given its consolidation of South Arturo and acquisition of Rodeo Creek, I would be shocked if REN didn't receive lots of attention from an exploration standpoint over the next several years so that it can hopefully support a 10-20 year mine life to provide refractory ore feed to its Carlin facilities.

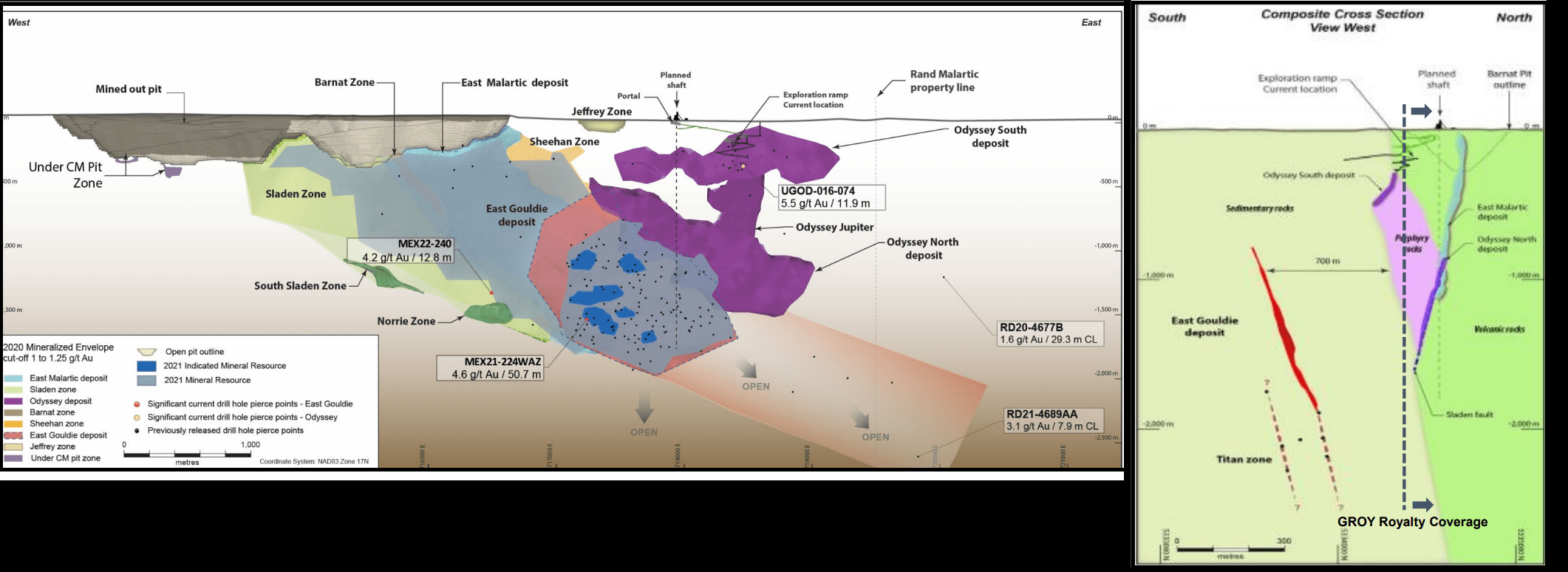

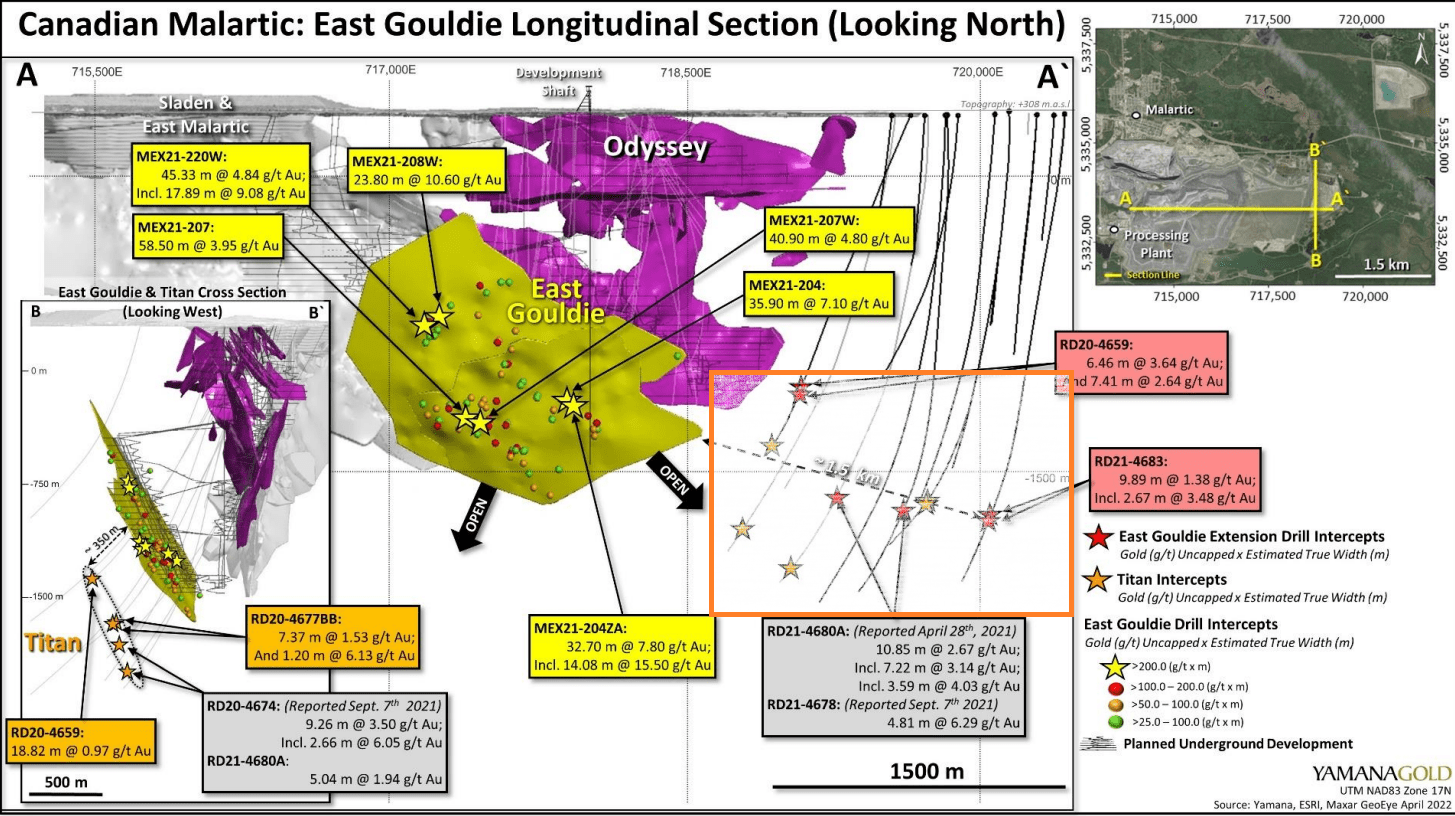

Odyssey Underground Zones & Exploration Success + GRC Royalty Coverage (Company Presentation) Canadian Malartic - Technical Report (Agnico/Yamana Tech Report)

{kind=link}

{kind=link}

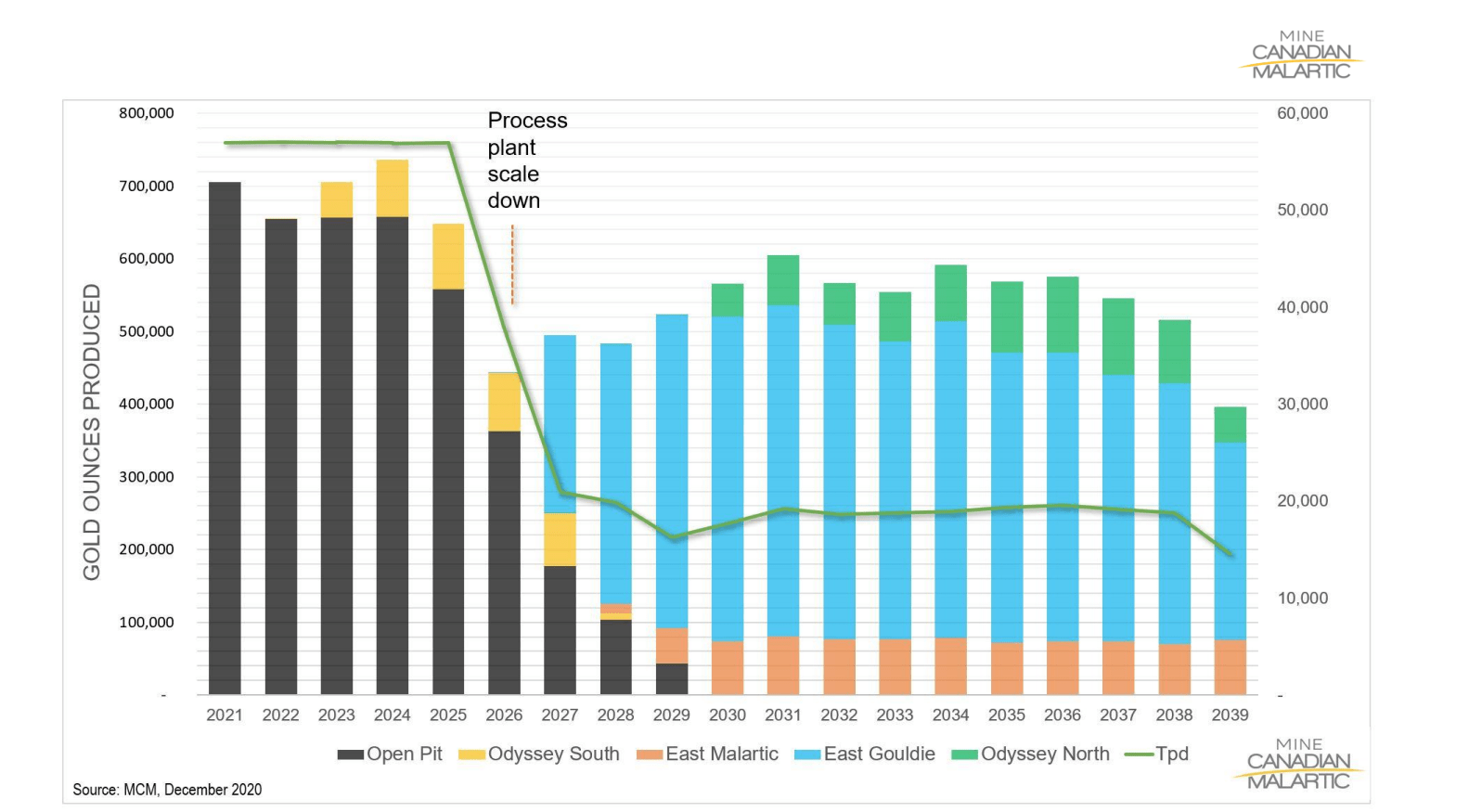

Moving to Canadian Malartic, we can see GRC's royalty coverage above with a 3.0% NSR on Odyssey North, the majority of East Malartic, and a portion of the Norrie Zone. The company also has a 1.5% NSR on the Midway Project which surrounds the Main Malartic Pit to the east and southeast, and just east of where drilling is currently ongoing at the East Gouldie Extension which extends onto the Rand Malartic Property outline. For those unfamiliar, Agnico Eagle will take 100% control of the project following the Yamana ( AUY ) acquisition, and the company is in the process of shifting from a massive open-pit operation (55,000+ tonnes per day) to an underground (~19,000 tonnes per day), with shaft sinking set to begin this quarter as well as first production from the Odyssey South Ramp.

As I've discussed in previous updates on GRC, the major beneficiary of the shift to mining at Odyssey Underground is Osisko Gold Royalties, which holds a massive 5.0% NSR on the main deposit (East Gouldie), which lies just outside of GRC's royalty coverage. Notably, Agnico Eagle and Yamana have seen considerable exploration success east of East Gouldie, with a potential 4.0 kilometer strike length for this deposit vs. just 1.5 kilometers of this deposit in resources. However, GRC does benefit from continued production at the open pits until 2028 and the start of production at East Malartic (2028-2039) and more than a decade of production at Odyssey North post-2029.

Odyssey Exploration Success (Yamana Presentation)

{kind=link}

Additionally, it's worth noting that while Osisko Gold Royalties has been getting the majority of positive headlines on its royalty ground, we recently saw drilling west of East Gouldie that suggests a possible connection of East Gouldie and Norrie along strike. Plus, Yamana gold noted in its Q4 exploration update that the Odyssey internal zones are meeting or exceeding expected grades with recent drilling, suggesting upside at these zones as well. Plus, this operation has capacity of 60,000 tonnes per day and will have 40,000 tonnes per day of excess capacity post-2028 once mining transitions to primarily underground. While I expect Agnico could truck ore from other deposits like Camflo and Wasamac to fill the mill and it's Osisko that has the per tonne royalty, we could see a second shaft that would likely focus on the East Gouldie Extension but may also pull additional ounces from the Odyssey zones and GRC royalty coverage.

To summarize, while I continue to see Osisko Gold Royalties and Agnico Eagle as the premier ways to play the consolidation and continued exploration success at Canadian Malartic, GRC does have a decent portion of this deposit under its royalty coverage and especially for a company of its scale. Meanwhile, exploration success to the west of East Gouldie towards Norrie is positive, as is the fact that it's in Agnico's best interest to make new near-mine discoveries to fill the Canadian Malartic mill, suggesting this deposit is going to be drilled aggressively the next decade. Hence, with decent royalty coverage and a solid rate on a mine that's likely to maintain production well into the 2050s, this is a very nice asset for GRC even if it paid up to obtain this royalty coverage.

Gold Royalty has discussed that it is unique in that it has three cornerstone assets, but I would argue that a more fair assessment is that it has two cornerstone assets, with a 0.75% NSR on a portion of Cote not being as significant of an asset. That said, Cote will move into production in Q1 2024 and the royalty covers the earlier years of the mine life, so this will provide a nice boost to annual cash flow starting in Q2 2024.

Valuation

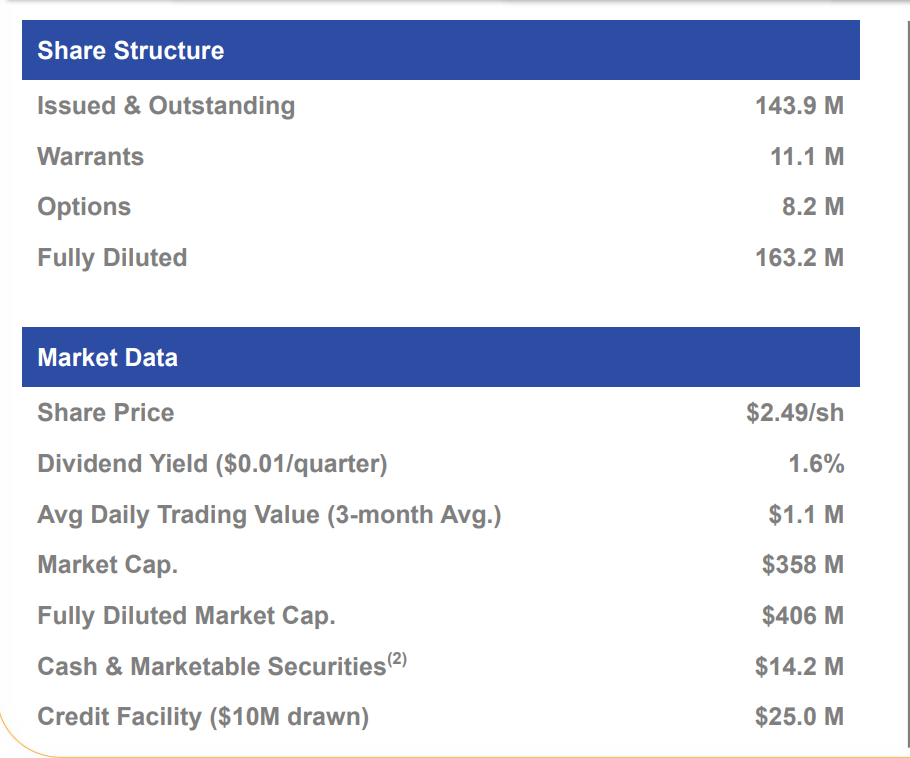

Based on ~165 million fully-diluted shares (year-end estimate) and a share price of US$2.45, GRC trades at a market cap of US$404 million, which is a steep valuation for a company that just generated less than $6 million in revenue/option income in FY2022. This is because it places GRC at one of the highest revenue multiples sector-wide trading at ~70x trailing sales. However, given the depth of GRC's development portfolio and the organic growth opportunities within its portfolio (Odyssey, Jerritt Canyon) stemming from excess processing capacity, valuing the company on stale figures like last year's sales or even FY2025 estimates (~$20+ million in revenue) would be a mistake. Instead, the better way to value the company is on a net asset value basis where it trades at less than 0.80x P/NAV.

Gold Royalty Shares Outstanding/Diluted, Trading Volume & Cash Position (Company Presentation)

{kind=link}

Based on an estimated net asset value of US$520 million and a P/NAV multiple of 1.0 to reflect its Tier-1 jurisdictional focus with strong operators as partners offset by its small scale (sub 10,000 GEOs per annum), I see a fair value for GRC of US$3.15. However, this assumes that the company doesn't do any new deals this year, which could boost net asset value, and I do like one of the more recent deals announced by GRC, with it paying a reasonable price paid for exposure to i-80 Gold's ( IAUX ) Granite Creek Project. The project hosts one producing mine (Granite Creek Underground), but could host a second mine that would be one of the highest-grade open-pit mines in Nevada if i-80 green-lights Granite Creek Open Pit post-2026.

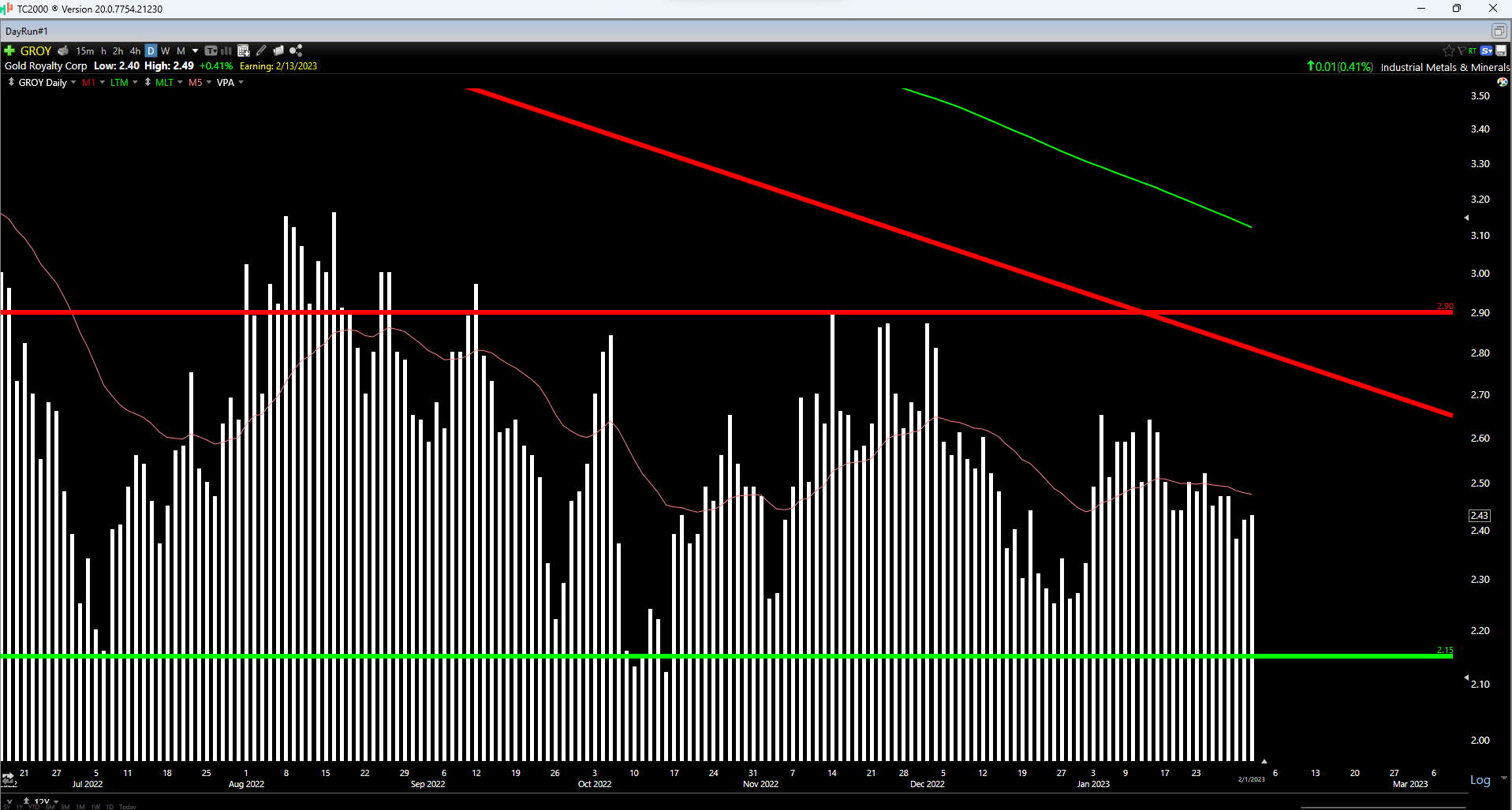

While this fair value estimate points to a 28% upside to fair value, I prefer a minimum 35% discount to fair value when it comes to starting new positions in small-cap names. This is because I want to be compensated for the increased risk of owning a more volatile and lower market cap and one (in GROY's case) that is not yet consistently generating free cash flow. Applying this discount results in an ideal buy zone of US$2.05 or lower. Meanwhile, from a technical standpoint, GRC has a potential support zone between US$2.10 and US$2.15, which is right near this ideal buy zone for an initial position. To summarize, I am not in a rush to jump into the stock just yet, even if it is starting to become more interesting from a valuation standpoint.

GROY Weekly Chart (TC2000.com)

{kind=link}

Summary

Gold Royalty Corporation has massively underperformed its peer group of royalty/streaming companies, and this isn't surprising at all, given that it had its IPO debut at a bubble-like valuation yet was still heavily promoted while it traded at more than 100x forward revenue . Fortunately, the stock has come back to reality over the past two years, and it's seen meaningful growth in its portfolio, with the company now sitting on 216 royalties across several different jurisdictions but with a concentration in prolific Tier-1 locations like Nevada (83 royalties), Quebec (25 royalties), and Ontario (64 royalties).

Some investors might be critical of the share dilution we've seen to date after three acquisitions, and one could argue that GRC paid a significant premium to swallow these companies. However, it had the benefit of using highly valued GROY shares to complete these deals, meaning it was much less expensive when we adjusted for arguably ~50% overvalued GROY shares used to complete these deals. Hence, although I didn't love the deals and the price paid, the result is that GRC has a very solid portfolio today and royalties on two cornerstone assets, with a solid runner-up in Cote, even if it's only a portion of the planned pit.

Canadian Malartic Mine (GRC Royalty) (Yamana Gold Presentation)

{kind=link}

The key going forward will be if the company can be patient and grow in a disciplined manner like Osisko Gold Royalties, waiting to acquire counter-cyclically and focusing on mostly world-class assets. However, with a portfolio that benefits from more depth, a solid technical team that includes Samuel Mah and Jerry Baughman, and the ability to grow using cash flow and debt post-2024 (vs. mostly equity to date), I see the future being brighter, especially if some "maybe" assets end up being green-lighted by 2027 (Fenelon, Granite Creek Open Pit, Lincoln Hill). That said, I see the low-risk buy zone being a little lower at US$2.05, so I remain on the sidelines for now.

For further details see:

Gold Royalty Corporation: Valuation Beginning To Improve