BESIY - Good Times Just Getting Started At BE Semiconductor Industries

2023-06-06 05:51:45 ET

Summary

- BE Semiconductor Industries (BESI) is a Dutch-based semiconductor equipment supplier with a strong balance sheet, net cash positive, and pays a decent dividend.

- BESI is a leader in Hybrid Bonding technology, which is expected to boost chip performance and reduce size, and has a 1-2 year head start in the space.

- Despite a massive run-up in share price, BESI still has 25% upside potential and offers an attractive income stream, making it a buy for investors looking for growth and income in the semiconductor sector.

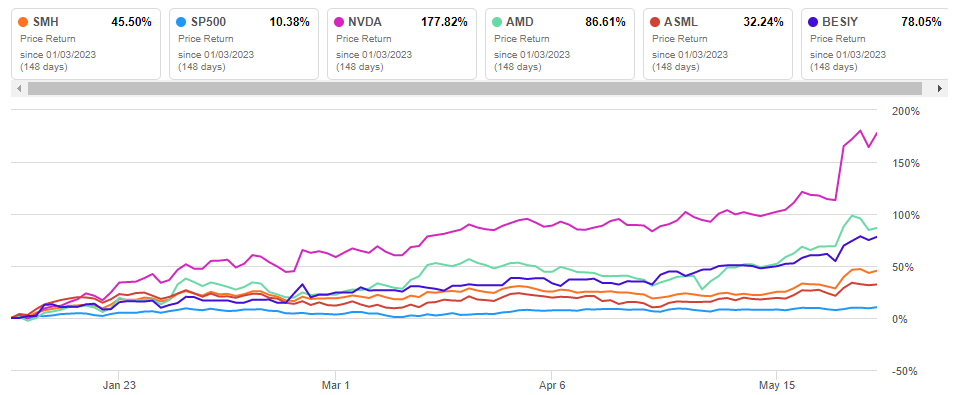

Semiconductors are the flavour of the day at the moment, with the Artificial Intelligence ((AI)) rhetoric boosting the space considerably. This coupled with a more upbeat tone around the future at recent results has culminated in a massive rise in share prices year to date, which has taken the VanEck Semiconductor ETF ( SMH ) to within 10% of its all-time high. This of course has caused many to rightly ask whether we're in bubble territory here. I don't know to be honest, but some caution is warranted, and I think one can no longer blanket buy in the space, the easy money has been made and it will certainly pay to be more selective here before jumping in.

This is a cyclical industry so one needs to be careful how you approach it. Recent results out of the semiconductor space recently are showing signs that the cycle may be bottoming and infers that spending in the sector is about to ramp up considerably. This after a boom in 2020/21 was followed by a swift and sharp reversal in 2022 as excess inventories, geopolitical tensions and rapidly shifting consumption patterns spurred a massive decline in the sector.

Mega cap Nvidia ( NVDA ) and others, like Advanced Micro Devices ( AMD ) for example have led the space higher resulting in market crushing returns YTD. Today however I want to talk about another stock. It has been a stellar performer since listing with consistent returns, it's also less followed by the market (and US retail investors in particular) for what I think are two reasons, firstly it's a Dutch based company and secondly, when it comes to semi exposure with a Dutch tilt, THE behemoth in the room is the mighty ASML Holding (ASML). Flying under the radar however is BE Semiconductor Industries ((BESI)) (BESIY). BESI gets limited airtime as a result, but I think that's a mistake and this is why.

Van Eck Semit ETF vs SPX vs NVDA vs AMD vs ASML vs BESI YTD (Seeking Alpha)

{kind=link}

Who are BE Semiconductor Industries

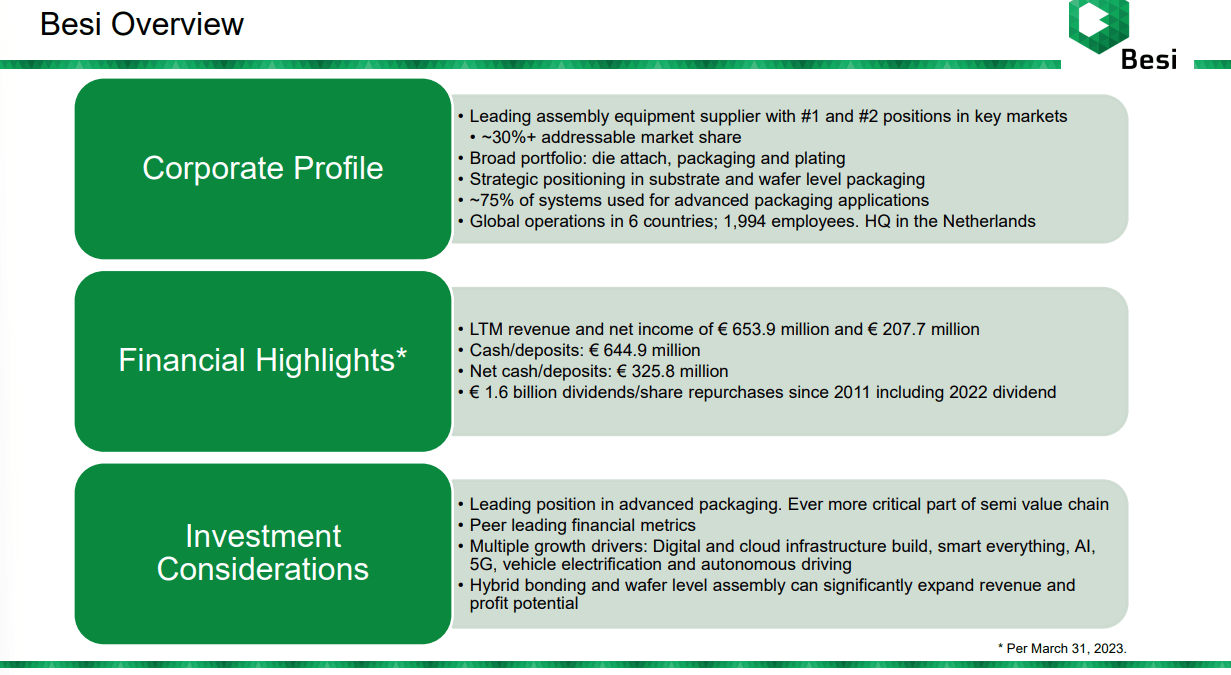

BESI is an assembly equipment supplier. They manufacture and distribute semiconductor equipment for both the Semiconductor and the Electronics industries. It plays a vital role in connecting the semiconductor/chip/die to other electronic components whilst protecting the chip from the external environment at the same time. The company has three major divisions; Die (Die is another word for a chip) attach, packaging & plating systems and it holds leading positions in its key markets. This is a business flying under many radars and yet plays an integral role in the industry it serves. It also has a solid balance sheet, is net cash positive, buys back shares and even pays a decent dividend. There's a lot to like here and things are about to get better in my view.

BESI Company Overview (Company Presentation)

{kind=link}

Not only does BESI have a large catalyst looming which we'll get to next but even before this it's been a business that has generated incredible returns and performance versus its broad peer group, and it screens favorably for stocks in the growth space with superior operating margins and a lower valuation then ASML for example.

Performance/Valuation vs peers (CapIQ and Morgan Stanley)

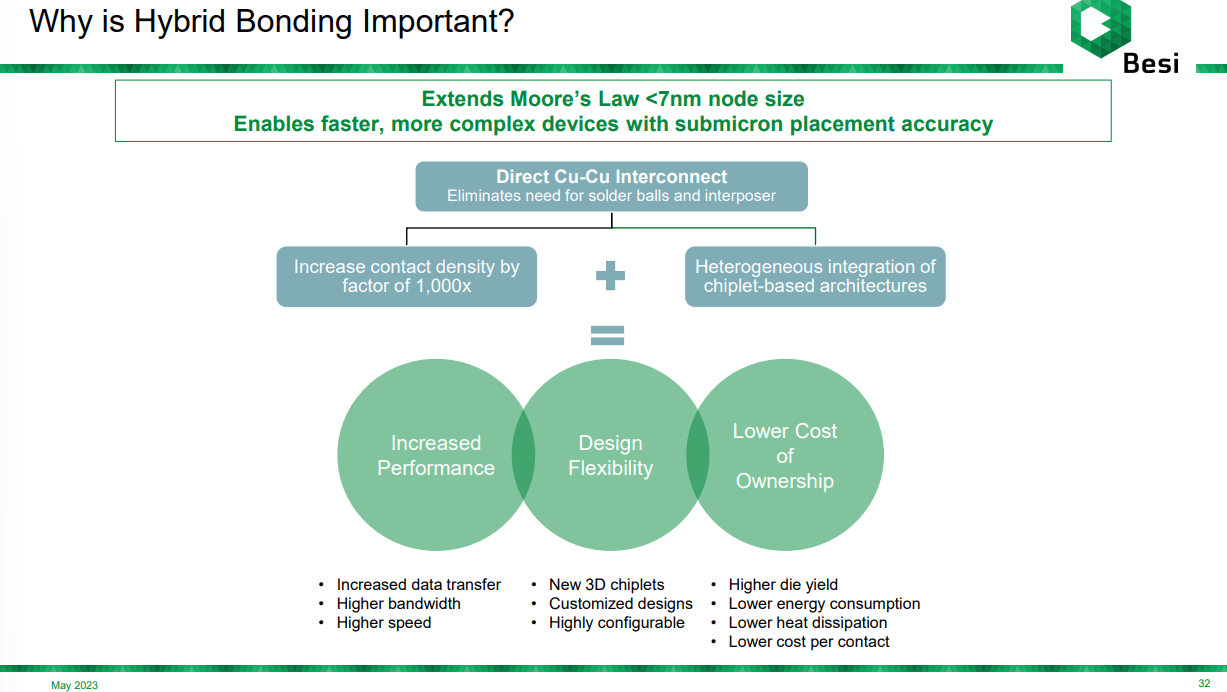

Hybrid Bonding is a game changer and BESI is a dominant first mover

Hybrid bonding is a form of advanced packaging which boosts performance for chips and reduces their size. What it does is it allows for less space by removing the need for bumps to connect chips and replaces them with small copper to copper connections instead. The result is that the sum of the whole is greater than its constituent parts. You get superior interconnect and with it, higher memory density. You also get expanded bandwidth, more power and improved speed and efficiency. It's the epitome of Moore's law where you basically fit more and more ability into an ever-smaller chip pack.

To put this into some sort of context the current go to technology, Thermo-Compression Bonding ((TCB)) has an interconnect density of 40 nm with the ability to go as low as seven. Hybrid bonding has the potential to reduce it to 1 nm.

Importance of Hybrid Bonding (Company presentation)

{kind=link}

To the industry this is a game changer, once again it reduces the size of the chips we use whilst boosting their ability and opens the door to a host of new opportunities and innovation. My understanding of this too is that this is new in that the technology is still in initial stages of adoption which means that the ramp up has significant potential. The benefits of this technology can be expanded as follows.

- Hybrid bonding is cheaper than the previous generation tool and its offers spacing improvement of ten times the size. i.e. cheaper and with significantly larger capacity.

- TCB technology cannot be used below 7nm which opens the opportunity for Hybrid Bonding to replace that entire market over time.

- The scale of the market is large. BESI currently targets 250 Hybrid Bonding tools by 2026 which individually would be less than 35% of wafer output below 7nm and just 2% of the market for memory players.

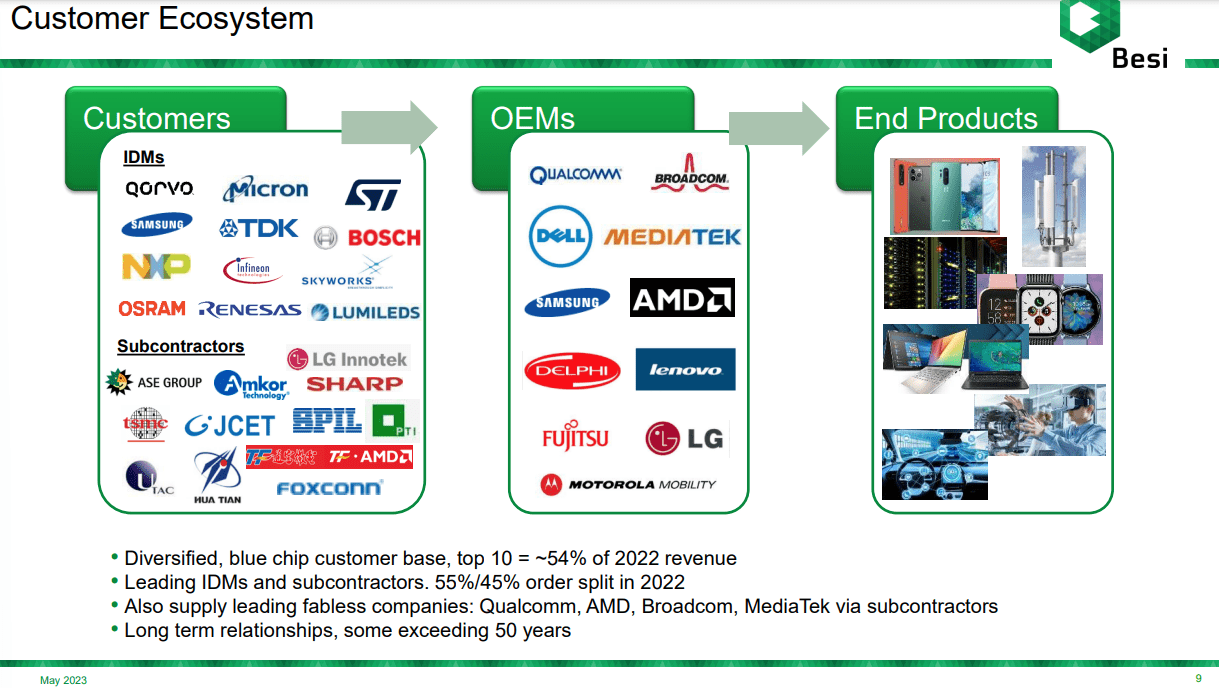

I'd point you to this presentation BESI did in December 2021 on Hybrid Bonding and its impact. This outlines the size and importance of the technology and intimates that BESI has the lead when it comes to Hybrid Bonding systems and technology. too and have already signed deals with both Taiwan Semiconductor ( TSM ) and Intel (INTC). As capacity grows, they have deals in the pipeline with the likes of Samsung ( SSNLF ) and Micron ( MU ) too which expands the growth runway with some 'visibility'. The client list is large and goes beyond these names of course and the end use of these chips is vast as well as can be seen in the following slide.

Customer list and ecosystem (Company Presentation)

{kind=link}

Why now

BESI is not a Mega cap stock, this is in relative terms a small company with a market cap of 'just' $9bn which vs fellow Dutch company ASML at $288bn, and of course other large global names such as NVDA $985bn, Taiwan Semiconductor $466bn, Broadcom ( AVGO ) $330bn, AMD $192bn, & QUALCOMM ( QCOM ) $129bn, etc. puts its size into perspective.

It also has revenues which at recent results came in at $774m in 2022 which again vs these other companies are 'small'. What we're after here though is the opportunity going forward and Hybrid bonding which is where they have a leadership position is set to explode higher in my opinion.

As I suggested above at current targeted capacity of 250 Bonding tools by 2026 the company would be servicing less than 35% of wafer output for logic players and under 2% for memory players. Yet these 250 tools equate to around $538m in revenue by 2026. This would be a fraction of the total market and even if competitors' step in its large enough for multiple players to succeed.

BESI has a clear advantage in that it is both the leader and the first mover in the space which means it can grab share faster than others during this initial window of opportunity. Estimates I've seen mention that BESI has a 1-2-year head start in the space which is something I'd expect them to take full advantage of.

As a cyclical business, the ramp up here will help buffer the broader company performance which might suffer from the current macro environment and help the business perform better during a potential recession too. This in turn should be followed by a spurt in growth as underlying markets recover providing added momentum to the business into 2024 and beyond. This may help the companies rating in the market as we traverse the next 12-18 months. BESI has survived cycles before and although not immune to them has continually grown post cycle bottoms and come out stronger every time. I'd expect nothing less than that this time around especially as Hybrid Bonding technology takes off.

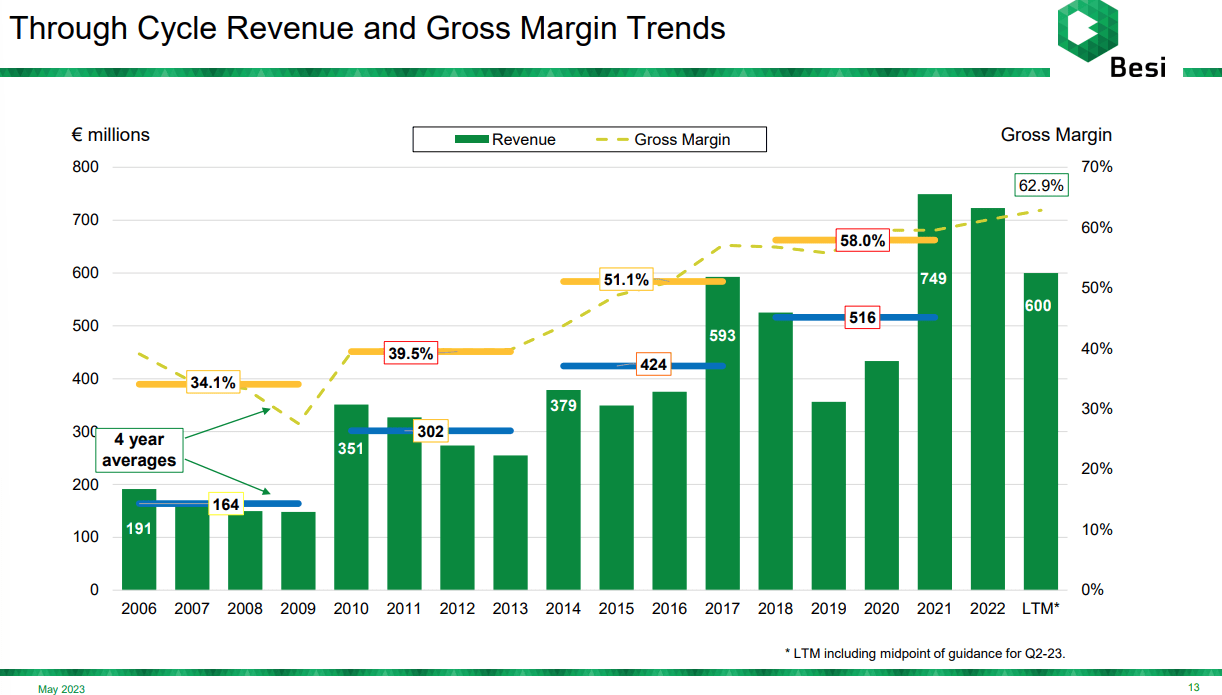

Revenues and margins through the cycle (Company Presentation)

{kind=link}

As you can see above coming out of the great recession each and every cycle has been met with higher base revenue than the last and gross margins have continued to rise as the company has grown. Gross Margins are incredible here and came in at 64.2% in Q1 23. Operating Margins are also excellent at 38.9% for the quarter. The first quarter results out on 26 April 2023 showed the cyclicity of the business with revenues down 3% quarter on quarter (qoq) and 34% year on year (yoy). This was as a result of lower orders in mobile and computing. Better mix though coupled with some forex moves and cost cutting pushed gross margins up to the 64.2% level.

Net income and margins fell too primarily because of stock based compensation qoq and on a yoy basis this was exacerbated by higher R&D spending and general industry weakness. The company maintains a net cash balance of $370m at end of quarter. The dividend policy operates in a range of 40-100% of net income per annum and as at last year shareholders earned €2.85 in dividends which represented a 93% pay-out ratio, this is consistent with the company's recent rate of payment since 2016 which has averaged 94%. Since 2016 the dividend pay-outs have totalled €14.60 per share.

The outlook for the next 3 months is for a qoq improvement of 20% at the midpoint as evidence of industry pick up and traction in Hybrid Bonding gains momentum.

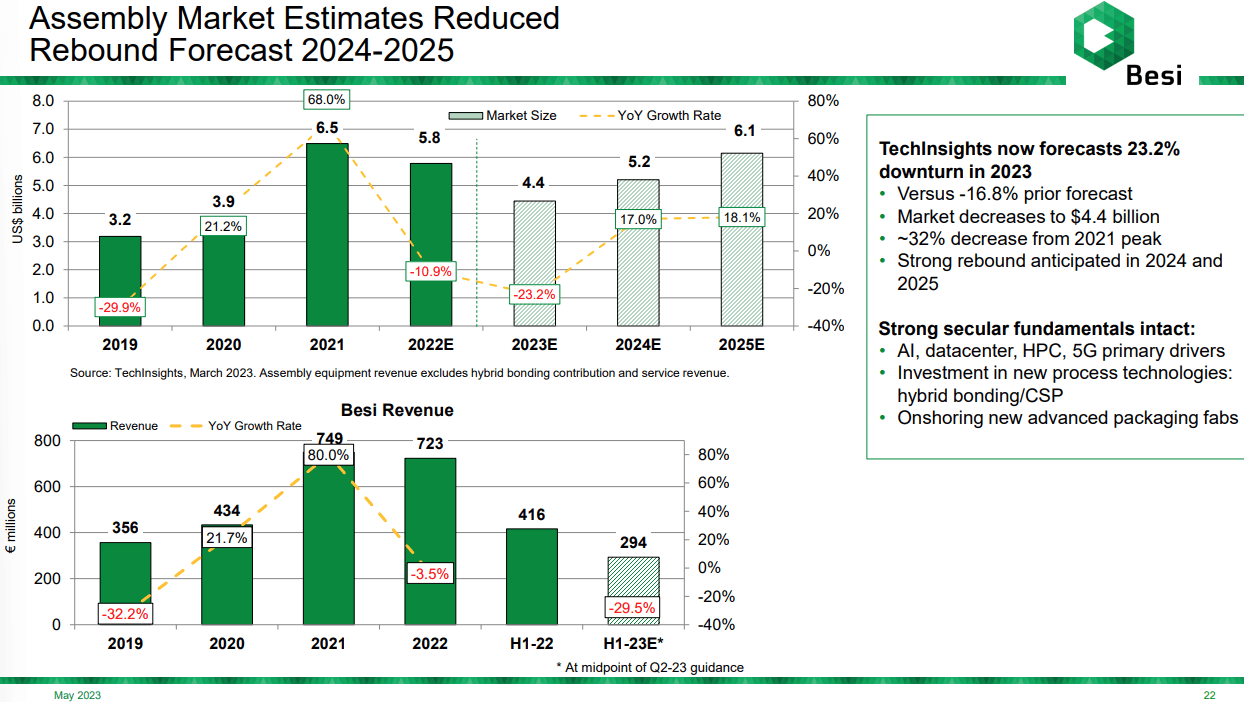

Looking forward the company has a goal to reach revenues north of €1bn by 2025. Due to the cyclical nature of the sector it's hard to model this in a straight line as both revenues and net income tends to be lumpy but within a rising trend. However, if we have in fact reached the bottom of the cycle and a new cycle spurred by AI and Hybrid Bonding which is supplemented by continued 5G and datacentre demand, then 2024 and 2025 could be setting us up for a nice rebound. One can see below how revenue bounces around when cycles turn, and the upswings can be quite violent.

Assembly market cycle and recovery forecast (Company Presentation)

{kind=link}

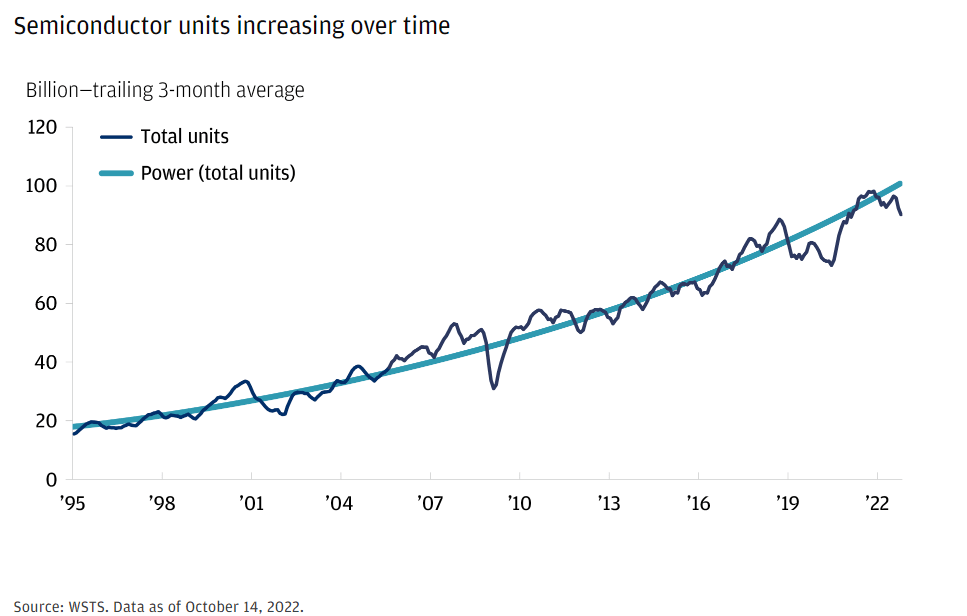

Structurally however even within these cycles the trend remains clear, semiconductor usage is growing rapidly off an ever-larger base and even as the World Semiconductor trade statistics group ((WSTS)) expects growth of just 4.1% in 2023 (vs 4.4% in 2022 and 26.2% in 2021) growth is not negative. It's a base that's just getting larger and will continue to do so.

Long term Semiconductor usage/volumes (World Semiconductor trade statistics group.)

{kind=link}

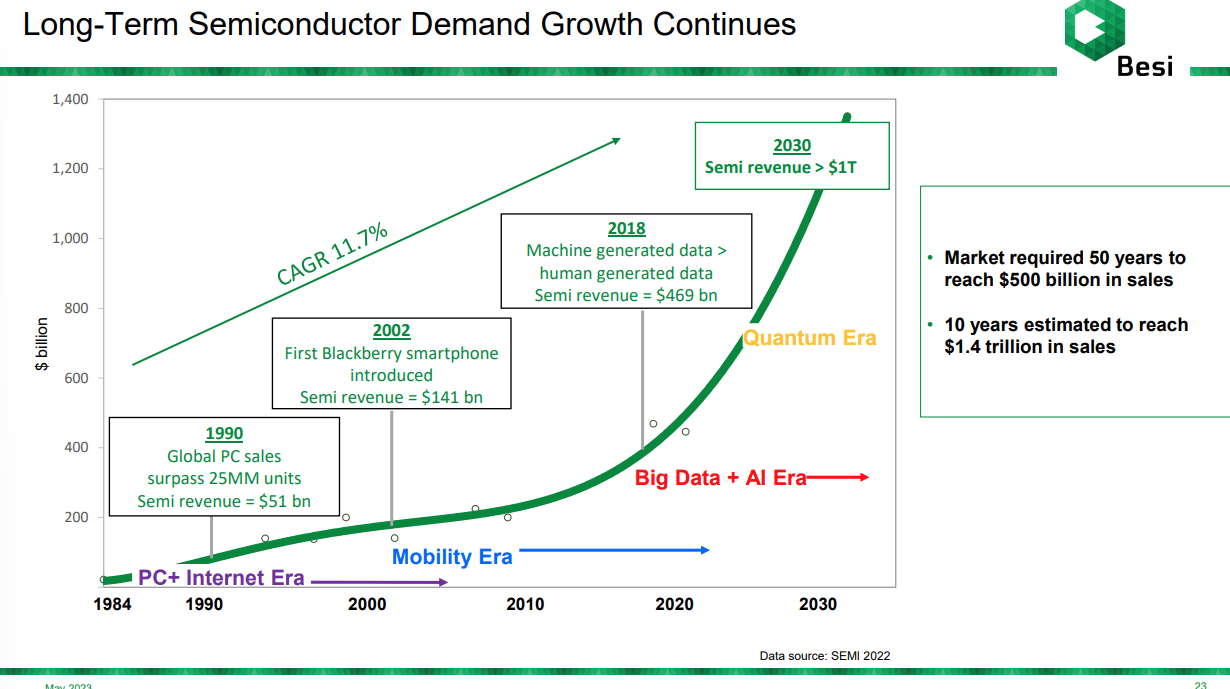

In fact, if you believe SEMI which is an industry group focused on the semiconductor space then explosive growth is on the horizon.

Exponential growth through tech cycles (Company Presentation)

{kind=link}

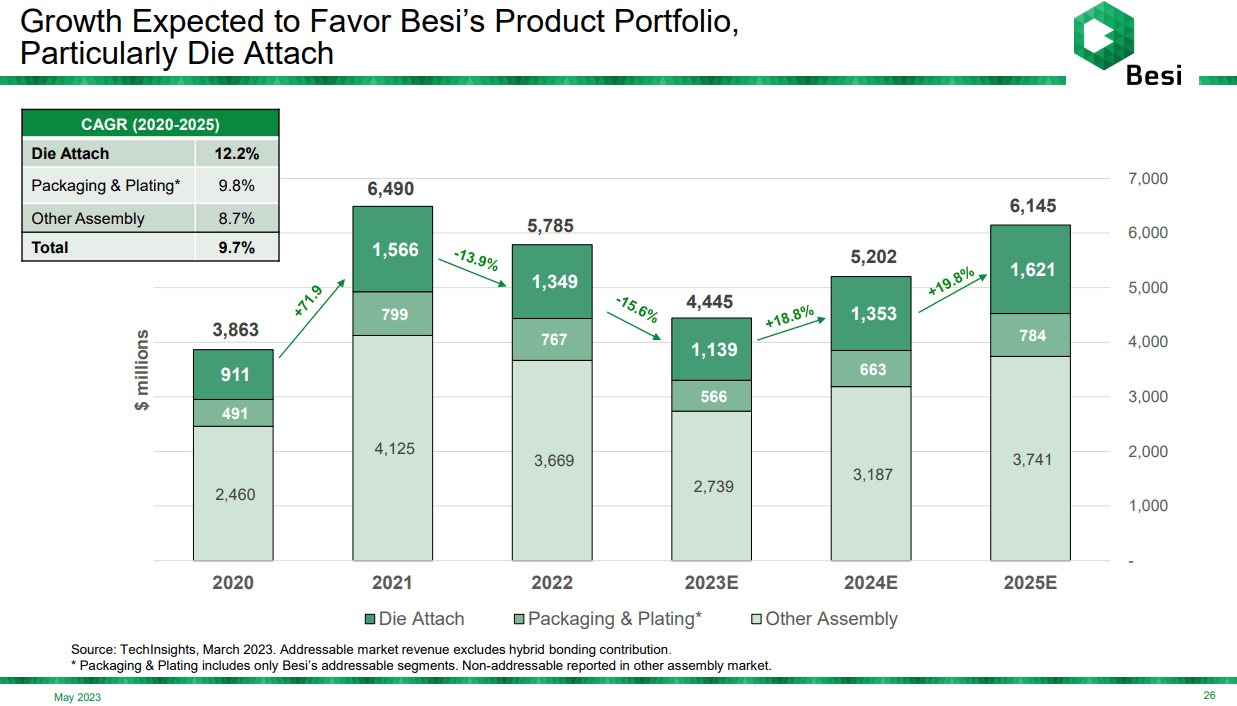

The share of the market that BESI operates in is also growing faster than the broader market over time, with Hybrid Bonding still excluded from this TechInsights projection we could be seriously underestimating the growth potential ahead of the company.

BESI product portfolio growth (Company Presentation)

{kind=link}

The problem of course is the price you pay for a ticket to the game, and whilst many wouldn't dare argue with the positive long-term dynamics that the industry is faced with, I'd be silly to conclude that after such an epic rally in the sector and in BESI YTD one shouldn't be a bit cautious.

What's it worth

I'd choose to value a company like BESI on a DCF basis because it allows you to smooth out the growth over a period and 'iron out' the lumpiness.

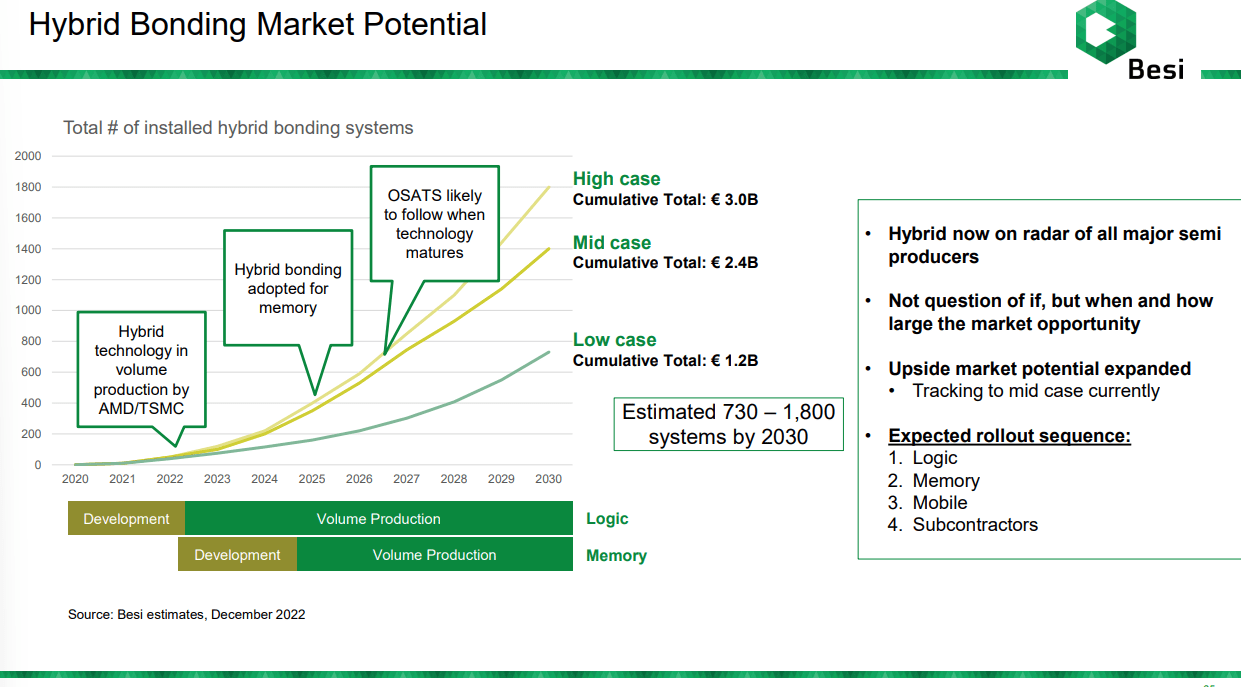

It seems to me that reading between the lines BESI has the clients to take up its capacity of 250 Hybrid Bonding Tools. In fact, they're busy growing capacity as we speak. According to the company thirty-five units were delivered to date since Q4 2021. Twenty-Eight Units were shipped in 2022 alone and since Q3 2022 14 new orders were received. As they scale, they are becoming more efficient too with times to delivery coming down. The company estimates that the market will require between 730 and 1800 systems by 2030 depending on how adoption evolves across the chain. So, we can punch a few numbers in and extrapolate some growth forecasts. To get to the 250 targets, they would need to deliver an average of fifty-five systems per annum which is quite a ramp from twenty-eight units last year. At the lower end of the range they estimate, (i.e.,730 units) there is substantial growth from this 250 base and at the higher end of 1800 unit's growth potential is extremely large.

Hybrid Bonding opportunity (Company Presentation)

{kind=link}

Essentially there's a runway for 20% per annum in revenue growth here and the company is forecasting Net Margins of 30-35% per annum. What this implies is that by 2027 we could see earnings in a range of €6.44 to €7.52 with a mid-point of €6.98. From a 2022 base of €2.90 this implies growth in EPS of 141% from 2022 - 2027 for a simple average of 28% per annum.

DCF valuation (Analyst assumptions)

At current exchange rates that equates to a USD target price of $137.60 vs current prices of $ 110.36 for upside potential of 25%. Should the dividend policy remain constant we could also look forward to dividends of around $7.00 per share at that point which equates to a dividend yield of over 6% at today's prices. Over and above this the company has been a consistent buyer of its own shares , offsetting dilution by stock-based compensation and convertible bonds in issue. Since the most recent buyback authorisation was announced for €300m in July 2022, just on €224m had been completed by the time of writing at an average price of below €64 per share (vs €102 currently.)

Conclusion

Despite its massive run up year to date due to all the excitement in the semiconductor space this year, it seems to me that BESI is still a stock that has attractive total return potential. This is a cyclical industry as we know so portfolio allocation is important here. Your exposure to the space should be dependent on both your risk profile and or your view of how 'hot' the semiconductor space is right now. This seems to be a company with a solid line of sight into future earnings growth and one could make a case for seeing great upside potential and an attractive income stream even at today's prices. You might decide to start with a smaller position depending on your risk profile and 'buy the dips' as the market ebbs and flows. However, if you're looking for a solid growth story with a decent underpin from an underfollowed gem in the semiconductor space, I think you could make a great start by adding a few BESI to your portfolio.

With 25% upside and a solid dividend underpin BESI is a BUY.

For further details see:

Good Times Just Getting Started At BE Semiconductor Industries