GOGL - Golden Ocean Group: Buy This Stock For Solid Dividend And Upside

2023-09-19 03:52:06 ET

Summary

- Golden Ocean is a global dry bulk shipping company that has recently experienced a downturn in its financials due to macroeconomic pressures.

- The company can sustain dividend payments as a result of the gradual rebound in the industry demand, which makes the annual dividend $0.40, representing a dividend yield of 5.20%.

- Despite the risk of fluctuating charter rates, the stock is undervalued and has the potential for 29.29% growth, with a decent dividend yield.

Investment Thesis

Golden Ocean ( GOGL ) is a global dry bulk shipping company that deals in the supply of essential commodities used in farming, manufacturing, and energy industries. It has recently experienced a downturn in its financials as a result of macroeconomic pressures. However, I believe it can rebound in the coming quarters as a result of positive industry dynamics and its increased vessel capabilities.

About GOGL

GOGL is dry bulk shipping company that deals in supplying essential commodities used in farming, manufacturing, and energy industries. These commodities mainly consist of grains, coals, ores, and fertilizers. Its fleet of dry bulk vessels is made up of Newcastlemax, Capesize, Ultramax, and Panamax vessels. The company owned 74 dry bulk vessels as of March 16, 2023, and construction contracts for 10 newbuildings. However, now it owns 84 vessels through its acquisitions. The company conducts its business in one reportable segment. Its business is operated through its subsidiaries located in Liberia, Bermuda, the Marshall Islands, Singapore, Norway, and the UK. It generates its revenues through time charter, voyage charter, and other activities. The time charter revenue contributed approximately 53.32% to the company’s total revenues in 2022. The voyage charter revenues accounted for 46.55% of the total revenues and the rest 0.11% of revenue was derived from other activities. In February 2023, the firm acquired six scrubber-fitted Newcastlemax vessels for $291.0 million.

Financials

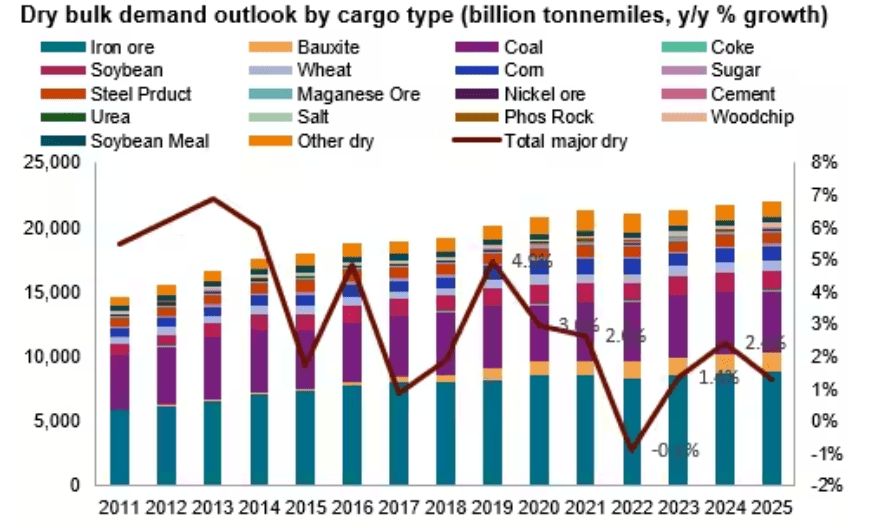

The shipping industry was negatively impacted after the Russia-Ukraine war due to restricted supplies of energy commodities. Further, this decline was also fueled by global macroeconomic and inflationary pressures. However, the scenarios are changing gradually and the demand is rebounding in the industry due to the development of various economies, shifting trade routes, and the increased need to secure the energy supply chains. In 2023, the dry bulk demand can surge by 1.4% with the resurgence of coal and iron ore shipments. Further, this demand is expected to grow by 2.5% in 2024. The Capesize market delivered strong growth in the year and it is projected to even grow further because of growing bauxite volumes in West Africa as the rainy season is over. In addition, the Indian coal flow is also expected to increase with the end of the monsoon. The Panamax market also has strong growth prospects due to good corn crops in Brazil and USA . Identifying these positive industry trends, the company has increased its vessel capabilities significantly. During the second quarter, it received deliveries of three Newcastlemax vessels and four Kamsarmax vessels as per its February 2023 acquisition. These acquisitions of vessels can act as a catalyst to accelerate the company’s growth as it can make it well-positioned to transport more commodities and capture the rapidly growing demand. In addition, its new, young, and highly fuel-efficient fleet can also enable it to create a strong competitive presence to secure more contracts. The company also has low cash breakeven levels which makes it highly resilient. As per my analysis, it can sustain this growth for a longer period and can gain a stable competitive presence in the market as the shipping industry has high entry barriers due to its capital-intensive nature and high regulatory operations.

Dry Bulk Demand Outlook by Cargo Type (S&P Global Commodity Insights)

{kind=link}

The company recently reported its quarterly results. It reported an operating revenue of $213.38 million, down 32.61% compared to Q222. This decline mainly resulted from adverse macroeconomic conditions. Net income dropped by 78.69% YoY from $163.74 million to $34.89 million. It reported a basic EPS of $0.17. It reported adjusted EBITDA of $80.40 million. GOGL reported $107.3 million in liquidity and long debt stood at $1.25 billion.

Share of Global Bauxite Trades in Capsize demand (Investor Presentation: Slide No:12)

The company experienced a downturn due to macroeconomic pressures, however, I believe it can rebound in the third quarter as it has received the deliveries of the acquired vessels which can help it transport more commodities and increase its profitability by making it well-positioned to cater to the growing demand in the industry.

Dividend Yield

{kind=link}

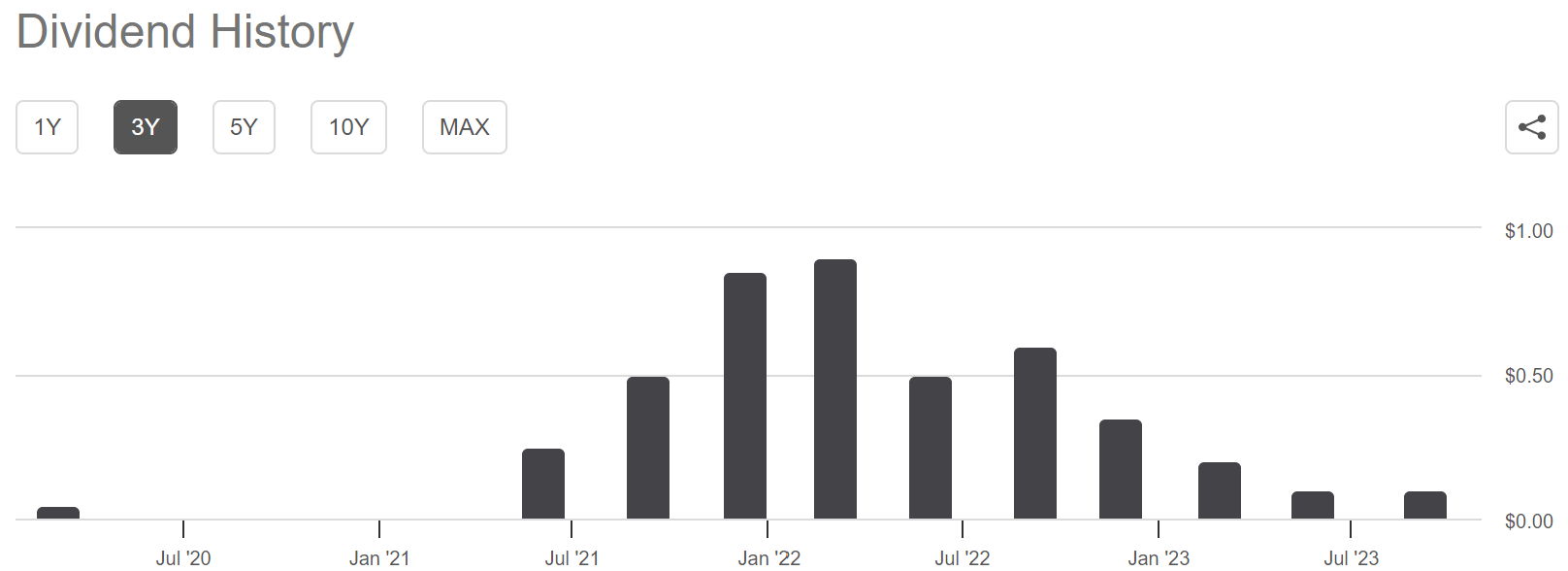

The company has regular dividend payouts which indicates its healthy positioning. In FY2022, it paid an annual dividend of $1.65 per share which included four quarterly dividends of $0.50, $0.60, 0.35, and $0.20 respectively. The dividend yield on this payout was 21.48%. However, it was impacted by its setback in FY2023. In FY2023, it paid a cash dividend of $0.10 in the first two quarters each and I believe it can sustain this dividend for the next two quarters as a result of the gradual rebound in the industry demand and its increased vessel capabilities which makes the annual dividend $0.40, representing a forward dividend yield of 5.20%. Even with the declined dividend payment, the company offers a solid forward dividend yield compared to the current share price. As per my analysis, the company can increase its cash flows steadily through its increased fleets and can increase its dividend payout over the years. This makes the company an attractive stock to hold in the portfolio.

What is the Main Risk Faced by GOGL?

The dry bulk shipping industry experiences cyclicity and the charter rates are highly volatile. The fluctuations in the charter rates are influenced by changes in the supply and demand of vessel capacities, as well as changes in the demand for major commodities that are supplied by water globally. In addition, global economic trends also influence the charter price. Its vessels are primarily chartered on the spot market, which is exposed to cyclicity and volatility. If the charter hire rates decline, it can negatively impact the company’s revenue and can contract its profit margin.

Valuation

The industry demand is expected to grow at healthy levels which can create opportunities for the company. It has recently received deliveries of its acquired vessels which can increase its transporting capabilities and help it to serve additional customers by increasing its profitability. After considering all the above factors, I am estimating EPS of $0.50 for FY2023 which gives the forward P/E ratio of 15.36x. After comparing the forward P/E ratio of 15.36x with the sector median of 19.85x, we can say that the company is undervalued. I believe the company might grow in the coming quarters as a result of positive demand in the industry and its increasing vessel capabilities which can help it to trade at its sector median. Therefore, I estimate the company might trade at a P/E ratio of 19.85x in 2023, giving the target price of $9.93, which is a 29.29% upside compared to the current share price of $7.68.

Conclusion

GOGL experienced downturn in its performance as result of macroeconomic pressures, however, it can potentially rebound in the coming quarters as demand in the industry is expected to increase and it has also received delivery of its acquired vessels which makes it well-positioned to transport more commodities and cater to rapidly growing demand. It is highly exposed to risk of fluctuating charter rates which can contract its profit margins. The stock is undervalued and we can expect healthy 29% growth from the current price levels as a result of its increased vessel quantities that can help to serve additional customers. It also pays a decent dividend which makes it an attractive stock to hold in a portfolio. After considering all the above factors, I assign a buy rating to GOGL.

For further details see:

Golden Ocean Group: Buy This Stock For Solid Dividend And Upside