GROY - Gold Royalty: Relative Valuation Continues To Improve

2023-08-31 05:27:26 ET

Summary

- Gold Royalty Corp. reported lower revenues and GEO volume due to unfavorable mine sequencing at Malartic and difficult year-over-year comparisons at Borden.

- From a bigger picture standpoint, the company exited the quarter with more royalties, a decent liquidity position, and a new paying royalty at Cozamin, plus lower expenses (dividend cut).

- In this update, we'll look at recent developments and whether this ~70% correction has left GROY in a position where it's getting close to being a Speculative Buy.

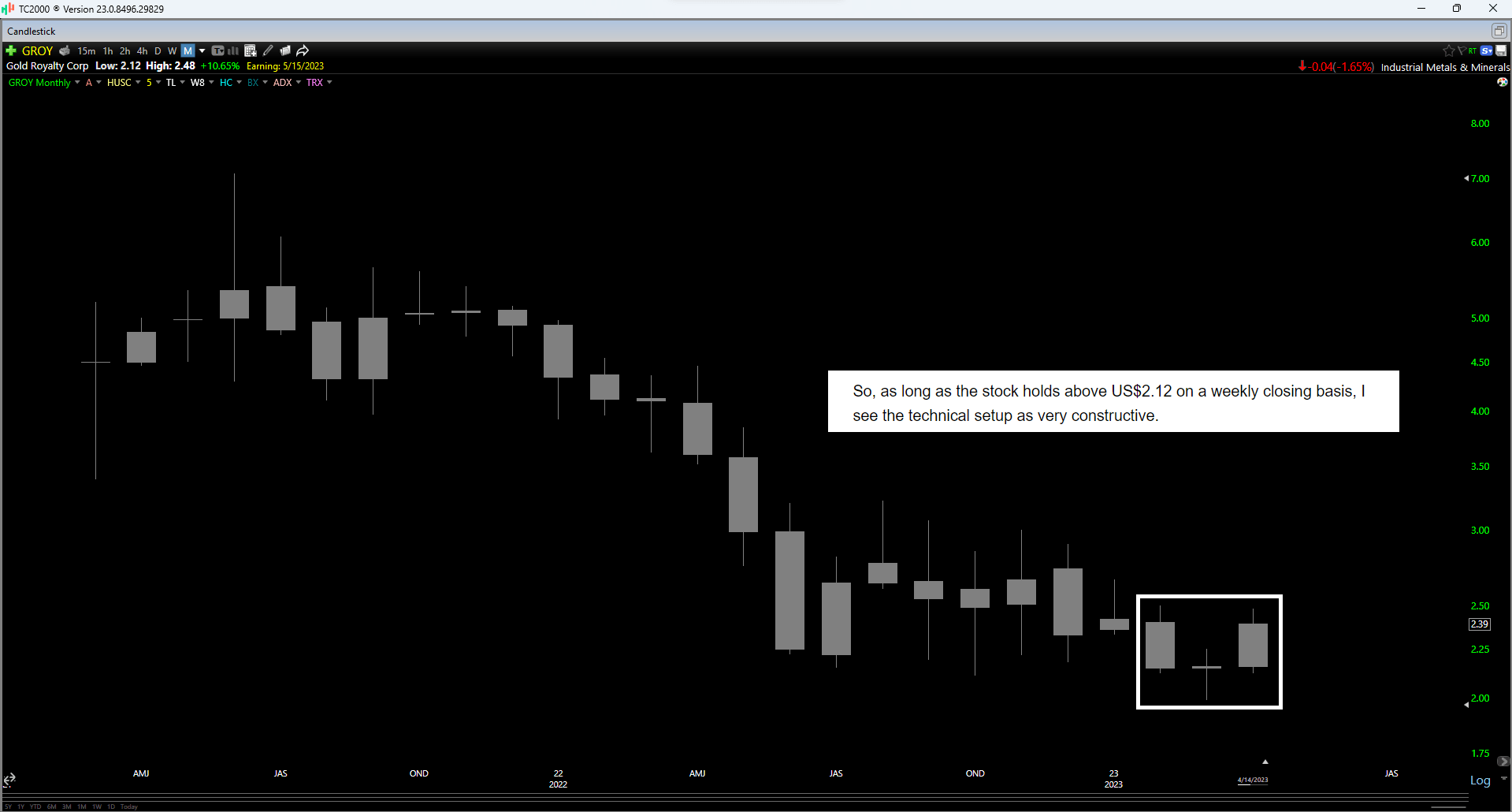

Just over three months ago, I wrote on Gold Royalty Corporation ( GROY ), noting that I would remain long the stock from my entry at US$2.13 if it could hold US$2.12 on a weekly closing basis. This is because the valuation was becoming more reasonable and the stock was working on a potential morning star reversal (rare bullish pattern) on its monthly chart, suggesting that if the bulls successfully defended the low of this pattern, the stock might finally be bottoming. Unfortunately, the stock immediately broke below US$2.12 for the week of April 28th, so I sold my position at break-even and have remained on the sidelines since then. However, while the stock has broken down, the relative valuation setup has continued to improve, and we've seen positive recent developments. Let's look at the most recent quarter below and recent developments across the portfolio:

GROY Monthly Chart - Worden.com, Seeking Alpha

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q2 Results

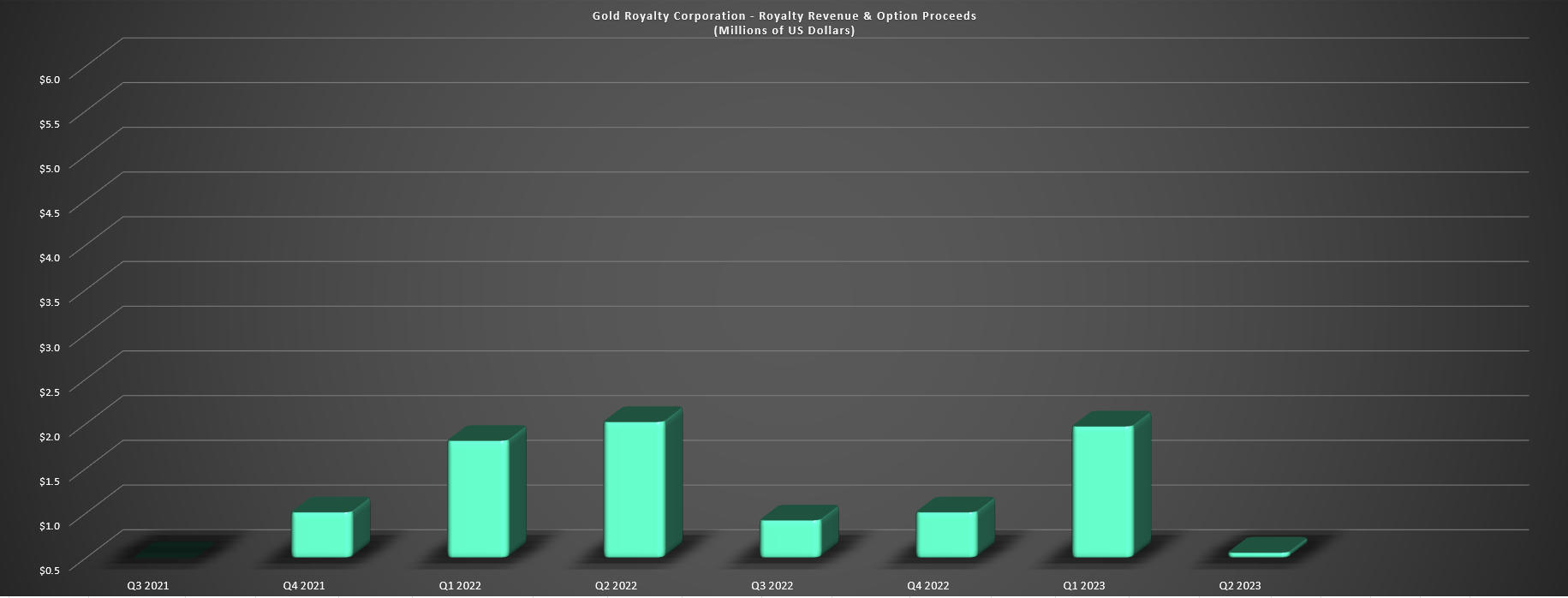

Gold Royalty Corporation ("GRC") released its Q2 results earlier this month, reporting quarterly volume of 237 gold-equivalent ounces [GEOs], a sharp decline from the year-ago period (1,031 GEOs). However, it's important to note that the company was up against near insurmountable comps with back payments owed from the Borden Lake Property in the prior-year period, which contributed 823 GEOs in Q2 2022 (Q2 2023: 225 GEOs). Unfortunately, this difficult comparison was impacted further by re-sequencing of planned mining at Canadian Malartic at the Barnat Pit, with attributable ounces from Malartic declining sharply as well. Finally, Jerritt Canyon's production wound down after the announced suspension of mining, a further hit to production. The result was that the company reported just ~$0.56 million in total revenue and land agreement proceeds in the quarter (royalty revenue: ~$0.47 million), down from ~$2.02 million in the year-ago period (~$1.91 million in royalty revenue).

GROY - Total Revenue & Land Agreement Proceeds - Company Filings, Author's Chart

{kind=link}

However, while this was a noisy quarter, the company has stuck to its soft guidance of $5.5 million to $6.5 million in total revenue and land agreements proceeds, it's exited the quarter with three more royalties than it had previously (0.75% NSR at Quarter Horse and 2.0% NSR at Goldfield West in Nevada, plus 1.0% NSR on a portion of Cozamin). Plus, this portion of the portfolio (royalty generation) continues to be a nice bonus to its low-risk royalty model, with $3.2 million in expected land agreement proceeds this year despite less than $90,000 spent in H1 on mineral interests maintenance expense. And while the company did report a net loss of $2.5 million and negative cash flow in the period, little has changed when it comes to its 2024 outlook, which is a much better year with higher contribution from Canadian Malartic and initial contribution from Cote.

The result is that we should see regular quarterly and annual records, with up to 4,000 GEOs in 2024 and upwards of ~5,000 GEOs in 2025, with the potential for Granite Creek Underground to sneak into late 2025 from a contribution standpoint (120,000 ounce production threshold before 10% NPI kicks). This should allow GRC to attain free cash flow positive status ahead of most of its junior peers by 2025 and begin transacting with cash flow and available liquidity. As it stands, GRC has $25 million available under its RCF (accordion included), appears to be done with equity sales under its ATM which helped to fund its Cozamin royalty acquisition, and this gives the ~$30 million in liquidity (~$5 million cash, $25 million available), placing it in a better position than some of its smaller peers to take advantage of the favorable environment for acquiring royalties.

Let's dig into recent developments:

Recent Developments

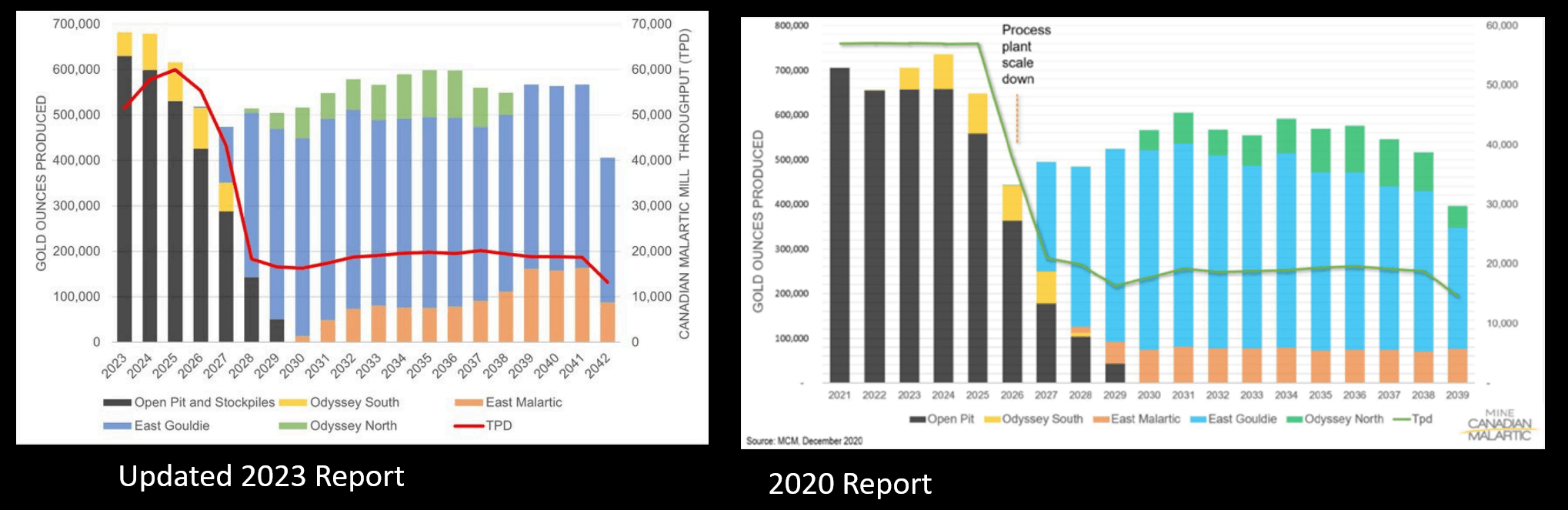

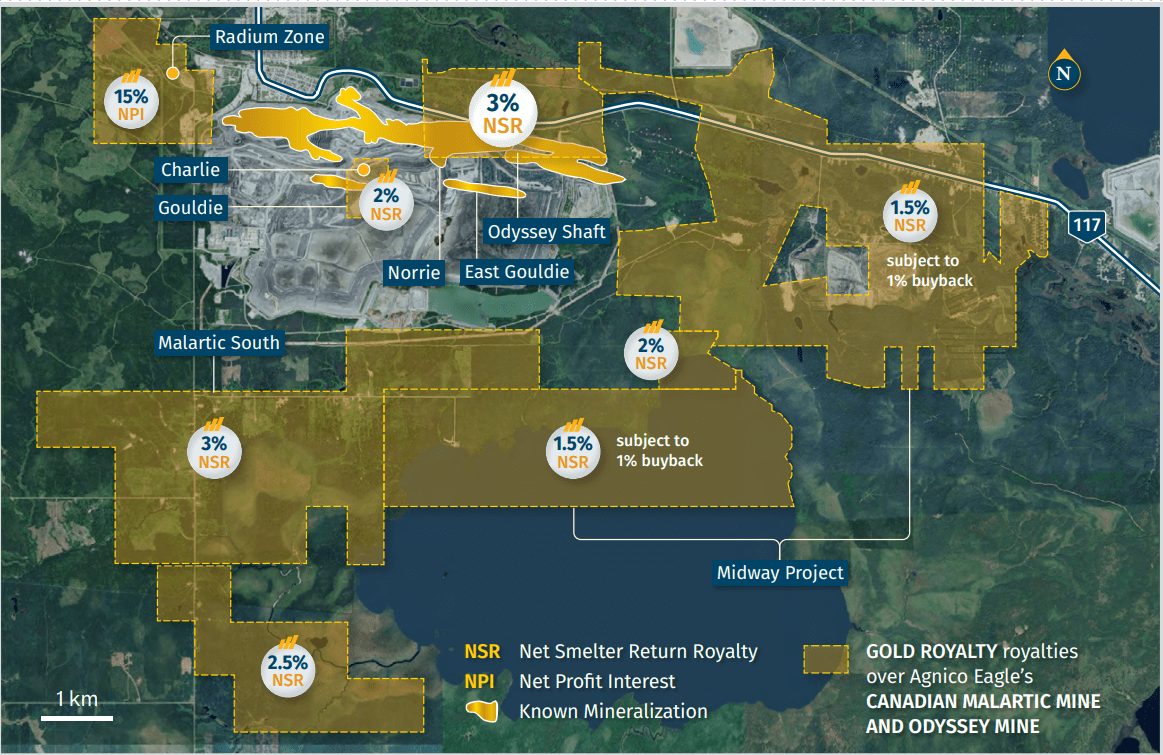

Beginning with the Canadian Malartic Mine (Odyssey), Agnico Eagle ( AEM ) released an update study noting that the mine life has been extended by three years to 2042 and that the average production profile has increased from ~547,000 ounces from 2029 to 2039 to ~558,000 ounces from 2029 to 2041. In addition, we've seen a 23% increase in gold production over the life of mine vs. the 2020 study, and the total resource base (M&I, inferred, and reserve ounces) now sits at ~15.7 million ounces. Plus, there appears to be a considerable upside to this figure, with Agnico noting that mineralization in the Odyssey internal zones is not included in the mine plan and is low hanging-fruit given its proximity to current and planned underground infrastructure. This benefits GRC, which holds a 3.0% NSR on the northern portion of the project, including Odyssey North, East Malartic, a portion of Norrie, and the Barnat Pit, with additional royalties to the east (Midway) and to the south (Malartic South).

Odyssey - Updated LOM Plan - Agnico Eagle Gold Royalty Corporation Coverage (Canadian Malartic) - Gold Royalty Corp Website

{kind=link}

{kind=link}

Elsewhere in the portfolio, construction at Cote Gold is ~86% complete, according to Iamgold ( IAG ), with GRC holding a 0.75% NSR on the southern portion of the pit. GRC's royalty at Cote Gold is expected to contribute in early 2024 based on Iamgold's stated first production of Q1 2024, with the first full year of commercial production being in 2025. Using conservative estimates, this should translate to ~1,000 GEOs next year and upwards of 2,000 GEOs in 2025 and 2026, with the higher-grade near-surface material in Zone 5 and Zone 7 expected to be sequenced earlier in the mine life. Based on these figures, this would translate to an annual contribution of ~$4.0 million per annum for GRC, nearly doubling its expected annual contribution relative to FY2023 guidance of $5.5 million to $6.5 million in land agreement and total revenue proceeds.

The last development worth noting at producing royalties is that GRC acquired a 1.0% NSR on two concessions on the Cozamin Mine in Mexico, with the asset expected to produce ~24,000 tonnes of copper and ~1.3 million ounces of silver from 2023 to 2027. This should translate to upwards of $1.0 million in contribution per annum at current levels, paying itself back well before the current end of the mine life (based solely on reserves) in 2030, and it gives GRC a fifth producing asset after the company dropped to four producing royalties with Jerritt Canyon going into care & maintenance. Notably, this deal also provides exposure to provide diversification across metals and smooth out volatility in the company's revenue and cash flow vs. its primary precious metals focus.

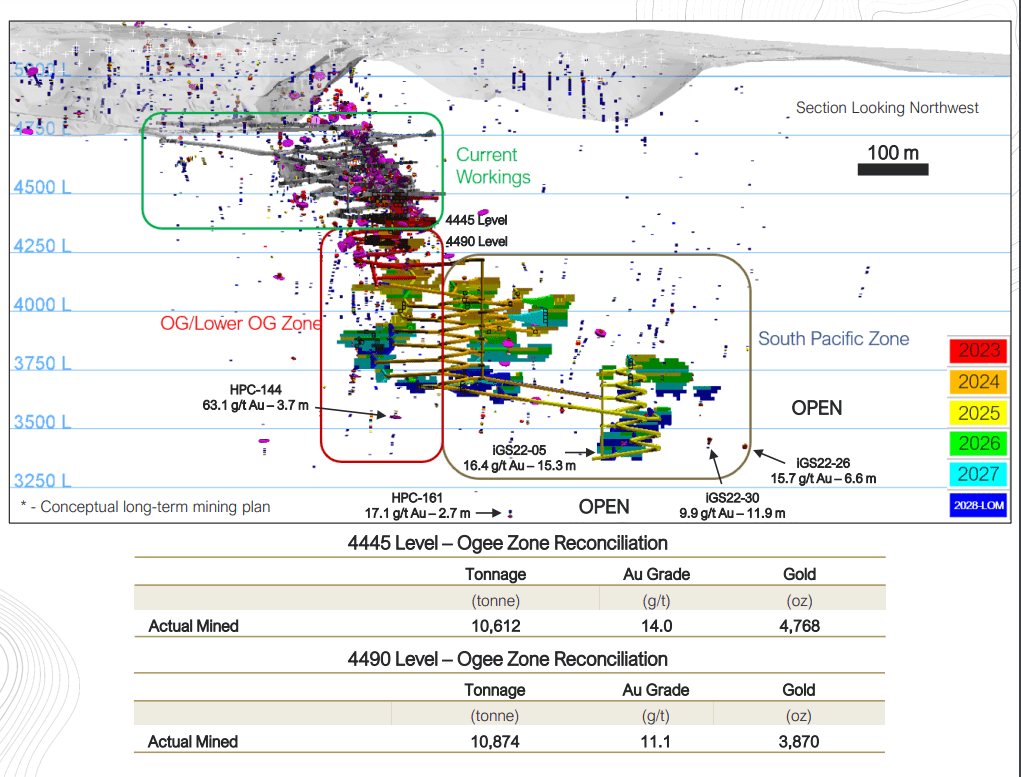

Moving over to development assets or those aren't yet contributing, i-80 Gold ( IAUX ) noted that the production ramp-up at Granite Creek is progressing well, with increased mining and development rates at the Ogee Zone and positive grade reconciliation on the first two fully mined levels. These two levels (4445 and 4490) yielded an average grade of ~11.1 and ~14.0 grams per tonne of gold, well above the average measured & indicated resource grade of 10.4 grams per tonne of gold at Granite Creek Underground, translating to ~8,600 ounces of gold. For those unfamiliar, GRC has a 10% NPI on this asset which will kick in once 120,000 ounces of gold have been produced (~100,000 ounces left to go), suggesting that the asset will begin contributing at some point in 2025.

Granite Creek/South Pacific Zone - i-80 Gold Presentation

{kind=link}

Although the current production rate may appear low at this asset, it's worth noting that Granite Creek Underground is still in the ramp-up phase and operating at nowhere near its full potential. This is because even under more conservative assumptions, mine production should increase to 750 tons per day at 11.0+ grams per ton of gold, which would translate to ~75,000 ounces per annum at an assumed 85% recovery rate. And while the resource may not seem that significant at ~650,000 ounces, I would not be surprised to see the property-wide resource increase to 1.5+ million ounces near-term (year-end 2024), and 2.5+ million ounces longer-term, with the addition of the high-grade South Pacific Zone and what appears to be further upside to the north, at depth, and in the gap zone.

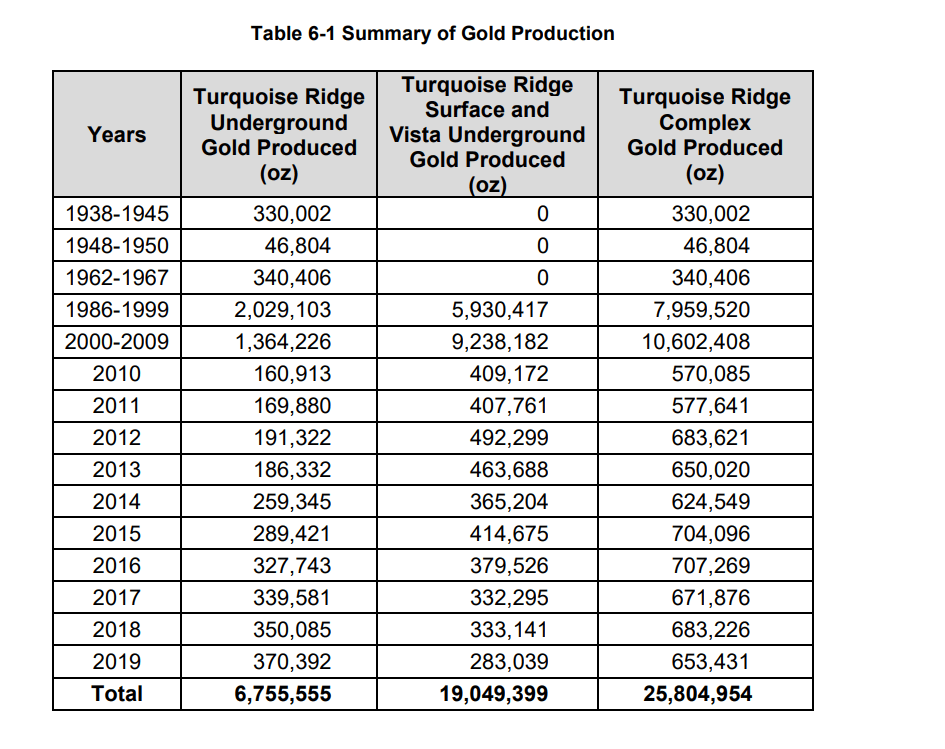

Turquoise Ridge UG & Complex Historical Production - 2019 TR

{kind=link}

To summarize, while the current resource base (assuming 80% conversion to reserves) may imply a sub 7-year mine life, this is an asset that could easily produce well into the late 2030s and likely much longer given that it's neighboring mine is producing 6x as much gold per annum (~450,000 ounces) and has produced over 7.0 million ounces of gold to date from the underground alone (27+ million ounces property-wide). So, while this asset may not be contributing yet and will sequence in behind Cozamin and Cote Gold in regards to initial contribution, this should be a meaningful contributor to GRC's annual GEOs post-2025.

As for other assets, Wallbridge Mining ( WLBMF ) released a PEA on its Fenelon Gold Project in northern Quebec, with it highlighting a 12.3 year mine life with ~212,000 ounces of annual production at industry-leading all-in sustaining costs of $924/oz based on ~2.7 million ounces of gold from the Tabasco-Cayenne, Area 51, and Gabbro zones. The company envisions a 7,000 tonne per day bulk mining scenario with stopes expected to average 30 to 40 meters in height, 20-25 meters in length and 20 to 25 meters in length, with this being a similar-sized operation to the Young-Davidson Mine near Matachewan, Ontario.

However, while this is a significant production profile and the asset boasts impressive economics which would translate to ~4,200 GEOs per annum attributable to GRC which was above my ~3,900 GEO estimate, there is one major issue. This is the fact that upfront capex is expected to come in at ~$503 million based on a relatively preliminary study, and we often see at least 20%+ cost creep from PEA --> FS as estimates get tightened up, translating to an upfront capex bill closer to $610 million. And given that Wallbridge has a sub $120 million market cap, there is no path to putting this asset into production for the company without a much stronger share price to allow it to raise equity and debt at some point, or a partner on the asset.

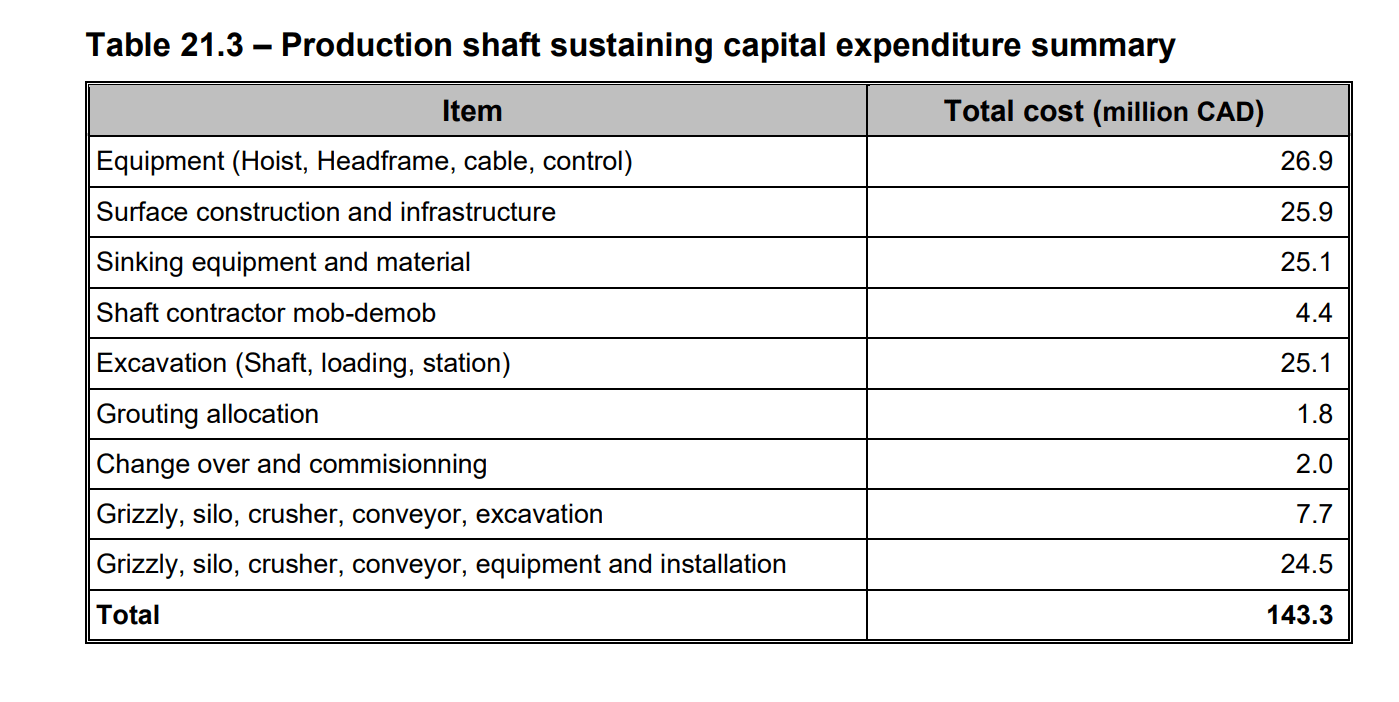

Fenelon Production Shaft Capex () - 2023 TR

{kind=link}

Given that this is a solid asset, the potential for a partner to come in is certainly a possibility, and we've seen interest in the region with Gold Fields teaming up on Windfall for a 50% stake, also in the James Bay region of Quebec. That said, Fenelon has two-thirds of the production profile with a similar capex bill given the planned construction of a 5.2 meter production shaft into the Tabasco-Cayenne Zone starting in Year 2 which will require significant additional capital (~$170 million under more conservative estimates) shortly after the start of commercial production. So, while we could see a partner come in at Fenelon, it would have to be a relatively large one given that this is what I would consider a mid-sized project from a capex standpoint (minimum of ~$600 million under more conservative estimates), which is likely above the available budget of most sub 300,000 ounce producers.

To summarize, while Fenelon came in above my estimates on potential GEOs with slightly higher grades (~2.7 grams per tonne of gold) and it's nice to see the project progressing, I have revised my first production timeline from 2028 to 2030 given that we're still at least four years away from permits and the big question mark is needing a partner given that I can't see Wallbridge moving this project forward at an accelerated pace on its own. That said, this is still a very solid asset even if it's likely best to model this further into the future, and this one asset alone could translate to $8.0+ million in annual contribution even if we see no gold price upside if and when production starts post-2029.

So, were there any negatives?

One negative for investors that had come for dividends was that GRC chose to suspend dividends with the company stating that it preferred to focus its capital on growing cash flow and NAV through accretive acquisitions. And while this is a blow to shareholders hoping for regular distributions, this was the right move for a company of GRC's size, especially in the current environment. This is because when we're arguably in the most favorable environment for scooping up royalties since the 2018 cyclical bear market in gold (and possibly even a better environment as debt was still an option at the time due to low rates even if equity prices were depressed), meaning that every available dollar should be going to improving the long-term royalty portfolio and striking while the proverbial iron is hot vs. wasting that money on a dividend that can be reinstated at a later date when there's more capital to go around and when the company has hit a sufficient size to justify returning some capital to shareholders through regular dividends vs. focusing on growth.

Valuation

Based on ~165 million fully diluted shares and a share price of US$1.52, GRC trades at a market cap of ~$250 million, making it one of the lowest market cap names in the junior royalty/streaming sector. This has left the company trading at roughly ~0.60x P/NAV, a deep discount to the mid-tier royalty/streaming peer group (~100,000 GEOs) that currently trades at an average P/NAV multiple of ~1.10x. However, while this is a very reasonable valuation, multiples have continued to compress sector-wide and I think a fair multiple for the mid-tier group is 1.40x while I see a fair value for GRC to adjust for this reality being 1.0x P/NAV. If we use a more conservative estimated net asset value figure of ~$410 million ($340 million combined for Canadian Malartic, REN, Cozamin, Cote, Granite Creek, Borden, Gold Rock, plus $110 million for the rest of the portfolio [-] $50 million in estimated corporate G&A), I see a conservative fair value for GRC of ~$400 million or US$2.42 per share.

Although this points to a 58% upside from current levels, I am looking for a minimum 40% discount to fair value to justify starting new positions in micro-cap royalty/streaming companies. After applying this discount, GRC's ideal buy zone comes in at US$1.45 or lower, but this is a Speculative Buy rating given that this is a company not currently generating free cash flow and sitting at a micro-cap valuation. That said, relative to some other producers that continue to lean on their issue equity to lock up new royalties and focus on development assets vs. cash-flowing assets, I think GRC is better positioned than a couple of its smaller peers. Plus, I like the recent deal for Cozamin that provides immediate cash flow without equity dilution. So, while I'm not in a rush to own junior royalty/streaming companies when mid-tiers are valued attractively and better positioned (higher liquidity, better lending rates), GRC would make the top-2 list of the junior names I track from a relative value and asset quality standpoint.

The designation as a #2 name in the junior space is supported by GRC having two very impressive long-life royalties in its portfolio (Canadian Malartic and REN) with top-3 gold producers as partners, the higher-grade 'starter pit' on another world-class asset in Cote Gold, and a decent development pipeline with a tilt towards Tier-1 ranked jurisdictions. The addition of a copper royalty is certainly a nice sweetener to this portfolio given that copper mines can be long-life with a solid track record of reserve replacement at Cozamin, and several of the exploration/development assets are located in the #1 mining jurisdiction. These include extensions to mineralization at the Carlin Complex with land west of Leeville and Pete Bajo, a royalty on Rodeo Creek which is adjacent to South Arturo, and land south of the #1 and #2 shafts at Turquoise Ridge, providing solid optionality as Nevada Gold Mines ultimately looks to continue growing resources/reserves at these assets given its ample sunk costs along the Battle Mountain and Carlin trends.

Summary

Gold Royalty Corporation saw significantly lower revenues and GEO volume on a year-over-year basis, affected by mine sequencing at Canadian Malartic, limited contribution from Jerritt Canyon (care & maintenance), and lower contribution from its other royalties category. However, quarterly results can be noisy for junior royalty/streaming companies with less diversification than their larger peers and lumpy concentration to a couple of assets, and while the dividend cut might have frustrated some investors, this was the right move to redirect this capital into what's a favorable hunting ground for new royalties. Plus, from a bigger picture standpoint, the portfolio is looking better than it was at the start of 2023, with a new royalty asset in Cozamin, a longer mine life at Odyssey, Granite Creek Underground being closer to first contributions, and Cote Gold being just one year from moving into commercial production.

Tip Of Iceberg - Optionality/Growth Below The Surface - TinyURL (MegaFreeWalls), Wall.AlphaCoders.com

{kind=link}

For junior royalty/streaming companies especially, it's the big picture that matters, given that investors are only seeing the proverbial tip of the iceberg regarding cash flow generation and the GEO profile. However, what's below the surface are potential mine life extensions that will increase NAV, new discoveries that will increase NAV, organic growth such as throughput expansions, and development assets that may be valued near zero today, but which could contribute meaningfully post-2027. And in this department, GROY has one of the better portfolios among its junior peers that's concentrated in Tier-1 jurisdictions with solid partners. So, while I am not long the stock currently, I see GROY as a Speculative Buy on further weakness with its valuation reaching levels where it might become a takeover target given that the market cap is now becoming supported by Canadian Malartic/Odyssey, REN, Borden, and Cote alone, with the rest of the portfolio being free upside to a potential suitor.

For further details see:

Gold Royalty: Relative Valuation Continues To Improve