GOGL - Golden Ocean Group: Eradicating COVID-19 From China Is About To Hurt

Summary

- Golden Ocean Group was the metaphorical golden goose for shareholders with massive dividends during 2021 and early 2022.

- Although sadly, it now appears to be inflicted with Covid-19 as China battles to eradicate cases from their country.

- This is hindering demand for dry bulk shipping at the same time that port congestion eases, thereby sending rates plunging.

- Once this flows through to their company later in the year, their leverage will surge to concerning levels and see their dividends plunge.

- Since there is seemingly more downside risk than upside potential, I believe that maintaining my sell rating is appropriate.

Introduction

The booming operating conditions within the dry bulk shipping industry during the last twelve months saw Golden Ocean Group ( GOGL ) as the metaphorical golden goose for shareholders with massive dividends. Although these extremely profitable times cannot last forever and thus back several months ago, it was seemingly time to abandon ship with the best days over, as my previous article warned. Whilst their subsequent financial performance was surprisingly strong and saw their massive dividend yield of 20%+ continue for another quarter, structural issues have not been resolved and if anything, they have worsened and unfortunately, eradicating Covid-19 from China is about to hurt their free cash flow and thus their dividends.

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing dividend coverage through earnings per share cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

{kind=link}

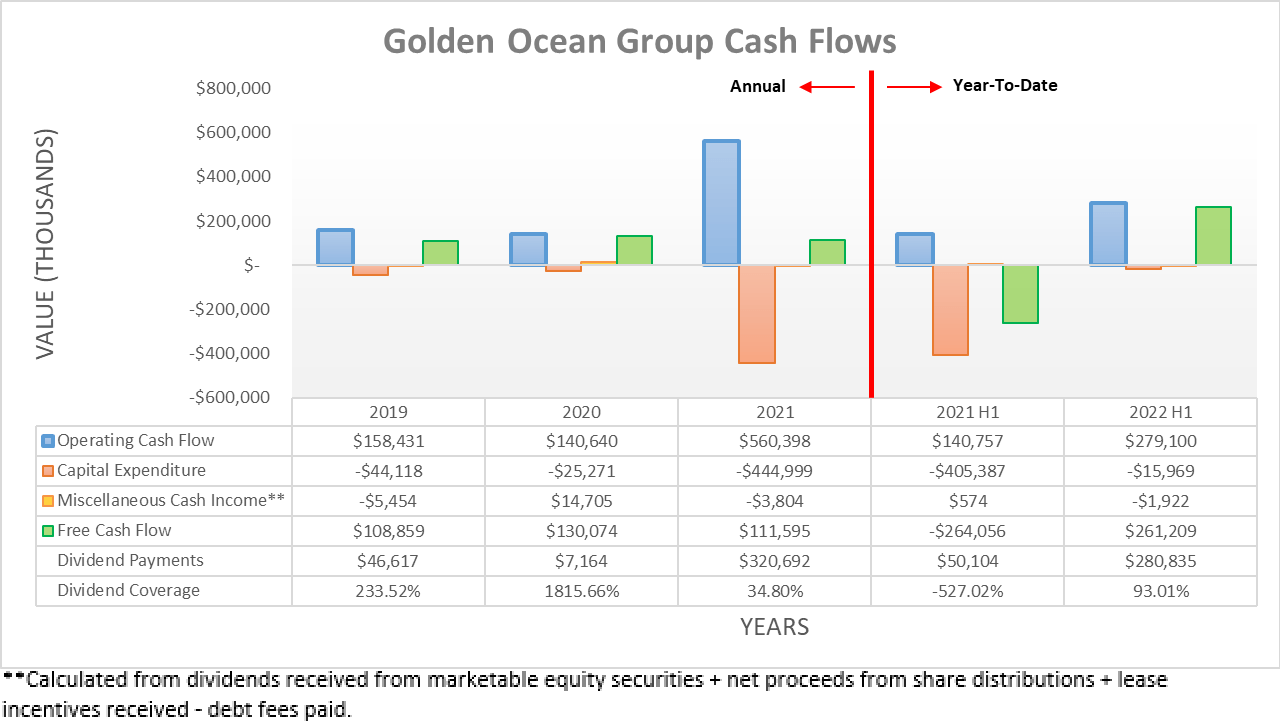

After seeing their cash flow performance soften during the first quarter of 2022 versus the fourth quarter of 2021, as discussed within my previously linked article, their result for the second quarter of 2022 was surprisingly strong. In fact, their operating cash flow climbed to $279.1m for the first half with the second quarter alone representing $155.5m and thus modestly higher than the $123.6m from the first quarter. Despite being better than expected and resulting in their variable quarterly dividends increasing to $0.60 per share, the risks on the horizon have not been alleviated and if anything, they have actually worsened.

Virtually every investor would already know that China is the single biggest and thus most important market for the seaborne trade of dry bulk goods, such as iron ore and coal. Their economic resilience during 2020 and 2021 as Western countries battled Covid-19 fuelled demand for dry bulk shipping in 2021 and early 2022 but alas, it appears that these fortunes are swinging the other way. Even though the pandemic seemingly became a background story throughout the West, the same cannot be said for China, which is sticking with their zero Covid-19 policy that continues to see millions of people in lockdown.

Unsurprisingly, this policy is compounding issues within their heavily indebted property sector and hindering economic activity. By extension, this is hindering dry bulk shipping rates at the same time as port congestion is clearing, thereby sending spot rates for their Capesize vessels plunging to sub-$10,000 per day by mid-August, which was far below their cash breakeven of $13,000 per day, as per slide eight of their second quarter of 2022 results presentation. Despite September seeing a rally, the Baltic Exchange Dry Index that tracks dry bulk shipping vessels remains a shadow of where it was one year ago, as per the graph included below.

Trading Economics

Earlier in the year, it was hoped that China would relax their zero Covid-19 policy but alas, this did not transpire and according to the analysts at Goldman Sachs ( GS ), they are likely to keep this heavy-handed approach into 2023. Unless they reverse course unexpectedly, this will see the pressure levied upon their economy continue for the foreseeable future, which is certainly not a positive outlook for dry bulk shipping that is clearly already seeing tough times.

They recently announced new a stimulus program but given its relatively minor $44b size, it is only topping up their earlier same-sized program. As a result, it does not offer much assistance to their construction industry that ultimately drives demand for dry bulk shipping and thus, it could be said that commodity markets were not impressed . Whether they announce further stimulus programs is uncertain but considering their famous ghost cities that have arisen from earlier massive stimulus programs, I am skeptical that throwing more money at stimulus is the answer in the medium to long-term.

Admittedly, their fleet sees strong contract coverage of 80% and 96% for their respective Capesize and Panamax vessels during the third quarter of 2022, although this quickly drops to only 25% and 27% respectively during the fourth quarter, as per slide fifteen of their previously linked second quarter of 2022 results presentation. If these weak spot market rates persist, which is certainly not impossible given this outlook, their financial performance is set to deteriorate rapidly as the end of the year approaches and thus, 2023 could see a downturn.

{kind=link}

Following the second quarter of 2022, their net debt edged slightly lower to $1.182b versus when conducting the previous analysis following the first quarter when it was $1.278b. Notwithstanding this improvement, it remains higher than its previous level of $1.086b at the end of 2020, where it was before the recent booming operating conditions. If removing their leases, it would have ended the second quarter of 2022 at $1.033b, which is barely lower and when compared to their previous level of $892.4m at the end of 2020, it is actually higher and thus no matter how their capital structure is viewed, it is more indebted than before the booming operating conditions of 2021 and early 2022.

{kind=link}

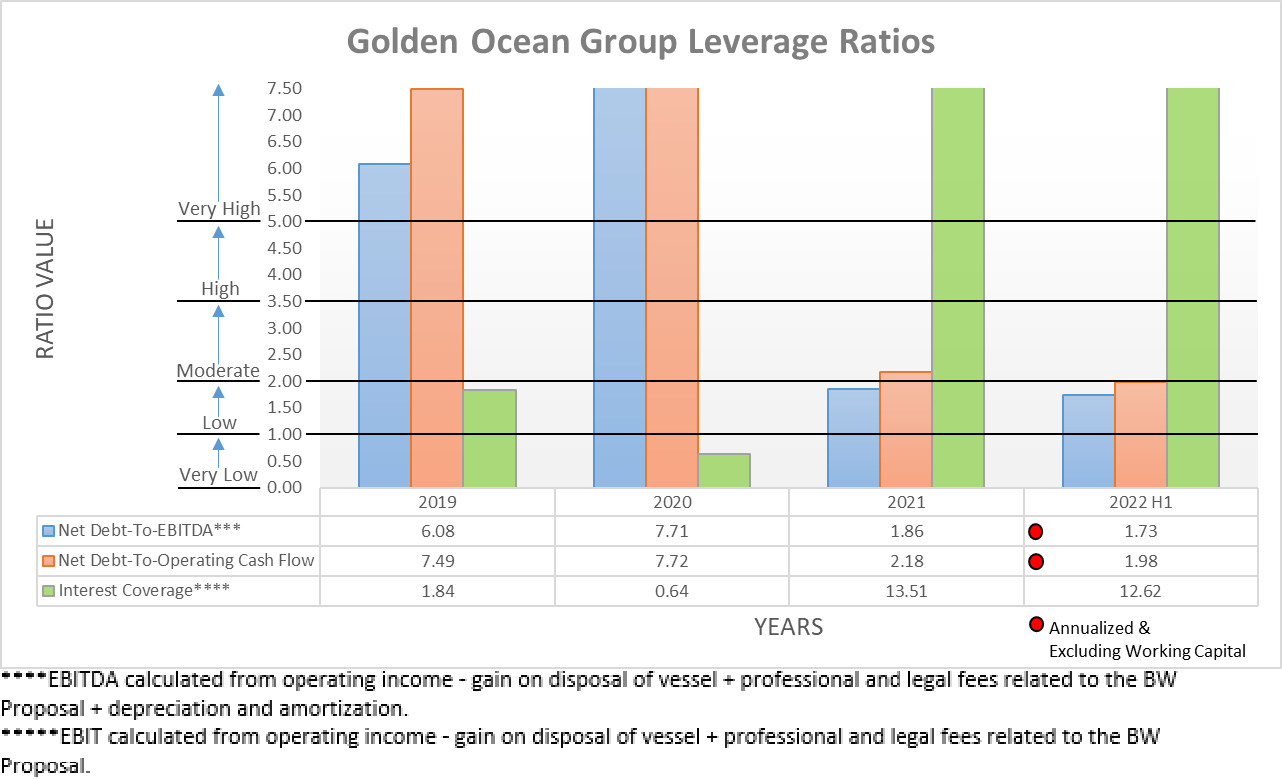

Thanks to their surprisingly strong financial performance during the second quarter of 2022, their leverage decreased more than expected with their respective net debt-to-EBITDA and net debt-to-operating cash flow down to 1.73 and 1.98. Apart from representing a modest decrease versus their previous respective results of 2.14 and 2.46 when conducting the previous analysis following the first quarter, they are now also within the low territory of between 1.01 and 2.00.

Whilst this obviously poses no issues right now, the words "right now" should be emphasized because they are vulnerable since they did not utilize their recent cash windfall to reduce their net debt versus previous years. To provide an example, the end of 2020 saw their respective net debt-to-EBITDA and net debt-to-operating cash flow at 7.71 and 7.72 and thus well above the threshold of 5.01 for the very high territory, which is still evident when looking back at the end of 2019 that saw respective results of 6.08 and 7.49. Despite having a healthy financial position at the moment, it rests solely upon their booming financial performance and sadly, not long-term solid fundamentals. The future remains uncertain but this nevertheless highlights that their fortunes can turn on a dime and could make deleveraging a priority in the future, which would be toxic for dividends in the short to medium-term since it would likely coincide with less free cash flow.

{kind=link}

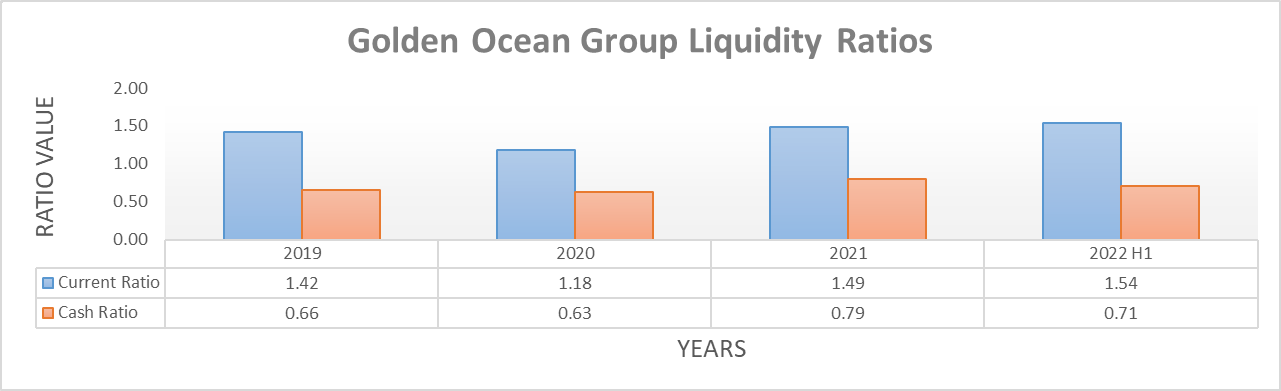

Despite the concerning outlook for their leverage, thankfully their liquidity appears strong with their respective current and cash ratios at 1.54 and 0.71 following the second quarter of 2022, thereby modestly above where they ended the first quarter at 1.21 and 0.44 respectively. Even though this means that they face no immediate solvency issues during 2023 from even a severe downturn, if looking into 2024 and 2025, they see large $200m+ debt maturities in each year, as per slide eight of their previously linked second quarter of 2022 results presentation. When combined with their accompanying guidance for circa $150m of capital expenditure during 2023, any potential forthcoming downturn could quickly drain their cash balance of $164m and credit facility that only retrains another $100m of availability, thereby enhancing the risks if their liquidity depletes.

Conclusion

At the end of the day, no one can necessarily see the future but at the moment, their outlook is not promising with China fighting to eradicate Covid-19 from their borders whilst only providing relatively minor stimulus. This makes further weakness in dry bulk shipping rates likely and once their strong contract coverage ends in the coming months, their financial performance will very likely deteriorate rapidly and see their leverage surge towards concerning levels. When combined, this should almost certainly see their dividends plunge, which makes for more downside risk than upside potential and thus I believe that maintaining my sell rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Golden Ocean Group's SEC Filings , all calculated figures were performed by the author.

For further details see:

Golden Ocean Group: Eradicating COVID-19 From China Is About To Hurt