GSBD - Goldman Sachs BDC: Still A Buy

2023-11-13 11:28:30 ET

Summary

- Goldman Sachs BDC reported its second consecutive quarter of NAV growth, reinforcing my previous buy rating.

- Shift in portfolio holdings towards higher-risk categories raises caution, but no further migration into category 3 is positive.

- The continued rise in NII means that the dividend is well-covered and increases the likelihood of a special dividend being paid.

Earlier this year I rated Goldman Sachs BDC ( GSBD ) a buy. At the time, I observed that, despite a historical decline in net asset value ((NAV)) per share, the then-recent 1% increase in the second quarter suggests a potential reversal of the NAV decline trend. However, I cautioned that a single quarter's improvement may not conclusively indicate a sustained reversal and that close monitoring would be required. Goldman Sachs BDC has now reported a second consecutive quarter of NAV growth which further reinforces the buy rating.

I also observed that the company's shift in portfolio holdings towards a higher-risk category 3, representing investments facing increased risk and potential covenant non-compliance, raised concerns. While management attributed this to liquidity pressures in specific holdings, I cautioned that close monitoring is necessary to assess the impact on the overall investment thesis. This is one area that still merits particular close monitoring as the recent results have again shown some of the earlier identified risks with an increase in non-accruals and a further increase in the percentage of its portfolio regarded as being at a heightened risk of default.

Portfolio Quality and Net Asset Value

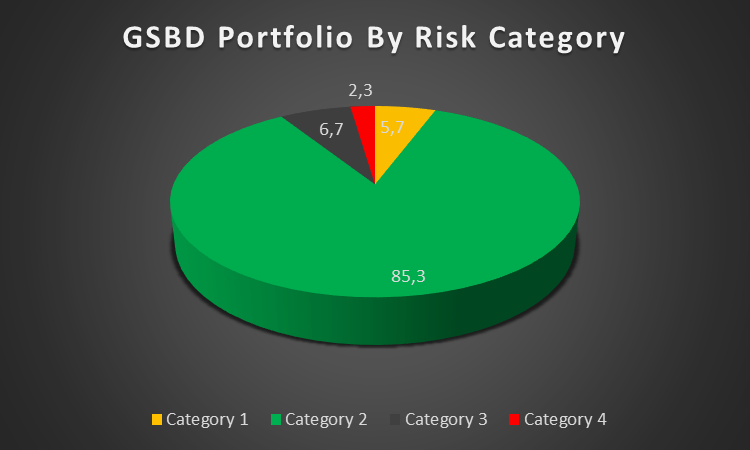

In GSBD's most recent earnings presentation , the BDC indicated that the percentage of its portfolio rated in category 3 has declined from 7.6% of its overall portfolio to 6.7% of its portfolio. While this may at first glance appear to be a welcome development this largely arose as a result of migration from category 3 to category 4 which presents an even greater risk of default. In terms of GSBD's internal risk rating category 4 suggests that the investment has experienced a significant rise in risk since its origination or acquisition. Typically, a majority or all of the debt covenants are violated, with payments being substantially overdue in this risk category. In these instances, there is a low expectation of full repayment, and the potential exists for a substantial loss of the initial cost basis upon exit.

GSBD Portfolio By Risk Category (%) (Author created based on company filings)

{kind=link}

While it is still important for investors to monitor the increase in the percentage of the higher-risk categories, these higher-risk investments still represent a relatively low percentage of its overall portfolio. It is also somewhat reassuring that there was no further migration from the lower risk categories (category 1 and 2) to the higher risk categories such as category 3.

The BDC also reported an increase in non-accruals with management noting that:

As of September 30, 2023, two new positions were placed on non-accrual and one portfolio company was removed from non-accrual during Q3. Investments on non-accrual status amounted to 2.3% and 4.2% of the total investment portfolio at fair value and amortized cost respectively. Subsequent to quarter-end, one additional name was placed on non-accrual status. The size of this position does not constitute a meaningful change to the percentage stated above."

These non-accruals further speak to the need to monitor credit quality closely. However, with an elevated percentage of the BDCs portfolio rated in risk categories 3 and 4, the increases in non-accruals were not entirely unexpected and do not affect the previously assigned buy rating. Nevertheless, further deterioration in credit quality continues to be a material risk to the buy rating and would deter many other investors.

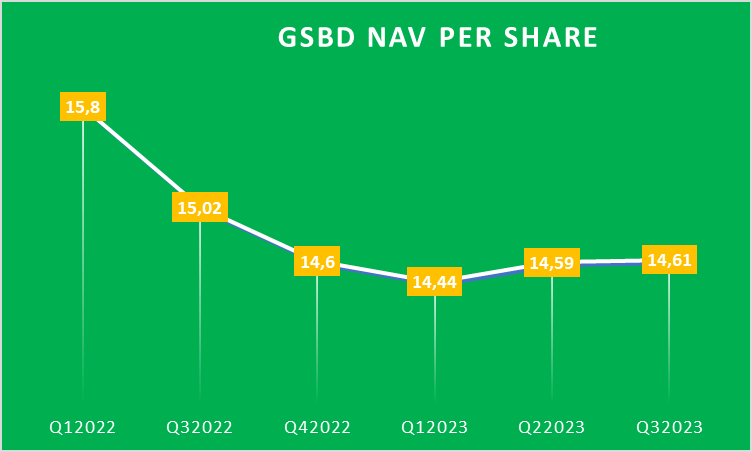

Goldman Sachs BDC has reported a rise in NAV per share of around $0.02 per share in the third quarter. While this does not represent a significant rise in NAV it again suggests that a discount to NAV would not be warranted for GSBD. The second consecutive quarterly increase in NAV reaffirms the buy rating I had previously assigned to GSBD.

{kind=link}

The Dividend and its Sustainability

I previously observed that GSBD could be ripe for a special dividend given the high net investment income ((NII)) coverage ratio the BDC has continued to report. In its previous earnings call management observed that:

In terms of the special, we're taking a long-term view of how to manage our balance sheet accordingly, looking at what our spillover is with future run rates, and will be opportunistic to the extent that it makes sense from a shareholder perspective to potentially issue a special down the road, but something that we're evaluating and we'll continuously assess and what makes the best sense for the balance sheet and shareholders."

This makes it clear that the special is also dependent on broader balance sheet considerations. The recent rise in NAV along with the continued rise in NII is further supportive of my previous argument in favor of a special dividend. However, the previously mentioned rise in NAV was largely driven by excess NII not paid as a dividend which suggests that it may be some time yet before a special dividend is paid. That being said, I remain of the view that GSBD is ripe for the payment of a special dividend within the next few quarters.

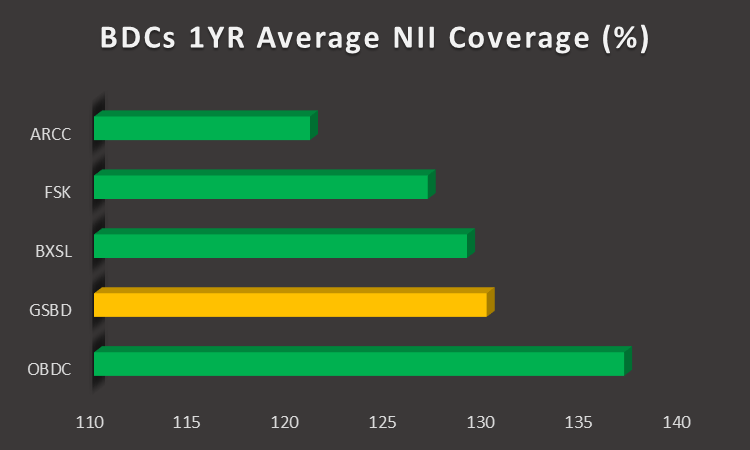

The BDC reported adjusted NII per share of $0.64 which represents a coverage ratio of 142% of its $0.45 per share quarterly dividend. When the asset acquisition accounting benefit is included the BDCs dividend coverage ratio rises to almost 149% for the third quarter of 2023. Its dividend has also continuously been well covered throughout the year with its 1-year average dividend coverage ratio currently sitting around 130%.

{kind=link}

This makes it clear that the dividend continues to be well covered by NII and a dividend cut remains highly unlikely. Should the dividend coverage ratio continue to rise the BDC may also need to increase the dividend or pay a special dividend to avoid running afoul of the regulations pertaining to its status as a BDC which requires it to distribute 90% of profits to investors.

Valuation

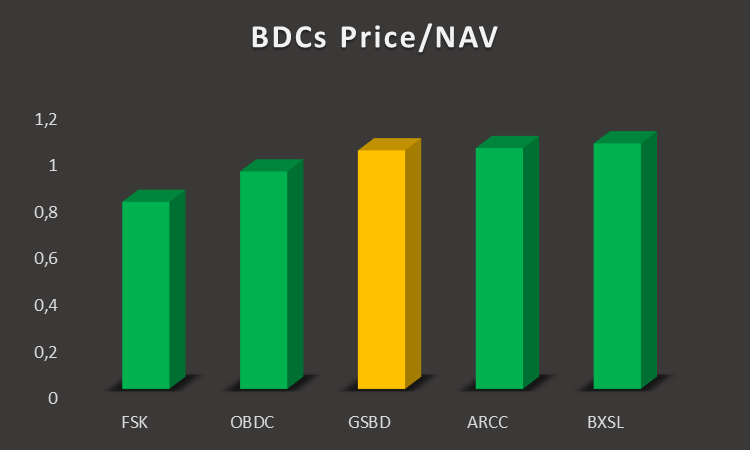

GSBD currently trades at a slight premium to NAV of less than 1%. This is right around the middle of the pack of the major BDCs considered in the peer comp chart below. It also remains below the BDC's 3-year average premium to NAV of around 11%. This suggests an upside potential of around 10% to reach its historic average premium to NAV.

{kind=link}

However, the stock might not rerate immediately as some market participants might be interested in monitoring the sustainability of NAV increases beyond NII retention. At present, I believe the stock is trading close to fair value given the elevated risks in its portfolio. However, the potential upside of a dividend increase and/or a special dividend is difficult to factor into a valuation but suffice it to say this would likely be received positively by the market.

Conclusion

My earlier buy rating on GSBD is reinforced by the company's second consecutive quarter of NAV growth, addressing concerns about its historical decline. The shift in portfolio holdings towards higher-risk categories 3 and 4 raises some caution, but the lack of further migration into category 3 is a positive sign. The increase in non-accruals is also noted and reflects the need to closely monitor credit quality, although it does not alter the previously assigned buy rating.

The rise in NAV, though modest, supports the argument against a discount to NAV for GSBD and a gradual rerating of the stock closer to historic levels. The potential for a special dividend remains plausible, given the continued high NII coverage ratio. The adjusted NII per share and dividend coverage ratios reinforce the sustainability of the dividend, making a cut unlikely.

For further details see:

Goldman Sachs BDC: Still A Buy