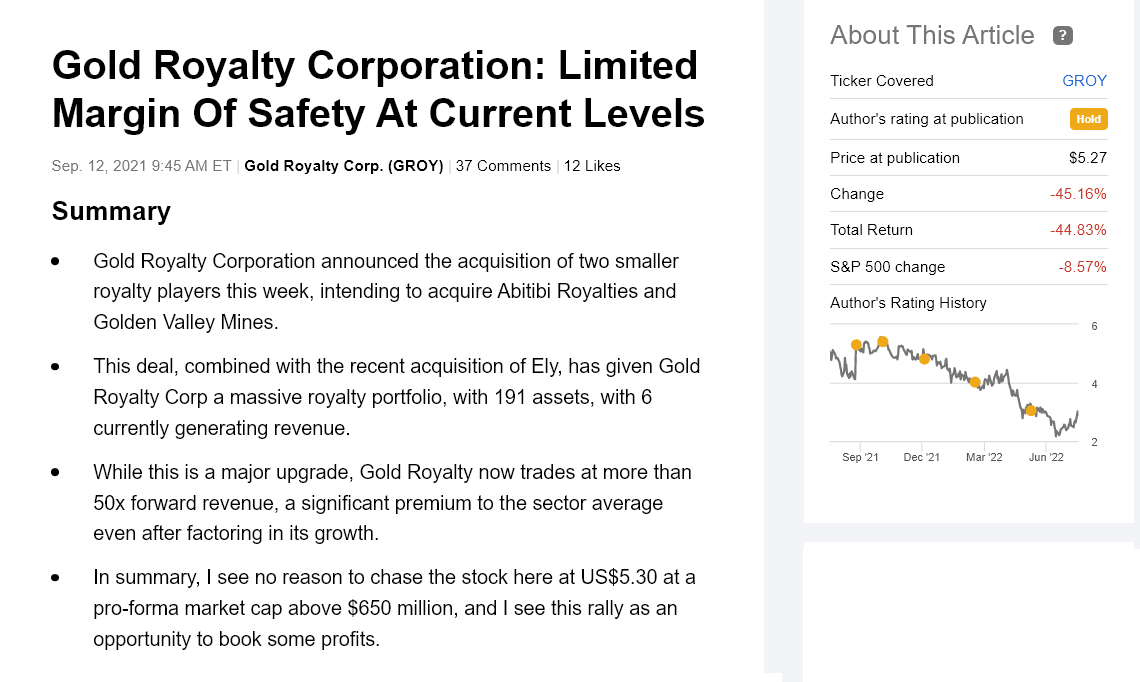

GROY - Gold Royalty: Valuation Beginning To Improve

- Gold Royalty Corporation ("GRC") is down 50% from its all-time highs and is one of the worst-performing names in the precious metals royalty/streaming space.

- This poor performance is not surprising given that GRC was hyped up last year and, as a result, entered the year trading at a massive overvaluation relative to peers.

- With the market cap now dipping below $500 million, GRC is becoming more reasonably valued, and we've seen some positive developments in the portfolio.

- That said, I still see far more relative value elsewhere in the royalty/streaming space, especially with much larger players trading at similar P/NAV valuations and much more attractive revenue multiples.

Just over ten months ago, I wrote on Gold Royalty Corporation (GROY) ("GRC"), noting that while its portfolio had grown considerably on the back of three acquisitions, this was an opportunity to book profits with the stock trading at a massive premium to its peers. Since then, the stock has seen a drawdown of 60%, underperforming not only the Gold Juniors ( GDXJ ) but even many riskier development-stage stories. For investors who were patient and waited on the sidelines, the valuation is finally becoming a little more palatable, and we've seen some positive developments in the portfolio. Let's take a closer look below:

GROY Article - September 2021 (Seeking Alpha Premium)

{kind=link}

Fiscal Q2 Results

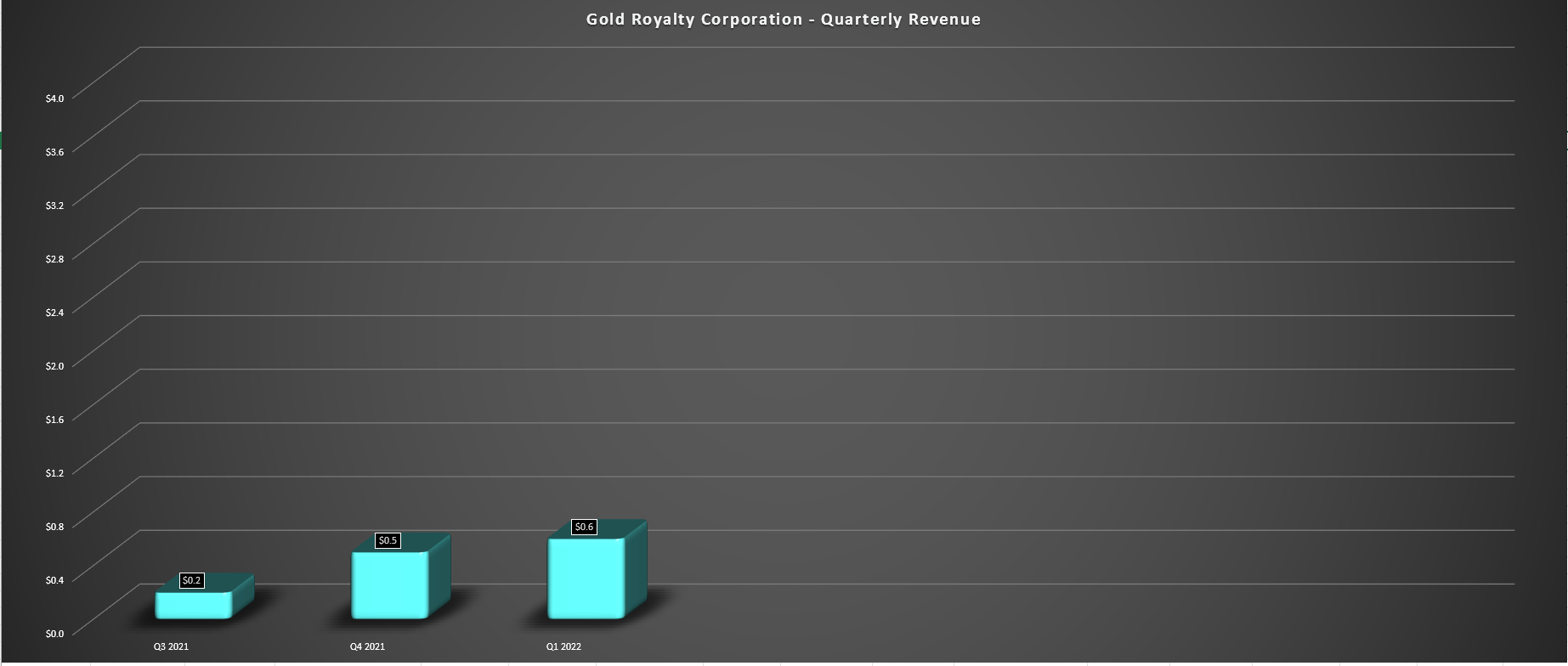

GRC released its fiscal Q2 results in May, reporting a quarterly volume of 302 gold-equivalent ounces [GEOs], a 5% increase on a sequential basis. This translated to $0.60 million in quarterly revenue, a new record for the company, though a paltry figure relative to its market cap (~$457 million). The increase in revenue was driven by its acquisitions of Golden Valley and Ely, which added producing royalties to the portfolio. GRC will also benefit from additional revenue from its 0.50% net smelter return [NSR] royalty on Newmont's ( NEM ) BordenMine in Ontario, where GRC began receiving royalty payments as of July.

GRC - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

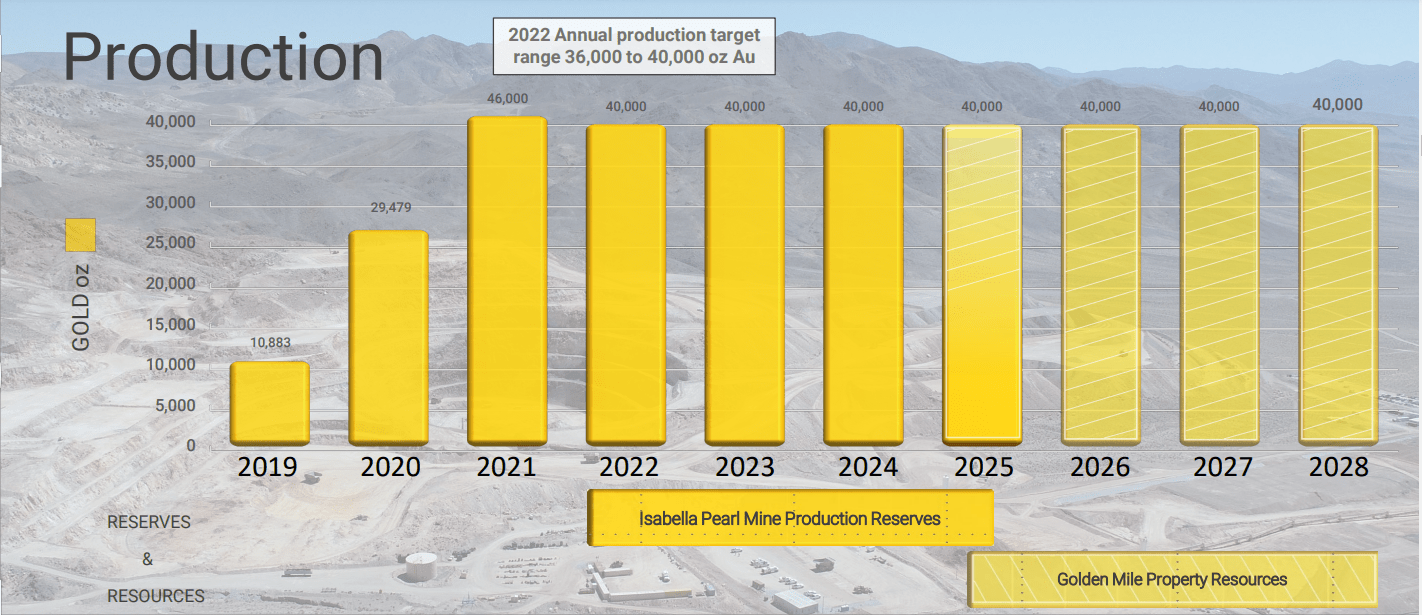

Based on current guidance, GRC expects a meaningful increase in annual revenue, from limited revenue last year to $4.6 million this year at the low end of its forecasts. This figure should have increased materially with the Cote Lake royalty coming online, but when you've got a partner with a track record as poor as Iamgold ( IAG ), it's always best to err on the side of conservative. Based on Iamgold's most recent commentary, commercial production has been pushed to the end of 2023, approximately a 4-month delay vs. its previous view of early H2 2023.

Isabella Pearl Production Estimate (Fortitude Gold Presentation)

{kind=link}

While this royalty on a portion of Cote and the expanded royalties on Monarch's ( GBARF ) now producing Beaufor Mine will boost the near-term revenue outlook, it's worth noting that this will be partially offset by a sharp decline in production at Isabella Pearl beginning in 2025. This is because Isabella Pearl's reserves are expected to wind down, with a plan to switch to Golden Mine to maintain similar production levels. Although GRC has royalties on Mina/County Line, these do not apply to Golden Mile, which appears to be the highest priority asset for Fortitude ( FTCO ). The Isabella Pearl royalty was especially attractive given that it was a gross revenue royalty without any deductions.

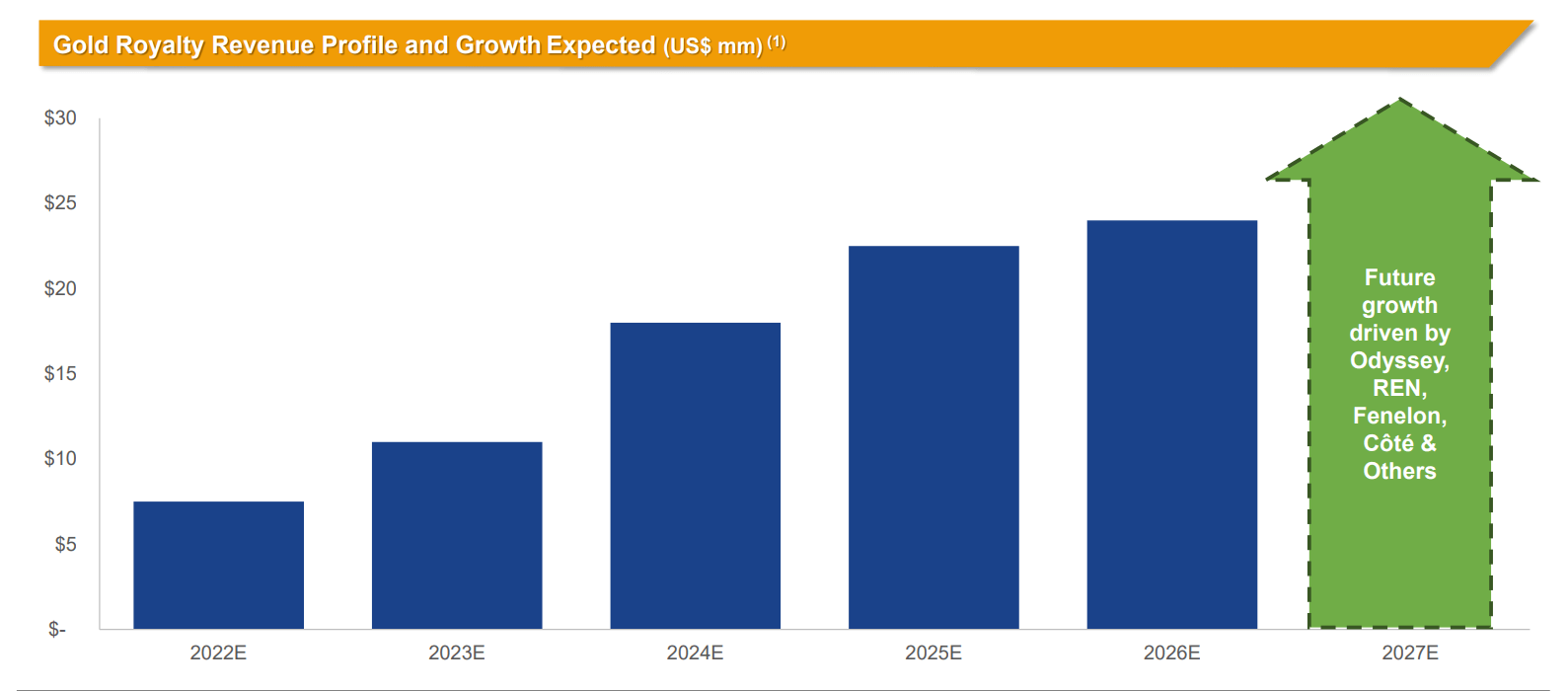

Gold Royalty - Forecasted Revenue (Company Presentation)

{kind=link}

If we look at the long-term revenue profile (above), the outlook is better, with considerable growth expected over the next several years. However, even if the company meets its estimated FY2026 revenue figure of ~$22 million by FY2026, we've still got a company trading at more than 20x 4-year forward sales. Putting this valuation in perspective, Osisko Gold Royalties ( OR ) can be purchased at 11x FY2022 revenue estimates. The best way to value royalty companies is on a P/NAV basis. Still, as discussed later, GRC doesn't stack up great on these valuation metrics either when adjusting for its small attributable production profile. Let's take a look at recent developments below:

Recent Developments

While the fiscal Q2 results left much to be desired with limited revenue generation, GRC has seen some positive recent developments in its portfolio worth highlighting. Before discussing the positive, it's worth discussing the negative, which was a $3.8 million write-down on Rawhide due to working capital constraints of the operator. Fortunately, this was offset by the exciting news that Gold Standard Ventures ( GSV ) received an offer to be acquired. This not only provided a more straightforward path to development for this asset (no financing risk), but it's likely pulled commercial production at the asset up from H2 2026 to H1 2025.

While a positive for GRC, given that it should add a producing asset, the real winner is Maverix Metals ( MMX ). This is because Maverix holds a 2.0% NSR royalty on Railroad-Pinion, while GRC's royalty comes in at just 0.44%. So, while Maverix will receive ~3,100 GEOs per annum from 2026-2029, GRC will receive closer to 700 GEOs per annum on average in the same period. Obviously, this is still a solid boost to revenue, especially given GRC's current GEO volume profile (~3,500 GEO estimate in 2023),. Still, it's considerably less from a revenue standpoint than Maverix will enjoy.

Jerritt Canyon Mine (First Majestic Presentation)

{kind=link}

The last piece of news worth reporting is that First Majestic ( AG ) has announced that it will ramp up production at Jerritt Canyon, potentially increasing throughput to as high as 3,800 tonnes per day by 2024, boosting annual production to ~170,000 ounces per annum. This would nearly double the annual production profile and help GRC's sliding scale per ton royalty on the asset. Assuming a 170,000-ounce production profile vs. ~100,000 ounces in FY2022, this would translate to an additional 350 GEOs attributable to GRC or another ~$0.6 million in revenue.

To summarize, while GRC looks to have lost its Rawhide 15% NPI temporarily and will see contributions from Isabella Pearl wind down by H2 2024, the company will see new contributions from Beaufor, Borden, and Cote going forward. It will also see a boost from Jerritt Canyon in 2024 and Railroad Pinion potentially as early as Q2 2025. Hence, its growth profile looks more believable, with the potential for up to 10,000 GEOs per annum by 2027. The next key catalyst will be more clarity on Barrick's ( GOLD ) Ren deposit, which could be tied into the Carlin Complex sometime in the next few years.

Valuation

Based on ~155 million fully diluted shares and a share price of US$2.95, GRC trades at a market cap of $457 million. While this might appear cheap for a company with nearly 200 royalties, it's important to note that the bulk of the portfolio (170 assets) is concentrated in exploration royalties that, in many cases, will amount to limited revenue over the next decade. For this reason, there's little value to these assets, especially when discounted out at a 5% discount rate. If we focus solely on the producing/development royalty portfolio (28 assets), which has more visibility, I have estimated a net asset value of ~$445 million, translating to a fair value of $2.87 per share at a 1.0x P/NPV multiple.

However, royalty companies often command a premium valuation to NPV (5%) given their low-risk business models, and I think a reasonable multiple for GRC, given its lack of diversification (8 producing assets) and small scale (sub 5,000 attributable GEOs in 2023) is 1.20x. Based on this multiple, I see a fair value for GRC of $3.44, or a 17% upside from current levels. This multiple is slightly below the peer average, given that there is limited long-term visibility into future production from Isabella Pearl or Rawhide, and the development portfolio is quite concentrated with one developer - GoldMining Inc. ( GLDG ). The latter means less money spent per project and a staggered development schedule if any assets ever do go into production.

I discussed this issue in my earliest article on GROY, which is why I thought it best to avoid the stock. The reason was that most royalty companies partner with one developer on their #1 or number #2 asset and partner with several developers, meaning that there can be lumpy years when many assets are heading into production at once. In GRC's case, several assets are held by a single company, meaning it won't benefit from this diversification.

So, is the stock a Buy?

While a 17% upside might be attractive to some investors, I want a much larger margin of safety when buying small-cap precious metals stocks. Generally, the minimum discount to a company's fair value I am looking for is 40%, but I will make exceptions at 35% in the case of companies with exceptional management and a phenomenal portfolio relative to peers. Given that I do not believe GRC's portfolio is superior to its closest peers, a 40% discount to fair value would mean that the stock would need to decline to $2.06 for me to become interested in the stock. So, while the froth has certainly come off the stock vs. when it was being hyped up on social media regularly last fall, I still see far better value elsewhere in the sector.

Summary

While a couple of recent developments have improved GRC's outlook (Gold Standard offer, Jerritt Canyon production increase), I was already modeling the latter given that it was discussed by First Majestic management, and the real beneficiary of the GSV deal is Maverix, with a royalty that's 350% larger (2.0% NSR vs. 0.44% NSR). So, while these recent developments don't hurt, they aren't game-changers. Meanwhile, we are seeing some major developments elsewhere, such as Royal Gold ( RGLD ) boosting its growth profile (Great Bear/Cortez) and Osisko GR's outlook at Canadian Malartic [CM] improving with each quarterly update, with it owning a massive royalty on the most attractive Malartic claim block - East Gouldie [EG].

Given that Canadian Malartic is the most attractive royalty held by GRC and Osisko GR also holds royalties on CM but the best deposit [EG], I continue to see it as the superior way to get exposure to this asset. This is especially true given that Osisko GR also holds a royalty on the Kirkland Lake Camp (recently consolidated). Plus, its growth will come from multiple assets with greater visibility into production start dates. Most importantly, though, it trades at a similar valuation to GRC, despite a 20x larger production profile. Hence, I see GRC as an Avoid at $2.95, preferring to invest in great companies when the sector is on sale, not average companies that trade at relatively small discounts to fair value.

For further details see:

Gold Royalty: Valuation Beginning To Improve