GOGL - Golden Ocean Group: The Baltic Dry Index Points Toward A Lower Profitability Outlook

2024-01-02 20:17:08 ET

Summary

- Golden Ocean Group has experienced a solid annual total return of ~28% due to vessel supply shortages and increased demand for dry bulk shipping.

- The volatility in the Baltic Dry Index, which measures global dry bulk shipping rates, may impact GOGL's performance as it falls from its recent high.

- The company's valuation and yield may be stretched, and investors should remain attentive to its profitability outlook and the impact of trade strain.

- Golden Ocean should not be materially impacted by the issues in the Red Sea as long as that situation does not continue to escalate.

Nearly one year ago, I published my bullish outlook for the dry bulk shipping giant Golden Ocean Group ( GOGL ). At that time, I believed that long-term supply constraints would offset lower shipping demand, encouraging higher rates and greater profitability. It also appeared that the reopening of China's economy and geopolitical changes in shipping trends would lead to slightly higher demand in many areas. For the most part, that view has proven correct as GOGL has risen by ~21% in value, delivering a solid annual total return of ~28%. Key bullish factors have been the vessel supply shortage and increased demand for iron and coal from China , encouraging a solid spike in the Baltic Dry Index .

As we begin the new year, it is an ideal time to look closely at stocks that experience significant volatility, like GOGL. With global shipping issues rising again due to the situation in the Red Sea, it is also essential to look at shipping stocks individually to see how the trade strain may impact them. Further, long-term investors in GOGL may want to remain attentive to its valuation and yield, which may be stretched today depending on our 2024-2025 profitability outlook.

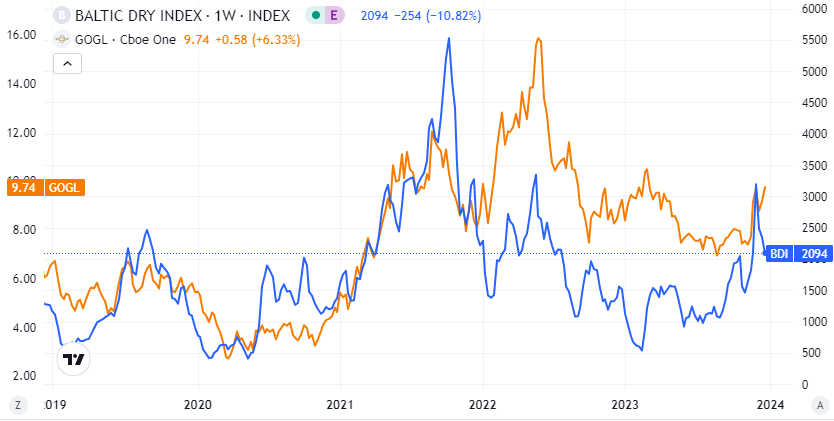

Baltic Dry Index Volatility Rising

Historically, GOGL's price and trend correlate to the Baltic Dry Index, which measures global dry bulk shipping rates. See below:

{kind=link}

The Baltic Dry Index records the cost of moving bulk commodities across the major shipping lanes in the world. The core cause for the rise in the Baltic Dry Index over recent months has been a combination of improved iron ore demand from China and a lower overall supply of shipping vessels. Of course, the index has seen a steep negative correction over the past month, while GOGL has had an excellent performance, potentially due to weakened demand in the Atlantic.

For the most part, the fallout in the Red Sea from Houthi attacks is primarily essential for container shipping stocks that are being targeted. For the most part, dry bulk shippers and tankers have continued to use the Red Sea trade route while container ships are rerouting around Africa. This issue is exceptionally bullish for container companies because it will create a shortage due to longer voyage times. There remains a decent risk that this situation will eventually impact dry bulk shipping in the Red Sea. Further , dry bulk firms are facing a similar issue in Panama due to the canal's drought, creating a significant backlog that is promoting an indirect shortage. Of course, while it is true that any geopolitical issues that block shipping should promote higher rates, they will also increase costs, thus not necessarily improving shipping profitability.

Still, Golden Ocean specifically benefits from higher iron ore exports into China, being a primary global driver of dry bulk demand. After falling earlier in 2023, iron ore prices returned higher in recent months as the government attempted to stimulate construction demand. Total steel production in China remains stagnant , but it is not falling as many had expected as its construction sector becomes more dependent on government stimulus. In the short term, these stimulus efforts have aided China's industrial activity but have not been nearly as effective as in the past. As such, I believe we will eventually see a sharp decline in China's iron ore imports once its government cannot support its substantial property market bubble. Whether or not that will occur in 2024 is unclear, but it is a significant ongoing risk to GOGL, given China is such a large importer of dry bulk commodities.

This demand risk is offset by the long-term supply shortage in dry bulk vessels. For years, the order book to the fleet ratio for dry bulk (and most others) has been shallow as companies reduce CapEx spending. See below:

Dry Bulk Orderbook as Percent of Fleet (Golden Ocean Group Investor Presentation Q3)

To me, this is one of the most significant long-term factors facing the marine industry. The total global bulk shipping fleet has become increasingly stagnant for over a decade. This production crashed in 2020 and has never recovered, leading to a considerable shortage of bulk shipping vessels. Of course, if global demand stagnates or declines, then no shortage should occur. However, we're seeing a general trend toward shortages and higher shipping rates, even with relatively slow demand growth today. As such, I expect that, without a decline in China's import demand, there should be a larger increase in the Baltic Dry Index over the coming years.

What is Golden Ocean Worth Today?

Golden Ocean is challenging to value because many macroeconomic and geopolitical factors influence its profitability today. Current EPS estimates for GOGL have declined since the 2022 peak as global demand has slowed and the acute shortages in 2020-2022 ended. The current EPS estimate is low at just ~$0.50, but that figure is expected to rise to over $1 two years from now. See below:

If we consider a $1.07 EPS in 2025-2026, GOGL's forward "P/E" for that timeframe would be ~9.2X. That is a fair figure, which is lower than many stocks as it discounts risks of a recession negatively impacting its profits. Of course, it is also not a low valuation for the company compared to the past eight years. See below:

The past eight years have been characterized by a general glut in commodities and a glut in shipping vessels. The company's price-to-sales valuation is elevated today, particularly given its operating margins are trending lower. That said, given the low order book ratio, there is a strong probability that Golden Ocean is in a positive super-cycle, which, like the early 2000s, may be characterized by shortages in crucial supply chain segments due to underinvestment. As such, while the risks relating to geopolitical issues and China's economy are high, I believe there could be a positive skew in GOGL's profit potential as this shortage unfolds.

Still, Golden Ocean is particularly expensive compared to its peer group on a forward "EV/EBITDA" basis. See below:

The trend in valuations among these firms is mainly dependent on market size. Golden Ocean is particularly large but will not be the largest once Star Bulk and Eagle Bulk merge . From a value standpoint, Genco ( GNK ) may offer the best overall risk-for-reward tradeoff today, with Golden Ocean potentially overvalued. Of course, it is also a more stable firm due to its larger size, giving it more diverse exposure to various shipping lanes worldwide.

The Bottom Line

Overall, I am neutral on Golden Ocean Group. The stock has seen significant returns since I covered it last and is now trading at a relatively high valuation compared to the range seen in recent years. The company's profits will rise over the coming years as the shortage expands in the dry bulk market.

That said, I believe investors are underappreciating the industry's dependence on China's commodity imports, which could decline substantially as its government struggles to prop up its construction sector. Further, while many view geopolitical events as bullish for the sector, they could also result in a general decline in economic activity and trade over time, hampering long-term growth potential. Thus, GOGL faces a mixed bag of positive and negative factors. While a long-term bullish view is justifiable due to shortages, I personally would wait for a better price point due to the immediate downside risk relating to China's import volatility.

For further details see:

Golden Ocean Group: The Baltic Dry Index Points Toward A Lower Profitability Outlook