GDEN - Golden Entertainment: Successful Divestitures And Cheap

2023-12-12 18:31:53 ET

Summary

- Golden Entertainment has delivered better-than-expected quarterly earnings and is expected to see FCF growth in 2024 and 2025.

- The company operates a diversified entertainment platform, including 8 casino properties and distributed gaming operations.

- Golden's focus on marketing, loyalty programs, and employee growth may lead to new net sales growth, but it faces risks from legal compliance and intense competition.

Golden Entertainment, Inc. ( GDEN ) delivered better than expected earnings results , and many analysts out there are expecting FCF growth in 2024 and 2025. Considering the recent divestitures made at very decent valuations, I would be expecting a successful reshape of the balance sheet, which may make the stock more appealing. Additionally, successful reward programs, customer database assessment, and headcount growth could bring new net sales growth. There are many risks related to legal compliance and intense competition. The debt is also not small. With that, I think that GDEN does appear cheap.

Golden Entertainment

Golden Entertainment was established in 1998 in Minnesota. Headquartered in Las Vegas, it operates a diversified entertainment platform, highlighting 8 casino properties in Nevada and Maryland. Additionally, it manages distributed gaming operations, including slot machines at various locations in Nevada and Montana.

Company’s focus includes brand-name taverns in the greater Las Vegas area. The company, publicly trading since 1999, has transformed itself to offer a comprehensive entertainment experience, merging casinos, distributed gaming, and taverns.

Golden excels in marketing its Nevada Casino Resorts, taking a comprehensive approach that encompasses local and regional advertising. Its strategy focuses on offering a complete tourist destination experience, from rooms to entertainment, restaurants, and attractions. It uses various media channels such as television, radio, outdoor, digital, social media, and public relations. In addition, it focuses the marketing of local casinos in Nevada towards local communities, highlighting the gaming experience, promotions, and gastronomy.

The company also focuses on attracting local and regional customers, highlighting outdoor amenities and activities. Its Nevada Taverns and Distributed Gaming segments seek to maximize profitability through strategic marketing efforts and a robust loyalty program, True Rewards.

With that about the business model, I believe that it is a great moment for reviewing the valuation of Golden mainly after the better-than-expected quarterly earnings results. In November 2023 , Golden reported sales close to $257 million with EPS GAAP close to $7.8.

Source: SA

Numbers from other investment analysts seem also quite beneficial. Even with lower net sales growth expected in 2024 and 2025, analysts are expecting FCF growth in 2024 and 2025. 2025 free cash flow is expected to be close to $132 million with net margin close to 7.3% and operating margin of about 13%.

Source: S&P

Competitors

In my opinion, Golden faces intense competition in the industry. In the casino sector, it competes with a wide range of establishments of different sizes and quality as well as non-gaming resorts. Competition varies in resources, brand recognition, and financial capacity, presenting significant challenges. The possible legalization of casino gaming in nearby areas and the expansion of Native American casinos also pose threats. In the area of ??taverns and distributed gaming, competition comes from diverse operators and the growing presence of online games. Moreover, alternative forms of entertainment pose additional challenges.

Golden Reports A Significant Amount Of Properties

In the last quarterly report, Golden reported cash and cash equivalents of about $261 million, accounts receivable close to $16 million, total current assets of $507 million, and total assets of $1.54 billion.

With property and equipment worth about $808 million, the largest assets are properties, which I believe are real estate and excess land in good areas in Las Vegas. Management discussed these assets in the last presentation reported in November.

The asset/liability ratio stands at more than 1x, and the total amount of long term debt appears lower than the total amount of property. Hence, I do think that the balance sheet appears stable. With that, I believe that studying the list of debt obligations and the WACC is beneficial to design the DCF model.

Current portion of long-term debt and finance leases stands at close to $4 million, with accounts payable worth $22 million, long-term debt of $716 million, and total liabilities of about $999 million.

Large Loyalty Program With A Significant Number Of Customers

Recently, Golden reported that its rewards program combines a massive database with customers, connected not only to casinos, but also to taverns and chain stores. I believe that data analysis and cross marketing opportunities will most likely bring net sales growth and perhaps FCF margin growth.

In my view, further understanding of the needs of clients will most likely increase the dollars obtained from each customer, which may bring profit margin increases. In this regard, it is worth noting that the profit margin increased in the last twenty years. Future results are usually unrelated to previous history trends. With that, given the previous performance, I would say that Golden is going in the right direction.

Source: YCharts

Successful Employee Training And Retention As Well As Further Employee Growth Will Most Likely Lead To Net Sales Generation

I believe that continued investment in talent development and retention is essential for Golden. The company believes that by creating an engaged environment for its team, it differentiates them and positions them as attractive employers. Employee retention is an essential part of the overall employment strategy. In my opinion, further headcount growth will most likely bring net sales growth and FCF generation. In this regard, previous headcount growth is worth noting.

Source: YCharts

Recent Divestitures May Reshape The Balance Sheet From 2024, Which May Make The Company More Appealing For Investors

Golden agreed to the sale of Rocky Gap for $260 million. The company also noted the sale of its Distributed Gaming Operations in Montana and Nevada. Management appears to be looking to reshape its balance sheet, which may bring cash increases in the coming months. If the net debt lowers, we may see increases in the fair valuation of Golden. It is also worth noting that the company is selling divisions at close to 9x-10x EBITDA, which is a bit more expensive than its current trading multiple. I believe that the sale of these divisions was done at beneficial prices.

Source: YCharts Source: Investor Presentation

Further Share Repurchases And Reduction In The Share Count Could Lead To Higher Fair Price

In the last quarterly report, Golden noted that management may deliver open market transactions, and block trades in the coming future. It is worth noting that the company continues to have remaining share repurchase availability. I believe that further repurchase of stock could lead to demand for the stock.

"On July 27, 2023, the Company’s Board of Directors increased its share repurchase program to $100 million. Share repurchases may be made from time to time in open market transactions, block trades or in private transactions in accordance with applicable securities laws and regulations and other legal requirements, including compliance with the Company’s finance agreements. As of September 30, 2023, the Company had $90.9 million of remaining share repurchase availability under its July 27, 2023 authorization." Source: Quarterly Report

Source: YCharts

Expectations Based On Previous Assumptions And Previous Financial Statements

My income statement expectations were mainly based on previous income statements and the assumptions recently noted. I assumed growth in gaming, food and beverage as well as revenue growth from rooms. I included net sales growth from 2023 to 2033 close to 24% and 6% and median revenue growth close to 7.86%, which I believe is conservative.

In particular, I included 2032 gaming of $1.933 billion, food and beverage of about $451 million, rooms of $355 million, others worth $202 million, and total revenues of about $2.941 billion.

With 2032 expenses from gaming of $1.090 billion, food and beverage worth $319 million, rooms close to $229 million, and selling, general, and administrative of close to $685 million, I did not take into account loss on disposal of assets, pre-opening expenses, impairment of goodwill, and intangible assets, so total expenses would be close to $2.394 billion. 2032 operating income stood at $547 million. Additionally, with interest expense of -$42 million and total non-operating expense of about -$51 million, I obtained 2032 net income of $494 million.

Source: My Own Figures

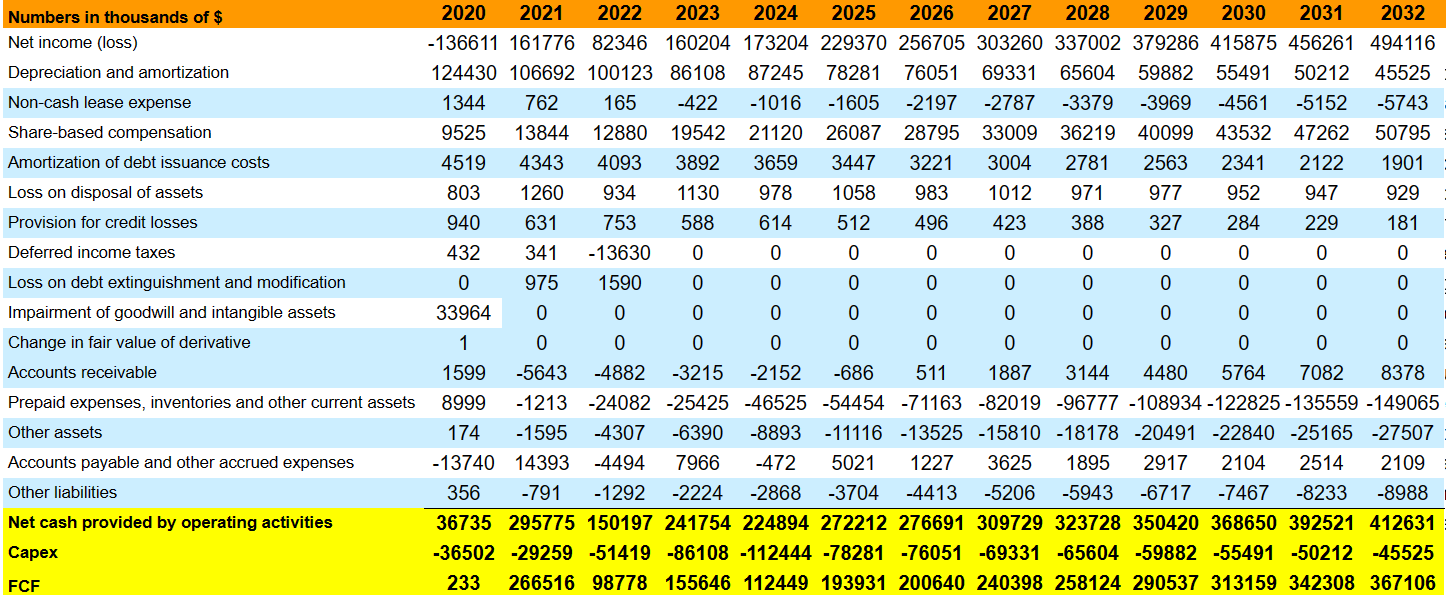

My cash flow expectations included 2032 net income of close to $479 million, non-cash lease expense of close to -$6 million, share-based compensation of about $50 million, and amortization of debt issuance costs of $1 million. Besides, with changes in inventories and other current assets of -$150 million, changes in accounts payable and other accrued expenses of $2 million, and changes in other liabilities of -$9 million, net cash provided by operating activities stood at $397 million. Finally, with 2032 capex of -$46 million, 2032 FCF would imply $352 million.

{kind=link}

EV/FCF Valuation Multiples, WACC, And Fair Valuation

For the DCF model, I studied the interest rate included in the credit agreement signed by Golden. The loans depend on the SOFR rate and a margin of about 0.5%, 1%, 2%, and 2.50%. The weighted average rate was said to be close to 8.11% and 7.85%, so I assumed a WACC of about 8%-12%.

"Under the Credit Facility, the Term Loan B-1 bears interest, at the Company’s option, at either a base rate determined pursuant to customary market terms (subject to a floor of 1.50%), plus a margin of 1.75% or the Term SOFR rate for the applicable interest period plus a credit spread adjustment of 0.10% (subject to a floor of 0.50%), plus a margin of 2.75%, and borrowings under the Revolving Credit Facility bear interest, at the Company’s option, at either a base rate determined pursuant to customary market terms (subject to a floor of 1.00%), plus a margin ranging from 1.00% to 1.50% based on the Company’s net leverage ratio, or the Term SOFR rate for the applicable interest period plus a credit spread adjustment of 0.10%, plus a margin ranging from 2.00% to 2.50% based on the Company’s net leverage ratio." Source: Quarterly Report

"The weighted-average effective interest rate on the Company’s outstanding borrowings under the Credit Facility was 8.11% and 7.85% for the three and nine months ended September 30, 2023, respectively." Source: Quarterly Report

For the assessment of the exit multiples, I checked the multiples reported by SA and the multiplied reported by Golden. In the past, Golden traded at close to 16x, 21x, and 26x FCF.

Source: YCharts

The EV/Sector Median EBITDA stands at close to 9.7x, and Price/Cash flow stands at about 8.37x. With these figures, I assumed exit multiples close to 7x-13x FCF, which I believe are conservative.

Source: SA

With FCF between $156 million and $352 million from 2023 to 2032, WACC of 8.1%-12.1%, and EV/FCF of 7x-13x, I obtained an implied valuation without debt of $1.6-$3.36 billion. Note that I included cash close to $261 million, and subtracted short term debt, long term debt, and other long-term obligations.

Source: Qingshan Capital Management

Additionally, my forecast price obtained stood between $58 and $117 per share, with a median close to $83-$84 per share. Besides, I obtained an internal rate of return between 5% and 21% and a median IRR of 12%. With these figures, I believe that Golden appears a bit undervalued.

Source: Qingshan Capital Management

Risks

The company faces significant risks related to handling substantial amounts of cash and complying with anti-money laundering laws. Violations of these laws could have adverse business consequences. The possibility of government investigations and legal sanctions poses additional threats. The gaming industry is subject to state and local taxes, and changes in tax laws may negatively impact revenue. Economic conditions and state budget deficits can lead to tax increases. The uncertainty in this legal and tax environment presents significant risks to the company's future.

My Takeaway

Golden Entertainment demonstrates a strong position in the entertainment and gaming industry. Its focus on the complete tourism experience, diversified marketing, and customer loyalty reinforces its competitive position. Divestitures are expected to reshape the balance sheet, and enhance the valuation of the stock as cash in hand may increase. Additionally, like other analysts, I am also expecting an increase in free cash flow thanks to further successful reward programs, customer database assessment, and headcount growth. Golden faces significant risks related to legal compliance and intense competition, and the total amount of debt is not small. With that, I believe that the stock is cheap.

For further details see:

Golden Entertainment: Successful Divestitures, And Cheap