PKG - Good Greif: Why This Company Deserves Your Attention

Summary

- Greif is an undervalued but well-run company with strong execution.

- The company is executing a $150 million buyback.

- Management understands that the stock is undervalued and wants to deliver shareholder value to bring it to industry-average levels.

Not Exactly Dunder Mifflin. But Kind Of

When you read the works of some of the all-time great investors, you notice a consistent theme: many of them have preferences for companies that you might consider, well, boring . Peter Lynch once wrote to the effect that sometimes a company with a name that simply sounded boring was enough to get him to want to learn more. As these investing greats tell it, companies that lack flash are often under-covered by Wall Street and as such can present great investment opportunities for diligent investors.

Greif (GEF) (pronounced Gry-ef), is one of those companies, in our opinion.

Founded in 1877, Greif is a world leader in industrial packaging and paper products. The company operates in two main business segments--Global Industrial Packaging ((GIP)), and Paper Packaging & Services ((PPS)). Interestingly, the company has somewhat of a hidden asset in third unit--Land Management. This unit owns about 300,000 acres of timberland that the company is likely to sell off in the near future, which would generate a significant amount of cash.

The packaging and container industry is at a bit of a crossroads overall, with two competing interests both driving and constraining growth. On the one hand, the continued growth of e-commerce is the main secular driver of cardboard and packaging demand, while consumer demands for more eco-friendly packaging solutions force companies into fresh capital expenditure cycles to meet those requirements.

Greif, we believe, is well positioned to compete in the industry, and undervalued to boot. We believe that the current stock price levels are very much out of line with the intrinsic value of the stock, presenting a margin of safety that investors shouldn't ignore.

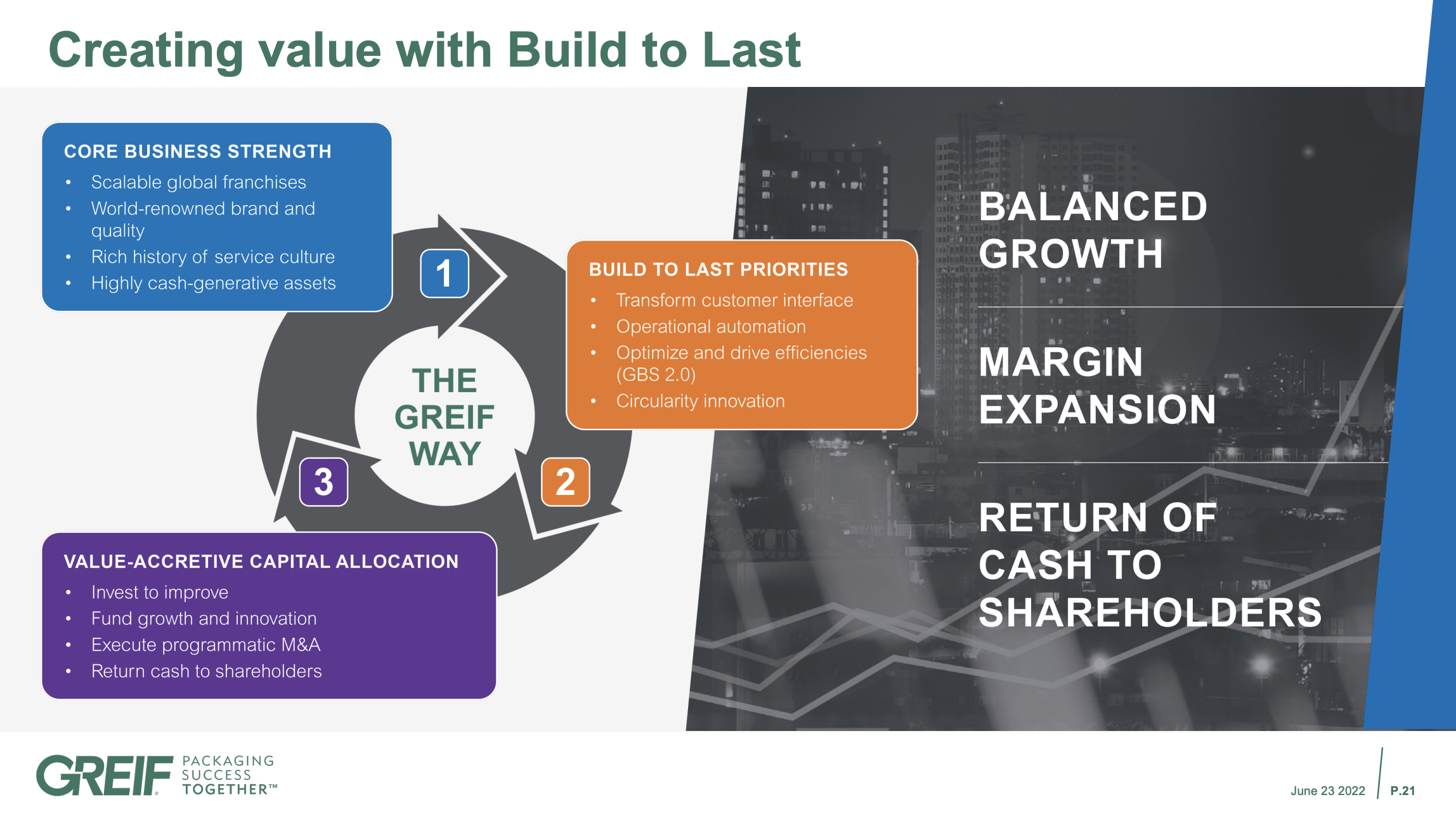

New Management, New Initiatives

For just a moment we'd like to focus on some of the areas the company drew attention to at its investor day in the Summer of 2022. In the last year Greif elevated Ole Rosgaard to the CEO role. In the past year the company has embarked upon a new strategy called Build to Last. Build to Last is a comprehensive overhaul of the way the company does business.

{kind=link}

This strategy is in the early innings of its execution, and we believe that management has the ability to execute to the upside. After all, Rosgaard is not an outsider--he has a history of working inside the company that we believe is a competitive advantage. He appears to be intent on making his mark within the company and on delivering the shareholders the value that the management team expressly believes they deserve (more on that later).

{kind=link}

Greif management believes there are several secular tailwinds that will soon accelerate company growth, even if the near term (6-12 month) outlook may be somewhat depressed.

First, Greif highlights that its nearness to its customers represents an under-valued characteristic. Paddy Mullaney, the chief of Greif's largest division, Global Industrial Packaging, had this to say:

[Y]ou can have a good network, you can have good processes, you can have good products, but you've got to know your customers' business. So, the third core pillar of why customers would partner with Greif is because we are very close to their business. We understand their requirements, but we also understand their customers' requirements. And where that plays a role, especially in relation to how we innovate going forward, so if we can partner with customers and we do, and we'll talk a little bit more about innovation, we want to make sure that we understand their markets. So where we can, we will innovate and develop products and processes.

In other words, what seems like simple packaging to you and I is, of course, not that simple to those in the industry, and Greif makes it a special point of emphasis to remain close to customer's operations to ensure that nothing goes awry in the critical final mile of product delivery where a faulty piece of packaging can result in a lost sale for the customer.

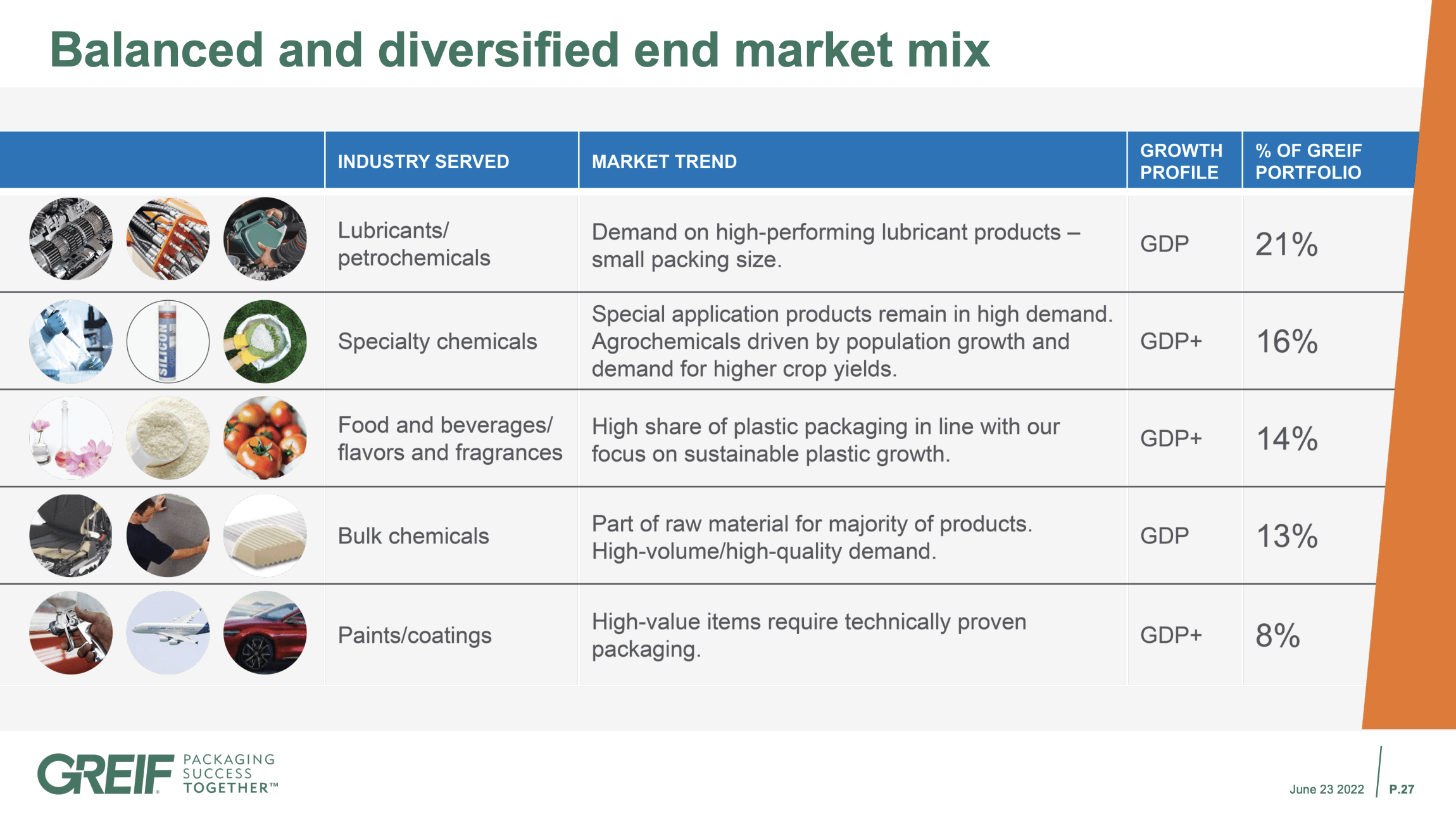

At this point we should make it clear we are not talking about an Amazon package delivery--although Greif does participate in that--but rather business-to-business deliveries. Take a look at Greif's GIP customer mix.

{kind=link}

These packagings are highly specific and require technical know-how that make Greif an embedded part of customer's supply chains. A glance at the slide shows that three of the five areas in which GIP concentrates grow at a rate above general GDP--specialty chemicals, food and beverage flavors and fragrances, and paints/coatings.

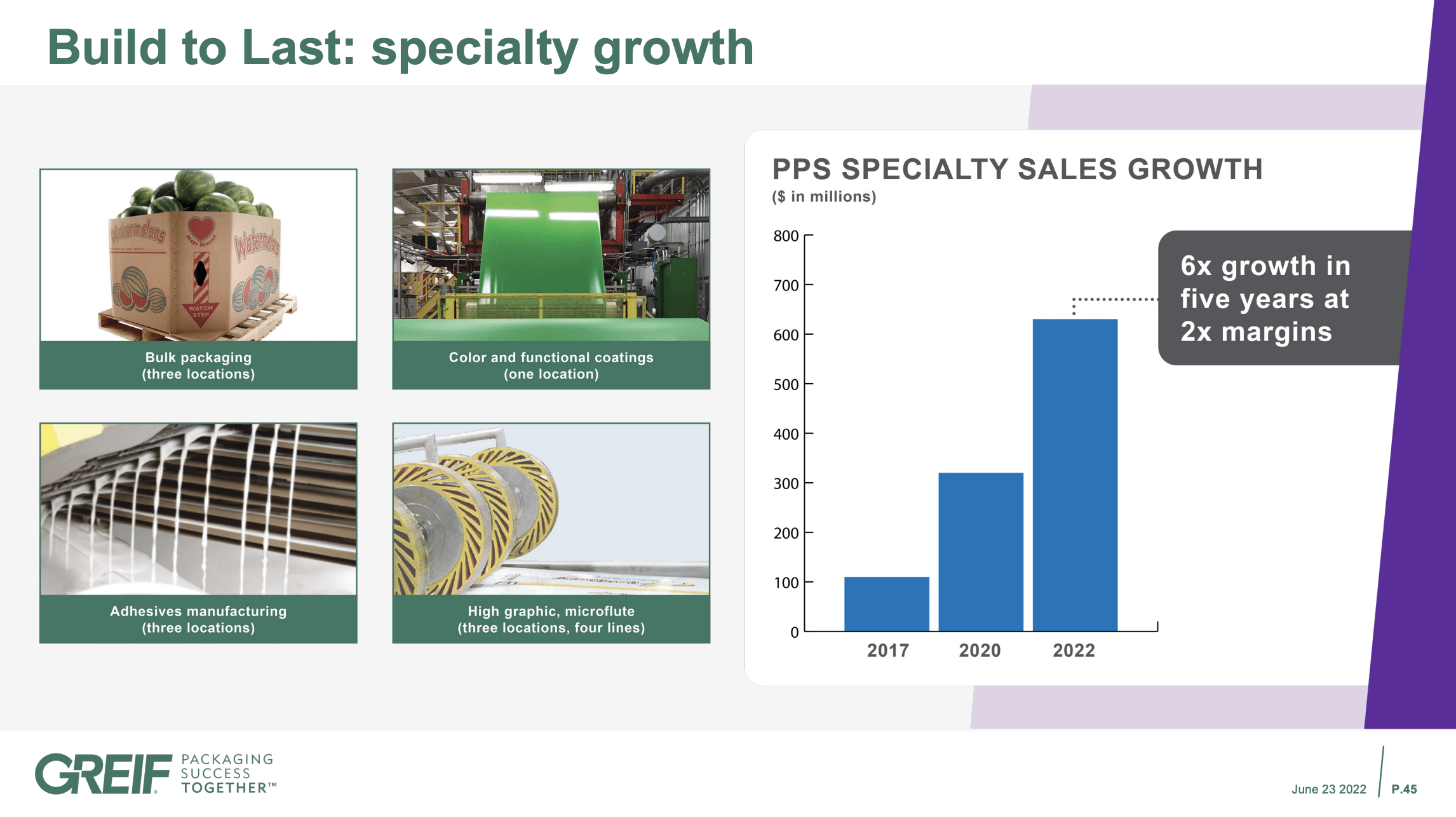

In the company's smaller division, Paper Packaging & Services ((PPS)), there is room for growth as well.

{kind=link}

In the last five years the company has seen 6x growth in its specialty PPS areas, which includes adhesives and bulk packaging. The adhesives segment in particular is a good example of the company's ability to execute a successful M&A strategy as well. The adhesives business is a bolt-on acquisition from Caraustar, which Greif purchased. In addition to being something that the company can sell, the adhesives purchased in the acquisition are also the adhesives used by the company in paper and tubing operations, creating an effective cost synergy for the company.

A Question of Value

Greif's executive leadership is well aware of the lagging value the stock market has assigned the company.

{kind=link}

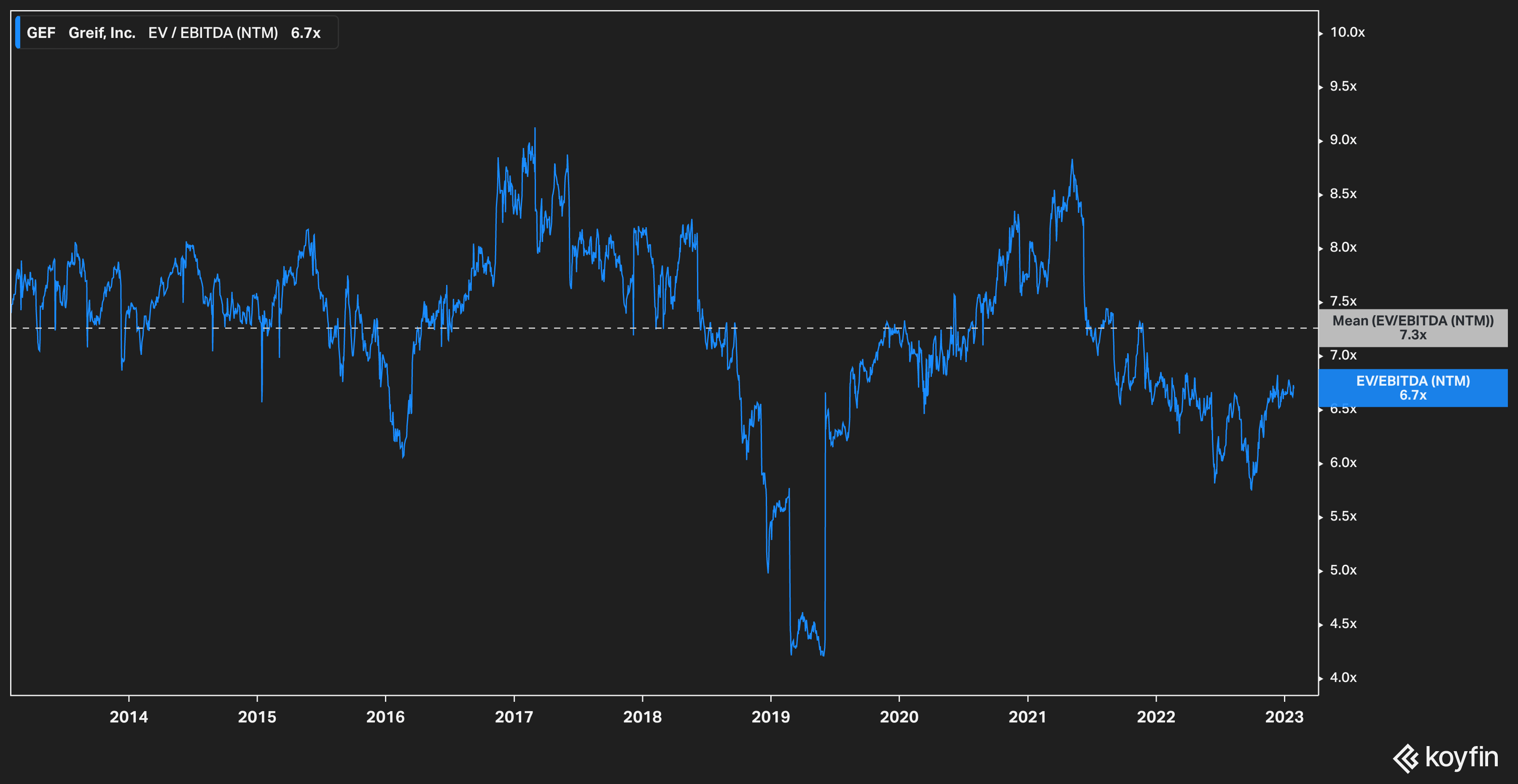

Greif has a 10-year forward EV/EBITDA average of 7.3x, compared to its current level of 6.7x. This is a significant discount to competitors.

{kind=link}

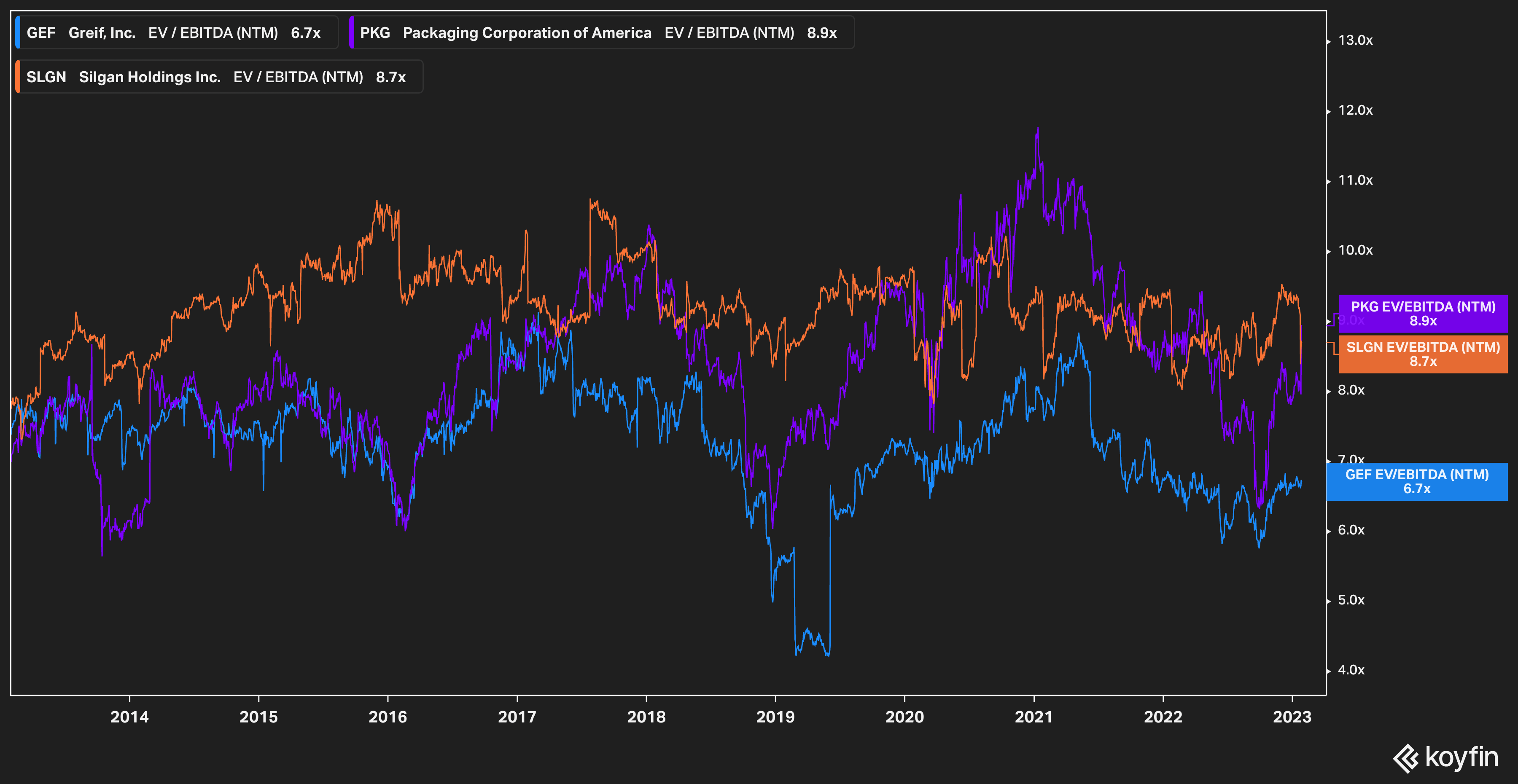

Two of Greif's leading competitors, Silgan Holdings ( SLGN ) and Packaging Corporation of America ( PKG ) trade--and have traded--at consistently higher multiples.

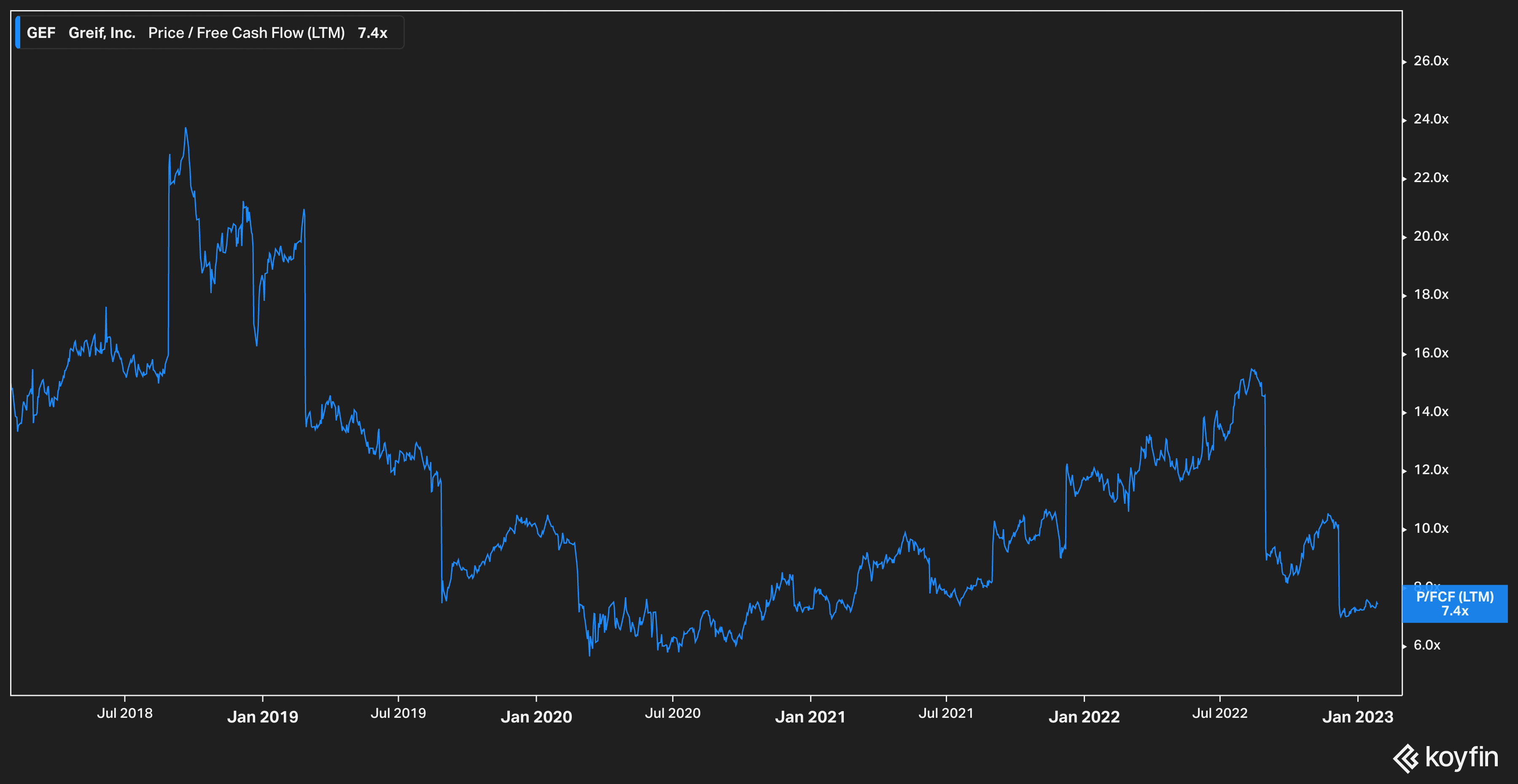

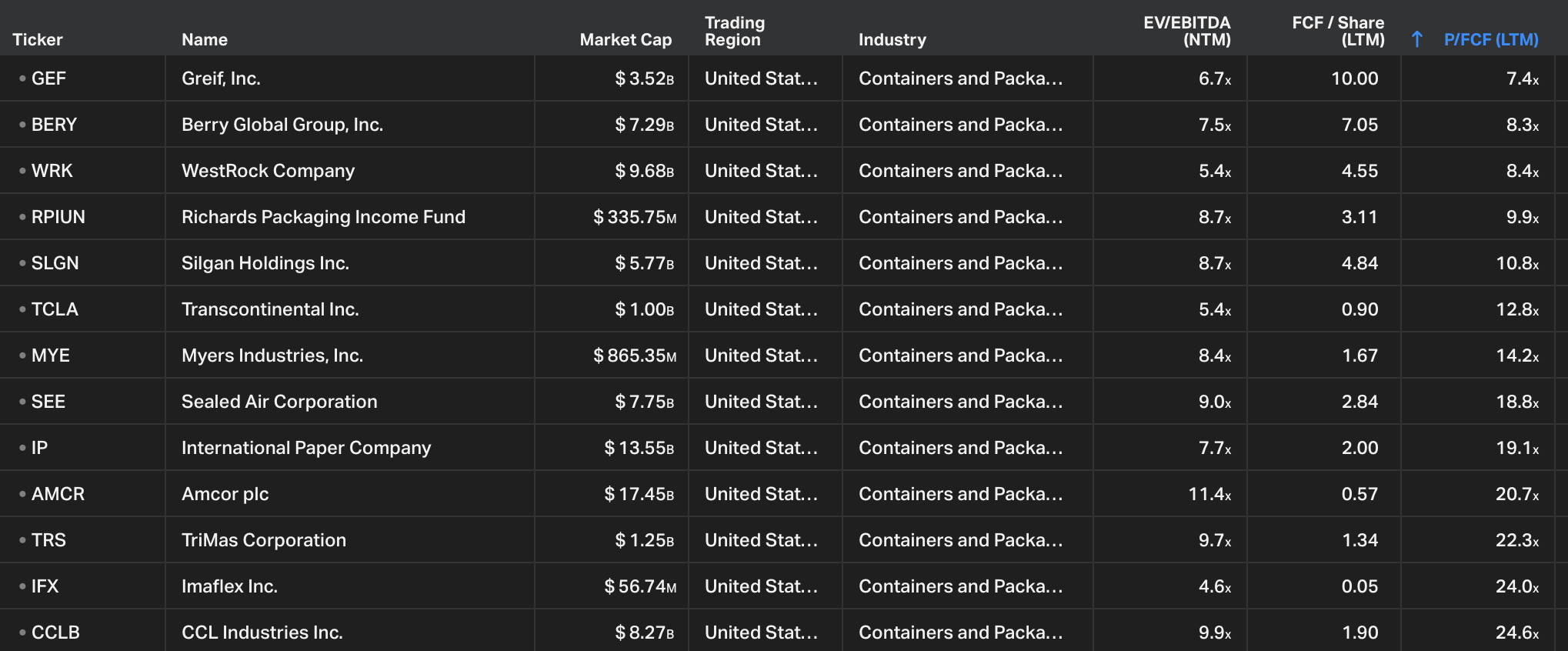

This is not because Greif runs an inefficient operation. In fact, Greif is historically cheap, trading at 7.4x price to free cash flow multiple, close to a five-year low.

{kind=link}

A 7.4x free cash flow per share (currently $10 per share) multiple is very low. The multiple is in fact the lowest multiple among other companies in the industry.

{kind=link}

Add to the low valuation based on price/FCF and EV/EBITDA the fact that the company is actively repurchasing shares, with a $150 million authorization from the company's board.

So What's the Market's Gripe With Greif?

So, what is the reason for this low valuation? We believe the answer is twofold. First, the company is executing a transition of leadership with a new growth strategy. Using a mix of process efficiencies and bolt-on acquisitions, the company is making smart moves to improve cash flow and return value to shareholders.

Unfortunately, when you run a... well, boring business like paper manufacturing, sometimes it can take a while for the market to notice.

Additionally, Greif has something that you might expect from a silicon valley software company, but not a 100+ year old paper concern--a dual stock class.

Greif trades under Class A (GEF.A) and Class B (GEF.B). Class A shares are non-voting, while Class B shares are controlled by a handful of families with long-running ties to the company. Importantly, Class B shares are not supershares--they do not possess multiple votes like those possessed by Mark Zuckerberg at Meta ( META )--but each share gets one vote. Most importantly, they can be bought and sold on the public market and generally trade at only a slight premium to the Class A shares.

Company leadership is not unaware of the difficulty posed to investors by two stock classes. The question is frequently asked on quarterly calls and was the subject of analyst questions on the company's investor day. While CEO Ole Rosgaard says that the board won't rule anything out--including the eventual elimination of the dual-class share structure to realize shareholder value--they believe that there are many more levers to pull that could generate the same if not more value.

The Bottom Line

We believe that Greif's low valuation against its peers, strong free cash flow generating ability, strong operational execution, and management with shareholder value being top of mind makes the company a very attractive idea for investors.

Using an industry average forward P/E of around 15x, we estimate that a fair price for Greif shares to be around $96 based on FY24's estimated earnings, a 29% upside from today's levels.

Thank you for reading our article.

For further details see:

Good Greif: Why This Company Deserves Your Attention